Gordon T Long Research exclusively located at MATASII.com

|

|

A SANCTION SUPPLY SHOCK & MORE SERIOUS SHORTAGES

The Ukrainian War is quickly turning into being as much a global financial crisis as a military conflict!

It is quite clear that whatever happens in Ukraine only aggravates a serious global problem around food, energy, and commodities generally.

By yet once again weaponizing US foreign policy through the use of economic sanctions, it may this time around go down in financial policy lore as the "Great Boomerang". Don't for a moment believe that Russia, China and the BRIICs weren't fully expecting it!

|

|

|

What economic sanctions against Russia are clearly triggering is the initial unwinding in the markets of decades of economic distortions in the developed western economies. Through a combination of currency and credit expansion and market suppression, the difference between market valuations and market reality has never been greater. Zero and negative interest rates, deeply negative real bond yields, and a deliberate policy of artificial wealth creation, by fostering a financial asset bubble to divert attention from a deepening economic crisis in recent years, have all contributed to the gap between bullish expectations and market reality. |

|

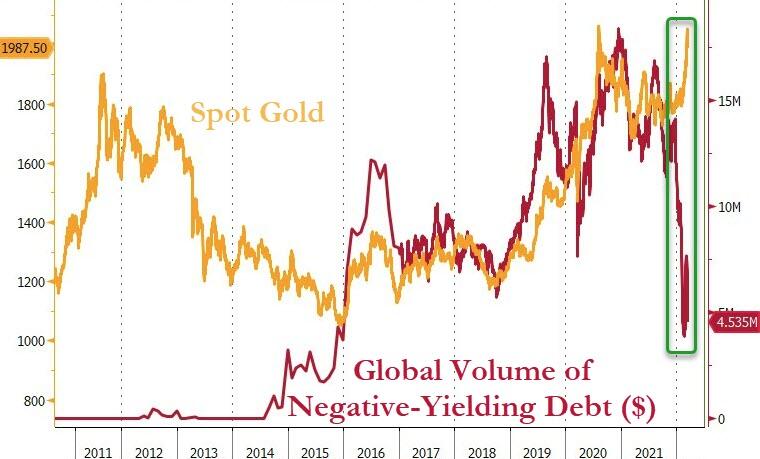

NEGATIVE YIELDING SOVEREIGN DEBT IS DISAPPEARING RAPIDLY! |

Investors have rediscovered the real safe-haven once again is hard assets (like Gold and Commodities) as global negative-yielding debt has dropped to just $4 trillion from over $16 trillion.

From the record highs in November, global bond and stock markets are down $18 trillion!

Gold & hard assets have become a real alternative to holding paper assets with increasing and worrying military turmoil.

|

|

|

WARNING

THE FED'S FOMC PRESS MEETING ON WEDNESDAY 03-16-22 MUST REFLECT ...

THE NEW REALITY OF SUSTAINED INFLATIONARY SANCTIONS!

FED RATES WILL GO UP WEDNESDAY BUT ALSO EXPECT THE FED TO SIGNAL 50 POINT HIKES IN FUTURE MEETINGS.

|

|

PUTIN IN AN ESCALATION CORNER - Must Escalate to De-escalate!

There is little doubt Putin made a massive miscalculation in invading Ukraine, but the West’s hurried reaction by seeking to isolate Russia and its commodity exports from the global marketplace is likely to prove to be an even greater miscalculation and problematic approach.

Putin is presently being forced into a corner and we have not yet seen his response. The consequence of the failure to take Ukraine will highly likely increase the likelihood that Putin will escalate the energy and commodity crisis as a means of destabilizing Russia’s Western enemies.

|

|

PUTIN HAD CLEARLY PREPARED FOR MORE THAN JUST AN INVASION OF UKRAINE!

He sold all his US Treasury Holdings and accumulated large FX Holdings of Gold Bullion Stored Safely in Russia

What else did he prepare for in addition to having an alternative to SWIFT ???

|

|

Putin could obviously see that the US fiscal and monetary situation was becoming untenable and we suspect he (and President Xi Jinping) decided to use this to create an existential threat to the US and the world financial system. They have both been quite public on their views on a new world order and their place in it.

Putin undoubtedly knows that the West has artificially suppressed the price of gold since former US Treasury Secretary Larry Summers' work on the "Gibson's Paradox" in the late 80s. As a consequence Putin has been building his gold reserves steadily for the past 20 years and accelerated accumulation over the 4 years (chart above).

PUTIN'S OPTIONS

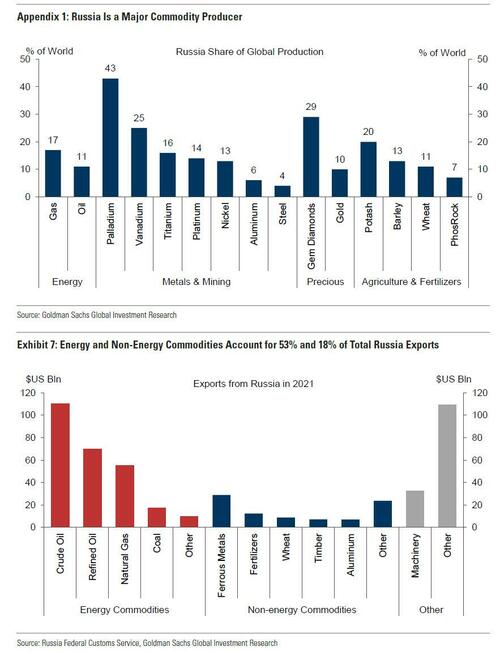

"Besides oil and natural gas, Russia exports substantial amounts of food crops and precious metals used in industrial production like aluminum, titanium, palladium, platinum, nickel, cobalt and copper.

Consumers are familiar with the retail end of the supply chain. But they aren’t as familiar with the input end. If you can’t source the raw materials, you can't produce finished goods.

For example, the farmers who grow food and raise livestock and the butchers and food processors who prepare that output into meat, poultry, bread and dairy products are not the source of the supply; they are intermediaries. The source of the supply chain is in fertilizers made from chemicals, especially nitrogen and phosphate.

Any break or bottleneck anywhere in this supply chain will result in either higher prices or empty shelves at the consumer end.

If Russian nitrogen exports are diminished and prices soar, that has a global impact including on U.S. farms. The impact of higher fertilizer prices does not stop with grain. Most grains are used not for direct consumption by humans but as feed grains for livestock. That means the fertilizer price increase will flow through to meat, poultry, eggs and dairy products.

These breaks are already occurring. Russia and Ukraine together provide more than 25% of the wheat supply in world trade and 20% of global corn sales. Ukrainian exports are already in disarray because of the war and Russian exports are being handicapped by the sanctions.

We learn through various sources that the Chinese have been "prescient" enough (or well planned and prepared for) to stockpile enormous quantities of grains and other comestible materials to protect their citizens from a summer food crisis.

- Twenty per cent of the world’s population has secured more than half the globe’s maize and other grains (Nikkei Asia, 23 December – see Figure 1). That was two months before Putin ordered the invasion of Ukraine, which has made the position over global food supplies even worse.

- China’s dominant position in maize will hit sub-Saharan Africa especially hard, while global shortages of rice will hit Southern and East Asian nations.

|

|

RUSSIAN RETALIATION

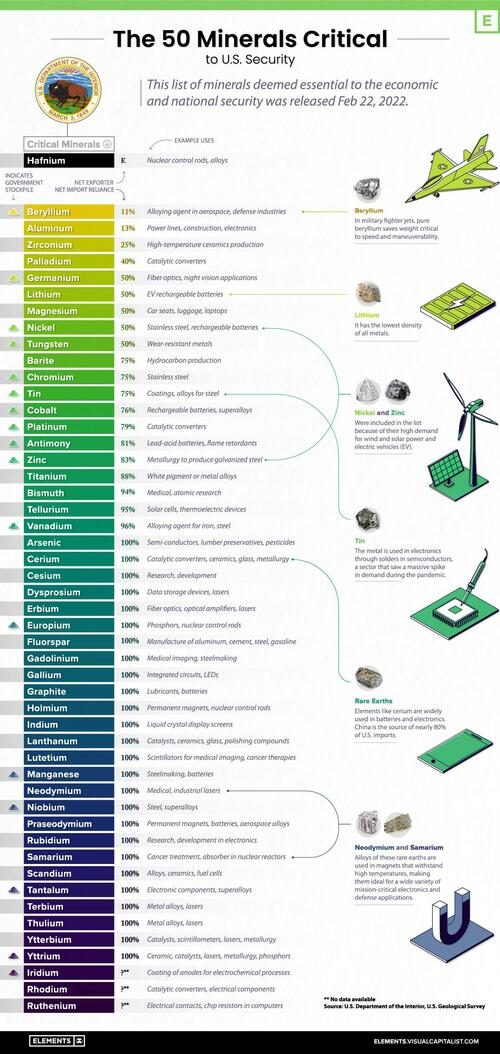

Between Russia, China, the BRIICS and aligned African resource nations, they control Global Industrial Raw Materials.

They now have the ability to choke / bypass the Industrial West if incented or forced to do so, because of what they see as predatory sanctions!

The aligned BRIIC nations along with the African countries now under agreement with China dominate global commodity production and supply. WILL THEY CHOKE THE WEST if a broader conflict develops? A conflict that Putin and President Xi see as a new world order. It is no coincidence that BRIIC member India has now formally come out (as sanctions are being applied) that they will continue to trade (and expand?) trade with Russia through a Rupee-Ruble Payments System.

|

|

WILL SANCTIONS DESTABILIZE THE EU BANKING SECTOR?

Sovereign, Corporate IG and HY bond prices are collapsing and with them their collateral supporting loans, VaR (Value-at-Risk) exposures as well as short term counterparts funding exposures. Together they have the potential to take down the whole banking system in a cascading collateral failure from top to bottom. This is because they are all leveraged "to the gills" with seriously weakening bonds and financial assets as collateral. The consequences for the global banking system are potentially frightening!

The commercial banking networks with the highest leverage are in the Eurozone with its G-SIBs asset to equity ratios averaging over 21 times, with some considerably higher. The Japanese banks are also at about 21 times. Both the ECB and the BOJ have imposed negative interest rates, so the rise in global interest rates are bound to wipe out commercial bank capital in these jurisdictions first.

|

|

RISING INFLATION BREAKEVENS AND FALLING NEGATIVE REAL RATES ARE POSITIVE FOR GOLD |

|

A CASCADING "COMMODITY COLLATERAL" CRASH? |

We are not talking about Commodity prices crashing - but rather quite the opposite!

Commodities are Collateral! Collateral is Money!

We can expect Commodities or hard assets to become an integral part of the value of of money as the US Dollar becomes less dominant in global trade. Commodities are not actually exploding upward. What is happening is fiat currency values are effectively being repriced lower on Geo-Political Risk.

A BRETTON WOODS III

While many have been predicting the birth of a new monetary system in the past decade, it is the nuances of the infamous Zoltan Pozsar's vision of the monetary future that is especially troubling presently on Wall Street. As he writes, we are now seeing "a regime shift unfold in funding markets current and a sea change in inflation dynamics and FX reserve management practices."

"We are witnessing the birth of Bretton Woods III a new world (monetary) order centered around commodity-based currencies in the East that will likely weaken the Eurodollar system and also contribute to inflationary forces in the West."

"A Crisis of Commodities: Commodities are collateral, and collateral is money, and this crisis is about the rising allure of outside money over inside money. Bretton Woods II was built on inside money, and its foundations crumbled a week ago when the G7 seized Russia's FX reserves".

The legacy of a western monetary system based on fiat currencies (and a US dollar reserve) appears about to end in an inflationary supernova. It will be replaced with a metallic monetary system, one using commodity-based currencies as a payment method (however, not quite a gold standard). One where China and the yuan will likely become the world's most important sovereign and currency, respectively.

|

|

|

CONCLUSION

The Russian invasion of Ukraine and the corresponding Western sanctions and seizure of Russian FX reserves are nothing short of a monetary earthquake. Russia, with the backing and support of China has just told the world that it is no longer going to sell its oil, gas and wheat for Western currencies which are programmed to debase. The West in its response just said in effect to all countries around the world: “If you have foreign exchange reserves, held in our system, they are no longer safe if we disagree with your politics.”

"It is similar to what the Canadians did when they moved to seize the bank accounts of Canadians who had demonstrated support for the truckers without due process of law. Both of these political moves are blatant advertisements for what I call 'non-state controlled money without counterparty risk', like gold and bitcoin. If governments can weaponize their money when they do not like what you are doing, what is the natural defense?"

Lawrence Lepard Manager of the EMA GARP Fund, a Boston based investment management firm

What is happening here is that whoever holds the most gold will hold the most real wealth, and by extension, gain the most prominent seat at the bargaining table for decades to come in a New World Order. Whether that table will be the IMF, the new AAIB (Asian Infrastructure Investment Bank) or any future central economic entity, the future will go to the player with the most metal, as they will be able to create the most currency, in whatever form it may take.

|

|

A US RECESSION

All of the above along with an ineffective political response to the Ukraine conflict will push the US into a Recession in 2023 or earlier.

DURING THE LOOMING NEXT RECESSION RUSSIA, CHINA and BRIICs will likely make their next push for a New World Order.

Not every recession is led by a 50% rise in crude.

But every 50% rise in crude has led a recession.

|

|

Yield Curve is now Flat and Nearing Inversion |

|

CURRENT MARKET PERSPECTIVE |

|

COMMODITIES ARE NOT FIAT! |

|

GOLD IS AGAIN THE GEO-POLITICAL HEDGE!

FEAR IS EVERYWHERE!

Gold along with the US Dollar has been the recipient of a major Flight-to-Safety since late January as can be seen by the shaded area in the gold chart to the right.

We have reached recent highs that signal a double top formation with the 2020 price high that kicked off a 20-month consolidation before recently leaping from a “coiled” spring position.

Our view on Gold is that contrary to the US Dollar, it is only beginning to be a Flight-to-Safety instrument, as it increasingly becomes once again a Geo-Political Risk Hedge. This is because we are now experiencing the results of mounting global tensions and the beginning of a shift in the World Order.

|

|

YOUR DESK TOP / TABLET / PHONE ANNOTATED CHART

NOTE: Any Problems with this Chart: E-Mail lcmgroupe2@comcast.net

|

|

NOTICE Information on these pages contains forward-looking statements that involve risks and uncertainties. Markets and instruments profiled on this page are for informational purposes only and should not in any way come across as a recommendation to buy or sell in these assets. You should do your own thorough research before making any investment decisions. MATASII.com does not in any way guarantee that this information is free from mistakes, errors, or material misstatements. It also does not guarantee that this information is of a timely nature. Investing in Open Markets involves a great deal of risk, including the loss of all or a portion of your investment, as well as emotional distress. All risks, losses and costs associated with investing, including total loss of principal, are your responsibility.

|

|

MATASII'S STRATEGIC INVESTMENT INSIGHTS |

|

2020 VIDEOS OUTLINING THE COMING RISE IN INFLATION & COMMODITY PRICES |

|

RELEASED - 03-09-22

VIDEO: 19 Minutes with 46 supporting slides.

|

|

IDENTIFICATION OF HIGH PROBABILITY TARGET ZONES |

|

Learn the HPTZ Methodology!

Identify areas of High Probability for market movements

Set up your charts with accurate Market Road Maps

Available at Amazon.com

|

|

The Most Insightful Macro Analytics On The Web |

|

PO Box 1224,

Norton, MA 02766

(508) 285 2213

|

|

|

|

|

|

|

|