There’s a lot going on. Let’s get to it. | | |

Tariffs and BS at the BLS?

On Friday, August 1st, many of the long-awaited tariffs went into effect, ending four months of the tariff on, tariff off discussion. The market quickly dropped as the combination of tariffs and weak economic data proved a bit much for the perma-bulls to handle. Let’s take a minute to sort out some of these events and then look at our recent portfolio positioning.

Tariffs

After announcing “Liberation Day” on April 2nd, the Trump Administration started off with an (almost) universal tariff of 10% on goods from outside the US. This was followed by a an interesting bit of mathematical gymnastics that tied tariff rates to trade deficits on a country-by-country basis. In theory, these “reciprocal” tariffs were supposed to reflect the trade barriers imposed by other countries on the US. In reality, the tariff schedule imposed tariffs – even on countries with whom we had a trade surplus – in a seemingly random way.

Of course, there are countries that have repeatedly broken trade deals with the US that need to be dealt with firmly yet cautiously. It’s true that China, for example, is a serial violator of trade policy with the US. But it’s also true that the size of China’s contribution to the revenue of S&P 500 companies is FOUR TIMES the size of their trade deficit.

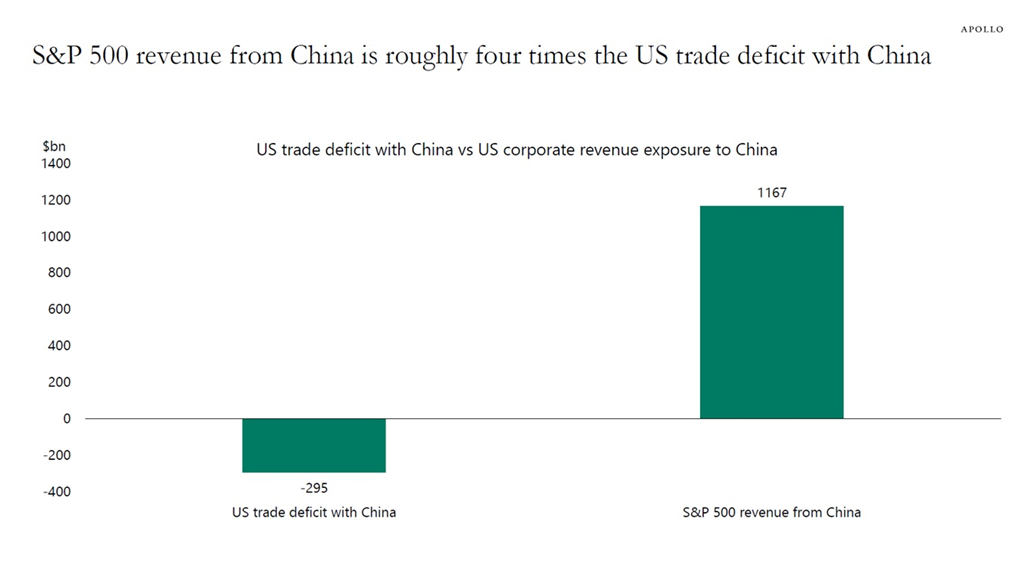

| | |

This is clearly a trade relationship that needs some degree of nuance. Yes, we – the US – would benefit by bringing more manufacturing jobs and infrastructure back to the US. Both will require a concerted effort, one that is likely to span more than one presidential administration. In starting this process, I feel we would be much better off starting with, as stated by Peter Boockvar, “a scalpel rather than a sledgehammer.”

While tariffs make the job of calculating present and future values of various assets, like stocks and bonds, more difficult, it’ll become less difficult once (if?) a stable set of criteria is set.

Economic Data

In an effort to make markets more confusing than they already are, some of the critical economic data regarding recent months’ labor and employment have been revised drastically lower. The Federal Reserve Bank (The Fed) has been under extreme pressure from the White House to lower interest rates. The Fed, relying heavily on data from the Bureau of Labor Statistics (BLS), has steadfastly refused citing ongoing signs of inflation and economic strength. And so far, they have gotten results by sticking to their guns. Although painful to some, the Fed’s hike in rates has slowed inflation by almost every measure, moving us closer to their 2% inflation target:

| | |

On Thursday last week, the Fed decided to hold rates steady rather than cut. Then Friday, the same day as tariffs became official policy for most US trading partners, the BLS announced revisions that greatly reduced jobs created and total employment while simultaneously raising unemployment.

All of that is, of course, bad. Had the weakness in the labor market been revealed a bit sooner, the Fed would probably have responded with a 25-basis point (0.25%) cut to the Fed Funds Rate. These revisions, while some are calling them “fraudulent” and “politically motivated” are most certainly the result of much more pedestrian causes: (1) declining participation in BLS surveys and (2) substantial reduction in BLS employees. Reuters had a great article outlining concerns at the BLS about a week before the latest round of data revisions. You can read it here.

Regardless of the exact causes of the data revisions, Trump fired the BLS chief and will appoint a replacement soon. Some cheer this decisive action, some are lamenting the possible loss of independence of the BLS – as well as the Fed – from the presidency. For now, we will have to wait and see.

What we do know is since Friday’s revelations, the odds of the Fed cutting rates 25-basis points at its September meeting have soared from 38% to 81%, according to CME Group.

Dollar Decline

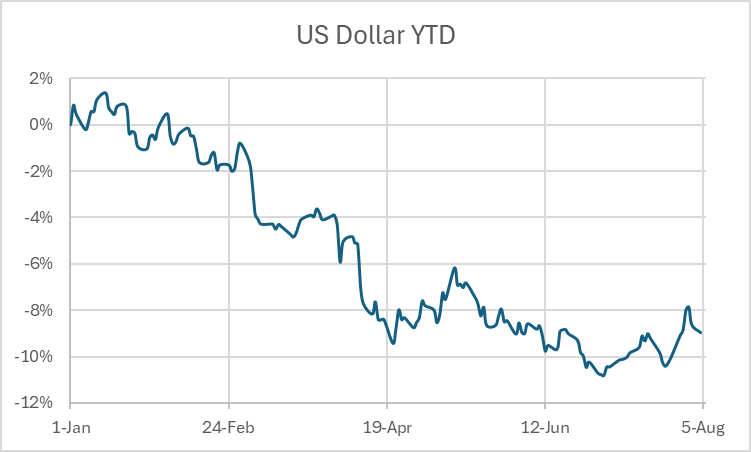

The US Dollar started 2025 on a horrible track, notching six consecutive monthly declines and falling a cumulative 10.6%, its worst half year since 1973. After a modest improvement in July, the dollar sits 8.9% lower than it started the year.

| | |

A weaker dollar makes foreign goods more expensive for US buyers which, when combined with tariffs, will tend to drive foreign trade away from the US. This can be a benefit for US manufacturers selling to US consumers. But it can also do economic harm to US manufacturers who sell to US consumers but rely on foreign raw materials and/or intermediate goods. It isn’t a one-size-fits-all, black and white type of issue. To steal again from Peter Boockvar, our trade policies need a “scalpel, not a sledgehammer.” The extent these policies will ultimately spur long-term economic growth or stagnation remains to be seen.

Portfolio Repositioning

Equity markets like nothing better, at least in the short run, than a Fed rate cut. Lower rates can make borrowing cheaper and profits greater. But often lost in the euphoria of a rate cut is the why of a rate cut. Sure, a FEMA agent giving your kid a teddy bear is nice…but it might also signify that your house burned down. A tax refund is a nice thing but also signifies you gave the government an interest free loan. And, of course, a Fed rate cut signifies the economy needs help to fend off a recession. Assuming a Fed rate cut is on the horizon, we don’t necessarily want to buy into euphoria or gloom and doom. We do, however, need to acknowledge the likelihood of economic uncertainty.

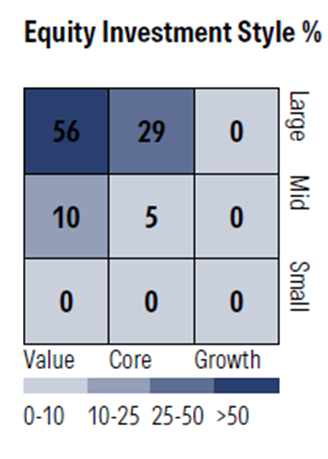

We have had our holdings drift to the upper left quadrant of the Morningstar Style Box where large cap stocks and value intersect. Prior to rebalancing we had a profile something like this:

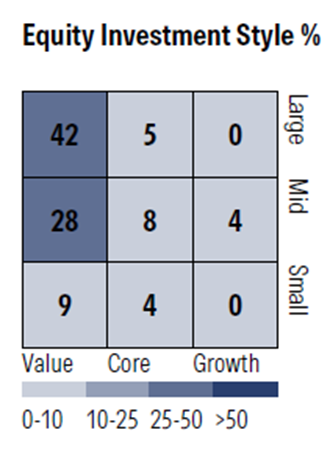

| | After rebalancing our accounts that are free of substantial taxable capital gains – IRAs, newer accounts, etc.- our holdings look more like this: | | |

So, we’re still value driven, as opposed to growth, but have broader exposure to mid- and small-cap stocks with, generally speaking: (1) lower P/E ratios, (2) smaller size, (3) lower debt/equity ratios and (4) larger dividends. Historically, stocks with these characteristics hold up better and bounce back stronger in a slowing economy.

Note that while we increased the number of companies in our portfolio, we didn’t really increase the total amount of stock exposure much, if at all. We have, to use an old Civil War term, kept some powder dry.

Broader Market Valuation

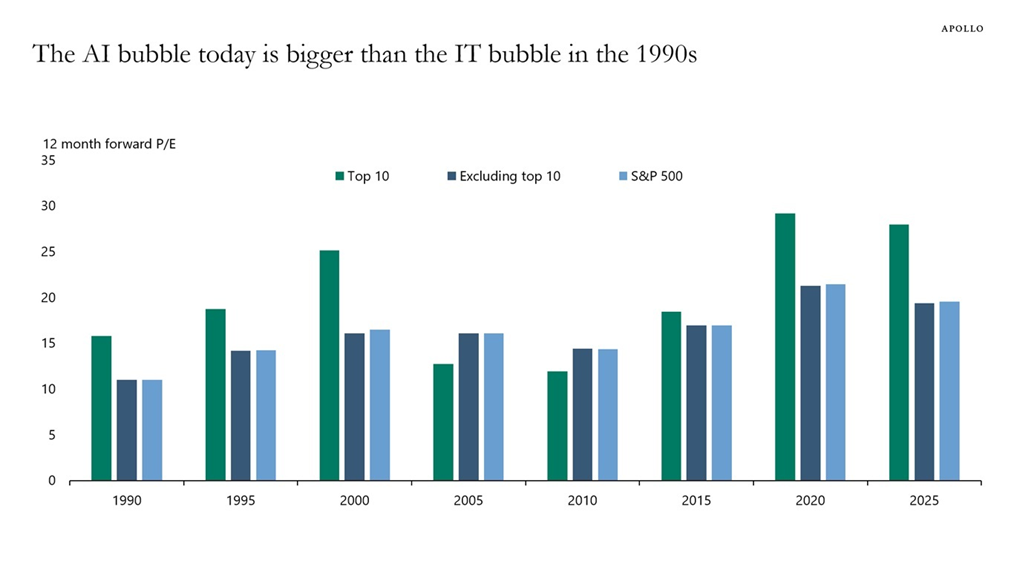

The broader market is pretty expensive by virtually all traditional measures. One sector leading the march higher is AI. With massive expenditures in software happening currently and planned expenditures in energy and infrastructure to keep the party going, AI is firmly in the realm of an investment bubble with P/E ratios dwarfing even the 1990’s IT bubble:

| | |

Where:

- “Top 10” denotes the P/E ratio 10 largest companies in the S&P 500 in green,

- “Excluding top 10” is the P/E of the other 490 companies in navy blue

- “S&P 500” is the S&P 500 (duh) in light blue.

Note, the IT bubble burst in 2001 and those stock valuations dropped substantially and stayed there for over a decade.

| | |

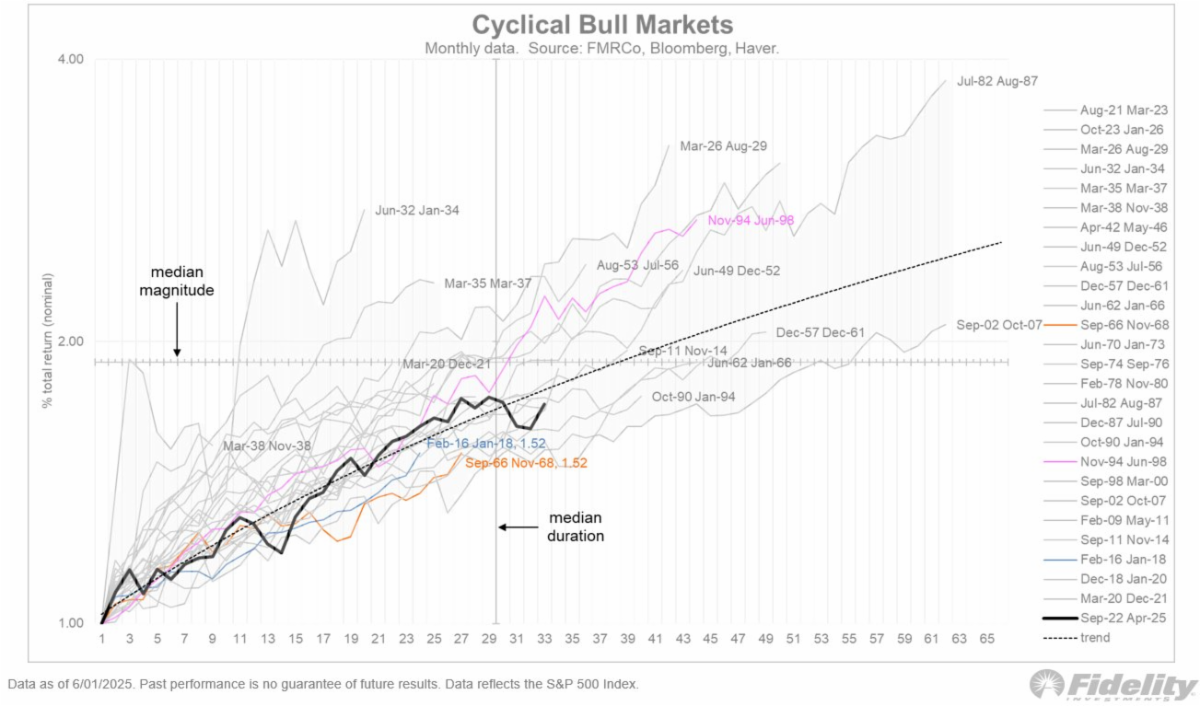

The above is from Fidelity Analyst Jurrien Timmer. He does quite a bit of work comparing market cycles and sees our current bull market cycle, the broader black line, as indicating that the bull hasn’t exactly run its course, it’s nearing the finish line.

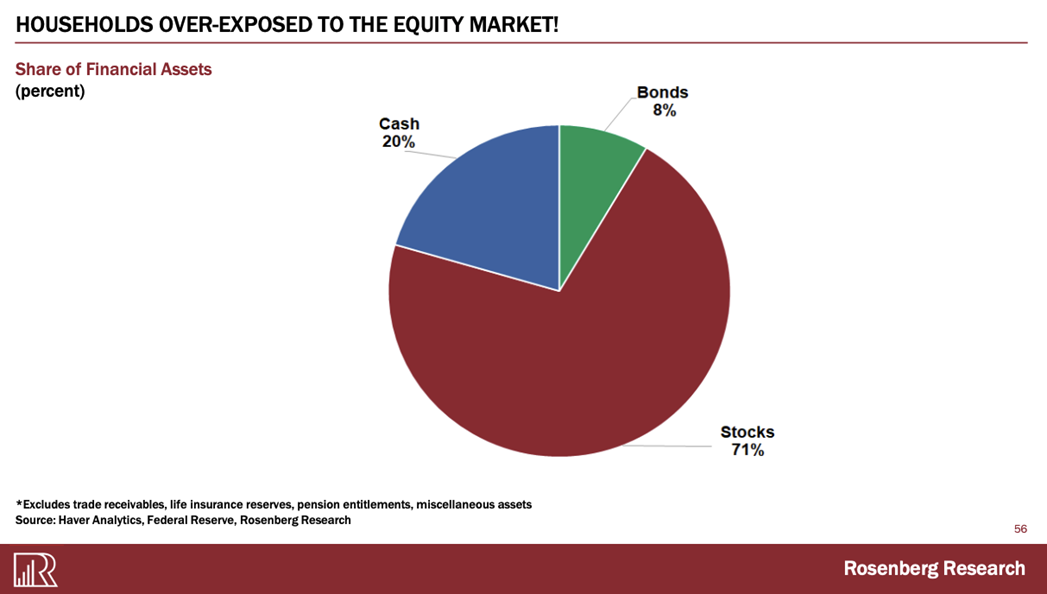

And last, from David Rosenberg, a look at individual households. I’ve shared before statistics showing more US households are holding stock than ever before – almost always a sign the party isn’t starting but is almost over. On top of that, the households that own stock, own more of it as a percentage of investable assets than ever before:

| | |

I suppose it makes sense that lots of people own lots of stock. Many of the new, exciting companies have risen a crazy amount, for a few years. I only hope some of those people heed the words of Warren Buffett:

“Never confuse brains with a bull market,”

And,

“When the tide goes out, you see who's been swimming naked”

As always, thank you for your encouragement, occasional scolding, jokes and, most of all, your trust. We are doing quite a few things to upgrade our website, reporting software and service. My daughter, Juliet, is working hard to streamline and update our documentation – many of you will hear from us via DocuSign toward that end in the coming weeks – and we’re excited to work with the several new clients who have joined us recently.

| | | | |