|

Limited choices, rising prices keep many first-time buyers from getting a home this spring

by FoxBusiness.com

Young people aspiring to buy their first home are already facing disappointment this year. Rising prices are putting more homes out of reach, and pickings are slim because few properties have come onto the market this spring, when sales are supposed to take off. Millennials are also burdened by heavy school debt and depleted savings that hurt their ability to qualify for a mortgage. Until their incomes start to rise meaningfully, many will be forced to keep hunting for a home while delaying the dream of ownership. This has weighed on overall home sales and economic growth throughout the rebound in housing the past three years. "People need to see more money in their paychecks before they'll take the plunge into homeownership," said Greg McBride, chief financial analyst at Bankrate. If early signs are any indication, there won't a noticeable jump in new homeowners during the spring. Amy Arnold and her husband began looking at listings in Denver late last year. The 28-year-old apparel buyer quickly found that the few homes in the couple's price range got snapped up for more than asking price, leaving her exasperated at how "crazy" the market seemed. For now, the couple has decided to keep renting a two-bedroom, one-bath house for $1,300 a month, hoping to have more money and find a better selection of homes once they jump back into the market. "It's very discouraging," said Arnold. "Hopefully next year we will be able to buy, but there's a chance we may have to rent again." Home prices nationwide have risen at more than double the pace of average hourly wages, making it harder for buyers to find the extra funds to save for a down payment. In Denver, a limited roster of homes has fueled the rising prices and given sellers the upper hand. Forty percent of homes that sold in February went for more than the asking price, according to online real estate broker Redfin. That's up from 21 percent a year earlier. In addition, half of the homes on the market went under contract in eight days or fewer. "Typically, January, February even March are not quite as highly competitive as when you go into the spring months," said Ilona Botton, a Redfin agent in Denver. "That's not how it was this year. It has been multiple offer situations every single month." The limited supply of homes is widespread. In March, one measure showed it would take fewer than five months to sell all the previously occupied homes in the U.S. In a market more balanced between buyers and sellers, it would take about six, according to the National Association of Realtors. What's more, heavy demand for low-priced homes means their prices are rising faster. Homes priced at $135,000 or less jumped 9 percent for the year ending in February, according to data from CoreLogic. Homes that priced at $226,800 or more climbed 5 percent over the same period. Beyond offering more money, some buyers are willing to waive home inspection or give sellers several weeks to move out following a sale, said Redfin's Botton. In general, areas with fewer homes for sale have stronger job growth that eclipses the pace of construction. Areas with larger inventories tend to keep the availability of housing in line with job growth. In Columbus, Ohio, aviation company executive Ryan Holtmann had plenty of options. He and his wife started shopping for their first home at the end of last year. The couple visited about 15 to 20 houses before buying a three-bedroom home for $154,900 at the end of February. "I was really surprised at how much was out there for the time of year," said Holtmann, 33. "There were three or four we liked and would have been more than happy to go with." One factor preventing more houses from hitting the market is that many homeowners still owe more on their mortgage than their home is worth. That's known as an underwater mortgage, or being in negative equity. While millions of homes have returned to positive equity as values come back, some 5.4 million, or 10.8 percent of all homes with a mortgage, remained underwater as of the October-December quarter, according to CoreLogic. Nevada topped the list. Nearly a quarter of its homes with a mortgage were underwater. More construction would help buyers, but activity has recovered slowly since 2010. That's one reason a recent report by mortgage buyer Freddie Mac forecast that the U.S. housing market will continue to see low levels of homes for sale for the next several years. As a result, even successful buyers are settling for less. Brett Singley, a first-time buyer in Los Angeles and a father of four, knew the kind of house he wanted and how much he could afford. But after six months of searching, the civil engineer shifted his sights to smaller and less expensive townhomes. In March, he bought one in Santa Clarita, a northern suburb. He got a three-bedroom for just under $300,000 - $100,000 less than what he was prepared to pay for a house. "We were originally looking for a four-bedroom house," said Singley. "But we didn't have a lot of options."

|

|

Secret real estate listings you won't find on the market

by CNNMoney.com

Just because there isn't a "For Sale" sign in a yard, doesn't mean the homeowner isn't taking offers. You just have to know the right person. Despite strong demand in many markets across the country, some homeowners are skipping the process of officially listing their home on the multiple listing services, leaving agents with the task of finding a buyer without publicly advertising it.

And real estate professionals say these "secret" listings -- commonly known as "pocket listings" -- are becoming more popular. Kofi Nartey, a real estate broker at The Agency in Los Angeles, has recently seen an uptick in off-market lists. He says they currently make up around 10% to 15% of his firm's sales. But in a seller's market with bidding wars driving offers well above the asking price in some areas, why would a homeowner sell their home in secret? The reasons vary: some want privacy, others are testing the waters and some think the exclusivity can draw a higher sale price. "Many times I've had pocket listings where people will say, 'If I get this number I will sell, otherwise I have no desire,'" said Jade Mills, a real estate agent with Coldwell Banker Residential Brokerage in Beverly Hills, who recently sold a $38 million home off market. These secret listings make up about 10% of her sales, an increase from previous years. Not publicly listing a home can reduce the pool of buyers, which could potentially mean missing a top offer. Mills said nonpublic listings tend to be advantageous for properties listed at $10 million or higher. "In the upper price ranges, you don't have as good of a chance of getting multiple offers." She recently sold a house for $1.35 million, more than the asking price and after getting multiple offers, something that she said probably wouldn't have happened if it wasn't publicly on the market. Off-market listings can be beneficial to agents by upping their commissions if they represent both the buyer and seller. But connecting the right buyer for an off-market listing or drumming up new listings can be a challenge, experts said. Nartey frequently plays real estate matchmaker at social events. "Any time I hear at a cocktail party or birthday party ... if a [guest] mentions they are considering selling, I make a mental note of it," he said. "And then when I am another event and hear someone who is looking, it becomes a matching game." He added that public sales can lead to off-market sales when a neighbor stops by an open house and questions the asking price of the home. When the home sells for that once-thought inflated price, Nartey will sometimes approach the neighbor about selling. "We have the buyer demand to pair them with a home that isn't even on the market." Pocket listings are also sold among agents representing buyers and sellers. Those with an offline property will work with other professionals to find a seller. Some use a distribution list to connect an off-market seller with a buyer, said Brett Forman, managing director with Dolly Lenz in New York City. "There are people we know in trusted markets and companies that we believe have the Rolodex to insert themselves into a unique situation," said Forman. |

|

5 Reasons to Treat Your Debt Like an Emergency

by Credit.com

Whether it's credit card debt, student loans or personal loans that are burdening you, now is the time to pay them off for good. Although living in debt may seem to be the norm nowadays, it can hold you back from reaching your financial goals and living the way you want. Check out the list below to get motivated to treat debt like something that needs to be taken care of immediately. 1. Interest No matter how "good" your rates may be, interest on a debt or loan is still extra money that you have to pay. Interest rates can magnify the costs of your purchases quickly. Therefore, even if you snag a deal on a car or an article of clothing, you end up paying way more for it. And interest can add up without you even realizing it. Next time you only pay the minimum amount of your credit card debt, it can be a good idea to calculate how much interest you will be paying overall if you stick to your repayment plan. Then imagine what you could do with that savings if you repay the debt more aggressively. (Check out this credit payoff calculator to see how much interest you'll pay - or save.) 2. Credit Score Remember when you took out a loan? Have you ever bought a house? Applied for a credit card? That magic number lenders check to see what interest rate you qualify for and how much money they will lend you is called your credit score. Carrying too much debt can impact your credit score, which can then impact your ability to buy a home, a car or another major purchase. You can see how your debt is impacting your credit scores for free on Credit.com. 3. Financial Security - Now & Later If you dream of the days you can walk out of your office forever or even just want the peace of mind that comes with knowing you have reserve cash in case an emergency comes up, it's a good idea to pay off your debt. Saving for retirement and ensuring a prosperous financial future is made easier when a bulk of your paycheck every month isn't going toward repaying debt. 4. Investments Some of your more financially secure peers probably spend their time worrying about which CDs or stocks to invest in, whether they should buy or rent their next home and which government bonds have the highest yield instead of barely making ends meet with their monthly payments. The faster you pay off your debt, the faster your money can work for you instead of the other way around. 5. Stress Finally, debt can wreak havoc on your emotions, relationships and personal well-being. Worrying about whether you can meet your debt obligations can cause a lot of anxiety. This anxiety can then leave you feeling less connected to your friends, family and co-workers. It seems obvious but by paying off debt, you will no longer have to worry about paying off debt! There are many methods to speed up your debt repayment. Once you decide that it's a priority, you can begin finding the best way (or ways) for you. You can consolidate, make bulk payments if possible, refinance, cut spending, pick up a side hustle or even create your own combination of methods.

|

|

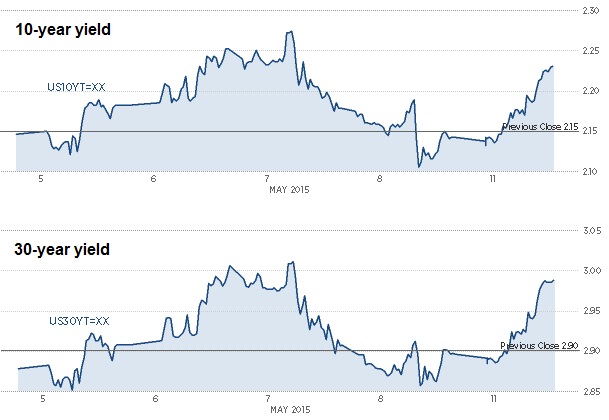

Bond Yields Spike, Market Looks for Capitulation

by CNBC

Treasury yields ripped higher Monday, putting pressure on stocks and signaling a possible sea change in the global rate environment.

The move in yields on the 10-year note and 30-year bond was surprisingly rapid and violent, and strategists were hard pressed to pinpoint a specific reason for the shift. Markets will now focus on rates Tuesday, to see if Monday's high yields are just the starting point for a new trading range. Traders in the futures pit in Chicago characterized the move as being similar to a "global margin call," where each tick higher in yield into new territory forces more repositioning. The shift higher in rates then becomes self-fulfilling until there is a capitulative spike.

"This is starting to become a bad omen. This is not good. There's enough leverage out there in different forms, where if this is the end of the 'easy money, low long-term rates' story and the Fed is not going to be able to hike, the long-term interest rates market is going to do the tightening for the Fed, and this will be bad for most financial assets," said George Goncalves, head of rate strategy at Nomura. "If this move is really a referendum on central bankers providing too much liquidity and if this is the hangover part, it could go much further," said Goncalves.

The sharp move higher in rates caught many in the markets by surprise, since Friday's post-jobs report decline in yields seemed to be setting the stage for consolidation. But U.S. yields followed European yields higher Monday and then moved even further on their own.

Bond yields have been moving higher for two weeks now, after the reversal in European sovereign yields, particularly the bund. The market had viewed Friday's jobs report to be neutral enough to keep Fed rate hikes on hold until the fall.

"There's relatively little going on right now so it seems like a situation where even though rates backed up to a level that we haven't seen in quite some time, it feels like nobody wants to be the first one in the pool because they're just not sure where it's going to go," said Ward McCarthy, chief financial economist at Jefferies. He said the lack of liquidity in the bond market was helping to exaggerate the move.

"The bond market is getting beaten like a rented mule," said McCarthy. "I think it's one of these situations where it's the early stages of (quantitative easing). QE has always caused some counterintuitive market behavior. I think right now, we're in the early stages of ECB (European Central Bank) QE." Even before the ECB embarked on its QE program, European yields headed lower to the point where the German 10-year had been closing in on a zero rate, before switching direction.

The U.S. 10-year touched a high 2.28 percent Monday and the 30-year bond yield reached a high of 3.05 percent for the first time since November. The selloff accelerated and stocks fell with it in afternoon trading. "That it's happening with mediocre growth tells me this is a major headwind," for stocks, said Peter Boockvar, chief market analyst at Lindsey Group. The Dow fell more than 100 points but recovered some losses late in the session, closing down 85 at 18,105.

"This is a global trend change," said Boockvar, pointing to the decline in European yields. He also highlighted a bottoming in commodities prices, which has some traders betting that inflation will re-emerge, a trigger for the Fed to raise interest rates.

"The bond's been bleeding all morning. European bond markets traded poorly. The more the day went, the 10-year yield was up another tick. There's obviously a trend change going on. Rallies are now being sold. They're all giving back Friday's rally. There's a big-time change going on in the global bond market."

The market is now focused on three auctions this week and whether the selloff will stabilize. The Treasury auctions $24 billion in three-year notes at 1 p.m. EDT Tuesday. But the most important are the $24 billion 10-year note auction Wednesday, and the $16 billion in 30-year bond auction Thursday.

"I thought we dodged the bullet last week. The key is going to be how these auctions are taken down," said Goncalves. "They're big auctions. If people are actually interested in buying them because there's value, they'll overlook the weird momentum. If they don't, it means the strong hands didn't step in."

Besides the auctions, there is the JOLTS report on job openings for March at 10 a.m. EDT Tuesday, and the NFIB small-business survey is released at 9 a.m. As for data, markets are most focused on Wednesday's retail sales report.

San Francisco Fed President John Williams speaks at 12:45 p.m. EDT in New York, and New York Fed President William Dudley participates on a panel in Switzerland at 3:15 a.m. EDT on the implications of diverging monetary policy.

McCarthy said the rise in rates won't hurt the economy, but the move up in the 10-year will show up in mortgage rates. The move higher could get some borrowers off the sidelines if they believe the shift will continue, he said.

"It's a relatively low-volume trade. It's not capitulation as much as it is reluctance to stand in front of the move," said Ian lyngen, senior treasury strategist at CRT Capital. He said some market players were pointing to the upcoming auctions as a reason for the selling but that didn't make sense.

"The selloff in Treasurys is outpacing the selloff in bunds today," he said, adding Mondays are notoriously low-liquidity days.

|

|

You Can Put a Price on Love: Is Your Relationship Too Costly?

by U.S. News

Anne Violette admits she has dated some "deadbeats" in her time. In particular, there were two boyfriends who lived with her but didn't pull their weight, quitting jobs and refusing to find other options, leading to Splitsville. With one, Violette meticulously tracked shared household expenses for six months. Her findings were infuriating: While she'd contributed $64,000, her live-in beau had only fronted $7,000.

"I must have a sign on my head that says 'sucker,'" says Violette, a ghostwriter and copywriter from Pearland, Texas, whose book "Men Are Like Wine," draws upon her sour -- and at times expensive -- relationship experiences.

Some relationships really do cost too much. And we're not talking about the high cost of drama or stress or the awkwardness of being a mismatch -- all of which can be potential deal-breakers -- but the cold, hard cash poured into relationships without equivalency or much happiness in return. If this sounds familiar, but you're reluctant to break up because, well, you're still in love, ask yourself these questions.

Have You Both Talked About Your Feelings?

It's one thing to throw out hints that you'd like your significant other to occasionally spring for dinner or at least say thanks for you always being the one to open your wallet, but your partner isn't a mind reader. You may also have been in this pattern for so long that your partner thinks everything is great and simply has no idea that you're a smoldering caldron of resentment. That's why it's important to have an honest discussion early in the relationship, says Lisa Brateman, a psychotherapist and relationship specialist in New York City.

Dan Nainan, a standup comedian in New York City, was once in a relationship that began with him paying for everything. So he had a very direct conversation with his girlfriend early on. "Two weeks into our relationship, I sat her down, and I said, 'We have been going out for two weeks, and in that two weeks, you have not offered to pay for a single thing. Not for dessert when I buy dinner, or the tip, or a ticket on the subway, anything. Therefore, from now on, if you still want to go out with me, you have to pay for half of everything. If we go to a restaurant, you pay half. If we go on a trip, you buy your own airline ticket and pay for half of the hotel and half of the expenses." She got up, left, immediately returned and said: "OK."

He may have been more direct than many people, but his timing was smart. Brateman suggests talking to your significant other about your money concerns, if you have any, before you're in too deep.

"Bringing it up early is important before the problem becomes monumental," she says. You especially want to have the talk before moving in together, she adds. You could start the conversation by saying something like: "I understand we have different spending styles, but I'm not feeling comfortable with how we've been handling our money," she suggests.

Does Your Partner Have Your Best Interests at Heart?

If your salary is vastly more than your partner's, it's unreasonable to expect her to constantly go halfsies on meals, movies and whatever else you're doing -- especially if you have expensive tastes. And if you're insisting she join you for outings and locales that eclipse her budget, she may be the one reconsidering her decision to be with you.

But Brateman says it isn't really about the money. It's how your partner feels about your money. If she seems to think she's entitled to have you always pay for everything, that's a red flag that she doesn't have your best interest in mind.

"You want a balance," Brateman says. "Maybe you buy the dinners, but she'll make dinner for you sometimes. Or if you go somewhere, will she occasionally buy the drinks or pay for a cab?"

Another sign that your partner doesn't think much of you, Brateman says: "If you ask her where you want to go to dinner, and she picks the most ridiculously expensive restaurant in town. If she's always picking things she would never pay for herself, that's a red flag."

Is Your Partner Trying to Resolve His or Her Money Issues?

This is really the deal-breaker. If your significant other knows that he or she is bringing money problems into the relationship but recognizes that the behavior needs to change, Brateman says that's a good reason to stick together. "Just because somebody has money problems, it doesn't mean that they always will," Brateman says. "If they want to fix things, there's hope. If somebody says, 'This is how I am, and who I always will be, and I don't care how you feel about it,' that match is probably not going to work."

For Violette, she thinks the moral of the story is that when it comes to money, opposites usually don't attract. "Always go out with someone who is at least your equal and has the basic fundamentals, like a car, a job and stable rent or a home of their own," she advises.

Of course, you may be dating someone who doesn't have the basic fundamentals but is a wonderful partner in other ways. Relationships are investments, but they aren't all about money. You're investing in your emotions as well.

But if you're always the majority stakeholder in all of the fundamentals of the relationship, the union is probably costing you too much. Alas, if that's the case, you can't take your significant other to a customer service desk and get your money back, but maybe it's time to make an exchange for something better. |

|