|

Spring Planting Complete -

Now What!

Blaise D Boyle, Director of Seed and Agronomy

| | |

With spring grain planting complete, the focus now shifts to crop establishment and early-season field management. Farmers should closely monitor soil moisture and seed emergence to ensure uniform stands across the field. Timely rainfall or irrigation is critical during this stage, as young grain crops such as wheat, barley, oats, and corn are especially vulnerable to stress while root systems develop. Producers should also watch for uneven germination, soil crusting, and early weed competition, as these issues can significantly reduce yield potential if left unaddressed.

As crops move into active vegetative growth, nutrient management and pest control become key priorities. Nitrogen applications may need to be adjusted based on crop conditions, weather patterns, and soil test results to support healthy tillering and canopy development. Weed pressure is typically managed through herbicide programs or mechanical control methods before weeds become overly competitive. Farmers should also scout regularly for insect pests and fungal diseases, which can spread rapidly under favorable conditions. Consistent field monitoring during this stage helps protect yield potential while minimizing unnecessary input costs. If you have questions, reach out to your CGI representative.

Once the crop is growing steadily, attention turns toward long-term crop performance and seasonal planning. Weather patterns, particularly temperature and rainfall during late spring and early summer, begin to shape grain fill and overall yield expectations. Farmers may use crop scouting reports, satellite imagery, or precision agriculture tools to evaluate field health and identify problem areas. At the same time, equipment maintenance, grain storage preparation, and harvest marketing strategies begin to take shape. Although planting season is complete, crop success now depends on consistent management and the ability to respond quickly to changing field conditions. For the latest crop and market information, be sure to connect with your CGI representative, they are there to help support a successful year.

| | |

|

DURUM

Ryan Statz, Merchant

| | |

- Durum markets are firming on the heels of the rally in the wheat complex, driven largely by drought concerns across the U.S. Plains and Midwest.

- While the U.S. Plains and Midwest have received most of the attention, durum production regions are also experiencing dryness, especially in northeast Montana.

- At the interior, durum is priced flat to, or even at a discount to, DNS in some areas. This will undoubtedly lead to grower reluctance to sell. At the same time, buyers are not yet willing to chase the market higher; at least not yet. There is still too much old crop supply available, and the potential for lower new crop stocks has not cornered many buyers to secure additional coverage. As a result, durum values have strengthened, but only slightly.

- With ample old crop stocks still available in both the U.S. and Canada, more risk is being placed on new crop markets and production prospects. As a result, most regions are showing carry market structures heading into new crop.

- Additional near-term pressure and risk stem from higher freight and fuel costs throughout the supply chain, which are rationing nearby demand.

- The market continues to weigh large old crop supplies, expectations for sizeable domestic and international crops, generally favorable planting weather around the world (with some exceptions noted above), and stagnant demand.

- Markets will continue to focus on:

- How North American and global ending stocks ultimately shape up.

| | |

|

HARD RED WINTER WHEAT

Ryan Statz, Merchant

| | |

- New crop HRW production concerns continue to fuel KC futures, lifting the broader wheat complex higher. Ongoing drought conditions remain the primary driver behind the rally.

- On Monday, the USDA further downgraded crop conditions across several key HRW production regions:

- Kansas declined 5% week over week in Good/Excellent ratings to 17%, versus 48% last year.

- Oklahoma declined 7% week over week to 9%, versus 53% last year.

- Texas declined 6% week over week to 10%, versus 42% last year.

- Montana, conversely, improved 10% week over week to 39%, compared to 83% last year.

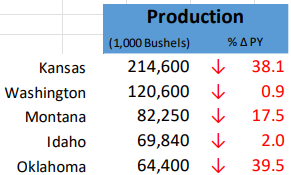

- On Tuesday, May 12, the USDA released its first state-by-state production forecasts for the 2026/27 crop year. The implied production forecasts are as follows:

| |

-

Altogether, the state-by-state forecasts point to a 514 million bushel HRW crop. This compares to the 2025/26 crop size of 804 million bushels, representing a substantial decline that has fueled futures markets and will likely push the market into more of a demand-rationing mindset.

- Market dynamics are expected to shift as destination markets reassess supply options and pricing relationships.

- Gulf and domestic basis markets are firming due to a lack of offers from nervous and cautious suppliers.

-

PNW basis markets are facing pressure from higher flat prices and increased freight and fuel costs, which have significantly rationed demand.

- With the PNW under pressure, there is hope that buyers will step in to help fill part of the demand void.

-

We are beginning to see some of this emerge as congestion in the Panama Canal, driven by increased oil tanker traffic, creates delays for vessels. This is leading to increased interest in PNW exports from Latin American countries, though it remains to be seen whether meaningful follow-through business develops.

- With abundant and competitively priced crops available internationally, U.S. markets will remain highly dependent on demand performance, both domestically and in export channels. Markets will also be watching closely for class-by-class substitution trends as HRW values strengthen and Northern Spring wheat prices soften.

| | |

|

HARD RED SPRING WHEAT

Justin Beach,

Red Wheat Product Line Manager

| | | |

Spring wheat continues to follow the direction of the HRW market, with the supply shock from the latest WASDE report sparking a sharp rally. The recent strength in the market has reportedly encouraged increased spring wheat acreage, something we have consistently heard from both internal teams and other grain companies.

Basis levels in the country are holding steady to lower following sharply higher shipping costs driven by fuel surcharges and elevated secondary freight rates. We are also seeing nominally higher values out of Canada, while U.S. pricing is beginning to narrow the gap versus Canadian offers. The U.S. will likely need to remain competitive for new crop business against the tail end of old crop supplies in Canada. The question moving forward is whether U.S. values move lower, Canadian values move higher, or if both occur simultaneously.

At this point, millers are not yet showing aggressive buying interest given the current carry market structure. However, we believe more HRS wheat will ultimately be purchased in place of HRW due to projected crop sizes and, more importantly, widening price spreads between the classes. The weather market continues.

| | |

|

SOFT WHITE WHEAT

Steve Yorke, Merchant

| | | |

It has been a wild couple of weeks in the grain sector. Chicago futures are up roughly 50 cents since our last newsletter, while cash white wheat prices have gained 20–25 cents, moving back to around $6.45. A nice rally being fueled by the USDA report released on May 12.

Key highlights from the report include:

- U.S. wheat carryout projected down 173 million bushels versus last year

- HRW production down 25% year over year as dry conditions persist across the U.S. Plains

- Tighter global wheat stocks, though still within the range of trade expectations

- SWW ending stocks remain burdensome at this time, with export projections for the upcoming marketing year estimated at 200 million bushels. While this is still a healthy export number, additional demand will be needed to further reduce stocks.

Currently, we are seeing negative basis levels for SWW, something that has been relatively uncommon over the past several years. For growers with HTAs in place, futures markets will likely need to settle back and export demand improve before basis returns to more typical levels in the 30–60 cent range. There is still plenty of time for basis to recover.

While the recent rally has been encouraging, current pricing is beginning to push U.S. wheat out of the export market as global values remain considerably cheaper. As always, keep orders working and stay in close contact with your grain buyer to remain informed on the latest developments impacting these highly volatile markets.

https://columbiagrain.com/producer-solutions/

|

| |

|

William Warnock,

Guest Commentator - Buyer

Jamestown, ND

CORN

| | | |

Over the past several weeks, the corn market has steadily rallied, driven largely by major geopolitical developments. The situation surrounding the Strait of Hormuz has played a significant role in market increases, as rising fertilizer, fuel, and energy costs are beginning to have a broader impact across the market. At the same time, the high-level meeting between the U.S. and China, which many view optimistically, is now underway, though outcomes remain uncertain. With potential implications involving Iran, along with the possibility of large agricultural purchase announcements coming out of Beijing, markets will be closely watching both the discussions and any resulting impact on prices.

The WASDE report released on Tuesday also provided some support to corn markets. Projections for slightly lower planted acreage and lower year-over-year yields continue to keep sentiment constructive for corn. Going forward, those numbers will remain important to monitor, as stronger yields or increased acreage could quickly shift the outlook and pressure values lower. Export pace from both the PNW and Gulf has also remained consistently strong. While export demand was initially viewed as largely optimistic, it is now helping reinforce current price levels. Futures markets have moved above several key support levels, though with multiple market-moving events still unfolding, those levels may continue to be tested in the weeks ahead.

On a more localized level, the political issues that dominated earlier conversations this year have started to take a back seat to more immediate growing season concerns. Many farmers continue to ask whether rising fertilizer costs will reduce corn acreage, though most indicate they already secured fertilizer coverage for the upcoming season. Moisture conditions remain a major concern, particularly as Kansas, Nebraska, and Oklahoma continue to struggle with drought, while dry conditions are also beginning to expand into western North Dakota. With no frost currently in the forecast, seeding progress has roared along and should be finished shortly. With plenty of stories of corn still in the bin that will start to and is expected to wrap up soon. At the same time, there are still reports of significant old crop corn remaining in on-farm storage that is expected to begin moving once planting concludes, as preparations continue for what could be a very active summer season.

| | |

|

BARLEY

Matthew Schorn, Merchant

| | | |

Malt Demand and Price Trends

- The weaker demand story for malt barley continues as consumer preferences shift away from beer toward other alcohol alternatives. U.S. barley demand is heavily tied to malt production compared to other countries, where feed barley drives the market.

- Malt demand does appear to be finding more of an equilibrium, and things are beginning to stabilize rather than continue declining.

-

New crop contracts seem to have run their course, with production contracts largely filled. We saw a 50¢–$1.00/bu premium to feed markets, and now attention will shift to production and quality outcomes.

-

Seeding is wrapping up, and the focus will shift to weather and growing conditions. Crops are looking for their first significant rainfall to get things started.

Canadian Domestic Feed Market

- Domestic feed markets are starting to firm as export pace remains strong and the rally in the wheat board pulls other grains higher.

- With the wheat board firming, the milling-feed spread has widened, making wheat less competitive against barley and corn. One less feed substitute could push additional demand toward corn and barley, which may support firmer values.

- Corn remains competitive in feed rations relative to barley, which will likely limit any major upside potential for barley prices.

- We are starting to see some new crop interest as early crop conditions gain attention from feeders. Historically, feeders have been able to buy at lower levels closer to new crop in an inverted market.

- Crop conditions across all commodities will remain the main focus moving forward.

|

| |

Flax

Sean Ferguson, Merchant

| | | |

StatsCan reported March Canadian flax stocks at 380,000 MT, higher than industry expectations, which generally ranged between 320,000–350,000 MT. Exports remain a key variable for overall carryout levels, as current demand from both European and Chinese buyers continues to appear supportive.

Movement of flax into the Lakes region and to the West Coast has increased in order to fulfill export sales to Europe and China, respectively. If export demand continues at a strong pace, Canadian carryout levels could move closer to more average historical levels.

Nearby prices are expected to remain supported as Canadian growers begin fieldwork. However, the market still holds an inverse to new crop values, meaning nearby prices are expected to gradually converge toward new crop levels as long as crop conditions in Eastern Europe and Canada remain favorable.

While oilseeds such as canola and soybeans have benefited from recent volatility in energy and biofuel markets, flax has not received the same level of support, as it is not used as a feedstock within biofuel programs.

Another market worth monitoring is sunflower seed. Global sunflower production is projected to increase to 61.8 MMT, up from 56.2 MMT, which could place additional pressure on flax values. At the same time, Black Sea flax acreage is expected to increase year over year, continuing to weigh on the broader global flax market.

| | |

In its latest World Oilseed Markets and Trade report, the USDA is projecting record oilseed production and record crush volumes for the upcoming crop year. This outlook is being driven by increasing vegetable oil demand from the biofuel sector, along with additional crush capacity expected to come online.

Global rapeseed and canola supplies remain large, with countries such as Russia and India projected to produce record crops. Canada’s canola crop is currently estimated at 22 MMT, not far from last year’s production of 21.8 MMT. Despite expanding global crush capacity, world ending stocks are still expected to increase year over year, which could eventually pressure prices.

Crush margins remain strong as elevated energy prices continue supporting vegetable oil values globally, particularly in North America.

The CAD/USD exchange rate has moved modestly lower over the past week, as the strength of the U.S. dollar has continued to outpace the Canadian dollar. Persistent inflation expectations have tempered hopes for near-term interest rate cuts, helping support the USD, while stronger crude oil prices continue to lend support to the CAD.

It remains to be seen how sustained increases in energy prices will ultimately impact the global economy. Historically, the broader macroeconomic effects of sharp energy price increases tend to lag by roughly four quarters from the initial spike. In general, recessionary economic environments are not typically supportive for oilseed prices.

| | |

US market is currently stagnant due to a lack of farmer selling and participation at current elevator bid levels. The global market continues to trade at lower values and find cheaper origins outside of the US. Unfortunately US domestic demand is not large enough to clear the remaining old crop stocks, primarily in Montana and North Dakota. Sierra/PNW variety chickpeas continue to find demand in the global market.

In Pakistan, the market is flooded with chickpeas for the time being. They will continue to buy at current values but are unwilling to pay the higher prices. We are watching to see if rains on the harvest in Mexico will impact quality and bring some demand back into the USA.

| |

International pea markets were little changed week over week for both yellow and green peas. Another large yellow pea crop is expected out of the Black Sea region, which is likely to keep a lid on prices in the near term. Even so, we have seen a modest increase in yellow pea bids to farmers as buyers look to secure coverage for the U.S. domestic market.

Green pea markets remain more subdued as major global buyers continue to work through large existing stocks from Argentina and Canada, while growers continue holding out for higher prices. At this time, we do not expect a quick recovery in global green pea bids.

| |

Any pricing support in lentils resulting from the Section 32 tender has now largely faded, and pricing for #1 grades across all commodities pulled back last week. India has announced a tender for 60,000 MT of split green lentils or local tur. While North American green lentils are expected to be selected due to their more competitive pricing, we do not anticipate a significant pricing response in North American markets, as India currently has ample supply available.

The CGI pulse team is attending the Global Pulses Conference this week, and so far international markets do not appear to be placing much attention on the dry conditions in Montana. However, global markets are currently supported by ample supply from multiple origins, and in Canada, the lentil crop is expected to get off to a favorable start.

| | US Pinto and Black Bean markets have been firm in recent weeks due to strong competition for new crop acreage. The main concern is a drastic reduction in the acreage base in both the MNDAK region as well as Nebraska/Colorado. However, Mexico has more than sufficient supplies of national grown pintos for the foreseeable future so upward price momentum can potentially stall if there is no demand follow through and/or significant demand rationing at higher prices. Navy bean markets stay well bid nearby but more supply is entering the market, particularly in the medium/large white bean categories. Kidney bean markets see a sufficient US Acreage base and a potentially large Argentina crop. | | |

Matt Schorn

May’s WASDE report released the first 2026/27 balance sheet projections, pointing to tighter grain supplies and helping support wheat markets early this week. President Trump is also meeting with President Xi in China to discuss trade, including U.S. soybean and corn exports.

The wheat outlook turned notably more bullish, with U.S. production forecast at 1.561 billion bushels, down 424 million bushels from last year. Lower harvested acreage and declining yields were the primary drivers behind the reduction, following deteriorating crop condition ratings. Hard Red Winter wheat saw the largest declines, while spring wheat acreage is also expected to decrease. USDA projects average U.S. wheat yields at 47.5 bu/acre, down from last year’s record 53.3 bu/acre.

USDA projects the 2026/27 U.S. corn crop at 15.995 billion bushels, down roughly 6% from last year’s record crop due to lower acreage and softer trend yields. Planted corn acreage is forecast at 95.3 million acres, down 3.5 million acres year over year, while yield is projected at 183.0 bu/acre compared to 186.5 bu/acre last season.

USDA projects the U.S. soybean crop at 4.435 billion bushels, up 173 million bushels from last year due to higher harvested acreage and trend-line yields. Harvested acreage is expected to rise to 83.7 million acres, while yields are forecast to remain unchanged at 53.0 bu/acre. Demand remains supportive, driven by record soybean crush projections and continued growth in soybean oil demand from the biofuel sector.

Markets remain highly sensitive to weather forecasts and crop condition changes heading into the growing season. Geopolitical tensions, including ongoing concerns surrounding the Strait of Hormuz, continue to support energy and freight markets, adding broader macro volatility across commodity markets.

In the current environment, Hedge-to-Arrive contracts remain an effective tool for locking in elevated futures prices while leaving basis open for potential improvement later in the season. When rallies are driven by geopolitical risk and supply concerns, futures markets can become inflated relative to local cash values as the market works to ration demand. For old crop bushels, Cash+ contracts may also provide an opportunity to capture additional value while futures remain elevated.

The additional risk-management options listed below can help producers manage volatility, stay disciplined, and take advantage of opportunities when the market presents them.

Columbia Producer Solutions Tools:

- Good-till-Cancelled (GTC)

- Basis Contracts

- Accumulator Contracts

- Ratchet Orders

- Collar Orders

Reach out to your local buyers and managers to review these options, or others, on our Columbia Producer Solutions platform of marketing tools.

| | |

INTERNATIONAL BUSINESS

Yuya Takano, Wiley Wang

International Merchants

| | |

CORN

The export market remains active and firm, with some Asian buyers continuing to purchase corn from the PNW. Japan resumed buying August-shipment corn following the Golden Week holidays, while Korea has also issued tenders for July and August shipments, concentrating a significant amount of demand on the PNW. Export capacity for August is expected to remain tight as many terminals have scheduled maintenance during that period. The market is also finding support from expectations surrounding potential agricultural purchase announcements tied to the Trump–Xi meeting this week, helping keep export sentiment firm.

SOYBEANS

The PNW soybean export market remains relatively quiet, with limited activity and subdued Chinese demand contributing to an overall softer tone. Many buyers are currently covering needs with Brazilian and Gulf-origin soybeans. However, ocean freight rates have surged due to tensions involving Iran, while congestion and waiting times at the Panama Canal continue to worsen. To avoid potential shipping delays, Japanese crushers made emergency purchases of PNW soybeans for July shipment, though the broader trend still favors Brazilian origin supplies. Market attention remains focused on the outcome of the Trump–Xi meeting and the possibility of agricultural purchase agreements being announced. At the same time, uncertainty remains around whether China’s buying interest could stay limited due to geopolitical concerns and ongoing energy market instability in the Middle East.

WHEAT

The recent rally in wheat futures, driven by weather concerns and geopolitical tensions, continues to create challenges for overseas buyers. With some purchasing demand delayed for an extended period, we are beginning to see certain end users step in to cover July and August positions. Significant volatility in ocean freight markets remains an ongoing challenge, and when combined with higher commodity prices, many end users are questioning whether they should continue waiting before making purchases.

In PNW production areas, winter wheat crop conditions are performing better than the reported national average. However, the overall bullish market sentiment is not currently helping encourage movement of the upcoming new crop.

| | | | |