|

|

|

The Struggles Of Being A Retirement Plan Provider And How To Manage It.

What you have to deal with.

Any good retirement plan financial advisor will tell you that relationships in the retirement plan busi- ness mean everything. The relationships that an advisor can have with their clients and other retirement plan professionals are the most important things and everything else is secondary. One of the most important relationships that a financial advisor can develop to augment their practice to current and future clients is finding a few third party administrators (TPAs) to work with. In many ways, the TPA's can be the financial advisor's best friend and this article will show you why. Any good retirement plan financial advisor will tell you that relationships in the retirement plan busi- ness mean everything. The relationships that an advisor can have with their clients and other retirement plan professionals are the most important things and everything else is secondary. One of the most important relationships that a financial advisor can develop to augment their practice to current and future clients is finding a few third party administrators (TPAs) to work with. In many ways, the TPA's can be the financial advisor's best friend and this article will show you why.

To read the article, please click here.

|

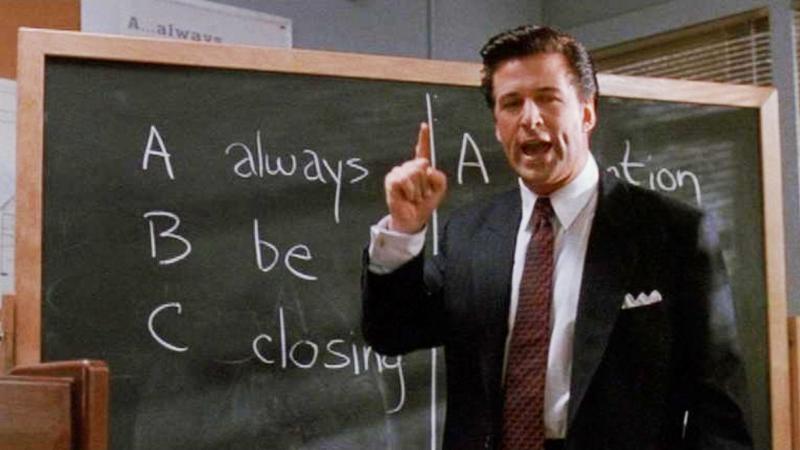

Always Be Watching.

Always, always.

Who can forget Alec Baldwin's speech in Glengarry Glenn Ross on how salesmen should "Always Be Closing" and how coffee is for closers only? It was the highpoint of a great movie.

I'm not going to go through a discussion on sales, but a cautionary tale that you have to advise your clients to navigate a path where other plan providers will try to sell you client products or services that they don't need. So instead of Always Be Closing, you should "Always Be Watching" what happens with your client.

I have a retirement plan sponsor client trying to terminate their retirement plan. The retirement plan has a fully paid up insurance policy and the sole owner participant wants to purchase that policy from the Plan. So my client talks with a salesperson with the insurance company about the policy. Of course, the new salesman wants to sell my client another insurance policy that he doesn't need since the business is folding and he's 71. So I always watch and my client avoided buying a new policy.

I advised my client that he should open a new bank account for his retirement plan at the local bank when dealing with transferring the life insurance policy. So my client goes to the local bank and just wants to set up a bank account for the plan's trust. The bank tells him that he has to meet with the financial advisor at the bank, i.e, the broker. Why does anyone have to meet a broker to open a bank account? Not to talk about how my Mets will do in 2016.

It's not enough to service the client, you always have to watch and make sure that the client doesn't end up buying retirement plan services and products that they don't need.

|

The Vagueness of the Best Interest Exemption.

It doesn't mean much.

One of the interesting points of the new fiduciary rule is the best interest exemption that is intended to stop conflicts of interests especially for brokers who need to meet a new fiduciary standard.

As long as a broker can show that investment guidance was in the best interest for their clients, they should avoid being tagged as having a conflict of interest especially if they are selling their own proprietary product or getting a better trail of fees.

What is the best interest exemption? It seems like a low burden for a broker to meet, nut I think it's so vague that only litigation will end up defining what is actually in the best interest for clients.

Just my two cents.

|

|

|

| |

|

|

|

Politics plays a big part.

You read articles about the Department of Labor's (DOL's) new fiduciary rule and experts will tell you that it's the greatest thing since sliced bread, the worst thing since Caddyshack II, or somewhere in between. I learned a long time ago that you can't please everybody.

If you come from the broker side of things, it's Armageddon. If you're on the registered investment advisor side of things, the DOL sold old out by watering down the requirements laid out in the proposed rule.

What you really have to realize about the DOL is how the role of politics played into the implementation of the rule, it was one of the overriding factors in its formulation, change, and implementation.

The DOL under Phyllis Borzi's leadership under the Employee Benefits Security Administration (EBSA) staked a lot of political capital on changing the fiduciary rule. 6 years of trying to formulate some type of rule that would get a broad range of support is the reason that the current DOL administration had to come up with a new rule. Any politician or administration official is concerned about legacy and Borzi knows how much of a failure she'd look like if there were no new rule because that was something she was talking about for years.

As far as the changes from the proposed rule, a change was going to be made. The proposed rule was always going to be more stringent than the final rule because it's the game of politics Noting the opposition from Wall Street and watering down the standards of the proposed rule is a way of throwing a bone to Wall Street. It was the DOL's way of trying to say that they listened and made changes, but all along they knew that changes were going to be made to get a final rule in.

Further showing that's it's all a game of politics, the DOL won't make the rule effective until January 1, 2018. That means a new administration in the White House will see that the rule gets implemented or they may delay it or they may kill it. It will depend who is in the White House, who is in charge of the DOL, and who will be in charge of EBSA in 2018. So the current DOL administration looks good on paper for the new rule, but by delaying its implementation for 18 months, they are kicking the can for the next administration who will get the blame if the rule doesn't get implemented because it's all about politics.

|

|

Offering an education is a must for advisors.

It has to be offered.

I had a few advisors who asked me about offering investment education as it pertained to the fiduciary rule, but it's clear that the Department of Labor wants it offered when it made a carve out to the final rule to allow for it.

Advisors ask me all the time of the role of education in participant directed 401(k) plans. Participant directed 401(k) plans that are governed under ERISA §404(c) offer the plan sponsors liability protection based on a participant's gains or losses on their account when they direct their own investment.

There have been so many misconceptions that plan sponsors and advisors have had concerning ERISA §404(c) plans. They had this belief that if they just give a mutual fund lineup and some Morningstar profiles to plan participants that they are exempt from liability. ERISA §404(c) protection is about following a process and Morningstar profiles is just not enough education to give to plan participants. On the flipside, education to participants doesn't have to amount to an MBA education.

I think an effective education component to ERISA §404(c) plans should include enrollment meetings where the characteristics of the plan are discussed, as well as the investment options, and offering the building blocks of financial education to assist participants to get a better understanding on how to choose investments.

Advisors that may have issues in offering education should always consider using some of the online resources out there such as rj20.com and smart401k.com, who could offer investment advice that an advisor can't if they won't comply with the investment advice regulations.

In addition, written materials such as plan highlights and some Morningstar profiles should always be distributed.

Also while many advisors dislike, one on one meetings to participants should always be offered. While most participants will probably shun such meetings, they should always be offered to those that want them because as we know, every participant has a different financial goal and need. One on one meetings offer participant individualized attention on asset allocation and fund choices; it can be an effective means of educating plan participants more than what a general enrollment meeting can offer. It can help participants understand how retirement plan assets relate to their other assets as part of a comprehensive financial plan.

Advisors should always look at education as liability protection, because offering participant education help a plan sponsor minimize their liability under ERISA §404(c).

While I always stress education as important part of the fiduciary process, it's not about achieving a specific result from participants directing their own investments. Offering participants educations is like the old proverb, "You can lead a horse to water, but you can't make him drink." So no matter how great the education component is, there is no guarantee that it will help plan participants achieve a better financial result because like they say, there is no guarantee in life, except maybe death and taxes. The participant who put all his money into a mid-cap fund because he considers it the "average of the market" may still do so even after getting education at the enrollment meeting and through one on one meeting. As with most things with retirement plans, it's about following a process and not guaranteeing a result.

|

|

CEO of Sentinel Benefits passes away.

John Carnevale, the President and Chief Executive Officer of Sentinel Benefits, a Massachusetts and New York based producing third party administrator (TPA), died of a heart attack suddenly last weekend.

I never met John, but our paths crossed a few times in the past 8-9 years over a couple of TPAs that Sentinel Benefits eventually purchased.

I never had a bad word with John and we exchanged a few phone calls, but I always had a feeling that John only called to gauge my feelings about things especially with one TPA that Sentinel Benefits merged with, a former employer of mine that I wrote quite a bit in the first few years of my practice. You can also check my Kindle book for some of that ancient history.

My experiences with John revolve around the snowball effect, where one small snowball (a business decision) can cause an unintended avalanche. As far as my former employer, I can tell you that if it was not for a partner of that employer who didn't like me and his "superstar" administrator, I will tell you that Sentinel Benefits would still be a Massachusetts TPA instead of having offices in New York too. I'll leave at that.

The other snowball effect that involved John is something I'm rather thankful to John for because it allowed me to grow as a person and as a businessman. Someone who was perceived as a mortal enemy of mine (I needlessly initiated much of that perception) quietly returned to the retirement plan business to serve as an independent fiduciary/registered investment advisor. Apparently this fiduciary was hurting Sentinel's investment advisory business. So John called me to see some insight from me and I was perplexed with the call because I didn't understand why my old grudge with this fiduciary had anything to do with Sentinel losing business. Any issue that I had with this fiduciary was over and I have a policy of not getting involved in someone else's fight because I have enough fights of my own.

To cut the story short, I reached out that fiduciary not long after John's call. It allowed me to bury the hatchet with someone who really wasn't an enemy of mine; his partner was actually the enemy. It allowed me to repair a relationship with someone that I deep down liked and respected; this fiduciary is now one of my favorite clients. Repairing that World War sized riff allowed me to grow as a person and a businessman because I didn't let an old grudge get in the way of getting new business and it allowed me to forgive someone who hurt me deeply. I grew as a person because it also allowed me to understand this relationship and how to properly serve it.

So I would like to thank John Carnevale for inadvertently helping me grow as a person and I'm sorry that I didn't tell him that when he was alive. May he rest in Peace.

|

The Rosenbaum Law Firm Advisors Advantage, May 2016

Vol. 7 No. 5

The Rosenbaum Law Firm P.C.

734 Franklin Avenue, Suite 302

Garden City, New York 11530

516-594-1557

Fax 516-368-3780

Attorney Advertising. Prior results do not guarantee similar results. Copyright 2016, The Rosenbaum Law Firm P.C. All rights reserved.

|

|

|

|

|

|

|

| |

|