|

|

|

The Good Fundamentals of Being a Retirement Plan Financial Advisor.

Better than winning ugly.

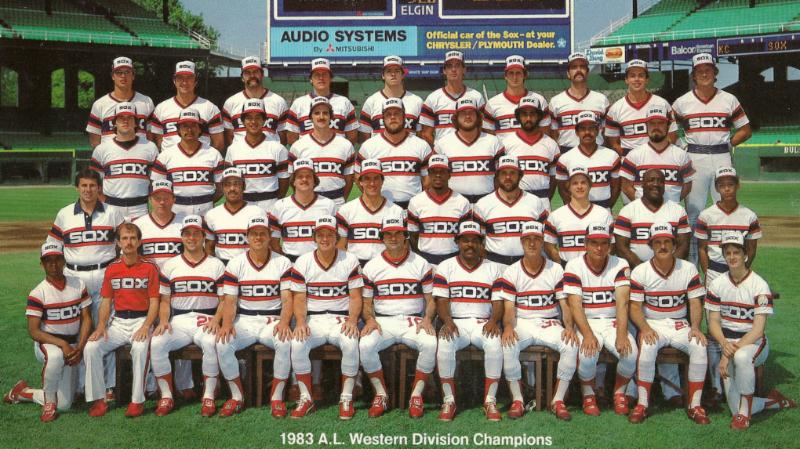

In 1983, the Chicago White Sox won the American League Western Division under the guidance of future Hall of Fame manager Tony LaRussa. Doug Rader, then-manager of the Texas Rangers, accused the Sox of "winning ugly" for their style of play, which meant they won games through scrappy play rather than strong hitting or pitching. Strong hitting, strong pitching, and strong fielding are the good fundamentals of baseball and good fundamentals usually trump winning ugly (the Sox lost 3-1 in the Championship Series against the Baltimore Orioles). As a retirement plan financial advisor, you don't have the luxury of winning ugly. You need good fundamentals to function in the retirement plan space and this article will help you lead that way. This article will help you learn the good fundamentals of being a retirement plan financial advisor. In 1983, the Chicago White Sox won the American League Western Division under the guidance of future Hall of Fame manager Tony LaRussa. Doug Rader, then-manager of the Texas Rangers, accused the Sox of "winning ugly" for their style of play, which meant they won games through scrappy play rather than strong hitting or pitching. Strong hitting, strong pitching, and strong fielding are the good fundamentals of baseball and good fundamentals usually trump winning ugly (the Sox lost 3-1 in the Championship Series against the Baltimore Orioles). As a retirement plan financial advisor, you don't have the luxury of winning ugly. You need good fundamentals to function in the retirement plan space and this article will help you lead that way. This article will help you learn the good fundamentals of being a retirement plan financial advisor.

To read the article, please click here.

|

|

The proposed Fiduciary Rule and the selling of Fear.

It's part of their job.

I'm a Howard Stern fan since I was about 11. I'm sorry if you're offended, but I love that brand of humor. One of the main producers of funny materials are guys by the name of Sal & Richard. Aside from their phony calls, they have this bit where they interview people on the street by asking them a question about something that isn't going to happen such as: how do you feel about Howard Stern signing the national anthem at the Super Bowl or did you hear that the Jews are trying to replace Thanksgiving with Chanukah (in 2013, they occurred at the same time)? Rather than challenge the veracity of the question, the people on the street opine as if the nonsensical event is actually happening and it's hilarious. If people don't know whether the event is taking place or not, they will offer an opinion just because they are too embarrassed to admit they know nothing about the question. I'm a Howard Stern fan since I was about 11. I'm sorry if you're offended, but I love that brand of humor. One of the main producers of funny materials are guys by the name of Sal & Richard. Aside from their phony calls, they have this bit where they interview people on the street by asking them a question about something that isn't going to happen such as: how do you feel about Howard Stern signing the national anthem at the Super Bowl or did you hear that the Jews are trying to replace Thanksgiving with Chanukah (in 2013, they occurred at the same time)? Rather than challenge the veracity of the question, the people on the street opine as if the nonsensical event is actually happening and it's hilarious. If people don't know whether the event is taking place or not, they will offer an opinion just because they are too embarrassed to admit they know nothing about the question.

I feel that this is the same thing regarding a poll conducted by U.S. Hispanic Chamber of Commerce and Greenwald & Associates, a research firm. The poll claims that if the Department of Labor (DOL) changes the fiduciary rule, small employers will stop sponsoring retirement plans and will suspend employer contributions. It's absolute nonsense.

The survey included 607 retirement plan decision makers at businesses with up to 500 employees. 30% of the plan sponsors in the poll say it is at least somewhat likely they will eliminate the retirement plans currently available to employees.

More than 40 percent of small businesses without a plan say the regulation would be at least somewhat likely to cause them to charge participants higher fees or not offer matching contributions. What does the fiduciary rule have to do with matching contributions or affect the plan sponsor's capacity to make one?

Sometimes you will get an answer based on how you answer the question and I sincerely doubt that the poll sufficiently addressed what the new fiduciary rule actually entails.

I think that most plan sponsors don't understand the proposed rule that would require all retirement plan financial advisors to serve in a fiduciary capacity especially hen I read this in Financial Advisor Magazine:

""The findings presented here show that the DOL expansion of fiduciary status will only impede the ability of small firms to offer their employees retirement-plan accounts, thus hindering American workers from saving for a reliable future," says Javier Palomarez, president and CEO of the U.S. Hispanic Chamber of Commerce. ??The regulatory change by DOL expanding fiduciary status would limit the retirement plan assistance that some financial professionals can provide to small-business clients, assistance that is valued by small businesses, according to the survey. The expected change would put limits on conversations with small businesses about how to select and monitor the investment options available under a plan, and how those investments are performing, Greenwald and Associates says."

Are we talking about the same rule here or was this just a poll using loaded questions meant to lean plan sponsors toward saying the fiduciary rule is a bad idea because it would limit retirement plan assistance? You know the answer. A new fiduciary rule would treat all retirement plan advisors, as fiduciaries and it would eliminate some of the abuse where some advisors push funds for the plan's investment lineup just because it pays the advisor better. Requiring any retirement plan financial advisor as a fiduciary makes them have skin in the game, which means they would have to be more prudent in their role as an advisor since their duty is to the plan and not to their pocketbook.

This poll is just an attempt at putting fear in trying to defeat any proposed fiduciary role. I'm sure that if I asked the same 607 plan sponsors whether they think the DOL fiduciary rule is bad because it will require plan sponsors to pay a 5% tax to the DOL, they will have a negative poll result as well.

Don't oppose the fiduciary rule on fake fear, oppose it based on the facts. I support it based on the facts.

Retirement plans are a mess and one way to make them better is a fiduciary rule. Weren't the same people who think the fiduciary rule is a bad idea the same folks who said people would terminate their plans because of the fee disclosure regulations? I don't know, but it's the same selling of fear and we know how it turned out after fee disclosure. Lots of plans are still around.

|

|

|

|

|

|

|

As a Plan provider, saying sorry can go a long way.

It can defuse a potential blowout with a client.

I worked for someone once who I thought was the biggest pain in the rear end and I think when I got older and started my own business, I finally understood where he was coming from. I worked for someone once who I thought was the biggest pain in the rear end and I think when I got older and started my own business, I finally understood where he was coming from.

When I work on my own and something doesn't get done, it's all on me. When I worked for law firms and especially third party administrators (TPA), there are times when you have to rely on others and when they don't get what you need done, you can't get your stuff done. When my boss asked me why I didn't accomplish something or if I did something wrong based on the information provided, he didn't want to hear any type of excuse. He just wanted me to acknowledge that I did wrong without making any excuse even if they were valid. I once drafted a defined benefit plan document 5-7 times because the actuary and the client couldn't handle as to what the plan was supposed to say rather than how they thought should be administered. The fact that the actuary had no clue how he administered the plan didn't change the fact that the client was disappointed.

The same thing can be said about clients. They don't want to hear excuses; they just want to hear that you're sorry. When you're on the phone with a government agency and they haven't acted on something for you, you don't want to hear from the person you're complaining to that they're understaffed. If you're complaining about the work done for you, you don't want to feel that the person who was supposed to get the work done thinks your concern is silly by responding LOL to your complaint.

Sorry is the hardest word sometimes because people think sorry equals guilt or admission of liability. It isn't. I find it a great method to defuse a situation. There are times when I failed to get something done because I was ill or flooded with work and I said I was sorry because I didn't meet the client's expectation, It happens, thankfully not so much. The sorry went a long way into nipping any remaining anger with my failure to get something done.

I have families destroyed and business partnerships disintegrated just because someone put too much weight in what saying sorry meant. Saying sorry doesn't mean someone has something over you or that you're going to have say sorry many more times, it's just a great way to communicate with someone who is disappointed in you. It helps healing the disappointment they had.

I'm sorry you had to read this, but it's something I thought you should read.

|

|

As a plan provider, learn to say no.

There are some times when you have to turn down business.

I always believe that regardless of whether it's business or in regular day-to-day life, that you can't be everything for everybody. Being honest with that is only half the battle. I always believe that regardless of whether it's business or in regular day-to-day life, that you can't be everything for everybody. Being honest with that is only half the battle.

A lot of times, I met folks who are interested in starting a registered investment advisory (RIA) firm. I get calls for my insight on the retirement plan business, as well as my work in drafting advisory agreements for RIA firms and their retirement plan clients to comply with the fee disclosure regulations (which I do for $1,000 on a flat fee basis, cheap plug) here. I also get asked on whether I could work on their RIA registration or whether they should use one of those businesses that only deal with RIA set ups and registration. Looking at my experience in doing that and comparing myself to these businesses, I politely tell them that these firms would be a better fit for their RIA registration. It's not that I couldn't do the work; it's just that the fees and length of time in doing the work is probably better by using a business that does nothing but RIA registrations. Perhaps these new RIAs will be a client of mine, perhaps not, but at least I was honest with them. Again, you can't be everything for everybody.

I have a friend of mine who works for a great third party administration (TPA) firm in the Northeast. Only problem is that when it comes to smaller plans, the fees are high. Nothing wrong with that, except if you are a smaller plan and were dead set on getting this TPA to handle your plan. Anyway, this salesperson met one of the accountants he was familiar with. The accountant had a lot of opportunity in single employee, defined benefit plans. With a $4,000 minimum for the actuarial work, the salesperson told the accountant that they were better off finding another firm for these plans at less than half what his minimum fee was. Again, you can't be everything for everybody.

Contrast this with a case at my old TPA. We had a 401(k) plan where the human resources director hated us from day one because we wouldn't do the work she received from the previous TPA she liked. She was a problem from Day 1, but we took the case because we had a great relationship with a southern RIA firm. So this client was a problem from Day 1, but they seemed to be interested in changing the plan by making it a K-SOP, basically adding an employer stock ownership feature (ESOP) to it. The client's advisors asked me about our experience with it and I was honest, I said we had a couple of those cases. Our lack of experience showed up in some of the presentations to the client (of which I was not invited to attend). Story cut short, our lack of knowledge was exposed and not only did we lose the client, the RIA who referred us the client lost the client as well.

Regardless of whether it's a TPA, RIA, and an ERISA attorney, you know you found an honest provider when they basically tell you that they can't handle your plan because the plan is not a right fit for their book of business. As a plan provider, you also need to be honest and forthcoming when you can't do the work. Know your limits and let the potential clients know what they are.

|

|

No matter how great you maybe, some people still think their trash is gold.

Aside from my children and my wife, my favorite person of all-time was my grandmother Rose. In a few weeks, it would have been her 90th birthday and I wish she could have made it because she was the most selfless person I ever met, who was full of life, and love for family. When my grandmother decided she would move upstate to live with my aunt, she started cleaning out her apartment. She put her trash on the side of the street for sanitation pickup and she was amazed that people on the block were looking through her trash. She said: "what do they think I threw out, gold?" Aside from my children and my wife, my favorite person of all-time was my grandmother Rose. In a few weeks, it would have been her 90th birthday and I wish she could have made it because she was the most selfless person I ever met, who was full of life, and love for family. When my grandmother decided she would move upstate to live with my aunt, she started cleaning out her apartment. She put her trash on the side of the street for sanitation pickup and she was amazed that people on the block were looking through her trash. She said: "what do they think I threw out, gold?"

It was a funny line, but I think my grandmother didn't understand that to some, her trash might be gold.

As a professional plan provider, we usually think we're great and we're stumped when a potential client cherishes an incumbent plan provider that we know is no good and we're dumbfounded by it. It's human nature to question what a plan sponsor could see in such ap plan provider, but we see this all the time whether it's business or in family. What we may think is trash is someone's gold and what we think is gold is someone else's trash.

I worked for a third party administrator, where the chief operating officer would champion some administrator or actuary or salesperson as a superstar. They never were a superstar, but since this fellow cared less about good administration and more about paying employees on the cheap, they were his superstars. He would tell me how he got an actuary for a $75,000 salary; the fellow wasn't $7,500 even more so after the other partner woke up the actuary while he was sleeping at work.

I remember when a relative of mine dated someone she unfortunately married. I would hear my mother tout that he was a businessman. Dropping out of a community college, operating a hot dog stand at a flea market, and owning a dry cleaning store that did none of its dry cleaning doesn't make a businessman. 24 years and 3 careers later, the jury is still out. But some people have such wacky (we think of low) expectations of their plan providers, that no matter how great you are and how bad the incumbent is, it's not going to change.

It's like the Olive Garden. Having grown up in such an Italian-Jewish neighborhood such as Canarsie, Brooklyn who all moved where I live in Oceanside, Long Island, I hate the Olive Garden. When you grow up with great Italian food, you find Olive Garden an affront because it tries to be the McDonalds of Italian food. Some people out in the Midwest where there are not many Italians may think the Olive Garden is the greatest thing ever. I'm not going to debate someone who loves the Olive Garden because you can't properly debate opinions.

The lesson here is that there are some times; you're not the answer because the plan sponsor loves the plan provider. Maybe the plan provider is a relative; maybe the plan provider went to the same college as the owner of the company; maybe the plan sponsor likes to surround himself or herself with incompetent people to make himself or herself competent (that TPA COO did that). Whatever the reason, it's a waste of time to crack that nut. Just remember you're not crazy, but maybe the plan sponsor is.

|

2014 Berla Scholarship Awarded.

Thanks for your continued support.

I am pleased and honored to announce that Diane DeSimone, Stony Brook Class of 2015 is the winner of the 2014 Rozalia and Emil Berla Scholarship Fund. I am pleased and honored to announce that Diane DeSimone, Stony Brook Class of 2015 is the winner of the 2014 Rozalia and Emil Berla Scholarship Fund.

I started The Rozalia and Emil Berla Memorial Scholarship Fund at my alma mater, Stony Brook University. This scholarship is named for the two greatest people I ever knew, my maternal grandparents who both survived the Holocaust.

Many of you in the retirement plan industry have contributed already and you have my thanks. If you can spare just a couple of bucks towards this worthwhile scholarship, I would greatly appreciate it.

$1,000 isn't much, but for a student attending such a great school, it's a substantial step in paying tuition.

You can donate online through this link. All you need to do to make sure the scholarship gets the money is to type "Berla" in the fund designation.

You can mail any contributions to

Send to Jane McArthur c/o College of Arts & Sciences, E3320 Melville Library, Stony Brook, New York 11794-3391. The Berla Scholarship should be noted on the memo line of your donation.

All gifts will be noted with a tax receipt.

|

The Rosenbaum Law Firm Advisors Advantage, June 2014

Vol. 5 No. 6

The Rosenbaum Law Firm P.C. 734 Franklin Avenue, Suite 302

Garden City, New York 11530

516-594-1557 Fax 516-368-3780

Attorney Advertising. Prior results do not guarantee similar results. Copyright 2013, The Rosenbaum Law Firm P.C. All rights reserved. |

|

|

|

|

|

|

|

|

|