|

|

The New Fiduciary Rule: What It Means To Plan Sponsors

Bottom line: what does it mean?

More than a dozen years ago, there was a medical report that dental plaque could cause heart disease. I thought it was some sort of dental conspiracy to increase revenue as fluoridated water and other dental hygiene has had to have a negative effect on the dentists' bottom line. Regardless of my cynicism, good oral health is important because many health problems are actually derived from poor oral hygiene. While some people only see a dentist when something in their mouth hurts them, many visit the dentist for annual or semi-annual checkups as preventative care, to avoid dental problems later. Brushing, flossing, and checkups help avoid root canals, caps, and dentures. More than a dozen years ago, there was a medical report that dental plaque could cause heart disease. I thought it was some sort of dental conspiracy to increase revenue as fluoridated water and other dental hygiene has had to have a negative effect on the dentists' bottom line. Regardless of my cynicism, good oral health is important because many health problems are actually derived from poor oral hygiene. While some people only see a dentist when something in their mouth hurts them, many visit the dentist for annual or semi-annual checkups as preventative care, to avoid dental problems later. Brushing, flossing, and checkups help avoid root canals, caps, and dentures.

To read the article, please click

here.

|

The Bottom Line On What Retirement Plan Sponsors Need To Do.

This is what they need to do.

I worked for a third party administrator (TPA) for almost 5 years and one of my favorite things about the boss there was that he just wanted to cut to the chase. We had an actuary who developed a speech im- pediment when he was nervous, and when asked a question by the boss, he would either stammer or go through an actuarial tangent that no one would understand. The boss would ask the actuary what the bot- tom line was. Plan sponsors need to know the bottom line and this is what this article is all about when it comes to their responsibility. I worked for a third party administrator (TPA) for almost 5 years and one of my favorite things about the boss there was that he just wanted to cut to the chase. We had an actuary who developed a speech im- pediment when he was nervous, and when asked a question by the boss, he would either stammer or go through an actuarial tangent that no one would understand. The boss would ask the actuary what the bot- tom line was. Plan sponsors need to know the bottom line and this is what this article is all about when it comes to their responsibility.

For the article, click here.

|

|

|

Plan Document Problems That Can Be a Pain for Plan Sponsors.

There is something wrong with hearing nothing, seeing nothing.

Retirement Plan documents must be written; they just can't be some oral promise to pay retirement plan benefits. A written plan document is a legal document with legal ramifications in governing a legal entity known as a retirement plan. A retirement plan document can cause many issues for a retirement plan sponsor, and since most plan sponsors are wary of ERISA attorneys because of their billing practices (don't worry, I charge a flat fee) many don't know. So this "free" article can help plan sponsors take count of the many problems their plan document can have on their retirement plan and what steps they should take to avoid these problems. Retirement Plan documents must be written; they just can't be some oral promise to pay retirement plan benefits. A written plan document is a legal document with legal ramifications in governing a legal entity known as a retirement plan. A retirement plan document can cause many issues for a retirement plan sponsor, and since most plan sponsors are wary of ERISA attorneys because of their billing practices (don't worry, I charge a flat fee) many don't know. So this "free" article can help plan sponsors take count of the many problems their plan document can have on their retirement plan and what steps they should take to avoid these problems.

To read the article, please click here.

|

|

|

|

|

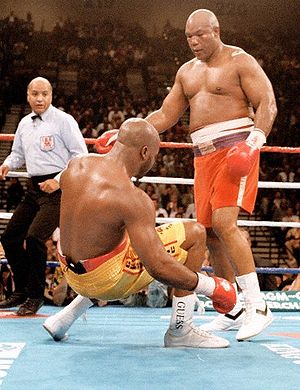

Yes, it did.

I love boxing and one of my favorite fights is when George Foreman shocked the world and knocked out Michael Moorer to become heavyweight champion at age 45. Jim Lampley doing the HBO broadcast proclaimed: "it happened! It happened!"

When the first big lawsuits started going against some large 401(k) plans, naysayers like this fellow on LinkedIn named Elmer said that talking about fees and fiduciary issues to small to medium sized 401(k) plan is meaningless because small to medium sized 401(k) plans don't get sued.

I always said that just because small to medium sized plans weren't sued doesn't mean that they won't be sued in the future.

Well, it happened, it happened.

A new class-action lawsuit was filed in federal court in Minnesota that targets excessive 401(k) fees in a $9 million plan. The suit, Damberg v, LaMettry's Collision Inc., claims that plan fiduciaries breached their duties under ERISA for allowing excessive fees to be charged for plan investments, record keeping, and administration.

What does it mean? It means that the threat that financial advisors and ERISA attorneys like me having been saying for years is finally a reality, small plans can be sued.

If you have a small to medium sized 401(k) plan or know someone that does, maybe it's time to have a discussion about plan fees if a discussion hasn't taken place before.

|

For audit situations, there is one.

I had a client who had been undergoing a Department of Labor (DOL) audit. Their mistake? Years ago, a former participant asked for a distribution from this trustee directed profit sharing plan (so no 401(k)) and my client failed to respond. There was no second request as the participant contacted the DOL.

The plan is small potatoes; maybe $700,000 in assets and the employer can't make employer contributions since the economy downturn a few years back.

The DOL auditor conducted an interview with the client. I sat in on the call without alerting my presence because the last thing I wanted to do is let the DOL agent be alarmed that ERISA counsel was retained. The agent sounded so young and the last thing I wanted to do was scare her.

The interview basically was a script, she even asked questions that only pertained to a 401(k) and my client alerted that the plan had no salary deferrals. The script sounded like one of my articles (without the cultural allusions to Caddyshack, Airplane!, and The Godfather). The DOL agent wanted to know if the plan had an investment policy statement, whether there was a financial advisor on the plan, whether that advisor is in contact, and whether there is a process to review the advisor's work. Additional questions were about the third party administrator, where there was a contract with them, and fee disclosure. Thankfully, the plan sponsor was able to give the right answers and the audit concluded quickly.

The lesson here is that whether the plan is audited by the DOL because of a complaint or something random, a plan sponsors needs to have a well run retirement plan so they could give the DOL agent the correct answers they are looking for. Better have a plan that is well run prior to a DOL audit, it's less costly that way.

|

Meaningless Plan Surveys.

They don't know what they don't know.

There was a new 401(k) plan sponsor survey on which providers are associated with being a "good value for the money".

Providers Most Associated with "Good Value for the Money"

Among all plan sponsors

1 Empower Retirement

2 Ascensus

3 Fidelity Investments

4 Betterment

5 OneAmerica

6 Vanguard

7 Paychex

8 American Funds

9 ADP Retirement Services

10 Wells Fargo

Source: Market Strategies International: Cogent Reports™, Retirement Planscape: May 2016

I think most of these providers are actually good, but did you see what I see? The two biggest payroll providers made the list. What does that tell you? Plan sponsors may know about paying low fees, but they might not really understand good value. These payroll providers charge a reasonable fee, but their lack of attention to compliance testing details doesn't make them a good value when errors are discovered and have to be corrected.

|

The Rosenbaum Law Firm Review, June 2016

, Vol. 7 No. 6

734 Franklin Avenue, Suite 302

Garden City, New York 11530 Phone 516-594-1557 Fax 516-368-3780

Attorney Advertising. Prior results do not guarantee similar results.

Copyright 2016, The Rosenbaum Law Firm P.C. All rights reserved.

|

|

|

|

|

|

|

| |

|