|

Monthly Market Update for May: New Highs, IPOs, Inflation, and a new Fed Chair

June 2026

| | |

Pat McFawn | Financial Advisor - Registered Representative

Dale White | Financial Advisor - Registered Representative

Steve McFawn | Financial Advisor - Registered Representative

| | |

May was a strong month for investors, with major indices reaching new all-time highs, even as the bond market faced challenges from inflation concerns. The S&P 500 climbed above 7,500 for the first time, supported by continued strength in technology stocks. At the same time, long-term interest rates rose to nearly two-decade highs before moderating later in the month as oil prices declined. Hopes for a peace deal in Iran also supported markets, although the situation remains uncertain.

May also marked a leadership transition at the Federal Reserve for the first time since 2018, with Kevin Warsh sworn in as the new Fed Chair. While this naturally raises questions around monetary policy, history shows that markets and the economy have performed well across many different Fed leaders. For long-term investors, recent strength in the stock market is welcomed, although it is important to maintain portfolio balance to navigate all parts of the market cycle.

Key Market and Economic Drivers in May

- The S&P 500, Nasdaq, and Dow Jones Industrial Average gained 5.1%, 8.4%, and 2.8%, respectively, for the month. All three major U.S. indices finished the month at new all-time highs.

- Volatility declined over the month, as measured by the CBOE VIX index, ending May at 15.32.

- International developed markets returned 2.6% based on the MSCI EAFE Index in U.S. dollar terms, while emerging markets returned 9.5% based on the MSCI EM Index.

- The 30-year Treasury yield reached 5.18%, its highest level in nearly two decades, before finishing the month below 5%. The 10-year Treasury yield rose to 4.4%. The Bloomberg U.S. Aggregate Bond Index returned 0.3% for the month.

- Oil prices fell with Brent crude closing at approximately $92 per barrel and WTI at $88.

- Gold ended the month slightly lower at $4,539 per ounce. The U.S. Dollar Index stood at 98.94, also down only slightly.

- First quarter real GDP was revised lower from 2.0% quarter-over-quarter to 1.6%. April inflation showed headline CPI at 3.8% year-over-year and core CPI at 2.8%.

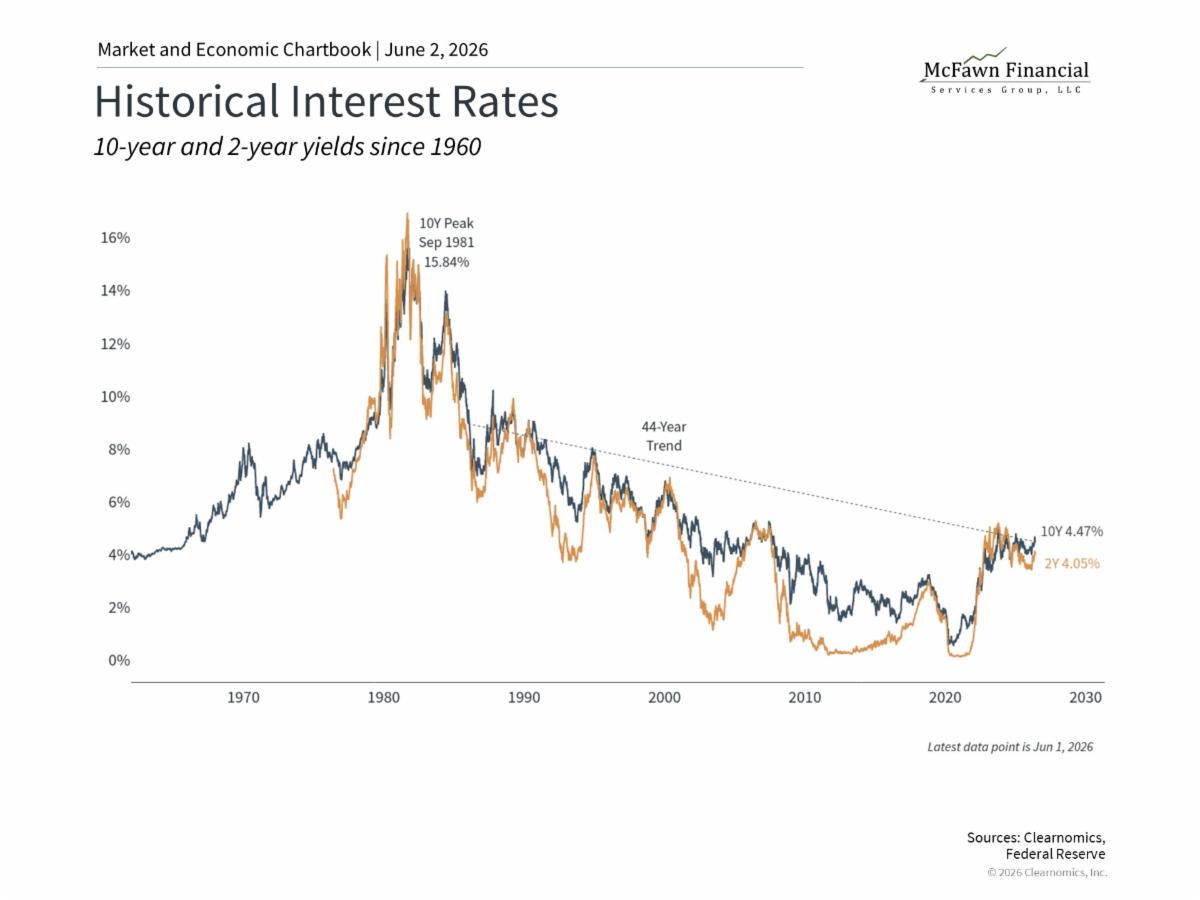

Long-term interest rates rose before moderating

| | |

One of the most important developments in May was the volatility in interest rates. The 30-year U.S. Treasury yield reached its highest level in nearly two decades during the month, before settling back below 5%.1 The 10-year and 2-year yields both rose as well, as expectations that interest rates would stay higher for longer grew. The market now expects the Fed to hike rates once by the middle of 2027 in response to inflation concerns.

This occurred because both the Consumer Price Index and Producer Price Index reports came in above expectations due to energy prices. Rising inflation tends to push interest rates higher, since investors require more compensation if each dollar is worth less. The concern among some economists is that inflation will broaden across all goods if fuel prices stay higher for longer. Oil prices have come down slightly, to around $4.30 per gallon on average across the country, but this is still about $1.50 higher than before the war in Iran.2

Higher interest rates matter because they affect all parts of the economy and markets, especially if they are the result of inflation. For consumers, there is a direct effect on the cost of borrowing including personal loans and mortgage rates. The same is true for businesses since it affects the cost of financing their operations, borrowing to grow, and more.

When it comes to financial markets, higher rates mean that future cash flows are worth less today than they otherwise might be, affecting today’s asset prices. At the same time, higher yields mean that bonds are now offering more meaningful income than they have in many years, which can support diversified portfolios going forward.

Still, it’s important to maintain perspective on these moves. Markets have swung in both directions multiple times this year on changing expectations for a peace deal, and the situation continues to evolve. Interest rates have also been very difficult to predict over the past several years. While they remain high today, they are also far lower than many feared when inflation was running hotter and when the Fed was raising rates.

The stock market reached new all-time highs

| | |

In spite of higher interest rates and headwinds to the bond market, the stock market continues to reach new all-time highs. The S&P 500 surpassed 7,500 in May for the first time and there have been 22 all-time highs this year through the end of May.3 While the Magnificent 7 and other large technology stocks have continued to support the market, the rally has also been broader than in some prior years.

This strong market backdrop has fueled interest in upcoming IPOs for companies such as SpaceX, Anthropic, OpenAI, and others. These companies have grown primarily through private investments, and the trend over the past two decades has been for companies to remain private for longer. While attention is often paid to the immediate stock price moves after companies go public, the long-term benefit is that IPOs broaden the opportunity set for all investors. If you consider today’s large tech companies, for instance, it’s not their IPOs that are most important, but how they have performed in the decades since.

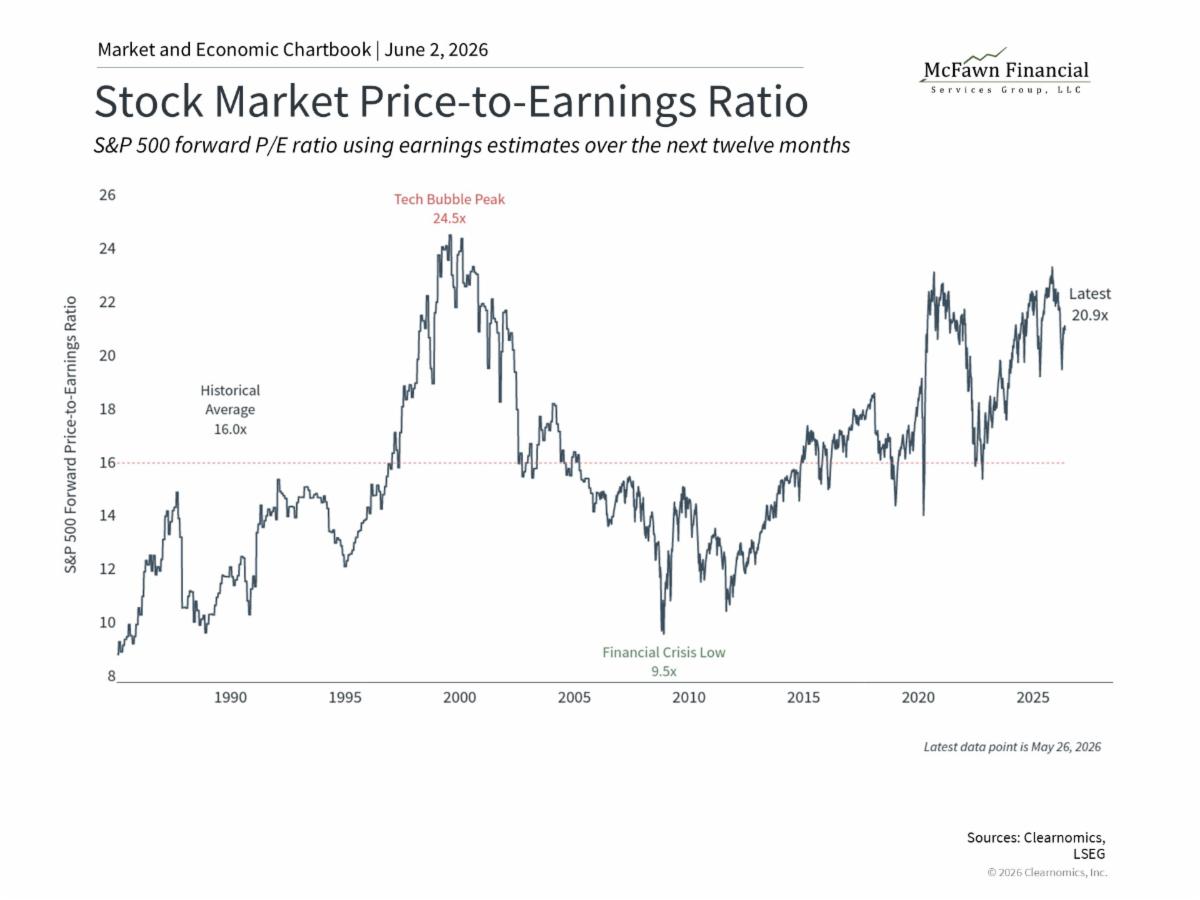

The fact that major indices reach new all-time highs is not unusual during a bull market. Historically, markets have trended upward over long periods of time, which means they often spend much of that time at or near record levels. What matters more than the level of any single index is whether the underlying fundamentals remain healthy. Corporate earnings have continued to grow at a healthy pace, with consensus estimates pointing to further growth in the coming year.4

Strong corporate earnings growth has helped to keep valuations stable, even as the market has reached new highs. The S&P 500 price-to-earnings ratio, for instance, is hovering around 20.9x, within the range of the past several years. At the same time, these valuations are well above long-term historical averages. While elevated valuations do not predict what the market will do over the next year or two, they are an important consideration when it comes to building portfolios for the long run. Maintaining balance across sectors, sizes, and styles can help investors manage risk while still benefiting from market trends.

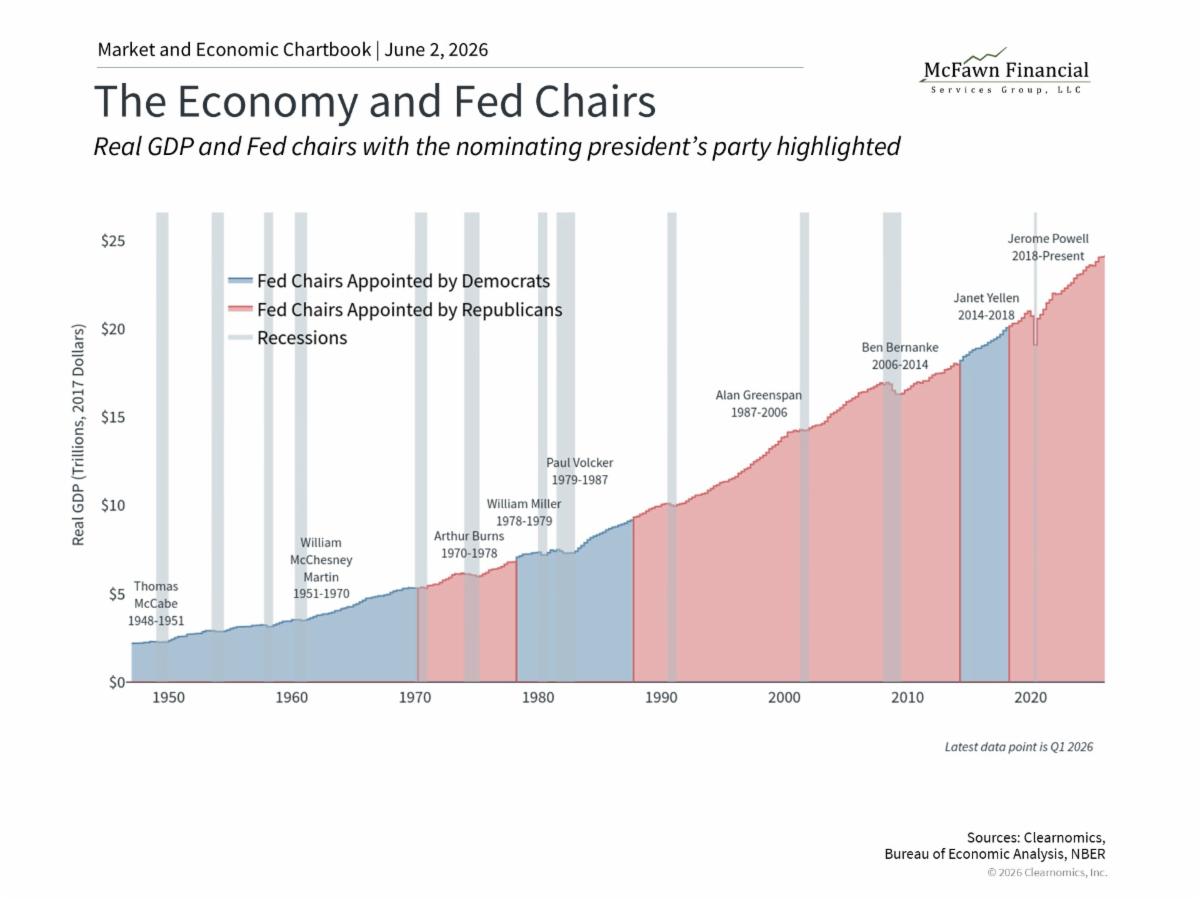

Kevin Warsh sworn in as the new Fed Chair

| | |

Kevin Warsh was sworn in as the new Chair of the Federal Reserve in May, succeeding Jerome Powell. Warsh previously served on the Fed's Board of Governors during the 2008 global financial crisis and is viewed by markets as a known quantity with experience in monetary policy and financial markets.

Fed leadership transitions happen infrequently by design, so they naturally raise questions about the path of policy in the years ahead. Warsh is seen as a reformer, which can raise more uncertainty as to how a Fed under his leadership will conduct monetary policy. In his recent Senate testimony, Warsh emphasized that monetary policy independence is essential and that policymakers must act in the nation's interest. He has also signaled a preference for a more focused central bank, with views that have historically leaned toward managing inflation risks.

Regardless of what reforms Warsh might bring to the Fed as an institution, it’s clear that policymakers face a challenging economic environment. The overall economy is still healthy, but inflation has accelerated in recent months while the labor market has been mixed. Supporting hiring would normally call for lower rates, while addressing inflation would suggest tightening financial conditions. This creates a difficult balancing act, and markets have now flipped from expecting further rate cuts to at least one rate hike.5

For investors, history shows that the economy has grown across the tenures of many different Fed chairs, regardless of political environment or policy approach. Earnings growth, productivity, demographics, and innovation are ultimately the most important drivers of long-run returns. Changes at the top of the Fed can generate uncertainty, but they rarely alter these long-term fundamentals.

The bottom line? May brought new milestones for the stock market, extending a strong run for investors. While headlines around inflation, the new Fed Chair, and geopolitics will likely continue to generate uncertainty, the best approach for investors is still to focus on their long-term financial goals.

References

1. https://home.treasury.gov/policy-issues/financing-the-government/interest-rate-statistics

2. https://gasprices.aaa.com/

3. Clearnomics research based on Standard & Poor’s index data

4. Clearnomics research based on LSEG earnings data

5. https://www.cmegroup.com/markets/interest-rates/cme-fedwatch-tool.html

| | The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. | | |

As always, if you have any questions, please do not hesitate to call us at (248) 619-0090.

This information, developed by an independent third party, Clearnomics, has been obtained from sources considered to be reliable, but Raymond James Financial Services, Inc. does not guarantee that the foregoing material is accurate or complete. This information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. This information is not intended as a solicitation or an offer to buy or sell any security referred to herein. Investments mentioned may not be suitable for all investors. The material is general in nature. Past performance may not be indicative of future results. Raymond James Financial Services, Inc. does not provide advice on tax, legal or mortgage issues. These matters should be discussed with the appropriate professional. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected, including diversification and asset allocation. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Holding bonds to term allows redemption at par value. There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Raymond James is not affiliated with nor sponsors or endorses Clearnomics or any of the aforementioned organizations.

Leading Economic Indicators are selected economic statistics that have proven valuable as a group in estimating the direction and magnitude of economic change. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. Inclusion of this index is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transactions costs or other fees, which will affect actual investment performance.

The Bloomberg U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market. The MSCI EAFE Index represents the performance of developed markets outside of the U.S. and Canada (Europe, Australasia, and the Far East). The MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Market (EM) countries. The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies. The Consumer Price Index (CPI) measures the average change over time in the prices paid by urban consumers for a basket of goods and services. It is one of the most widely used indicators for inflation.

| | |

Securities offered through Raymond James Financial Services, Inc. member FINRA/SIPC. Investment advisory services are offered through Raymond James Financial Services Advisors, Inc. McFawn Financial Services Group, LLC is not a registered broker/dealer and is independent of Raymond James Financial Services.

The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stock of companies maintained and reviewed by the editors of the Wall Street Journal.

The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represent approximately 8% of the total market capitalization of the Russell 3000 Index.

Bitcoin issuers are not registered with the SEC, and the bitcoin marketplace is currently unregulated. Bitcoin and other cryptocurrencies are a very speculative investment and involves a high degree of risk.

Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

Please visit https://www.raymondjames.com/legal-disclosures/social-media-disclaimer-icd for Additional Risk and Disclosure Information. Raymond James does not accept private client orders or account instructions by email. This email: (a) is not an official transaction confirmation or account statement; (b) is not an offer, solicitation, or recommendation to transact in any security; (c) is intended only for the addressee; and (d) may not be retransmitted to, or used by, any other party. This email may contain confidential or privileged information; please delete immediately if you are not the intended recipient. Raymond James monitors emails and may be required by law orregulation to disclose emails to third parties.

Investment products are: Not deposits. Not FDIC or NCUA insured. Not guaranteed by the financial institution. Subject to risk. May lose value.

This may constitute a commercial email message under the CAN-SPAM Act of 2003. If you do not wish to receive marketing or advertising related email messages from us, please reply to this message with "unsubscribe" in your response. You will continue to receive emails from us related to servicing your account(s).

| | | | |