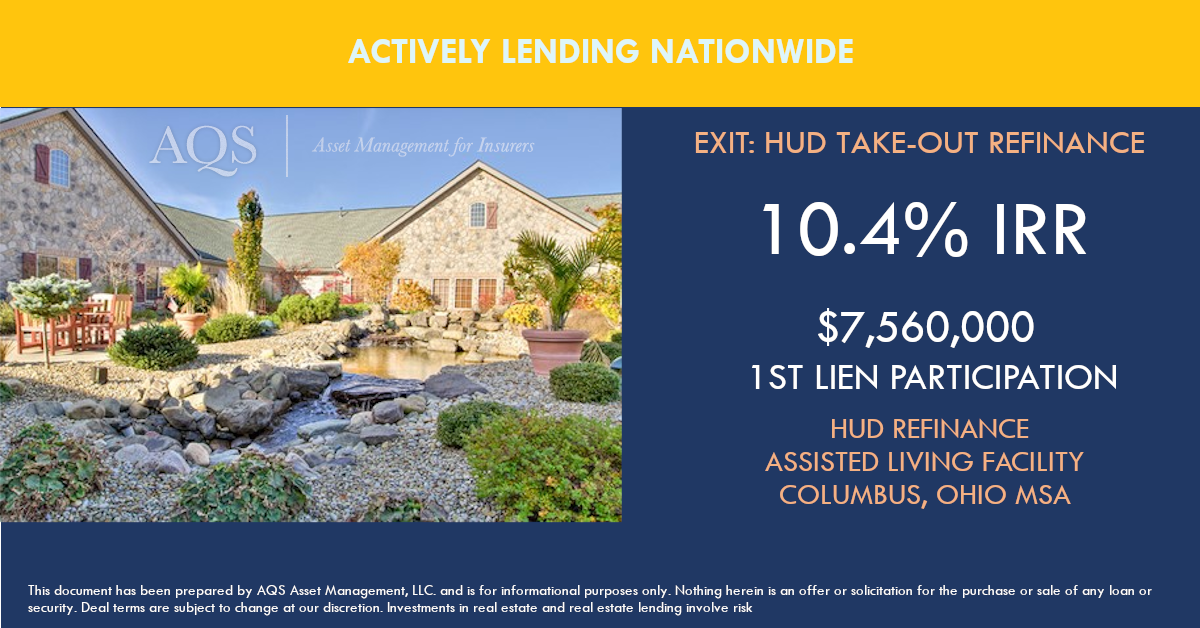

Commercial Lending - Also Where the Yield Is. Collateral too.

AQS has created a structure in which clients are super-senior, first lien and the sponsor/underwriter has 'skin in the game'. Insurance friendly, pledged collateral, great rates, short maturities. Avoid the CMBS 'mill'.

The following is just one of the loans in which AQS has successfully invested and exited.