|

First off, my heart goes out to those of you who lost their homes or had to be evacuated. We were without electricity for a couple days but suffered no real difficulties due to the fire. With memories of the 2014 Colby Fire, just a couple blocks north of us, firmly etched in my memory, we kept a close eye on the news reports. Here’s to hoping the worst is over.

Let’s jump into what’s going on, what we’re planning to do and a brief personal note.

Stocks

For starters, let’s discuss where the market’s valuation is now. (Spoiler alert, it’s high. Really high.) Let’s look at a few – six, to be precise - measures of the market’s current valuation:

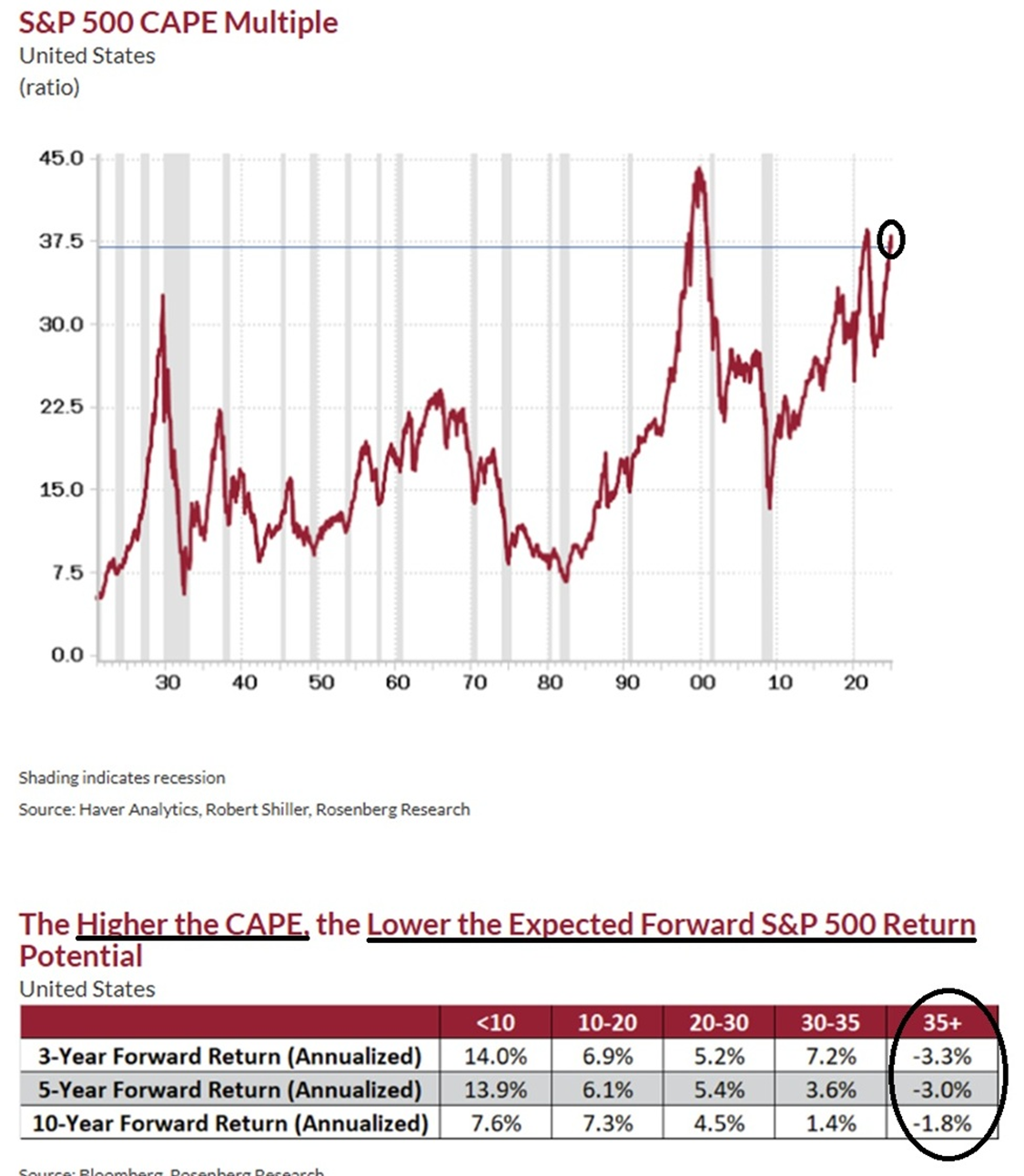

(1) The CAPE (Cyclically Adjusted Price Earnings) Ratio is currently sitting at right around 37. That’s high.

| |

|

A 37 CAPE is high enough to indicate the average annual expected return for the S&P 500 for the next 3-, 5- and 10-year periods is negative.

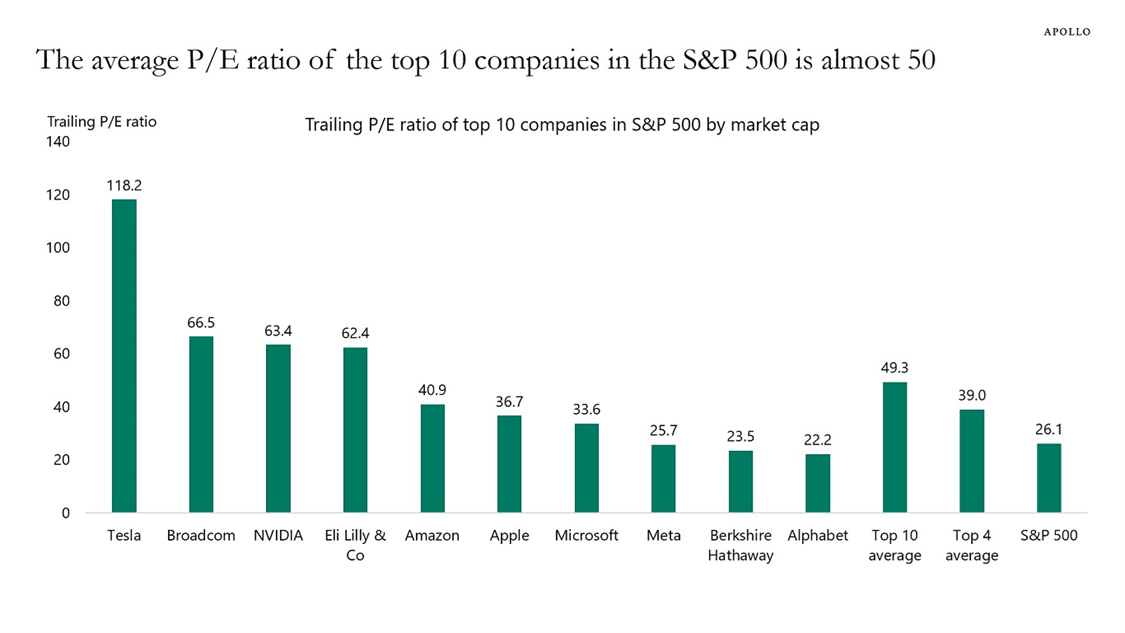

(2) The P/E Ratio for the 10 largest companies of the S&P 500 is just under 50. That’s high.

| |

(3) The Price to Book Ratio for the S&P 500 has never been higher. Ever. | |

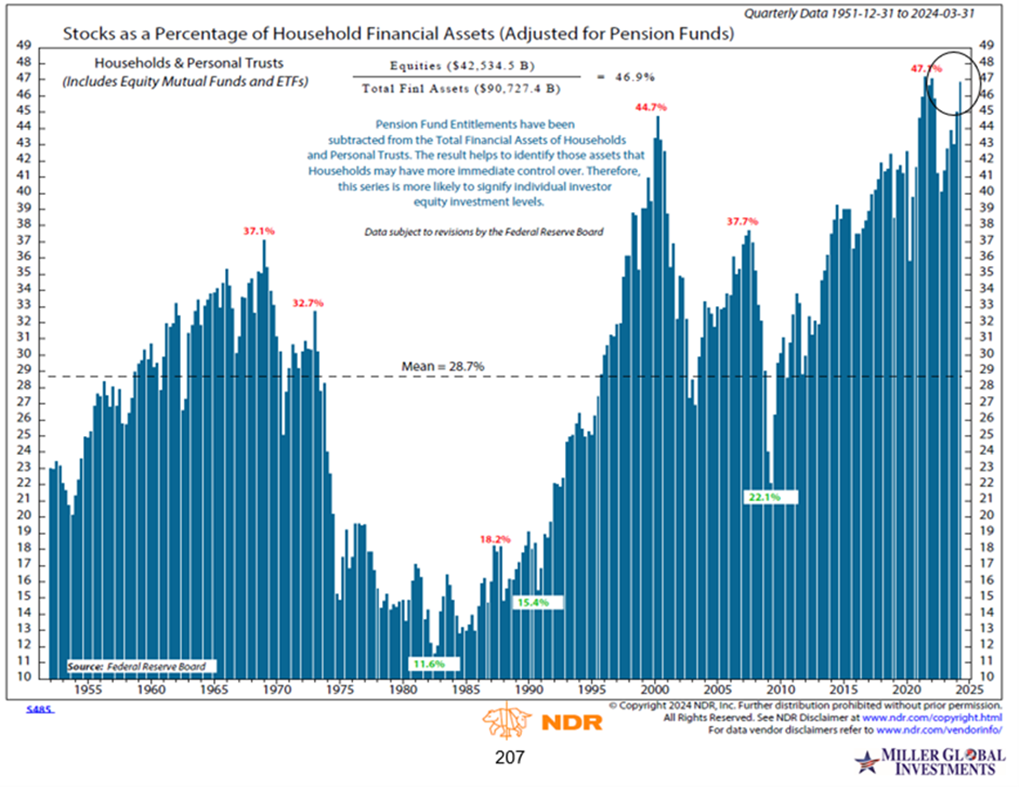

(4) Stocks as a percentage of household assets are at an all-time high. | |

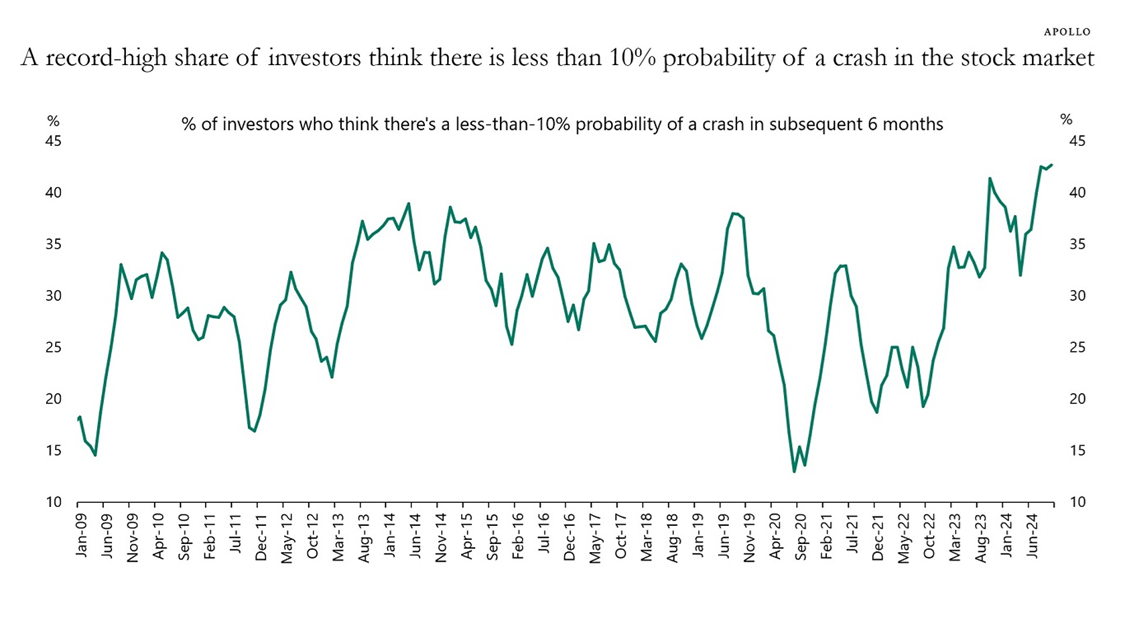

(5) Investor sentiment is very high. Traditionally, investor sentiment is a strong contrary indicator of the market's next move. | |

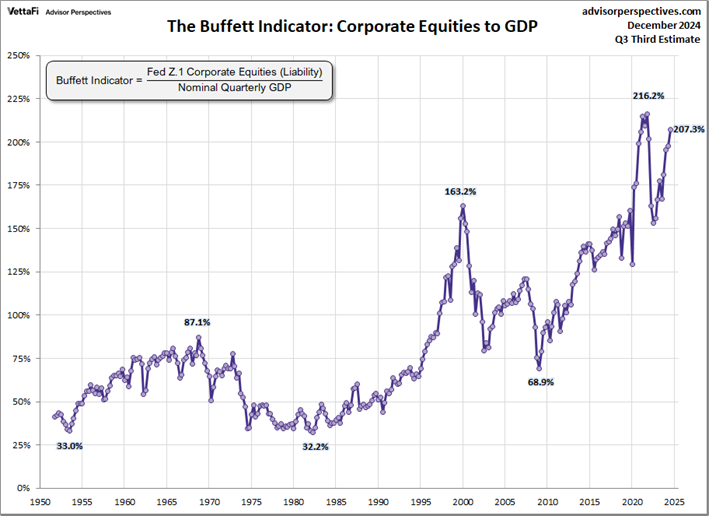

(6) And last, but not least, the Buffett Indicator, which he discussed in detail in a 2001 issue of Fortune magazine (You can access the article here), compares the value of stocks to US GDP (Gross Domestic Product). The current ratio of 207.3% is really high. | |

|

Quoting Buffett from that 2001 article, “The message from the chart is this: If the percentage relationship falls to the 70% or 80% area, buying stocks is likely to work very well for you. If the ratio approaches 200% - as it did in 1999 and part of 2000 – you are playing with fire.”

With that ratio now above 200%, the all too real concept of playing with fire really hits home.

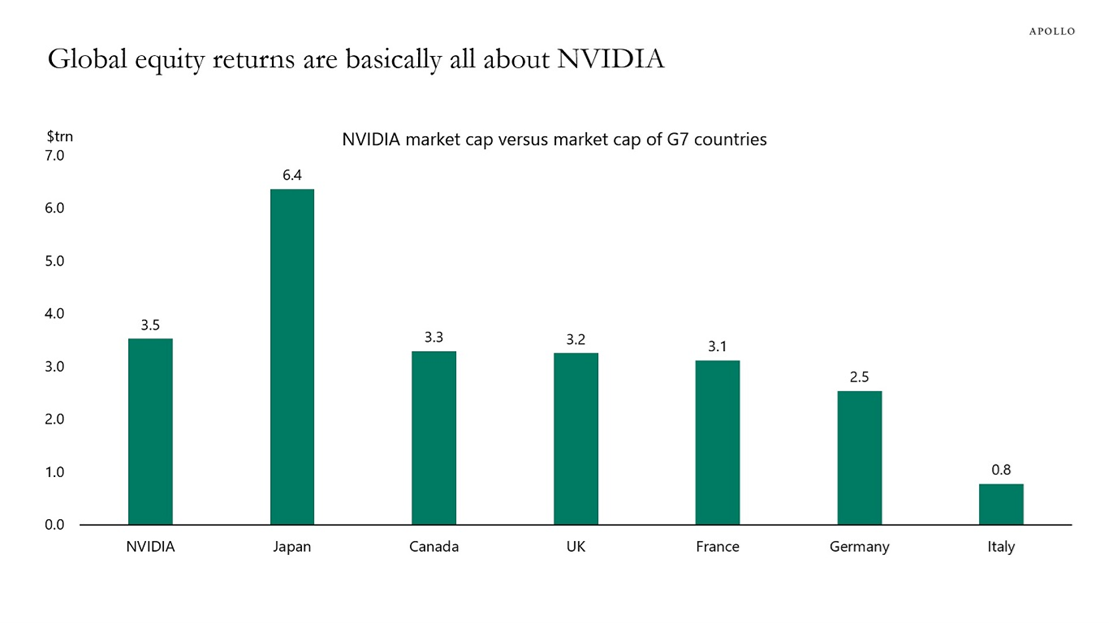

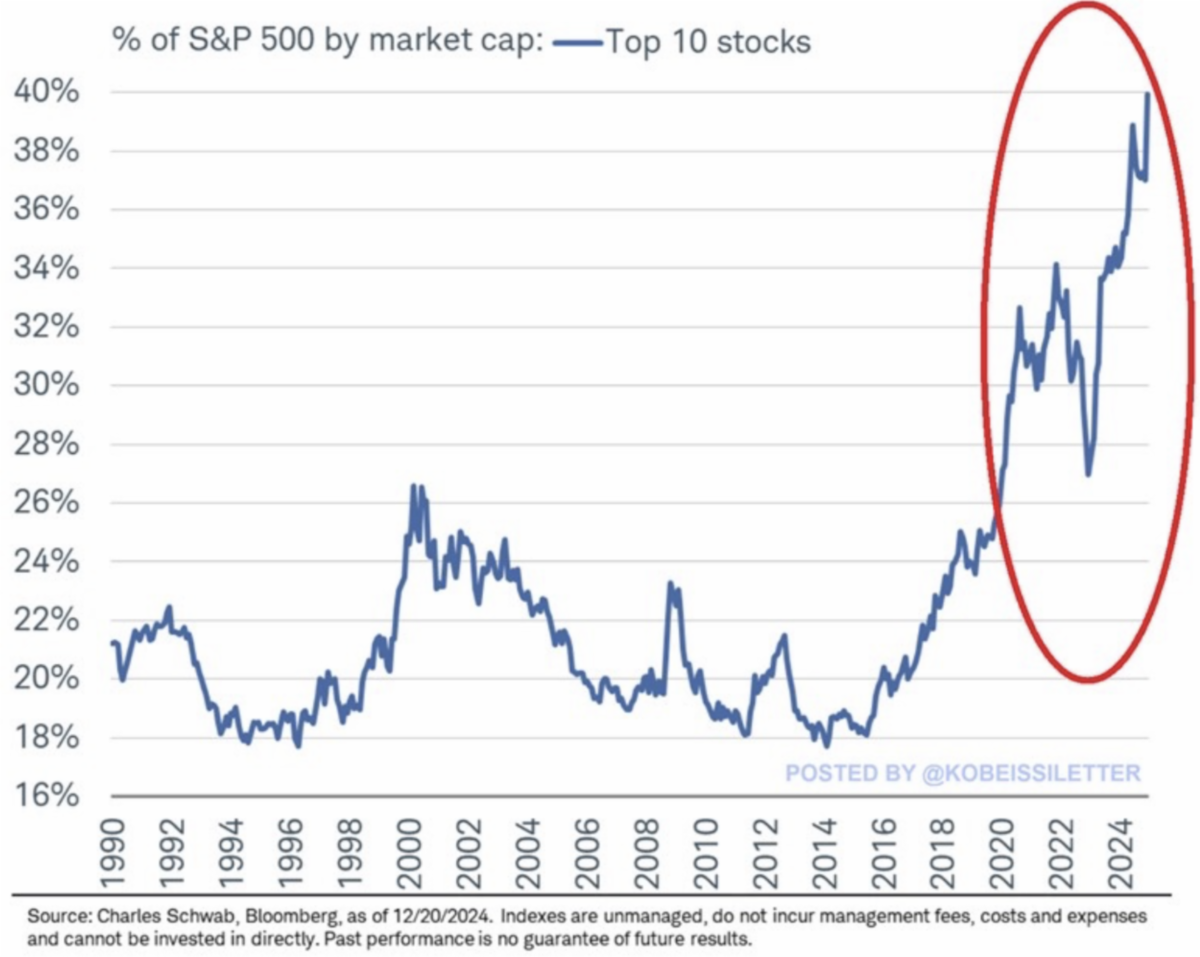

So, why the sky-high valuations? As I’ve mentioned a few times, the 10 largest tech stocks now make up over 1/3 of the S&P 500’s value. Nvidia itself is worth more than the entire Canadian stock market. In fact, it’s worth more than each of the G7 nations apart from Japan:

| |

|

And for those of you disappointed that one US company isn’t bigger than Japan’s market capitalization, rest easy. All we need to do is add Apple (or Microsoft to Nvidia) to get a bigger market cap than Japan.

Of course, the engine driving these valuations is Artificial Intelligence. Nvidia, Apple, Microsoft, Amazon and others are trading at valuations I haven’t seen since 1999-2000 run up in tech stocks. And we know how that ended. My biggest concern with the AI driven stocks is that AI has yet to do anything close to what many folks expect AI to do. Rather than torture you with more graphs about ridiculous valuations, please do yourself a favor and read any (or all!) of the following articles by Gary Smith and/or Jeffrey Funk. They’re written in user-friendly prose and pose practical questions of logic and math to various AI programs.

Inflation

Inflation is definitely not under control yet. The market has told the Fed, very decisively, that reducing rates isn't working.

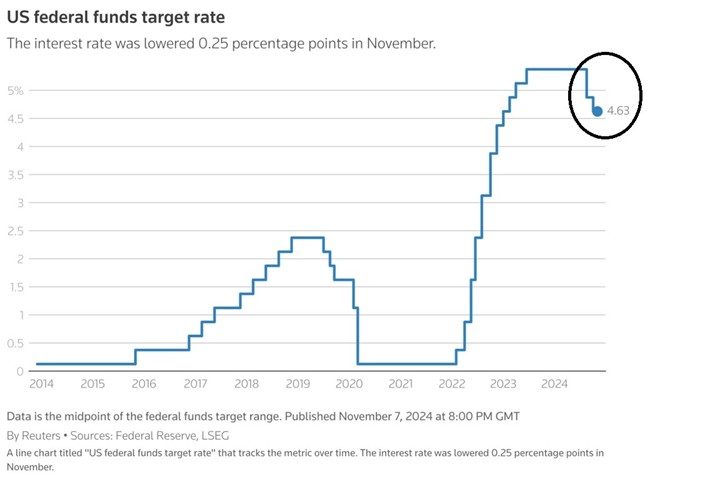

Since September, the Fed has cut rates 100 bps (100 basis points or 1%):

| |

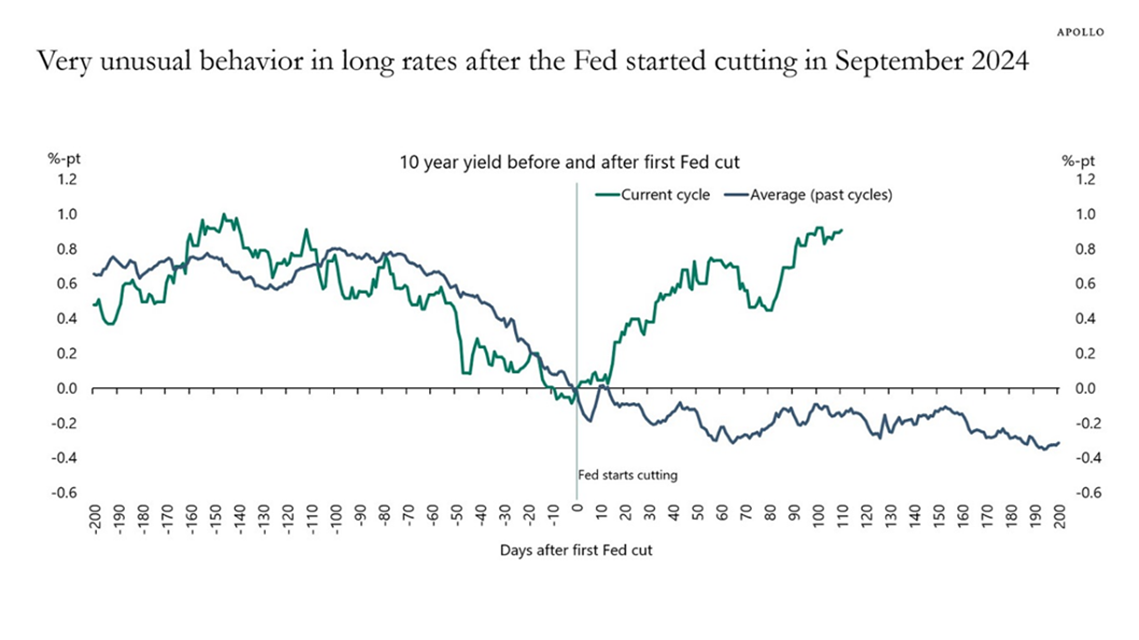

But since then, the 10-year Treasury Bond has risen 1%. The exact opposite of the Fed's intention: | |

|

While the Fed has a great deal of influence on short-term rates, longer-term bonds, like the above-mentioned 10-year treasury, are entirely driven by market forces. In this case the bond market is stating the fed, in lowering rates, has gotten it wrong. Rates seem to be headed higher for longer.

To compound the inflation problem, we’re heading into a new administration with several policies that’ll add to the inflationary backdrop. Let’s discuss three of them.

- Tariffs. During his first term, Trump imposed tariffs on Chinese goods between 7.5% to 25%. This time around the proposed rate is as high as 60%. As happened in his first term, these new tariffs, which will also extend to Canada, Mexico and other countries, will result in higher prices being passed on to American consumers and companies. Additionally, our trading partners may impose retaliatory tariffs in goods they import from the U.S. thus increasing the inflationary effect.

- Immigration. The planned deportation of millions of workers will probably create a labor shortage. The food processing, agricultural, hospitality and construction industries are all liable to see either reduced output and/or higher labor costs. This may well result in lower or non-existent profit margins, reduced output and higher prices for consumers.

- Tax cuts. The Trump Administration passed the 2017 Tax Cuts and Jobs Act and many of the provisions of that Act are set to expire in 2025. Assuming these tax cuts are extended or renewed, the resulting increased disposable income will, unsurprisingly, tend to be inflationary.

*Please note none of these observations are meant to be political in nature. My only aim is to find investment opportunities that offer decent returns with acceptable levels of risk. Here ends the disclaimer.

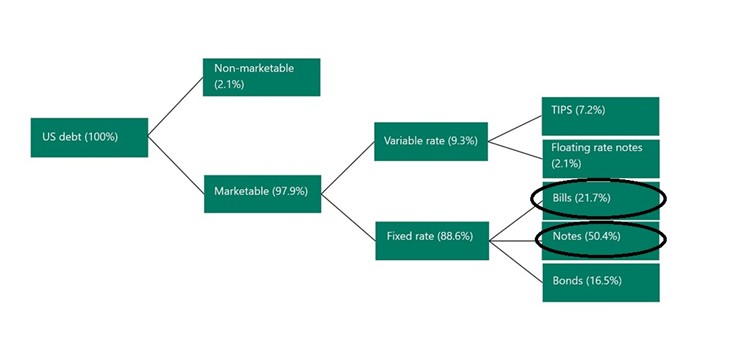

One last bit about inflation. With just over $36 trillion in debt, interest expense is now a bigger budget item than the defense budget. For the last couple years, T-Bills (debt that has 1 year or less from the time they’re issued) have been paying over 4% interest. They make up just over 21% of government debt. The more concerning issue to me is the government’s T-Notes, with maturities ranging from 2-10 years. As previously issued T-Notes - sporting interest payments under 1% - come due, they will be refinanced with interest rates higher than 4% or maybe 5%. That’s going to add substantially to interest expense as T-Notes currently make up 50% of all government debt.

| |

|

What now?

Well, with the market, as measured by the S&P 500, priced so high, we will continue to take money off the table, especially in some of our more expensive names. We believe much more attractive entry points await. There are several that I like at current prices, but I am pretty sure we’ll have the opportunity in 2025 to buy them cheaper. Please give me a call or send me an e-mail if you’d like to discuss any of them or this strategy.

I know we’ve missed out on a good portion of the market’s 2024 move. The fact is most investors aren’t doing that well unless they own that small handful of stocks that have made a huge run up in the AI fueled hysteria that currently grips the market. In fact, the concentration of the S&P 500 has never been greater:

| |

|

For 2025, we’ll try and stick to Charlie Munger’s philosophy, “extreme patience followed by extreme decisiveness.” This seems to be a year where that will pay off handsomely.

One Last Thing

The last part of 2024 was rough. My November included a couple bouts with food poisioning/flu - I'm still not sure which. Then January began with wildfires that destroyed the houses of many friends and a couple clients.

But the worst part was in betweeen those two events. My 90 year-old father, who had been in declining health for the last year, fell and broke a hip on December 6th. He wasn't able to overcome the complications and passed away on December 22nd.

He was a great father, grandfather, great grandfather and husband. His ability to twist the English language into never before heard - yet often understandable – phrases was unmatched. He had a tremendous work ethic and, eventhough he was fairly tone deaf, a boundless love for music. We were blessed to have him live 13 years after my mother passed which is substantially longer than any of us expected.

| |

|

So, 2024 didn't end in a great way but we're determined to make 2025 great year. We have someone joining the McClure Investment Management team that I'm very excited about. It'll definitely free up time for more client meetings and communications (like this one) but will also bring some fresh insight to the operation. More about that in the months ahead.

But for now, I'd like to thank you for your faith in me and our ability to navigate a challenging investment landscape. We're looking forward to a challenging - and rewarding - 2025.

Bob McClure

| | | | |