|

1Q 2026 Helicopter Market Update and Pricing Review Summary

Prepared by HeliValue$, Inc.

Jason Kmiecik, ASA – President

On April 30, 2026, HeliValue$ held its Q1 2026 Pricing Review Meeting, where our analysts conducted a detailed, model-by-model review of every helicopter listed in The Official Helicopter Blue Book®. The goal was to evaluate current resale values and market performance against recent global transactions and market data. This quarterly assessment provides a comprehensive view of ongoing trends in helicopter resale pricing, supply, and transaction activity across all major weight classes and configurations.

Key Market Insights

Overall Market Performance:

During the first quarter of 2026, the global helicopter resale market continued to lose momentum following the strong post-pandemic recovery that characterized much of 2023 through 2025. Market participants reported a noticeable decline in buyer activity, longer decision-making cycles, and fewer completed transactions across most helicopter categories. While demand remains present, buyers have become increasingly selective, focusing on aircraft with strong maintenance histories, modern avionics, and immediate availability.

Several factors have contributed to this slowdown. Ongoing geopolitical uncertainty, including escalating tensions and military conflict involving Iran, has increased volatility in global energy and financial markets. This uncertainty has led some operators and private buyers to delay major capital expenditures, including aircraft acquisitions. In addition, a limited selection of high-quality aircraft available for sale has reduced buyers' opportunities, further suppressing transaction volume.

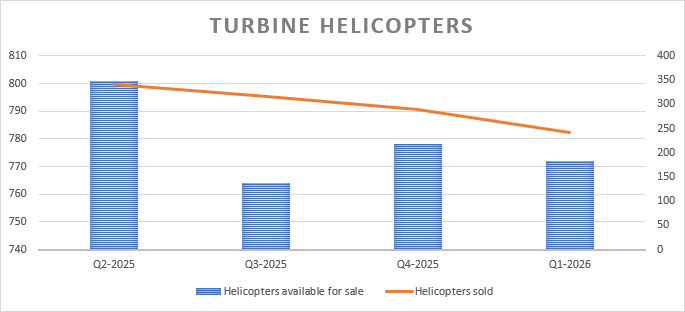

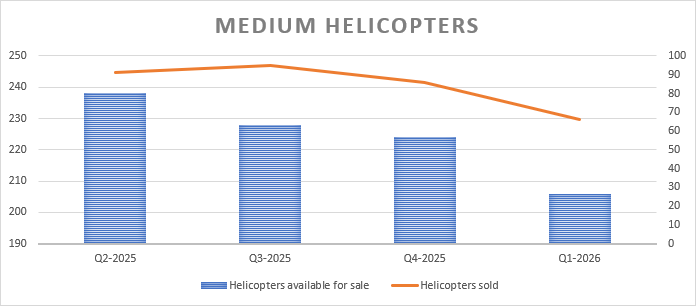

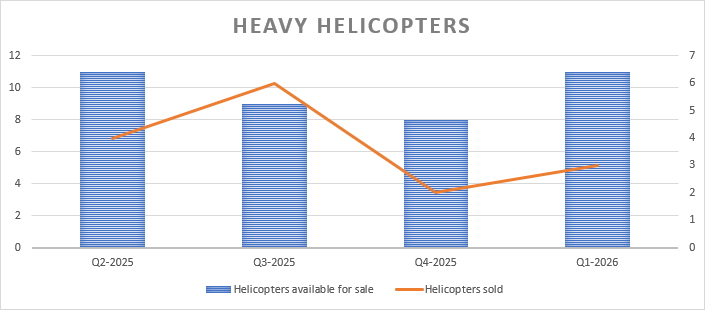

Market performance has varied significantly by segment. Light twin-engine and heavy helicopter categories have remained relatively resilient, supported by demand from emergency medical services (EMS), offshore energy operations, utility work, government agencies, and specialized commercial operators. In contrast, single-engine turbine helicopters and certain corporate transport models have experienced softer demand and fewer completed transactions.

Supply trends also differed between aircraft classes. The inventory of turbine-powered helicopters continued to tighten as owners held onto existing assets and fewer aircraft entered the resale market. Meanwhile, piston helicopter inventory increased, reflecting weaker demand in the training, recreational, and entry-level ownership segments.

Pricing remained mixed. Of the nine helicopter models tracked that experienced meaningful valuation changes during the quarter, five recorded value increases while four recorded value declines. This reflects a market that remains highly segmented, where desirable, low-time aircraft continue to command premium pricing while older or less sought-after models face increased pricing pressure.

Supply and Transaction Volume:

One of the most notable developments during the first quarter of 2026 was the continued decline in both available inventory and completed sales transactions. Although the supply of many turbine helicopter models fell further during the quarter, transaction activity slowed as well, indicating that reduced inventory alone is not driving market performance.

Compared with the same period in 2025, overall helicopter inventory declined by nearly 18%, leaving prospective buyers with significantly fewer aircraft to choose from. The reduction in supply has been particularly pronounced among late-model turbine helicopters, where many owners have elected to retain aircraft due to high replacement costs, lengthy factory delivery schedules, and uncertainty regarding future market conditions.

Despite the tighter supply environment, transaction volume has not increased as might typically be expected. Instead, many buyers have adopted a more cautious approach, influenced by elevated financing costs, economic uncertainty, and concerns regarding global geopolitical developments. As a result, aircraft are generally spending more time in the evaluation phase before sales are completed, even though quality inventory remains limited.

The combination of declining inventory and slower sales activity suggests the market is entering a period of reduced liquidity. Buyers continue to face challenges in finding suitable aircraft, while sellers are encountering a smaller pool of active purchasers. This dynamic has created a market characterized by low inventory, modest transaction volume, and generally stable pricing, particularly for desirable turbine aircraft.

Looking ahead, industry participants will be closely watching interest rate trends, geopolitical developments, and manufacturer production schedules to determine whether transaction activity rebounds during the remainder of 2026. Until greater economic certainty emerges, most analysts expect the resale helicopter market to remain cautious, with selective demand supporting values for premium aircraft while overall transaction volume remains below recent historical averages.

Please note that all Q1 2026 figures shown in the accompanying charts are preliminary and subject to revision as additional verified transaction data is received and processed in the coming months. Chart data provided by JETNET Marketplace.

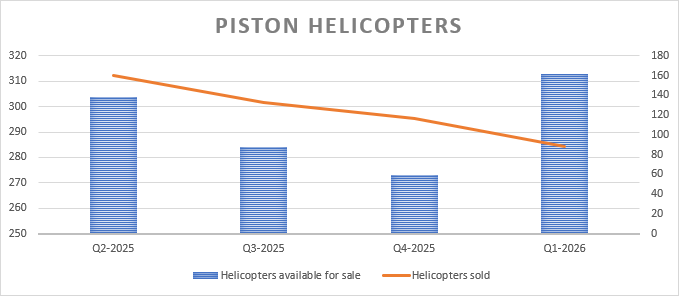

Piston Helicopters

Market Overview

The piston helicopter market remained relatively healthy through much of 2025 and into the early stages of 2026, supported by steady demand from private owners, flight training organizations, and recreational operators. However, market conditions shifted noticeably during the most recent quarter. Transaction activity slowed considerably, and the number of helicopters being offered for sale continued to increase, resulting in market dynamics that are beginning to favor buyers rather than sellers.

The combination of rising inventory and declining sales volume has created a more competitive environment among sellers. Buyers now have more aircraft to choose from, allowing them to be more selective and negotiate more aggressively on pricing and terms. This marks a significant change from the tighter market conditions experienced over the past several years, when limited inventory often resulted in quicker sales and stronger pricing.

Robinson Helicopters Driving Inventory Growth

A major contributor to the increase in available inventory has been the Robinson fleet. Over the past 12 months, the number of Robinson helicopters listed for sale has increased by approximately 11%, accounting for much of the overall growth in piston helicopter supply.

This trend carries significant weight because Robinson helicopters dominate the piston helicopter market, representing an estimated 85% to 90% of the world's active piston helicopter fleet. As a result, changes in Robinson inventory levels often serve as a reliable indicator of broader market conditions.

The increase in Robinson aircraft being offered for sale may be attributed to several factors, including owners upgrading to turbine aircraft, rising operating and maintenance costs, changing economic conditions, and some operators choosing to reduce fleet size. Regardless of the underlying reason, the growing supply of Robinson helicopters has increased competition among sellers and provided buyers with more purchasing options than they have had in recent years.

Growing Divide Between Premium and Higher-Time Aircraft

The market is becoming increasingly segmented based on aircraft condition, maintenance status, and remaining component life. Low-time, well-maintained helicopters with complete maintenance records continue to attract strong buyer interest and generally sell more quickly than the broader market. Aircraft that have recently undergone major maintenance events or possess significant remaining engine and component life are particularly desirable.

In contrast, higher-time helicopters and aircraft approaching major maintenance milestones are facing increasing pricing pressure. Buyers are placing greater emphasis on future ownership costs and are becoming more cautious about acquiring helicopters that will require substantial maintenance investments shortly after purchase.

One of the most significant factors affecting values is the increasing number of helicopters approaching engine overhaul intervals. The market has experienced a steady rise in listings for aircraft that are either nearing overhaul requirements or already due for overhaul. As engine overhaul costs continue to rise due to inflation, labor shortages, parts availability challenges, and higher manufacturing costs, many owners are choosing to sell their helicopters rather than invest in expensive overhauls.

Consequently, buyers are often discounting these aircraft more heavily to account for anticipated maintenance expenses. The gap in market value between a helicopter with substantial remaining engine life and an otherwise identical helicopter nearing overhaul has widened noticeably over the past year.

Market Outlook

Looking ahead, current trends suggest that the piston helicopter market will continue moving toward a buyer-friendly environment throughout the remainder of 2026. Inventory levels are expected to remain elevated, particularly among Robinson models, while transaction activity may remain subdued unless financing conditions improve or economic uncertainty diminishes.

Aircraft with low operating time, strong maintenance histories, modern avionics, and significant remaining engine life should continue to perform well and retain value. However, sellers of higher-time aircraft or helicopters approaching major maintenance events may need to adjust pricing expectations as buyers become increasingly focused on long-term operating costs.

Overall, the piston helicopter market appears to be entering a period of greater balance after several years of seller-favored conditions. Buyers are benefiting from increased selection, improved negotiating leverage, and more opportunities to identify value within the marketplace, while sellers are finding that aircraft condition, maintenance status, and remaining engine life are playing an increasingly important role in determining marketability and value.

|