Weekly update from the National Housing Conference | | News from Washington | By Brittany Webb | | |

Affordable HOMES Act passes House

The U.S. House of Representatives passed H.R. 5184, the Affordable HOMES Act, by a bipartisan vote of 263–147, advancing legislation aimed at strengthening housing affordability and supply through manufactured housing. A total of 57 Democrats voted in favor of the bill, and no Republicans opposed. Ahead of the vote, a group of affordable housing organizations, led by the National Housing Conference, urged House leadership to support the bill, emphasizing that manufactured housing is one of the fastest and most affordable ways to expand housing options for lower-income households.

The Affordable HOMES Act, introduced by Representatives Erin Houchin (R-Ind.) and Jake Auchincloss (D-Mass.), would return sole authority over manufactured housing energy efficiency standards to the U.S. Department of Housing and Urban Development (HUD), eliminate overlapping authority granted to the Department of Energy (DOE), and rescind DOE’s May 2022 manufactured housing energy efficiency rule which has not yet gone into effect. It also provides the ability for DOE to provide recommendations to HUD as a part of its process to update the HUD code. Housing advocates stressed that while energy efficiency remains an important goal, standards must be workable, cost-effective, and developed by housing experts.

“Higher energy efficiency standards are an important goal, but they must be designed with affordability in mind and by the agency with housing expertise,” the letter states, noting that HUD has regulated manufactured housing standards since 1974. “At a time when our nation urgently needs more affordable housing of all kinds, unworkable standards, increased costs, and regulatory confusion only hamper progress,” the letter concludes.

“As demand for affordable homes has surged, so have unnecessary costs, making the dream of homeownership slip further out of reach for Americans. The Affordable HOMES Act takes a practical approach by cutting red tape and regulations that contribute to pricing American families out of owning a home, which will increase supply and lower costs,” said Rep. Houchin.

"Affordable homeownership should be Congress's top economic priority," said Rep. Auchincloss. "This bill makes progress by unlocking production of manufactured housing and lowering prices by up to $10,000 per unit. Coming off a big bipartisan vote in the House, the Senate should pass this, fast, to start cutting costs in the housing market."

In addition to NHC, the letter was signed by Atlanta Neighborhood Development Partnership, Inc., California Community Reinvestment Corporation (CCRC), CBC Mortgage Agency and the Chenoa Fund, Community Solutions, Homeownership Council of America, Inclusive Abundance Action, Manufactured Housing Institute, Mortgage Bankers Association, and UnidosUS.

| |

Trump proposes ban on large institutional investors

President Donald Trump stated on social media the federal government will move to ban large institutional investors from purchasing single-family homes, framing the proposal as part of a broader effort to improve housing affordability and expand homeownership opportunities. He said the policy would take effect in 2026 and would target large financial firms and investment funds that have increasingly acquired single-family homes in recent years. He further called on Congress to codify whatever steps are taken in law, though it is unclear if he can.

“People live in homes, not corporations. I will discuss this topic, including further Housing and Affordability proposals, and more, at my speech in Davos in two weeks,” the post reads.

The Administration cited concerns that large-scale investor activity has contributed to rising home prices and reduced the availability of entry-level homes for first-time buyers, particularly in fast-growing metropolitan areas.

Housing analysts and industry groups cautioned that the proposal could face legal and implementation challenges, noting that institutional investors account for a relatively small share of total single-family home purchases nationally but are more concentrated in certain markets. According to data from Cotality, investors are now buying 25% fewer homes than they were five years ago when pandemic markets spurred increased interest and bidding wars. Critics also warned that limiting investor participation could reduce rental supply in some regions, while supporters argued the policy could ease competitive pressures on owner-occupants and help rebalance the market toward homeownership.

| | | |

Fannie Mae, Freddie Mac directed to buy $200 Billion in mortgage bonds

In a post on social media, President Trump directed Fannie Mae and Freddie Mac (the Enterprises) to purchase $200 billion in mortgage bonds, which he says will lower mortgage interest rates and help address housing affordability concerns across the nation. The statement prompted a decrease in the spread between the interest rate on mortgage bonds and Treasuries by 0.1 percentage points. The Enterprises have already been increasing their holdings of mortgage bonds by over 25% since October. The post emphasizes a recent focus on housing affordability and levers that the Administration is exploring for addressing overall housing costs.

“There is no question if Fannie and Freddie get back into buying mortgage bonds for their portfolios, mortgage rates will undoubtedly fall,” said NHC President and CEO David Dworkin. Other experts reported skepticism and concern that the Enterprises could again become “buyers of last resort” for mortgage bonds.

The Federal Housing Finance Agency (FHFA) also adopted new affordable housing purchase goals at the end of 2025, effective on February 23, reducing some low-income single-family purchase goals for each Enterprise. NHC submitted comments on the change as part of the Underserved Mortgage Markets Coalition, urging FHFA to maintain the purchase goals and not issue reductions.

| | | |

Treasury announces $10B New Markets Tax Credit awards and program updates

The U.S. Department of the Treasury announced $10 billion in New Markets Tax Credit (NMTC) allocations covering the 2024 and 2025 rounds, marking the first awards issued following the program’s permanent authorization. According to Treasury and industry analysts, the combined allocation represents the largest single issuance in the program’s history.

The latest allocations place increased emphasis on rural and non-metropolitan communities, with roughly 20 percent more investment directed to those areas compared to prior rounds. Funded projects are expected to support small businesses, health care facilities, manufacturing, and community infrastructure in low-income communities.

Treasury also outlined steps to strengthen compliance and oversight of what it describes as enforcement of federal anti-discrimination laws, including enhanced monitoring of award recipients and clearer enforcement mechanisms. Treasury officials said future NMTC allocations will continue to prioritize projects that deliver measurable community benefits, including job creation, access to essential services, and investments that support affordable housing and economic development in underserved areas.

“Investors, businesses, and communities now have the long-term certainty they need to plan ahead. With the NMTC program now permanent, it is imperative that these federal incentives are focused on lasting job creation rather than the latest political trends,” stated Treasury Secretary Scott Bessent.

“This $85 million New Markets Tax Credit award will enable us to continue driving transformative projects in underinvested communities, creating opportunity where it is needed most,” said Mark McDaniel, President and CEO of Cinnaire, an allocation recipient. “With the NMTC program now made permanent, we can plan for long-term, high-impact investments that strengthen local economies, support workforce development, and build more resilient communities for decades to come.”

| |  | |

HUD reports FHFA MMI Fund remains well above requirements

The U.S. Department of Housing and Urban Development (HUD) released its annual report on the Federal Housing Administration’s (FHA) Mutual Mortgage Insurance (MMI) Fund, reporting that the current MMIF capital ratio remains at 11.47%, more than quintuple the statutory 2% requirement and unchanged from FY 2024.

HUD said the results underscore FHA’s ability to responsibly manage risk while continuing to support access to mortgage credit for first-time and underserved homebuyers, particularly in a high-rate environment. FHA-insured loans continue to represent a disproportionate share of lending to first-time buyers and borrowers with moderate incomes, reinforcing the agency’s countercyclical role as conventional financing becomes less accessible.

The Mortgage Bankers Association acknowledged the strengthened capital position of the MMI Fund in its briefing of the report and further acknowledged that the report may prompt policy changes. Bob Broeksmit, MBA President and CEO, stated they “will review the report in greater detail to assess whether any policy changes are warranted to improve affordability and access to homeownership in 2026, including a potential reduction in FHA’s annual mortgage insurance premiums. Any such changes should be calibrated responsibly and informed by a careful evaluation of the program guidelines and the economic factors behind the rising serious delinquency rate to ensure the program remains safe, sound, and sustainable.”

| | | |

Fed issues CRA asset thresholds

The Federal Reserve Board, in coordination with the Federal Deposit Insurance Corporation, announced updated asset-size thresholds under the Community Reinvestment Act (CRA) that will apply as of January 1 this year. The annual adjustment reflects changes in the Consumer Price Index for Urban Wage Earners and Clerical Workers, measuring inflation, and determines how banks are categorized for CRA examination purposes.

Under the update, a bank will be considered a “small bank” if it has assets of less than $1.649 billion, while institutions with assets of at least $412 million but less than $1.649 billion will be classified as “intermediate small banks.” These designations affect the scope and structure of CRA evaluations, including the lending, investment, and service tests applied by regulators. The updated thresholds will remain in effect throughout calendar year 2026.

| | | |

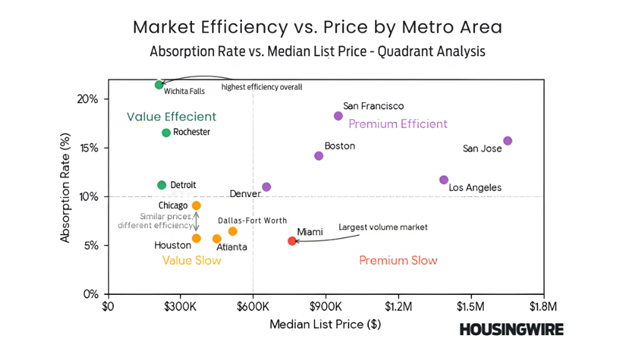

Market absorption offers insight into behaviors of metros

A new analysis from HousingWire examines absorption rate as a key indicator of housing market efficiency, arguing that it offers clearer insight into near-term market pressure than market size alone. Absorption rate measures the share of active listings that go under contract in a given week, capturing how quickly inventory is being cleared and how competitive conditions are for buyers. The analysis shows that metro areas with similar median home prices can experience very different levels of competitive pressure, underscoring that price levels alone do not fully explain market dynamics. By focusing on absorption rather than total inventory or sales volume, the data highlights where demand is outpacing supply in real time, providing a more precise signal of tightening or loosening market conditions as affordability challenges persist.

| | |

Leading housing and civil rights organizations submitted comment letters in response to the CFPB’s proposed changes to the Equal Credit Opportunity Act, emphasizing the risks of weakening fair lending protections. NHC’s letter, along with those from the Housing Assistance Council, HOPE, the National Association of REALTORS®, NAHREP, and NFHA, urges regulators to preserve disparate impact, discouragement, and special purpose credit program provisions to ensure discriminatory practices can still be identified and remedied. The letters warn that narrowing ECOA’s reach could deepen racial and geographic gaps in access to safe, affordable credit and undermine efforts to advance homeownership.

NPR reports on a new generation of shelters specifically designed for unhoused seniors, highlighting a converted hotel outside Salt Lake City that offers semi-private, wheelchair-accessible rooms and in-room bathrooms for people 62 and older or those with complex health conditions. The shelter pairs with age-appropriate design with on-site medical care, medication management, and case management, allowing residents to stabilize their health and ultimately move into permanent housing.

An article from National Mortgage Professional takes a measured look at how artificial intelligence is actually being used across the mortgage industry, pushing back on potential inflated expectations and marketing hype. The piece finds that while AI adoption is expanding, most deployments remain narrowly focused on operational efficiencies, such as document processing, customer communications, and compliance support, rather than fully autonomous underwriting or credit decision-making. Industry leaders quoted in the article stress that data quality, regulatory risk, and explainability continue to limit broader applications, reinforcing that AI is more likely to function as an assistive tool than a replacement for human judgment in the near term.

The National Housing Conference (NHC) was widely quoted in major national media following President Donald Trump’s recent housing policy announcements, including plans for Fannie Mae and Freddie Mac to purchase up to $200 billion in mortgage bonds and efforts to prepare an executive order focused on housing affordability. NHC’s insights were featured in The Washington Post, The Wall Street Journal, The New York Times, and Bloomberg.

| | The National Housing Conference is a diverse continuum of affordable housing stakeholders that convene and collaborate through dialogue, advocacy, research, and education, to develop equitable solutions that serve our common interest. | | Defending Our American Home since 1931 | | Copyright © 2024. All Rights Reserved. | | | | |