|

|

Good morning, and happy fall.

The investment markets have continued their outstanding performance so far this year. Large cap US stocks are up more than 16% this year. International developed markets stocks are up more than 21%, while emerging markets stocks are up 33%. Bonds have been slow and steady with a 3.4% return year-to-date.*

Open enrollment for Medicare runs Oct. 15 - Dec. 7. It's always a good idea to review your Medicare coverage and pricing, and especially your Part D drug coverage to make sure you're getting the lowest total cost for your prescriptions when you factor in premiums and co-pays.

Open enrollment for the health insurance marketplace policies runs from November 1 - Dec. 15. If you have one of these policies, reviewing your coverage is especially important this year because of the changing landscape.

The retiree social security cost-of-living adjustment was just announced for next year at 2%. This also applies to federal retirees in the FERs and CSRS programs.

We were thrilled to see Richard Thaler receive the Nobel Prize in economics because he's been the renegade economist who tries to explain how we

really make financial decisions, not just how economists think we

should make financial decisions.

We have some information on his work in the newsletter.

Please let us know of any suggestions for newsletter topics or questions in your financial world. Thanks for reading, and live well!

|

|

|

Richard Thaler: How We Make Financial Decisions

|

|

|

|

|

|

What to Do About the Equifax Data Breach

|

|

|

|

|

|

Average Investment Returns Aren't Common!

|

|

|

|

|

|

|

Third Quarter Investment Market Review Third Quarter Investment Market Review |

You may have joined many professional investors in feeling surprise at the bull market's continued progress in third quarter. And those who were "sure" we were due for a correction this year have missed out on truly phenomenal performance in stocks. In case we needed any reminders that the markets are impossible to predict, this year is just one more example. You may have joined many professional investors in feeling surprise at the bull market's continued progress in third quarter. And those who were "sure" we were due for a correction this year have missed out on truly phenomenal performance in stocks. In case we needed any reminders that the markets are impossible to predict, this year is just one more example.

A breakdown shows that just about everything gained at least modestly in value these last three months. The broad measure of US stocks, the Russell 3000, index was up 4.57% for the quarter and 13.91% this year through Sept. 30.

T

he S&P 500 index of large company stocks gained 4.48% for the quarter and is up 14.24% in calendar 2017.

Small companies as measured by the Russell 2000 Small-Cap Index are up 5.67% for the quarter and 10.94% this year.

As nice as the returns have been domestically, international stocks this year have been even kinder to investment portfolios. The broad-based MSCI EAFE index of companies in developed foreign economies gained 5.4% in the recent quarter, and is now up 19.96% in dollar terms for the first nine months of calendar 2017. Emerging markets as measured by the MSCI EM index were up 7.89% in third quarter and 27.78% year-to-date.

In the bond markets, you know the story: coupon rates on 10-year Treasury bonds have risen incrementally from 2.30% at this point three months ago to a roaring 2.33%. The Barclays aggregate bond index is up 3.4% for the year so far and 0.85% for this quarter.

One might imagine that the uncertainties around government policy and fundamental economic issues would spook investors, and if those weren't scary enough, there's the nuclear sabre rattling sound coming from North Korea. Hurricanes have disrupted economic activity in Houston and large swaths of Florida, while Puerto Rico lies in ruins. Yet the bull market sails on unperturbed.

How can this be? Because if you look past the headlines, the underlying fundamentals of our economy are still remarkably solid this deep into our long, slow economic expansion. Corporations reported a better-than-expected second quarter earnings season, with adjusted pretax profits reaching an annualized $2.12 trillion-which means that American business is still on sound footing. Unemployment continues to trend slowly downward and wages even more slowly upward. The economy as a whole grew at a 3.1% annualized rate in the second quarter, which is at least a percentage point higher than the recent averages and marks the fastest quarterly growth in two years. There is hope that the new tax package will prove as business-friendly as the Trump Administration is promising.

Economists tell us that the multiple whack of hurricane damage will slow down economic growth figures for the third quarter, although the building boom fueled by the destruction will mitigate that somewhat. There are no economic indicators that would signal a recession on the near horizon, and one of the potential panic triggers-a Federal Reserve Board decision to recklessly raise interest rates-seems unlikely given the Fed's extremely cautious approach so far.

And fourth quarters have historically been kind to investors-much kinder than third quarters.

There are still potential speed-bumps down the road. There are concerns about the healthcare marketplace. There's the possibility of multiple trade wars with America's major trading partners: the NAFTA members Canada and Mexico, and with China. Tight immigration rules could lead to limited labor supplies.

But it's hard to be pessimistic when your portfolio seems to grow incrementally every quarter. The current 12-year stretch of economic growth below 3% a year is America's longest on record. But if the U.S. charts a prudent economic course, it's possible that the current expansion could at least set new records for longevity. This current expansion just turned 99 months old. The all-time record is 120 months, from 1991 to 2001. We may have longer to wait for the next great buying opportunity in stocks. In the meantime, it makes sense to keep your portfolio rebalanced to its target to continue benefiting from the bull market while still avoiding excessive risk.

If you found this information and would like a more in-depth analysis of the third quarter investment markets, including performance of the small and value premiums, please see the full report on our website.

Article adapted with permission of Financial Columnist Bob Veres.

Source of investment returns is Morningstar for the period ending September 30, 2017. Russell 3000 TR USD for the Russell 3000 Index. S&P 500 TR USD for the S&P 500. MSCI EAFE NR USD for developed international markets. MSCI EM NR USD for emerging markets stock. Barclays US Agg Bond TR USD for the US Aggregate bond index. Russell 2000 TR USD for the Russell 2000 Small Cap Index.

|

|

| Renegade Economist Richard Thaler Wins Nobel Prize |

|

|

|

| Economist Richard Thaler |

|

Imagine a person who always, in every circumstance, makes rational decisions with his money. He saves when he ought to and spends exactly as he should spend, in order to maximize the "utility" of whatever wealth he happens to possess. He defers gratification with ease. When he invests, he has instant and total access to all possible information related to every item in his portfolio, including the details of every company's financials and any impactful world events, even if they haven't reached the news media yet. If he found a $100 bill on the sidewalk, he would immediately go out and invest it in a steel mill.

Most of us have never met a person like that, but this is how most economists, when they build their models, assume that normal humans behave. All of us-and especially professional financial planners-know that these assumptions are far from what we see in the real world, which makes us question whatever economists tell us about group behavior like the financial and economic markets, laws and regulation, or what consumers will do next.

All of this is why a silent cheer went up around the professional investing world when University of Chicago economist Richard Thaler was awarded the 2017 Nobel Prize in Economics by the Royal Swedish Academy of Sciences. Thaler spent his entire career exploring the differences between these unrealistically idealized economic assumptions and actual human behavior. He demonstrated that people take mental short-cuts-called "heuristics"-when they make what they believe to be logical decisions. He showed that in the real world, their decisions are often impulsive, and self-control is more of an aspiration than a reality.

|

|

|

One of Jean's favorite books |

Thaler also developed a theory of "mental accounting," which explained how people make financial decisions by creating separate accounts in their minds-one for college funding, say, and another for retirement, and still another for vacations or a new car. He explored those mental short-cuts and found that people tend to expect more in the future of what they've recently experienced (recentcy bias) and uncomfortably often they believe themselves to have more knowledge about their decisions than they actually do.

An experiment with a lost ticket uncovered the "sunk cost" effect. Thaler found that if people purchased a $100 opera ticket and lost it on the way to the show, they would be unlikely to buy another ticket, reasoning that $200 was too much to pay. But if we were perfectly logical, the only choice upon approaching the ticket counter should be whether it was actually worth $100 to hear the opera, and we had already made that decision when we bought the first ticket.

This is actually the second time that the Nobel Prize in Economics has been awarded to behavioral theorists who strayed from the economic party line. Daniel Kahneman won the prize in 2002 for his work with fellow psychologist Amos Tversky on human behavioral biases and systematic irrational behaviors.

In the models that economists produced out of their assumptions of perfectly rational, all-knowing investors and consumers, we could never have market bubbles or market crashes, since every market price is right and fair at every moment. In that strange world, nobody would ever pay more than anybody else for a product or service. Thaler's prize-and Kahneman's before him-suggest that the world of economics is starting to catch on to the messy decision-making that actually goes on in the real world.

Article adapted with permission of Financial Columnist Bob Veres.

|

|

| How to Respond to a Data Breach |

Protecting ourselves from identity theft is top-of-mind since hackers broke into Equifax's database and stole personal information tied to 143 million of us.

The hackers accessed people's names, Social Security numbers, birth dates, addresses and, in some instances, driver's license numbers. They also stole credit card numbers for about 209,000 people and dispute documents with personal identifying information for about 182,000 people. There is no reason to think that data is not for sale to criminals who can use it to open new lines of credit or file phony tax refund requests in peoples' names.

If you have credit, then there's a high probability that identity thieves now have your Social Security number and address. To contain the potential damage, the U.S. Federal Trade Commission recommends that you take several steps immediately.

First, under federal law you're allowed to request a free copy of your credit report once a year from each of the three credit reporting agencies: Equifax, Experian, and TransUnion

at

www.annualcreditreport.com

. You can do this every 122 days by rotating among the agencies. Look for suspicious accounts or activity that you don't recognize-such as someone trying to open a new credit card or apply for a loan in your name. If you DO see something, visit http://www.Identitytheft.gov/databreach to find out how to mitigate the damage.

Then monitor your online statements. The credit report won't tell you if there's been money stolen from a bank account or suspicious activity on your credit card. Unfortunately, you'll have to turn this into a habit. In most cases, theft happens over time, starting with small amounts stolen from across your accounts.

Finally, place a credit freeze and/or fraud alert on your account with all the major credit bureaus. You can put a fraud alert, for free, by contacting one of the credit agencies, which is required to notify the other two. This will warn creditors that you may be an identity theft victim, and they should verify that anyone seeking credit in your name is really you. The fraud alert will last for 90 days and can be renewed.

If you're really worried, consider putting a freeze on your credit.

A freeze blocks anyone from accessing your credit reports without your permission-including you. This can usually be done online, and each bureau will provide a unique personal identification number that you can use to "thaw" your credit file in the event that you need to apply for new lines of credit sometime in the future. Another advantage: each credit inquiry from a creditor has the potential to lower your credit score, so a freeze helps to protect your score from scammers who file inquiries. The downside of a freeze is that financial and governmental institutions use your credit history to authenticate your identity when you open new bank or investment accounts, pull your social security record, or even change insurance companies. So it is somewhat of an inconvenience to have your credit frozen.

Fees to freeze your account vary by state, but commonly range from $0 to $15 per bureau. You can sometimes get this service for free if you supply a copy of a police report (which you can file and obtain online) or affidavit stating that you believe you are likely to be the victim of identity theft.

Many Americans have opted to sign up for a credit monitoring service, which won't prevent fraud from happening, but WILL alert you when your personal information is being used or requested.

There's one last way you can protect yourself. ID thieves like to intercept offers of new credit sent via postal mail. If you don't want to receive pre-screened offers of credit and insurance, you have two choices: You can opt out of receiving them for five years by calling toll-free 1-888-5-OPT-OUT (1-888-567-8688) or visiting

www.optoutprescreen.com.

You can also permanently opt-out by returning a signed Permanent Opt-Out Election form, which will be provided after you initiate your online request.

Unfortunately this need for vigilance is not short-term. Because our social security number is ours for life, this information being available to crooks means we'll need to monitor our accounts for years to come.

Article adapted with permission of Financial Columnist Bob Veres.

|

|

| The Uncommon Average |

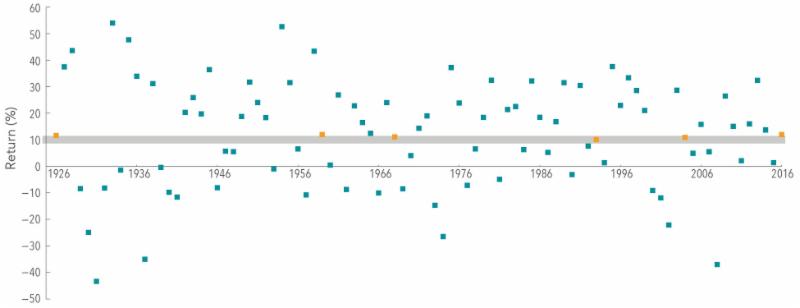

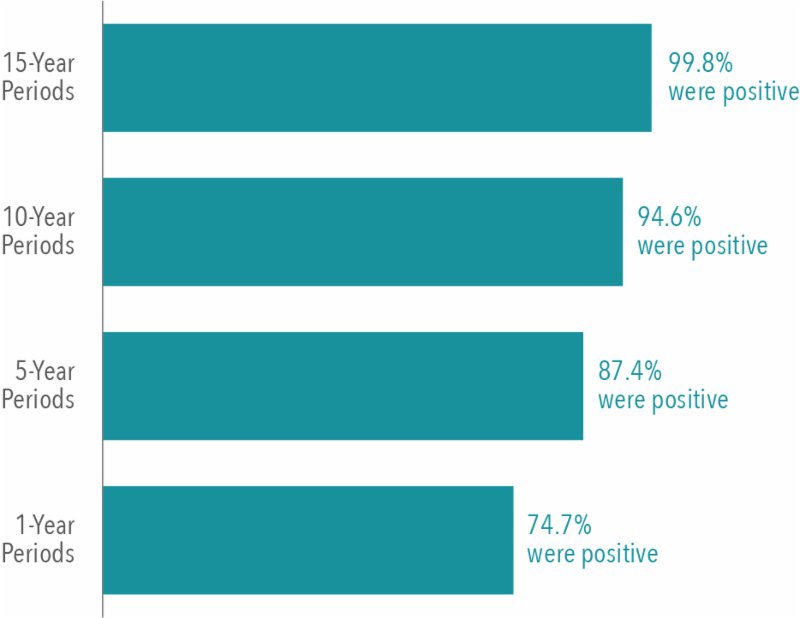

The US stock market has delivered an average annual return of around 10% since 1926.

[1]

But short-term results may vary, and in any given period stock returns can be positive, negative, or flat. When setting expectations, it's helpful to see the range of outcomes experienced by investors historically. For example, how often have the stock market's annual returns actually aligned with its long-term average?

Exhibit 1

shows calendar year returns for the S&P 500 Index since 1926. The shaded band marks the historical average of 10%, plus or minus 2 percentage points. The S&P 500 had a return within this range in only six of the past 91 calendar years. In most years the index's return was outside of the range, often above or below by a wide margin, with no obvious pattern. For investors, this data highlights the importance of looking beyond average returns and being aware of the range of potential outcomes.

Exhibit 1: S&P 500 Index Annual Returns 1926 - 2016

[1]. As measured by the S&P 500 Index from 1926-2016.

Source: Dimensional Fund Advisors LP. Used with permission.

There is no guarantee investment strategies will be successful. Investing involves risks including possible loss of principal. Diversification does not eliminate the risk of market loss.

All expressions of opinion are subject to change. This article is distributed for informational purposes, and it is not to be construed as an offer, solicitation, recommendation, or endorsement of any particular security, products, or services.

|

|

I hope you found this newsletter informative. KFP offers a free, no-obligation initial consultation to start the financial planning process for new clients. To learn more or schedule a time, call 817-993-0401 or e-mail [email protected].

Sincerely,

|

|

Jean Keener, CFP®, CRPC® and the entire Keener Financial Planning team

Keener Financial Planning provides as-needed, fee-only financial planning and investment management services. We're proud to have provided all advice on a fiduciary basis since the Firm's inception in 2008.

*Source for investment returns is Morningstar as of October 17, 2017. S&P 500 TR USD for the S&P 500. MSCI EAFE NR USD for developed international markets. MSCI EM NR USD for emerging markets stock. Barclays US Agg Bond TR USD for the US Aggregate bond index.

|

|

|

|

|

|

|