|

Quarterly Market Update for Q2 2026: Geopolitics, Oil and Market Pullbacks

April 2026

| | |

Pat McFawn | Financial Advisor - Registered Representative

Dale White | Financial Advisor - Registered Representative

Steve McFawn | Financial Advisor - Registered Representative

| | |

The first quarter of 2026 illustrates the importance of preparation when it comes to financial planning and investing. After strong gains in 2025, markets have faced a combination of geopolitical shocks, higher oil prices, and renewed economic uncertainty. The conflict in Iran, which began at the end of February, became the dominant market story, pushing oil prices sharply higher and sparking the first market pullback of the year. However, by the end of March, headlines around a possible ceasefire emerged, and the situation continues to evolve.

Taking a broader perspective, markets have still performed exceptionally well over the past twelve months. Beneath the surface, many parts of the market have supported portfolios, including energy and defensive sectors. There will undoubtedly be new market questions in the coming months, including a change in leadership at the Federal Reserve and the midterm election later this year.

For long-term investors, the first quarter is a reminder that markets rarely move in a straight line, and that the principles of sound investing matter most when uncertainty is at its peak.

Key Market and Economic Drivers

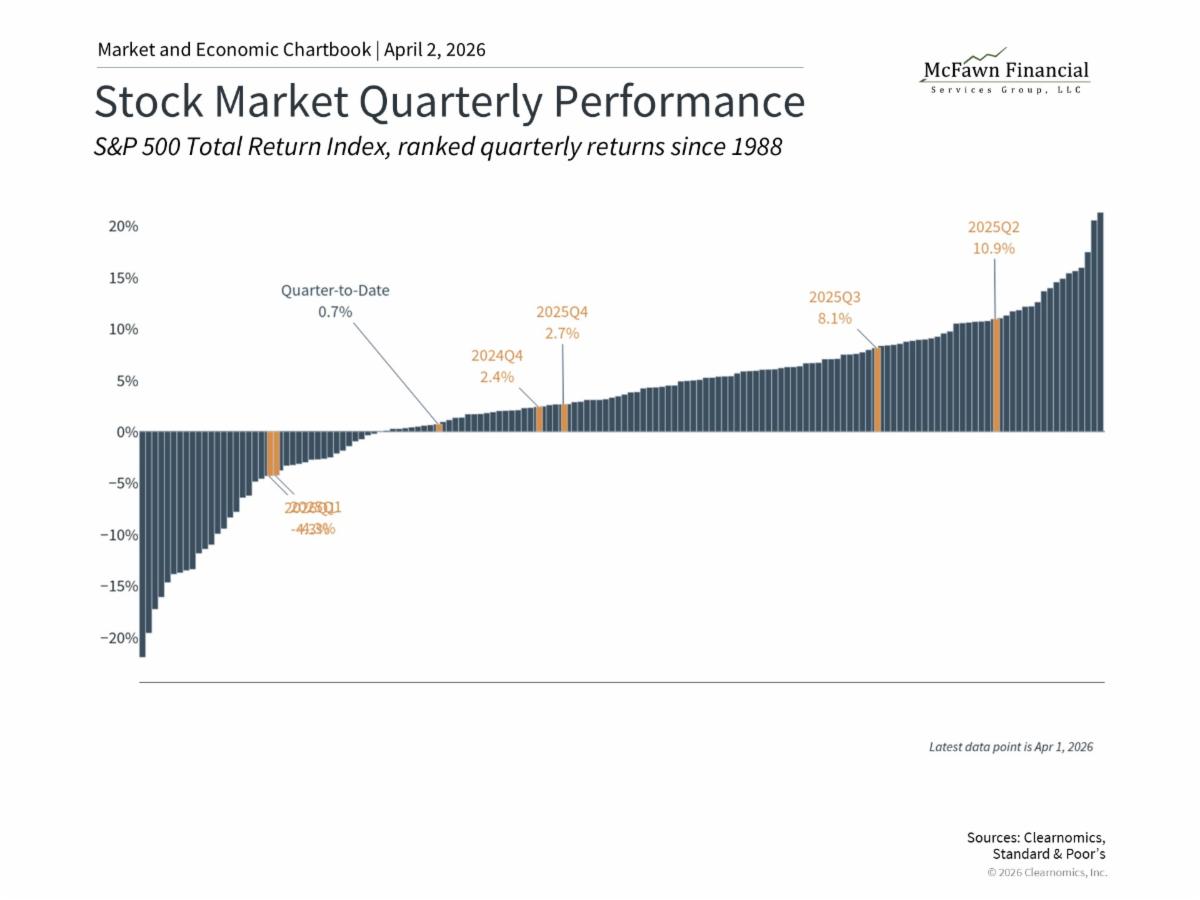

- The S&P 500 experienced a total return of -4.3% in Q1, the Nasdaq -7.0%, and the Dow Jones Industrial Average -3.2%.

- The Bloomberg U.S. Aggregate Bond Index was flat for the first quarter of 2026. The 10-year Treasury yield ended the quarter at 4.3% after falling as low as 3.9% at the end of February.

- Developed market international stocks (MSCI EAFE) were down -1.1% and emerging market stocks (MSCI EM) declined -0.1% over the quarter, both on a total return basis in U.S. dollar terms.

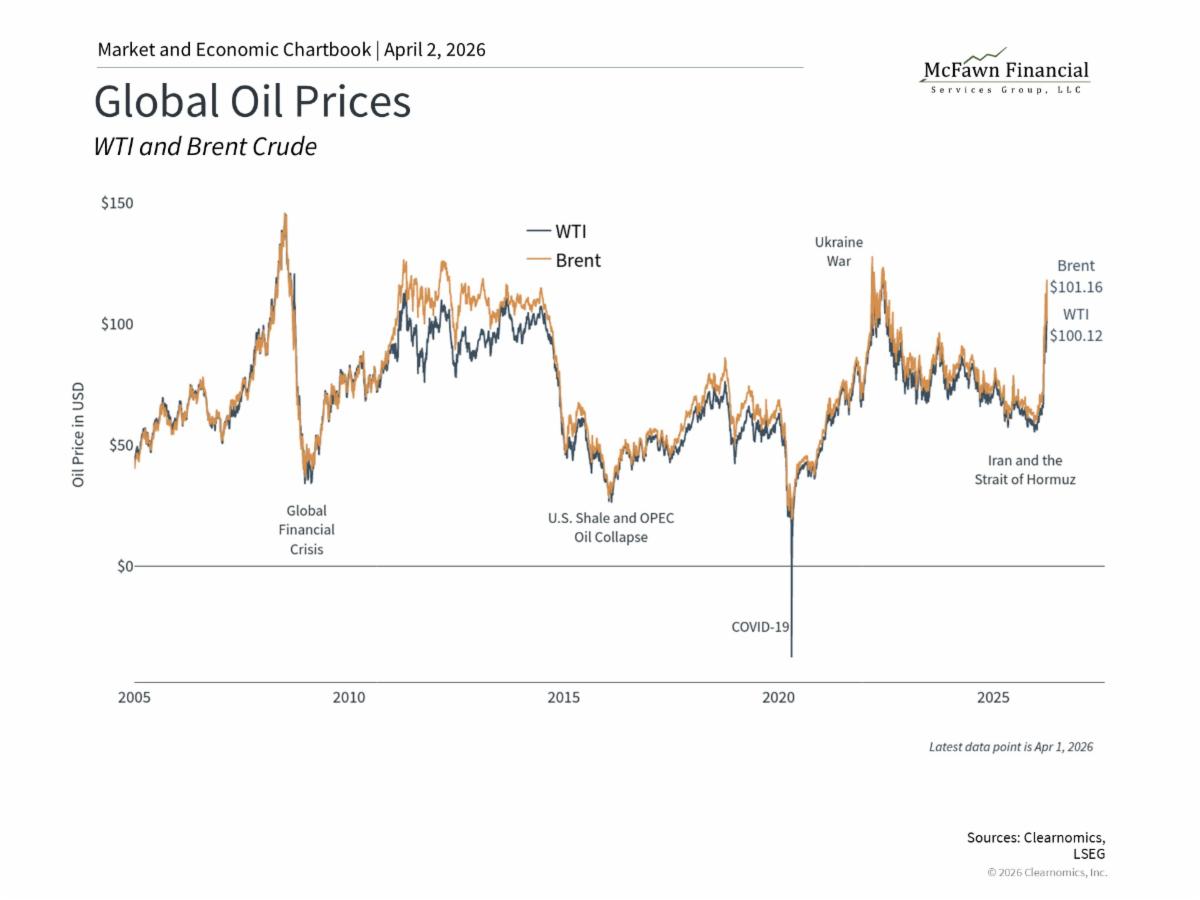

- Oil prices spiked with Brent crude reaching $118 per barrel at the end of March after beginning the year under $61. WTI ended the quarter at $101 per barrel.

- Gold ended the quarter at $4,668 per ounce after climbing as high as $5,417 in January. The U.S. Dollar Index (DXY) strengthened slightly to 99.96 over the same period.

- February inflation showed headline CPI rising 2.4% year-over-year and core CPI climbing 2.5%. The core PCE price index, the Fed's preferred measure, rose 3.1% year-over-year in January.

- The Federal Reserve kept rates unchanged within a range of 3.50% to 3.75% at both meetings during the first quarter.

Markets experienced the first pullback of the year

| | |

It’s natural to draw parallels between the start of this year and the beginning of 2025, since both were driven by global concerns. Coincidentally, both first quarter periods experienced pullbacks for the S&P 500 of 4.3%. While last year’s volatility was the result of tariffs and this year’s is due to the conflict in the Middle East, the effect on investor sentiment has been similar. When uncertainty rises, it’s natural for markets to experience short-term swings in response to headlines.

The past is no guarantee of the future, but zooming out can help us understand how markets have behaved historically. Despite the challenges in the first quarter of 2025, the stock market experienced strong gains through the remainder of the year, including dozens of record highs across major indices. The point is not that markets always recover quickly, but that market conversations tend to focus only on negative news. So, when rebounds do occur, they often do so when investors least expect them.

Perhaps the most helpful perspective is to remember that pullbacks are a normal and unavoidable part of investing. Since 1980, the S&P 500 has experienced an average intra-year drawdown of around 15%, even though markets tend to experience positive returns in more than two-thirds of years. It’s natural for the average year to experience four or five pullbacks of five percent or worse. Last year saw six such pullbacks, even though the S&P 500 finished the year with an 18% total return.

For investors, the key takeaway is that short-term market swings, especially those driven by headline risk, are simply part of the market cycle. Portfolios aligned with long-term financial goals are designed exactly to navigate these periods. This could be especially important as we approach the midterm election and fiscal concerns reemerge later in the year.

Geopolitics and oil prices are the primary source of uncertainty

| | |

The most significant market development of the first quarter was the escalating conflict in the Middle East, which drove oil prices higher. Disruptions to the Strait of Hormuz, which carries roughly 20% of global oil from the Persian Gulf to the rest of the world, led to production cuts across major oil-producing nations in the region. Brent crude ended the quarter at $118 per barrel, up over 94% year-to-date, while WTI crude surpassed $100, the highest levels since the war in Ukraine began in 2022. Oil will continue to react to geopolitical headlines, including around a possible ceasefire.

Higher fuel costs directly affect consumers through the price of gasoline at the pump and indirectly raise the prices of goods and services across the economy. The average price of gasoline across the country reached $4 at the end of March, and diesel prices have jumped significantly as well.

While these types of events do affect consumer pocketbooks, economists tend to view these types of “supply-side shocks” as temporary when considering the health of the overall economy. This is because oil prices tend to improve once the geopolitical event has stabilized. This was the case in 2022 when gas prices reached $5 before declining within months. While not pleasant, significant financial hardship is not expected to be an issue for the average American household at current gasoline levels.

History also shows that geopolitical events, while creating short-term instability, have not typically derailed markets in the long run. This includes the U.S. operation in Venezuela in January, which surprised markets but had little lasting impact on investments. While the current situation is still evolving and the humanitarian consequences are significant, investors who made dramatic portfolio adjustments in response to past events often did so at the wrong moment.

Economic growth is slowing but remains positive

| | |

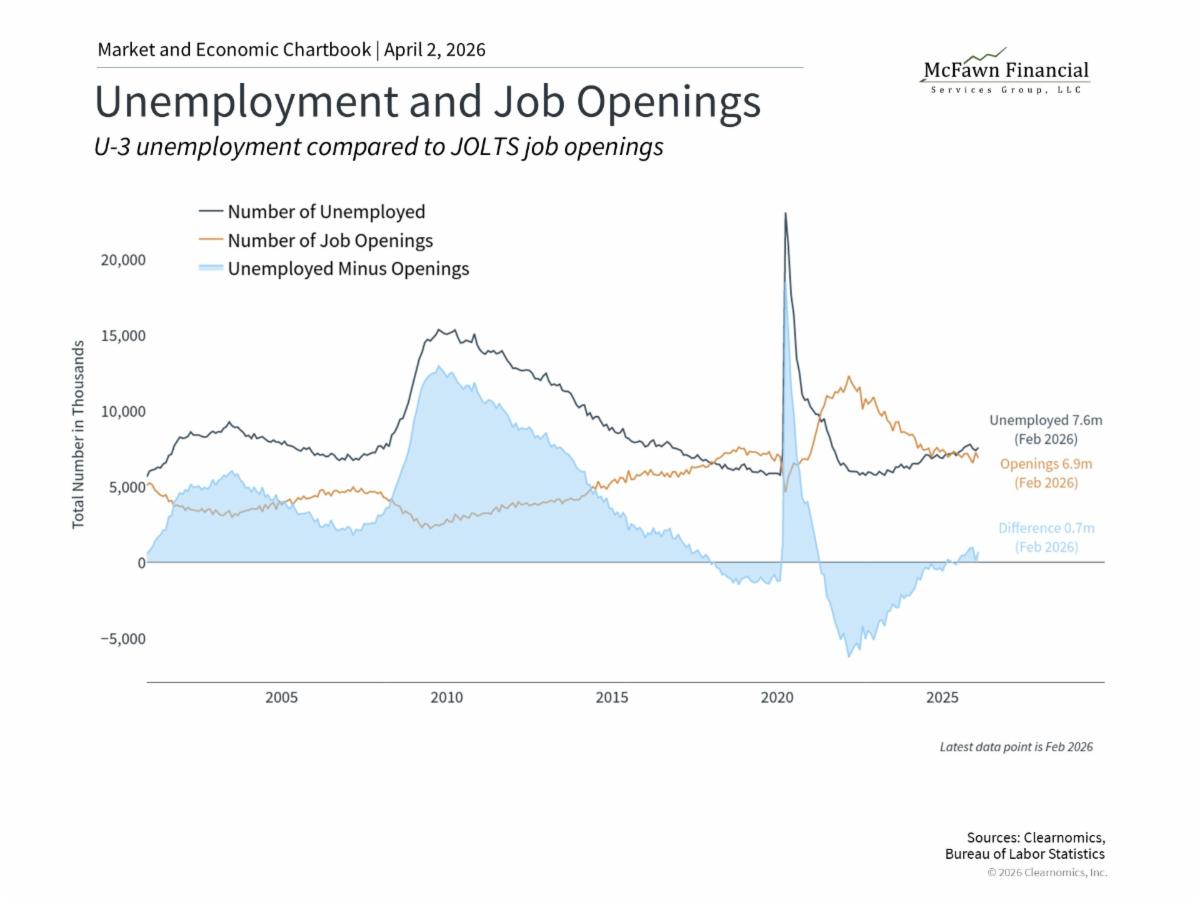

Volatile energy prices are just one piece of the broader economic puzzle. Other signs point to an economy that has cooled over the past year, but that is still fundamentally healthy. This is after many years during which investors and economists predicted recessions that did not materialize.

Perhaps the most closely watched area is the labor market, and the latest payrolls data show that February job gains fell by 92,000 and the unemployment rate edged up to 4.4%. Importantly, job seekers now outnumber job openings for the first time in years. As recently as 2022, there were two job openings for every unemployed individual, reflecting an exceptionally tight labor market. That relationship has now reversed.

However, the context around this matters. Fewer people are entering the workforce due to lower immigration and an aging population. In other words, both the supply and demand sides of the labor market are cooling, which has helped keep the unemployment rate near historically strong levels. Investors tend to watch jobs data closely because employment directly affects household income, consumer confidence, and spending. Consumer spending makes up more than two-thirds of GDP, and has been stronger than many expected over the past several quarters.

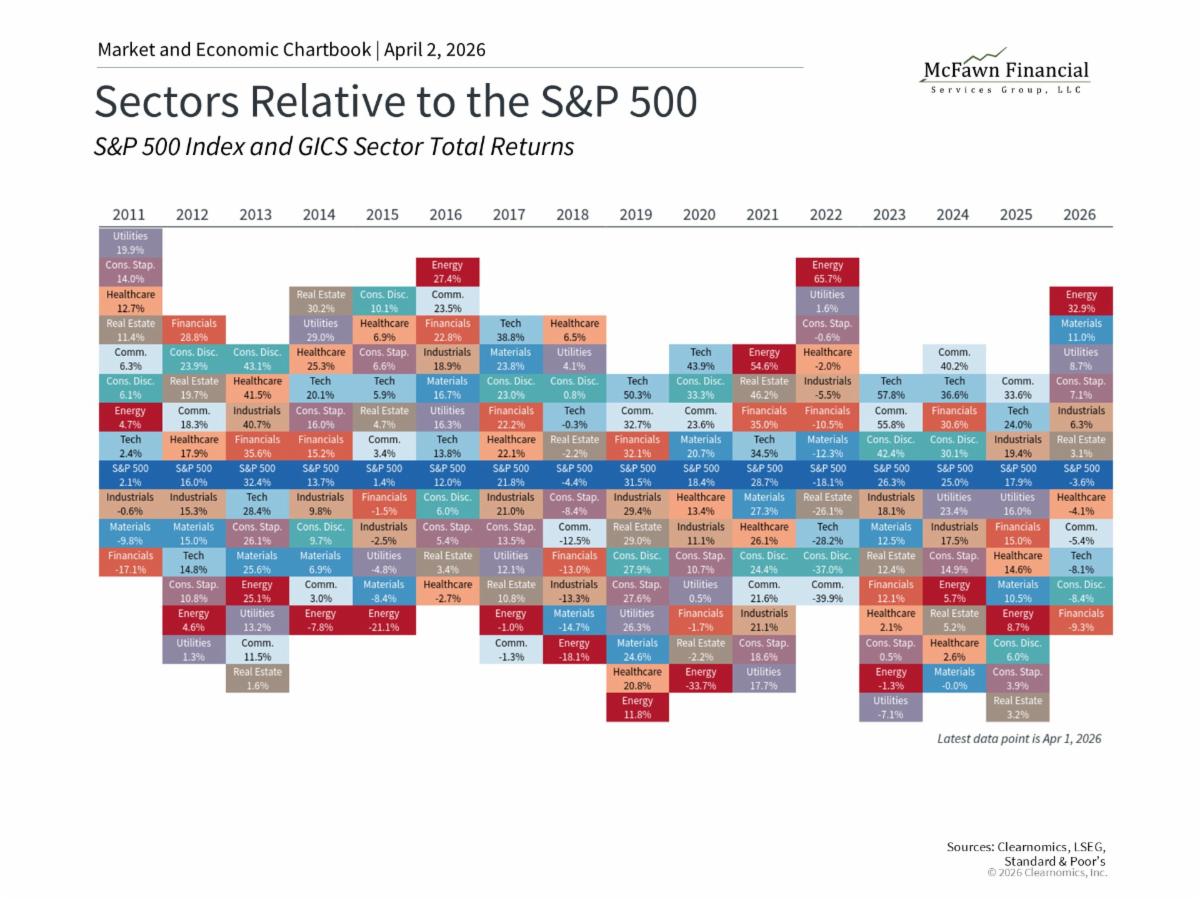

Sector performance has diverged

| | |

While the overall S&P 500 is experiencing a pullback, performance at the sector level has shown a wide degree of variation. In fact, six of the eleven S&P 500 sectors are positive for the year, and the difference between the best and worst performing sectors widened to nearly 50 percentage points in the first quarter.

The Energy sector has been the clear leader, gaining nearly 40% through the end of March, with higher oil prices expected to boost revenues and encourage further investment. Other sectors showing strength include Consumer Staples, Utilities, Materials, and Industrials, all of which have benefited from a more cautious market environment. Many of these sectors are often considered “defensive,” since they represent more stable businesses with steadier cash flows that are less dependent on the economic cycle.

In contrast, the Information Technology sector has declined approximately 9%, and many mega-cap stocks in the Magnificent 7 have underperformed. This is a shift from recent years when a small number of large technology companies drove the majority of market gains.

As always, it’s important to keep these moves in perspective. As the chart above shows, sector leadership can change based on market and economic conditions. Energy was the best performing sector in 2021 and 2022 when technology-related stocks struggled. This then reversed over the next three years. Just as with asset classes, it is extremely difficult to predict which sector will lead or lag in any given year, which is why a well-balanced portfolio is better positioned to weather different market environments.

The tariff story is evolving

| | |

Trade policy also took a turn at the end of January after the Supreme Court ruled 6-3 that the broad tariffs imposed under the International Emergency Economic Powers Act (IEEPA) were unlawful. The administration responded by imposing a temporary global import duty under a different law, Section 122 of the Trade Act of 1974. The administration also opened new Section 301 trade investigations in March, while about a dozen Section 232 investigations remain ongoing.

For investors, the main takeaway is that while the legal basis for tariffs has changed, the broader policy direction will continue. Tariffs will likely continue to impact the economy across consumer prices, business costs, and investor confidence. That said, last year showed that markets adapt to these types of policy changes over time. So, regardless of how the tariff story plays out later this year, the key is to stay invested and not overreact to policy moves.

The bottom line? The first quarter of 2026 challenges investors with geopolitical shocks, higher oil prices, and economic uncertainty. Yet markets have been resilient, with well-balanced portfolios and financial plans doing what they were designed to do. Investors should continue to focus on long run goals in the coming months.

| | The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. | | |

As always, if you have any questions, please do not hesitate to call us at (248) 619-0090.

This information, developed by an independent third party, Clearnomics, has been obtained from sources considered to be reliable, but Raymond James Financial Services, Inc. does not guarantee that the foregoing material is accurate or complete. This information is not a complete summary or statement of all available data necessary for making an investment decision and does not constitute a recommendation. The information contained in this report does not purport to be a complete description of the securities, markets, or developments referred to in this material. This information is not intended as a solicitation or an offer to buy or sell any security referred to herein. Investments mentioned may not be suitable for all investors. The material is general in nature. Past performance may not be indicative of future results. Raymond James Financial Services, Inc. does not provide advice on tax, legal or mortgage issues. These matters should be discussed with the appropriate professional. There is no guarantee that these statements, opinions or forecasts provided herein will prove to be correct. Investing involves risk and you may incur a profit or loss regardless of strategy selected, including diversification and asset allocation. Bond prices and yields are subject to change based upon market conditions and availability. If bonds are sold prior to maturity, you may receive more or less than your initial investment. Holding bonds to term allows redemption at par value. There is an inverse relationship between interest rate movements and bond prices. Generally, when interest rates rise, bond prices fall and when interest rates fall, bond prices generally rise. Prior to making an investment decision, please consult with your financial advisor about your individual situation. Raymond James is not affiliated with nor sponsors or endorses Clearnomics or any of the aforementioned organizations.

Leading Economic Indicators are selected economic statistics that have proven valuable as a group in estimating the direction and magnitude of economic change. The S&P 500 is an unmanaged index of 500 widely held stocks that is generally considered representative of the U.S. stock market. Inclusion of this index is for illustrative purposes only. Keep in mind that individuals cannot invest directly in any index, and index performance does not include transactions costs or other fees, which will affect actual investment performance.

The Bloomberg U.S. Aggregate Bond Index is a broad-based benchmark that measures the investment-grade, U.S. dollar-denominated, fixed-rate taxable bond market. The MSCI EAFE Index represents the performance of developed markets outside of the U.S. and Canada (Europe, Australasia, and the Far East). The MSCI Emerging Markets Index captures large and mid-cap representation across 24 Emerging Market (EM) countries. The U.S. Dollar Index measures the value of the U.S. dollar relative to a basket of foreign currencies. The Consumer Price Index (CPI) measures the average change over time in the prices paid by urban consumers for a basket of goods and services. It is one of the most widely used indicators for inflation.

| | |

Securities offered through Raymond James Financial Services, Inc. member FINRA/SIPC. Investment advisory services are offered through Raymond James Financial Services Advisors, Inc. McFawn Financial Services Group, LLC is not a registered broker/dealer and is independent of Raymond James Financial Services.

The Dow Jones Industrial Average (DJIA), commonly known as “The Dow” is an index representing 30 stock of companies maintained and reviewed by the editors of the Wall Street Journal.

The Russell 2000 Index measures the performance of the 2,000 smallest companies in the Russell 3000 Index, which represent approximately 8% of the total market capitalization of the Russell 3000 Index.

Bitcoin issuers are not registered with the SEC, and the bitcoin marketplace is currently unregulated. Bitcoin and other cryptocurrencies are a very speculative investment and involves a high degree of risk.

Investing in commodities is generally considered speculative because of the significant potential for investment loss. Their markets are likely to be volatile and there may be sharp price fluctuations even during periods when prices overall are rising.

Gold is subject to the special risks associated with investing in precious metals, including but not limited to: price may be subject to wide fluctuation; the market is relatively limited; the sources are concentrated in countries that have the potential for instability; and the market is unregulated.

Please visit https://www.raymondjames.com/legal-disclosures/social-media-disclaimer-icd for Additional Risk and Disclosure Information. Raymond James does not accept private client orders or account instructions by email. This email: (a) is not an official transaction confirmation or account statement; (b) is not an offer, solicitation, or recommendation to transact in any security; (c) is intended only for the addressee; and (d) may not be retransmitted to, or used by, any other party. This email may contain confidential or privileged information; please delete immediately if you are not the intended recipient. Raymond James monitors emails and may be required by law orregulation to disclose emails to third parties.

Investment products are: Not deposits. Not FDIC or NCUA insured. Not guaranteed by the financial institution. Subject to risk. May lose value.

This may constitute a commercial email message under the CAN-SPAM Act of 2003. If you do not wish to receive marketing or advertising related email messages from us, please reply to this message with "unsubscribe" in your response. You will continue to receive emails from us related to servicing your account(s).

| | | | |