|

|

Whether A Plan Sponsor Should Hire An ERISA §3(16) Administrator.

It's not for every plan.

Running a business is a complicated activity. You have to be an expert in your field, service, or specialty. In order to get your work, there is a point where you will need to outsource some key employer functions such as payroll and other human resource functions. So it stands to reason that it may be wise to cut back on the headaches and outsource your retirement plan administration. The concerns that plan sponsors should understand is that when it comes to their 401(k) plan, there is a difference between outsourcing and delegation. So this article is going to make 401(k) plan sponsors like you understand what outsourcing your plan administration with an ERISA §3(16) administrator entails and the traps you should avoid if you choose that route. Running a business is a complicated activity. You have to be an expert in your field, service, or specialty. In order to get your work, there is a point where you will need to outsource some key employer functions such as payroll and other human resource functions. So it stands to reason that it may be wise to cut back on the headaches and outsource your retirement plan administration. The concerns that plan sponsors should understand is that when it comes to their 401(k) plan, there is a difference between outsourcing and delegation. So this article is going to make 401(k) plan sponsors like you understand what outsourcing your plan administration with an ERISA §3(16) administrator entails and the traps you should avoid if you choose that route.

For the article, click here.

|

|

|

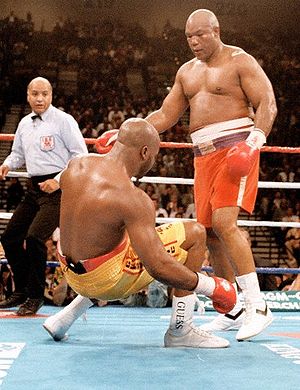

It Happened! Changes In The 401(k) Industry That Could Affect Your Plan.

Down goes Moorer with a right hand.

I've been a boxing fan since I was a kid when Marvin Hagler, Larry Holmes, Aaron Pryor, Tommy Hearns, Sugar Ray Leonard, and Mike Tyson were the premier boxers. One of my favorite boxing moments was in 1994 when 45-year-old George Foreman won the heavyweight title of the world by knocking out Michael Moorer with one punch. As Moorer was counted out, Jim Lampley proclaimed: "it happened, it happened." Foreman was being beaten for 9 rounds, but Moorer made this mistake of standing right in front of Foreman. Like the idea of a 45-year-old regaining the world heavyweight title, there are a lot of things over the past 20 years that people said couldn't happen when it comes to retirement plans and it did. This is about changes in the retirement plan industry that happened that can affect your 401(k) plan. I've been a boxing fan since I was a kid when Marvin Hagler, Larry Holmes, Aaron Pryor, Tommy Hearns, Sugar Ray Leonard, and Mike Tyson were the premier boxers. One of my favorite boxing moments was in 1994 when 45-year-old George Foreman won the heavyweight title of the world by knocking out Michael Moorer with one punch. As Moorer was counted out, Jim Lampley proclaimed: "it happened, it happened." Foreman was being beaten for 9 rounds, but Moorer made this mistake of standing right in front of Foreman. Like the idea of a 45-year-old regaining the world heavyweight title, there are a lot of things over the past 20 years that people said couldn't happen when it comes to retirement plans and it did. This is about changes in the retirement plan industry that happened that can affect your 401(k) plan.

To read the article, please click here.

.

|

|

|

|

Plan Sponsors Need To Deal With A Whole New 401(k) World.

It's a different world from where you've come from.

I've been an ERISA attorney for over 19 years and 401(k) plans have dramatically changed because of law changes, technological change, and changes in the marketplace. The problem is that most plan sponsors are stuck back in time when the courts and the government made it impossible for them to be sued or penalized. Business practices that were legal back then have been either eliminated or curbed because the courts and the Department of Labor (DOL) have frowned on them. What was good then isn't what's good now. Retirement plan sponsors need to understand the increased potential liability as plan fiduciaries and the best way to understand the changes that have taken place in the 401(k) plan business over the last 20 years. This article will let 401(k) plan sponsors understand how and why they need to be more vigilant in their role as a 401(k) plan fiduciary. I've been an ERISA attorney for over 19 years and 401(k) plans have dramatically changed because of law changes, technological change, and changes in the marketplace. The problem is that most plan sponsors are stuck back in time when the courts and the government made it impossible for them to be sued or penalized. Business practices that were legal back then have been either eliminated or curbed because the courts and the Department of Labor (DOL) have frowned on them. What was good then isn't what's good now. Retirement plan sponsors need to understand the increased potential liability as plan fiduciaries and the best way to understand the changes that have taken place in the 401(k) plan business over the last 20 years. This article will let 401(k) plan sponsors understand how and why they need to be more vigilant in their role as a 401(k) plan fiduciary.

To read the article, please click here.

|

Retirement Plan Sponsors Can't Afford To Be Cheap.

It costs more in the long run.

There is nothing wrong with being thrifty. You should never pay full price for something that you can get on a discount. Being thrifty is different from being cheap. Being cheap is about not wanting to pay for something just because you don't want to pay for it. I was a Vice President at my former Synagogue and nothing irritated me than members who didn't want to pay their dues when everyone knew they could afford to pay for it. When it comes to sponsoring a retirement plan, plan sponsors have a duty to pay only reasonable plan expenses, which means they have to be thrifty. Paying reasonable plan expenses isn't about paying as little as possible, so it means that plan sponsors don't need to be cheap. Quite honestly, they can' afford to be cheap because being cheap can cost a plan sponsor a lot more in the long run. There is nothing wrong with being thrifty. You should never pay full price for something that you can get on a discount. Being thrifty is different from being cheap. Being cheap is about not wanting to pay for something just because you don't want to pay for it. I was a Vice President at my former Synagogue and nothing irritated me than members who didn't want to pay their dues when everyone knew they could afford to pay for it. When it comes to sponsoring a retirement plan, plan sponsors have a duty to pay only reasonable plan expenses, which means they have to be thrifty. Paying reasonable plan expenses isn't about paying as little as possible, so it means that plan sponsors don't need to be cheap. Quite honestly, they can' afford to be cheap because being cheap can cost a plan sponsor a lot more in the long run.

To read the article, please click here.

|

|

Plans should get rid of forfeitures.

No sense that they should just sit there.

Forfeitures that occur when people terminate service from retirement plans is usually a problem when the plan sponsor and their providers forget about them. Whether forfeitures are used to pay expenses, reduce employer contributions or is reallocated is specified in the plan document. The problem is when they just left there to collect dust.

Forfeitures should be allocated in the year that they occur. If they don't, it might be an issue for the Internal Revenue Service (IRS) or the Department of Labor (if participants are deprived of an employer contribution from these forfeitures).

There is no reason that an employer should have hundreds of thousands of dollars growing each year in forfeitures, they should be allocated annually. Otherwise, the plan may run into an issue and it's silly to have compliance issues with something as silly as holding onto forfeitures.

So if you have a client with loads of forfeitures, tell them to get rid of them.

|

The problem with multiple loans.

It should be one to a customer.

When drafting new 401(k) plans, I always recommend allowing for a loan provision. I know there are quite a few plan providers who don't want any provisions that allow "leakage" of retirement assets, but I believe that when times are tough, plan participants should have access through a loan that they can repay.

As far as loans go, I only want one loan outstanding at a time. If participants want a loan, fine, but let's just let have one crack at it. A 401(k) plan shouldn't turn into a payday loan type operation. However, the real reason that I'm against multiple loans is the difficulty in recordkeeping. Recordkeeping multiple plan loans can be an absolute headache especially when it comes to recordkeeping repayments. I've seen too many situations where errors in recordkeeping let one or more loans go into default and becoming a deemed distribution or a prohibited transaction when not deal with correctly.

If you ask for trouble, you'll get it and I think that plan sponsors offering multiple plan loans are asking for it by allowing multiple loans that can only lead to a headache.

|

The Rosenbaum Law Firm Review, January 2018

734 Franklin Avenue, Suite 302

Garden City, New York 11530 Phone 516-594-1557 Fax 516-368-3780

Attorney Advertising. Prior results do not guarantee similar results.

Copyright 2018, The Rosenbaum Law Firm P.C. All rights reserved.

|

|

|

|

|

|

|

| |

|