ISSUE 171, April 17, 2026 | | | |

Plant with a Plan

Lars Birkeland, Seed Production Agronomist

| | |

Warren Buffett once said, “An idiot with a plan can beat a genius without a plan.” Now, he wasn’t calling anyone an idiot, but he definitely emphasized the importance of having a solid plan and sticking to it. Buffett’s investment success is a perfect example of this principle. He’s all about value investing—not chasing quick flips but focusing on quality companies with long-term growth potential. Fun fact: he even owns a big stake in the parent company of Columbia Grain.

For decades, he’s been consistent with his strategies, some might say almost boring—until you look at his impressive results.

The past year hasn’t been easy for agriculture, has it? With tariffs, international conflicts, and looming droughts, it’s been a rough ride. In times like these, having the right game plan is crucial. Sometimes the “boring” approach can outperform the flashy one. Taking a little extra time to ensure your drill is leveled and fine-tuned can lead to a more consistent crop stand. And considering split fertilizer applications can help manage those skyrocketing costs while boosting efficiency.

Don’t forget about your marketing strategies, either. While selling everything on a cash contract is straightforward, it might not maximize your market potential. Exploring options like basis contracts, hedge-to-arrive agreements, accumulators, and good-til-canceled orders can help you create a more profitable marketing strategy.

So, let’s get those plans in place and aim for a fantastic season together!

| | |

|

DURUM

Ryan Statz, Merchant

| | | |

After eight months of a mostly bearish tone, there have been slight signs that pressure may be easing, driven by several factors:

- U.S. planting season is right around the corner, which will limit inbound grower movement. Steady grower selling has kept markets under pressure in recent months.

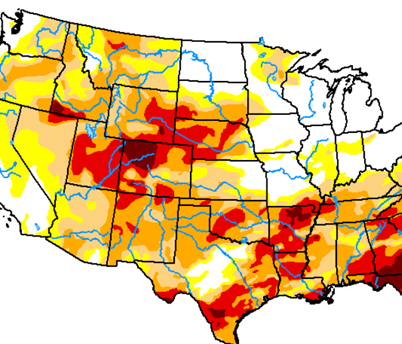

- Extremely favorable global weather is beginning to show some signs of deterioration. U.S. conditions—particularly in Montana—are well known, but Europe (namely Italy and Turkey) has received excessive moisture, with more in the forecast.

- U.S. acreage is expected to decline (down 11% year-over-year), with Canadian forecasts also pointing to reduced plantings.

- Other wheat classes continue to firm on the heels of U.S. dryness and ongoing geopolitical events overseas.

With ample old crop stocks still available in both the U.S. and Canada, more market risk is shifting to new crop production and yield prospects. As a result, flat-to-inverse markets are flattening, and some regions are beginning to show carry structures into new crop.

- Additional near-term pressure/risk remains in elevated freight and fuel costs throughout the supply chain, which continue to ration nearby demand.

Markets still see burdensome old crop supplies, large domestic and global production prospects, mostly favorable planting weather worldwide (with some exceptions noted above), and no meaningful increase in demand.

Markets will continue to focus on:

- How North American and global ending stocks ultimately shake out.

| | |

|

HARD RED WINTER WHEAT

Ryan Statz, Merchant

| | | HRW markets have seen an impressive cash rally over the last six weeks, initially driven by geopolitical events in the Middle East, followed by expanding dry conditions moving into the U.S. Southern Plains. Crop conditions continue to deteriorate in Kansas, Colorado, Oklahoma, and Texas, and that is clearly working its way into both futures and basis markets. | | |

As a result, we are seeing markets increasingly diverge from one another.

- Gulf/domestic basis markets are firming.

- PNW basis markets are under pressure due to higher flat prices and increased freight/fuel costs, which have rationed demand in a meaningful way.

- With the PNW under pressure, buyers may be incentivized to help fill that void.

We are beginning to see signs of this as Panama Canal congestion (driven by increased oil tanker traffic) creates vessel delays leading to increased PNW interest from Latin American buyers. Time will tell whether follow-through trade develops.

With abundant and competitively priced crops available internationally, U.S. markets will remain subject to demand-side pressure as we work to move domestic supply. The question remains: Will we see a summer push from growers ahead of harvest, or will carry out stocks expand as currently projected?

| | |

|

HARD RED SPRING WHEAT

Justin Beach,

Red Wheat Product Line Manager

| | | |

Spring wheat flat price has found support as of late. The initial run-up was supported by crude oil and the war with Iran. As the wheat market grew tired of that narrative, it began to recognize that higher freight and fuel costs throughout the supply chain would ration demand, and we have certainly seen that play out. Ocean freight remains expensive and sticky.

Now, spring wheat is following HRW higher amid legitimate concerns over U.S. production potential. We are seeing domestic and Texas Gulf basis firm as a result. There are significant concerns across Kansas, Oklahoma, Nebraska, and Texas regarding crop conditions.

In addition, vessels continue to struggle to pass through the Panama Canal. This has increased PNW interest from Latin American countries, and we will see whether follow-through trade develops. Duluth is back open, and attention will be on grain movement there and into Mexico, where we are seeing increased interest this week.

Domestic millers remain cautious in the spring wheat market as most of the action continues to center around HRW. The PNW remains quiet, with Canadian supplies considerably cheaper for more generic specification profiles.

Expect continued and increased volatility through planting season, particularly with limited farmer hedge pressure in the market.

| | |

|

SOFT WHITE WHEAT

Steve Yorke, Merchant

| | | |

Another week of choppy trade for the markets. The wheat sector continues to be influenced by crude oil and the war in Iran. Fundamentally, little has changed as stocks continue to build and business remains on the light side.

One factor also pushing futures higher, particularly in the K.C. market, is the ongoing drought across much of the Southern Plains. Concerns over a potential cold snap this weekend are now adding to that support. As of this writing, K.C. is up another 20 to 25 cents, which is something to watch closely.

In the white wheat market, we are seeing continued rainfall across much of the PNW, with crop ratings currently well above last year’s levels:

- Washington: 92% Good/Excellent

- Idaho: 86% Good/Excellent

Both are up 15 to 20 points from last year. Oregon is sitting at 64% Good/Excellent, also up roughly 15 points year over year.

There is still plenty of time for conditions to change and for moisture to shut off, but as of today the crop is looking strong. Spring seeding is in full swing aside from some rain delays, though the next several days look dry and should allow for productive progress.

Today we sit at $6.25/bu and expect the market to remain in a relatively tight range of $6.00 to $6.30 over the next few months unless we see a major shift in demand or further escalation in the war in Iran.

Look for upcoming grower meetings in your area, and as always, feel free to reach out to your local grain office for guidance.

https://columbiagrain.com/producer-solutions/

|

| |

|

BARLEY

Matthew Schorn, Merchant

| | | |

Malt Demand and Price Trends

- The weaker demand story for malt barley continues as consumer preferences shift away from beer toward alternative alcoholic beverages. U.S. barley demand remains heavily tied to malt production, unlike other global markets where feed barley is the primary driver.

- New crop contracts are available with a 50-cent to $1.00/bu premium over feed markets.

-

Focus will shift to weather and growing conditions as we move deeper into weather markets over the coming months of the growing season.

Canadian Domestic Feed Market

- Feed markets are stabilizing as export demand takes a breather amid increased ocean freight costs tied to higher energy prices. Additional export demand will be needed to push the market higher, and we are not seeing that today.

- Domestic feed demand remains weak due to a mild winter and fewer cattle on feed, both of which are reducing overall feed grain demand. While exports are attempting to support values, soft feed demand should limit major swings.

- Corn remains competitive in feed rations in Southern Alberta, with supplies originating from Manitoba and North Dakota. This will likely cap any significant upside in barley values.

- We are beginning to see some new crop interest. While many feeders remain on the sidelines, others are starting to take positions. Historically, feeders have often been able to buy at lower levels closer to new crop, but this may present a good opportunity to evaluate new crop sales.

|

| |

Flax

Sean Ferguson, Merchant

| | |

- The flax market has remained relatively flat as we enter the spring seeding season.

- Movement to the West Coast has increased, presumably for export to China. Chinese buyers covering demand out of Canada are providing support to the North American flax market.

- The caveat is that European buyers have remained largely absent from the North American market due to ample remaining supplies in Kazakhstan.

- Despite improved export prospects, North American carryout stocks are expected to remain heavy.

| |

- The canola market has traded relatively flat over the past week. Given current positioning, a steeper downside appears more likely than a sharp rally in canola futures.

- The initial explosive volatility in energy markets has begun to subside as global trade flows adjust to the shutdown of the Strait of Hormuz. An end to the war would likely be bearish for energy prices, which would pressure vegetable oil values and, in turn, canola prices.

- Fund positioning may also contribute to downward pressure, as managed money continues to hold a record-long position in soybean oil futures and a canola position equal to roughly 70% of the record long.

- Crush margins remain strong, and crushers are eager to lock in those margins further out on the curve wherever possible.

- We are entering the weather market as most spring crops are expected to be planted soon across the Northern tier. Expect prices and volatility to increasingly reflect crop conditions in the weeks ahead.

- The CAD/USD has traded sharply higher over the past week as weakness has spilled into the U.S. dollar. Traders are increasing bets on successful peace talks, and capital has begun moving out of the USD as demand for its traditional safe-haven status eases.

| | With Section 32 announced and awards expected in late April, prices for lower-cost lentil varieties are likely to see a gradual short-term increase as remaining supplies of good quality product are bought off the farm. At the same time, with new crop planting approaching and processors looking to begin clearing out bins amid a fairly large carryover and with no significant quality advantage over Canadian supply, prices could ultimately trend more stagnant to slightly firmer. A key factor to watch will be whether India becomes more active in the U.S. market, global tensions and rising ocean freight risks could impact demand and influence how the new crop market develops in the coming months. | | U.S. chickpea values feel relatively unchanged despite the government tender recently announced. Chickpea values have remained stagnant for most of the current crop year due to heavy supplies in North America, and an extremely competitive global market. Quality spreads among chickpeas have widened dramatically, with true #1 quality being somewhat uncommon across northern tier growing regions. Chickpeas with high splits and low moisture seem to make up the bulk of stocks still unsold. Expect quality spreads to continue to widen (low/mid quality worth less and high-quality worth more) as long as other pulse price values remain suppressed. A slight decrease in chickpea acres for the upcoming crop year could propel high quality chickpea values higher but will likely have little to no effect on low/mid quality chickpeas- as the lesser quality chickpeas have to compete in the global space. | Ongoing trade uncertainty between the United States and China has continued to limit movement, contributing to suppressed pea prices and a sizable old crop carry with no major export outlet. Planting intentions for the new crop are expected to remain similar to last year, which will not significantly reduce the current oversupply. However, lower price levels could improve the U.S.'s competitiveness in markets where it has previously struggled to price in. In the short term, the current Section 32 government tender should provide some price support as suppliers position themselves ahead of award announcements in late April, but amid the trade tensions the support will likely manifest in stagnant prices. | Markets have been firmer in recent weeks due to combination of improved domestic demand and a more competitive new crop commodity complex. Both Pinto Beans and Black beans have appreciated in value about $3/cwt since the 3/31 prospective plantings report. Mexico continues to be well supplied by their nationally grown crop, but US origin is still trading but in much smaller quantities and more price sensitive. | | |

Matt Schorn

We are now entering the Northern Hemisphere growing season, where weather becomes the dominant driver of price volatility. Below normal perception, cold weather, and lower moisture reserves are driving the wheat markets higher.

Combine weather markets with the current geopolitical risk surround the United States and Iran, market volatility is at an all-time high. Markets continue to price sustained geopolitical risk, keeping energy and freight costs elevated.

The volatility we are seeing from the above discussions is where Columbia Producer Solutions tools such as Good-Till-Canceled (GTC) and Collar orders can provide value. GTC orders allow producers to automatically capture favorable price opportunities during sudden market spikes, while Collar orders help protect those gains by locking in a price floor while still being able to take advantage of any upside.

The additional risk-management options listed below can help producers manage volatility, stay disciplined, and take advantage of opportunities when the market presents them.

Columbia Producer Solutions Tools:

- Basis Contracts

- Hedge to Arrive (HTA)

- Accumulator Contracts

- Ratchet Orders

- Collar Orders

- Cash +

Reach out to your local buyers and managers to review these options, or others, on our Columbia Producer Solutions platform of marketing tools.

| | |

INTERNATIONAL BUSINESS

Yuya Takano, Wiley Wang

International Merchants

| | |

CORN

The PNW export market has remained relatively quiet for some time.

Japan has already covered around 70–80% of its July corn requirements, while no Korean tender has been issued since the one held on the 8th of last week. Taiwan has also not held any tenders this month and continues to stay on the sidelines until both futures and cash markets stabilize.

In the Gulf, transit through the Panama Canal remains constrained due to the increase in energy tankers, product tankers, and LPG vessels. As a result, many ships are being forced to sail via the Cape of Good Hope. With longer voyage times and firmer ocean freight rates, demand for nearby PNW shipments has been increasing.

As for Brazil, farmer selling has slowed recently against the backdrop of a stronger real, keeping interior prices firm. Under normal circumstances, demand from East Asia tends to shift toward Brazilian corn from August shipment onward. However, firm Brazilian FOB values, together with steady freight rates, are expected to support PNW maintaining its price competitiveness for the time being.

SOYBEANS

The truth behind the reported additional Chinese purchase of 8 million tons of U.S. soybeans remains unclear, and no notable buying has been confirmed so far. The key issue is whether policy-driven purchases will ultimately materialize.

China continues to buy Brazilian soybeans, and of the seven vessels reported yesterday, one was for new-crop shipment in the 2027/28 marketing year. In the Gulf, a certain volume of soybeans is being exported to Japan, but due to transit restrictions at the Panama Canal, many vessels are effectively left with only two options: rerouting via the Cape of Good Hope or waiting at Panama.

Because soybeans are more vulnerable to damage during extended voyages, crushers have begun considering the use of PNW soybeans, which could lead to increased demand for nearby PNW shipments.

WHEAT

Ocean freight on pacific route begin to stabilize with price for nearby position to soften. There are still more risks for deferred position, but overall market will go into more predicable behavior. We begin to see demand being shifted from gulf to PNW with super tight costs and capacity of Panama Canal. This might continue since more energy products will continue to shift to gulf. So far this has not created additional demand for PNW but it is very welcome.

Winter wheat weather now is in focus. Long term rain forecasts slightly vary from model to model but so far none of them are very friendly.

| | | | |