|

|

DURUM

Ryan Statz, Merchant

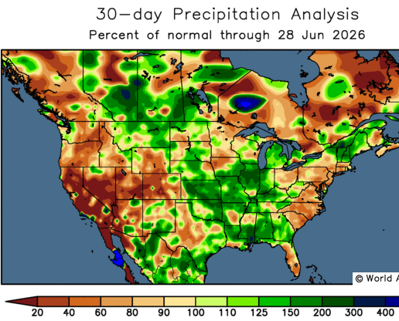

| | | - As we've said in previous updates, rain makes grain, and we've received more of it over the past few weeks.

| |

- For much of the same reason markets moved higher throughout April and May, they have now retreated following significant rainfall across North American durum production areas, improving crop prospects and early development. Risk was priced earlier, and now the market is shifting to a risk-off mindset.

- International production forecasts are also trending higher as harvest progresses in many regions.

- Quality remains a question mark in some areas, but increased production estimates could limit price appreciation in the nearby market.

-

Production forecasts continue to be revised, but we are becoming more confident that North African production will be substantial, which will undoubtedly reduce import demand to a significant degree.

- On June 30, StatsCan updated its acreage estimates for Canada. Durum acreage was revised lower to 5.86 million acres, down from the March estimate of 6.378 million acres and from 6.532 million acres planted in 2025.

-

Also on June 30, the USDA released updated state-by-state acreage estimates for the U.S. Compared to the March 2026 Planting Intentions report, total U.S. durum acreage was revised down another 6%, bringing planted area to 16% below last year.

- Montana acreage is estimated at 780,000 acres, down 12% year over year.

- North Dakota acreage is estimated at 980,000 acres, down 20% year over year.

-

While improved growing conditions and increased moisture are viewed as bearish factors, reduced acreage should provide some offsetting support to the market.

- As noted in previous reports, several outside factors continue to influence durum values, including:

- Ongoing turmoil in the Middle East

- Trade developments involving China

- Higher fuel and freight costs

-

Dryness in the Southern Plains affecting HRW wheat production

- Overall, the market continues to weigh large old-crop durum supplies, favorable crop prospects internationally, supportive growing conditions around the world, and a lack of increased demand.

| | |

|

BARLEY

Matthew Schorn, Merchant

|

| | |

Malt Demand and Price Trends

- The malt market appears to have found an equilibrium following a significant shift in consumer preferences away from beer and toward alcohol alternatives, albeit at lower price levels.

- We are seeing some old-crop demand for specific varieties ahead of new crop availability, but for the most part, demand appears to be well covered into the next crop year.

- Market focus has shifted to weather and growing conditions. El Niño may influence export supply chains from a global perspective; however, domestically, the U.S. market is currently focused more on quality concerns than production risk.

- With increased moisture and cooler temperatures, attention will turn to July to determine whether the malt crop can achieve the warm, dry finish needed to maintain quality. Any quality concerns could increase price volatility as buyers seek to secure supplies of quality malt.

Canadian Domestic Feed Market

- Domestic feed markets continue to decline as rainfall across the Prairies has improved confidence in the 2026/27 crop.

- Increased moisture and cooler temperatures have also created a "feed grain" mindset, as more off-spec malt barley and wheat could move into feed channels, increasing overall feed grain supplies.

- Expectations of larger feed grain supplies have led to lower bids, with some buyers stepping back from the market as they wait for additional clarity.

- Declines in corn and wheat futures have created opportunities for lower-cost feed alternatives, making barley the least competitive ingredient in feed rations. Corn currently remains the cheapest component, which is expected to continue pressuring barley values.

- New crop interest remains limited as early crop conditions appear favorable. Barley values could see an additional 50-cent decline toward last year's lows.

- Crop conditions across all commodities will remain the primary market focus moving forward.

| | |

HARD RED WINTER WHEAT

Ryan Statz, Merchant

| | |

- On June 30, the USDA released updated state-by-state winter wheat planted and harvested acreage estimates.

-

State-by-state HRW highlights:

- Kansas: 6.9 million planted acres (down 5% year over year) and 5.95 million harvested acres (down 12.5% year over year), reflecting significant abandonment.

- Oklahoma: 4.1 million planted acres (down 1% year over year) and 2.1 million harvested acres (down 25% year over year), also reflecting substantial abandonment.

- Texas: 5.5 million planted acres (unchanged year over year) and 1.6 million harvested acres (down 30% year over year), indicating considerable abandonment.

- Montana: 1.85 million planted acres (down 17% year over year) and 1.7 million harvested acres (down 20% year over year). Quality remains the biggest question mark.

- Production estimates continue to be refined as the growing season progresses. The market is already aware of the much smaller crop resulting from drought conditions across the U.S. Plains, and attention is now shifting toward the quality of the crop that will ultimately be harvested.

- The next question becomes how the balance sheet will adjust to accommodate the smaller crop.

-

Domestic demand is expected to shift, with mills potentially substituting HRW with NS or DNS wheat. Imports may also increase, as there are reports of Southern U.S. mills already sourcing wheat from Europe and South America, where values remain at a significant discount to U.S. offerings.

- While U.S. wheat still carries a premium to other world origins, spreads are narrowing and international buyers are beginning to take a closer look. The question remains how exports will adjust.

- Ongoing conflict in the Middle East continues to create volatility, particularly in energy markets.

- Transportation and freight costs continue to trend higher, both domestically and internationally. This could alter trade flows and increase pressure on interior markets.

-

Trade developments involving China continue to influence commodity markets, particularly row crops, but HRW wheat is not immune to these shifts.

- There are currently several competing forces influencing Kansas City futures, and markets appear to be lacking conviction. U.S. production is projected to reach a 30-year low, while global production is approaching record levels, creating a significant tug-of-war in price direction.

| | |

|

HARD RED SPRING WHEAT

Justin Beach,

Red Wheat Product Line Manager

| | | |

The past two weeks have been challenging from a price perspective, but today we are finally seeing futures find some relief following a significant round of data released by StatsCan and the USDA.

StatsCan surprised the market with an acreage estimate of 18.067 million acres, compared to the average trade estimate of 18.81 million acres. The primary shift was a rotation away from spring wheat and into canola.

The June 1 stocks report showed on-farm stocks down 4% from last year, while off-farm stocks increased 11% year over year. Stocks were slightly higher year over year in North Dakota and slightly lower in Montana. Overall, the report carried few major market implications.

The acreage report, however, provided more excitement. Total wheat acres were revised down 6%, with winter wheat acreage declining 5% and spring wheat acreage declining 6%. Notably, North Dakota saw a significant reduction in wheat acres, while Montana acreage increased by 200,000 acres. The increase in Montana appears to be a substitute for HRW acres.

On the export front, activity remains quiet, as most business is being booked for September forward and market attention continues to shift toward row crops. We remain competitive with Canadian values through September, but Canadian offers become considerably cheaper beginning in October.

Going forward, the market will focus on growing conditions as traders monitor crop size, yield potential, and quality prospects.

| | |

|

SOFT WHITE WHEAT

Steve Yorke, Merchant

| | | |

Futures markets have been choppy over the past few weeks, while white wheat values have gradually moved higher on continued export demand for August and September shipments and very little grower selling. This has helped push basis levels back into the 30- to 50-cent range for August and September delivery, which is welcome news for those with HTAs and accumulator contracts in place.

Fundamentally, attention remains focused on the HRW and SRW harvests, where we should see meaningful progress in the coming week as conditions dry out. As always, quality will be closely watched.

On the global front, SovEcon reduced its 2026/27 Russian wheat production estimate from 90.4 MMT to 88.9 MMT, citing a smaller planted area. While the revision is notable, it still points to a very large crop and is not a major market mover at this time. Australia also remains in the spotlight, as current indicators suggest a significantly smaller crop. Production below 20 MMT would be supportive for Pacific Northwest export demand.

Today, values are sitting in the $6.30 to $6.40 per bushel range for August and September delivery, and we expect the market to remain in a relatively tight trading range of $6.10 to $6.50. Continued reluctance from growers to sell new crop supplies, combined with active export demand, could push values above the $6.50 mark. Conversely, if growers become more aggressive sellers as harvest progresses, we could see additional downside pressure early in the season.

USDA acreage and stocks reports are due out today. Be sure to have orders in place and working to help capture cash or basis rallies as opportunities arise.

https://columbiagrain.com/producer-solutions/

|

| |

|

Joe Foley,

Product Line Manager - Corn & Soybeans

CORN

|

| | |

Corn prices remain in a downward spiral amid ample old-crop stocks and mostly benign weather forecasts across the United States. Nearly 10% of the national crop is now silking, with most production areas in relatively good shape. The latest USDA crop conditions report estimates that 67% of the crop is in good-to-excellent condition.

Fund selling has been a major factor over the past few weeks, as managed money has switched sides, liquidating long positions and moving to a net short position of approximately 70,000 contracts. Elsewhere, Brazil's winter corn harvest is approaching 25% completion, and we expect export competition to increase accordingly.

On the supportive side of the ledger, export demand remains very strong, with total U.S. commitments approaching 85 million metric tons, roughly 17 to 18 million metric tons ahead of last year's pace. The Pacific Northwest also continues to see an exceptional export program, with weekly inspections routinely reaching 500,000 to 600,000 metric tons.

In Europe, record heat is causing concern, with some analysts lowering their estimate of the EU corn crop to 50 million metric tons, compared to the USDA's most recent estimate of 57.5 million metric tons. This situation bears watching over the coming weeks, as it could increase European import requirements.

Finally, the market continues to anticipate renewed Chinese demand, potentially exceeding 10 million metric tons of U.S. corn, although that demand has yet to materialize. Weather in the United States during pollination, crop conditions in Europe, and any emergence of Chinese demand will remain key market drivers in the weeks ahead.

| | |

|

Joe Foley,

Product Line Manager -

Corn & Soybeans

SOYBEANS

| | | |

Soybean futures have come under significant pressure over the past few weeks, with fund selling serving as the primary catalyst amid generally favorable U.S. weather conditions. Nearly two-thirds of the U.S. crop is currently rated in the good-to-excellent category.

NASS released its June 30 acreage and stocks estimates today with few surprises. U.S. planted acreage is projected at 85.365 million acres, slightly above the March estimate of 84.7 million acres and well above last year's total of 81.215 million acres.

China has returned as a buyer of new-crop soybeans, although purchases have occurred at a measured pace. The latest USDA export sales report shows only 200,000 metric tons registered in China's name, though a portion of the 1.362 million metric tons currently listed as unknown sales will likely be switched to China. Sales reported as unknown destinations must ultimately be assigned to a specific country at the time of shipment through weekly export inspections.

China's return to the market is a positive development following a disappointing current crop year, during which purchases totaled less than 12 million metric tons, compared to more than 22 million metric tons a year ago. Demand will need to be monitored closely, however, as Brazil remains 20 to 30 cents per bushel cheaper than U.S.-origin soybeans for October Pacific Northwest shipment.

| | |

Flax

Sean Ferguson, Merchant

| | | |

The flax market has exhibited weakness since the last market report. StatsCan and the USDA recently released their planted acreage estimates, showing an overall increase in flaxseed acreage across North America. U.S. flax acreage was pegged at 286,000 acres, up 22% from 234,000 acres last year. Canadian flax acreage was estimated at 649,900 acres, up 5% from 620,200 acres a year ago. However, seeding delays reduced Canadian acreage from the March projection of 750,000 acres.

The trade will now wait to see what harvested acreage ultimately looks like, as rains across the Canadian Prairies have contributed to an increase in abandoned and drowned-out acres. Carryover stocks heading into the upcoming crop year are expected to be larger year over year, which will likely continue to weigh on prices moving forward. One of the biggest wildcards remains the Black Sea crop. Current reports suggest another record harvest is possible, provided growing conditions remain favorable.

| | |

The StatsCan acreage report pegged Canadian planted canola acreage at a record 23.4 million acres, an increase of 8.4% from last year. In the United States, the USDA estimated planted acreage at 2.92 million acres, representing a 27% increase year over year.

By state, planted acreage is estimated at 93,000 acres in Idaho, up 16% year over year; 171,000 acres in Washington, up 16%; 165,000 acres in Montana, up 12%; and 2.33 million acres in North Dakota, up 29%.

A similar story is unfolding across the Canadian Prairies as we are seeing in flax. Abandoned acreage has increased, and droughted-out acres are being widely discussed throughout the industry. The market will be watching closely to determine whether record planted acreage ultimately translates into a record Canadian canola crop.

Vegetable oil markets continue to trend lower as energy markets weigh on biofuel demand. The market is assigning a higher probability to a resolution with Iran and increased certainty surrounding energy shipments through the Strait of Hormuz. At the same time, imports of alternative biofuel feedstocks have increased, adding pressure to soy oil values.

Crush margins remain strong compared to historical levels, although they have declined significantly from the highs reached in May. Old-crop demand remains supportive for any available capacity at North American crush facilities.

The CAD/USD exchange rate continues to trend lower as weaker energy markets pressure the Canadian dollar. Meanwhile, the U.S. dollar has remained firm as investors seek the relative safety of the currency amid ongoing geopolitical uncertainty.

| | |

U.S. lentil acreage is estimated to be down 30% this year; however, stocks-to-use ratios are reported between 90% and 120%, depending on the data source. In practical terms, this means that even if the U.S. did not produce a lentil crop in 2026, carryover stocks from 2025 would be sufficient to meet global demand for the next twelve months.

The 2026 crop is progressing well so far, and Canadian supply-and-demand projections, along with crop conditions, are similar to those in the United States. As a result, we expect there to be very little excitement in green lentil pricing during the 2026/27 crop year. We continue to monitor monsoon activity in India to determine whether rainfall becomes more deficient than normal, but even under a poor rainfall scenario, demand potential appears insufficient to absorb existing excess stocks.

| |

Over the past 30 days, yellow pea prices strengthened as domestic buyers sought nearby coverage. However, with much of that demand now satisfied and crop prospects looking favorable in both the United States and Canada, the market has softened once again.

Given the size of the anticipated crop, it appears the U.S. will eventually need to be competitive in export markets to work through excess supplies. To achieve this, prices may need to decline by nearly another dollar per bushel.

Green pea activity has remained relatively slow, although some lots of high-quality product have traded at stronger values to satisfy split pea tender demand. Be sure the procurement team knows what inventory you have on farm and the prices you are targeting so we can reach out when these opportunities arise.

Looking ahead to the new crop, we expect green pea prices to remain under pressure. Striker varieties moving into Southeast Asia are currently trading at values below pet food markets due to abundant global supplies. Hampton and, to some extent, Arcadia varieties may continue to command premiums for exceptional quality, as those markets are somewhat tighter, but they remain influenced by the broader weakness in the overall pea market complex.

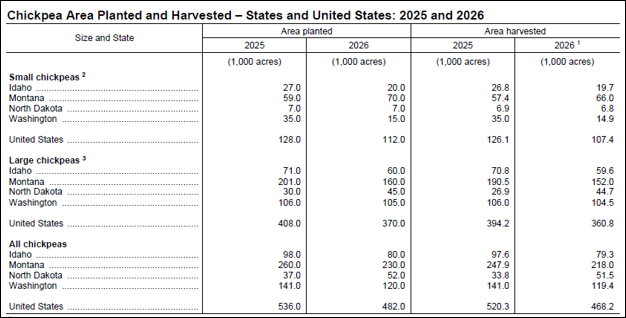

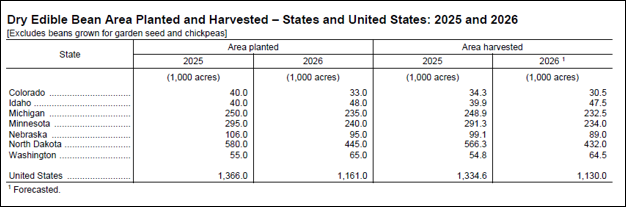

| USDA June Acreage reported Chickpea acres are down 10% Year-on-Year with Montana being the largest outright reduction and Idaho + Washington being the largest % reduction Year-on-Year. The USDA Stocks report showed a 40% YoY stocks gain with majority being off-farm. | | USDA June Acreage reported US Dry Bean acres down 15% Year-on-Year. North Dakota was down 23% Year-on-Year and accounted for the largest outright acreage reduction. This is more/less in line with market estimates. The USDA does not classify acres by variety so it’s up for the market’s interpretation. Regardless, this is one of the smallest Dry Bean acreage bases in the last decade+. | | |

Matt Schorn

The most recent USDA Acreage and Stocks reports added a key update to the balance sheet outlook. While acreage adjustments were generally not dramatic across the major crops, the market is now working with clearer supply-side confirmation heading into the critical summer weather window.

On the weather front, conditions since mid-June have shifted meaningfully toward a wetter and cooler pattern across much of the U.S. Corn Belt and Northern Plains. Above-normal precipitation and below-normal temperatures have slowed crop development in several regions. While moisture has generally supported yield potential where drought stress was building earlier in the season, the cooler pattern has tempered growth rates. Market is looking for July heat to see the crops realize their potential. Spring wheat markets have proven somewhat more resilient due to ongoing concerns regarding conditions in portions of the Northern Plains and the Canadian Prairies however, improved precipitation forecasts have contributed to the broader weakness across wheat markets.

In the wheat complex, Hard Red Winter (HRW) harvest is now well underway across the Southern Plains. Early yield reports remain mixed to disappointing and crop conditions continue to reflect lingering stress from earlier drought impacts. Protein levels and test weights are being closely watched as harvest progresses, with quality variability expected to remain a key theme.

In the current environment, risk management remains critical. Good-till-Cancelled (GTC) Orders can be an effective tool for capturing brief weather-driven rallies that often occur during the summer growing season. For producers who believe futures values may recover later in the season but want to secure attractive local cash opportunities today, Basis Contracts remain a valuable tool when futures levels remain unattractive.

The additional risk-management options listed below can help producers manage volatility, stay disciplined, and take advantage of opportunities when the market presents them.

Columbia Producer Solutions Tools:

- Good-till-Cancelled (GTC)

- Basis Contracts

- Accumulator Contracts

- Cash +

- Average Price Contracts

-

Ratchet Order

- Collar Orders

Reach out to your local buyers and managers to review these options, or others, on our Columbia Producer Solutions platform of marketing tools.

| | |

INTERNATIONAL BUSINESS

Yuya Takano and Wiley Wang

International Merchants

| | |

CORN

Global corn market has been at a switching phase these weeks, from heavily traded PNW corn to South American corn, to Asian destinations. This could last for a couple of months, then it should switch back to PNW corn once we get our harvesting going.

This is heavily influenced by the highly anticipated PNW soy export program for new crop, and we need to see continued new crop sales to China.

The Asian corn export market has now covered most needs through September shipments, so that period is largely done. For Japan, Korea, and Southeast Asia, most nearby–September demand has been covered from the PNW. The main exception is Korea, which also bought about two cargoes from Argentina in its tenders.

For October shipments, most Asian buyers are still on the sidelines. On the PNW side, exporters are being careful with new crop corn origination, and many elevators plan to reserve capacity for expected new crop soybean exports to China. Because of this, there are not many October corn offers out of the PNW at the moment.

In Brazil, weaker Chicago futures and a stronger real have slowed farmer selling. This has pushed inland prices higher and kept FOB premiums firm. Even so, for October shipment into Asia, Brazil is still expected to be the main origin, with some demand shifting away from the PNW toward Brazilian corn.

SOYBEANS

U.S. new‑crop soybean sales to China have finally started to appear, but the volumes are still small. It does not yet look like a full, demand‑driven import program. These sales look more like politically motivated purchases than aggressive buying based on crush margins.

That said, several new‑crop soybean cargoes have already been sold out of the PNW, and October export capacity is now filling up. On top of the existing bookings, the trade still expects more Chinese buying, so for the autumn period PNW logistics are increasingly being set up with soybeans as the priority.

However, the price gap versus Brazil remains a major obstacle. Even for October positions, U.S. soybeans are still about 25–50 cents per bushel more expensive than Brazilian beans. On a pure commercial basis, Brazil is still the cheaper and preferred origin. As a result, PNW soybean exports will depend heavily on how much of the “political” U.S.–China commitments actually turn into real, physical purchases. The pace and timing of Chinese buying will be the key driver from here.

WHEAT

Most European areas are experiencing high heat this week and might have an impact on the final yield. Their crop had received higher than normal precipitation in the growing season, so the crops should only result in some minor losses. The high heat would promote some higher protein and create ideal harvesting conditions.

Australia received nice rains across most of their growing regions, and crops are doing very well. Meanwhile, the local weather forecasting authorities continue to issue warnings for a serve drought for later months, which has made farmers less active to sell. This would be the biggest potential weather market to watch for the next months.

North American spring wheat regions all got rains, especially Canadian Prairies. Part of the Prairies are actually a touch too wet.

Market saw several feed wheat cargoes traded into South Korea from possibly EU origins. These tons directly replaced some of PNW feed wheat volumes.

| | | | |