|

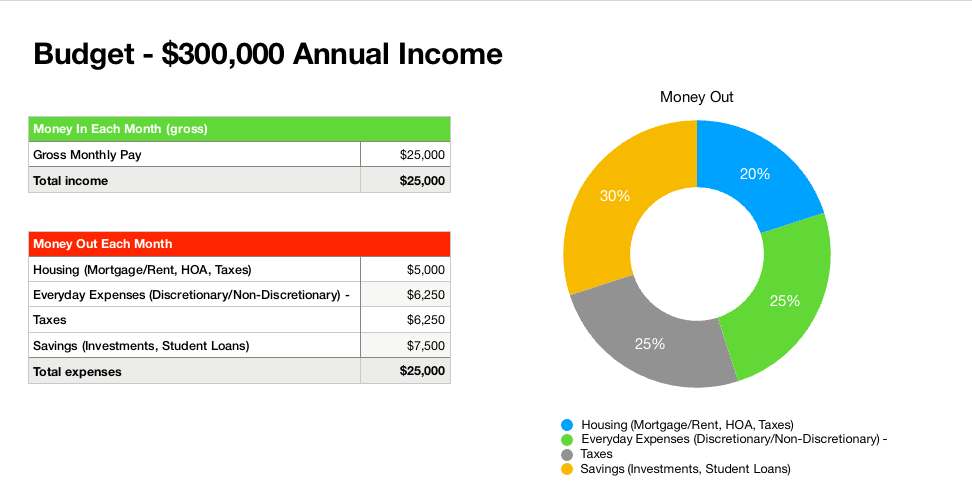

25% on Everyday Expenses: This includes groceries, utilities, transportation, and other day-to-day expenses.

20% on Housing: Rent or mortgage payments, property taxes, and insurance.

25% on Taxes: Federal, state, and local taxes.

30% on Saving for Your Future: This includes contributions to retirement accounts, emergency fund savings, and student loan debt payments.

Set Financial Goals & Systemize Your Savings

Establish both short-term and long-term financial goals. Short-term goals might include saving for a vacation or paying off a small debt, while long-term goals could involve saving for retirement or buying a home. The key is to "pay yourself first". Using the %'s above, take 30% of your gross pay and put it towards the savings goal (emergency savings, investments, student loans, etc). Utilize a separate savings account or brokerage account with a money market fund to keep these funds separate from the account you use for your everyday expenses. This ensures you are living day to day with what you have left (everyday expenses, taxes, mortgage/rent).

Prioritize Needs Over Wants

Differentiating between essential expenses (needs) and non-essential expenses (wants) is key to effective money management. When monitoring your monthly expenses, it's important to understand the difference between non-discretionary and discretionary spending:

Non-Discretionary Spending: These are essential expenses that are necessary for your basic needs and cannot be easily altered or eliminated. Examples include:

- Housing (rent or mortgage)

- Utilities (electricity, water, gas)

- Groceries and basic household supplies

- Transportation (fuel, public transit, car maintenance)

- Insurance (health, car, home)

- Taxes

Discretionary Spending: These are non-essential expenses that you have more control over and can adjust based on your financial goals and priorities. Examples include:

- Dining out and entertainment

- Hobbies and leisure activities

- Subscriptions and memberships (streaming services, gym memberships)

- Clothing and accessories

- Travel and vacations

As high-income earners, it's crucial to hold the reins back from going over your discretionary spending budget. While it's tempting to indulge in luxuries, maintaining a balance will help you achieve long-term financial stability. If you continuously exceed your discretionary allotment, you may inadvertently elevate your standard of living. This higher standard of living could lead to a greater income need in retirement, which may not be attainable.

It might be helpful to use software to monitor how much money is being spent on these four categories, as well as how much is being spent towards discretionary and non-discretionary spending. Many budgeting apps can provide detailed insights and help you stay on track. Budgeting apps we use/like are Simplifi by Quicken and YNAB. Monarch is a new comer that is has had real good reviews but we haven't tested it out yet.

Build an Emergency Fund

Life is unpredictable, and having an emergency fund can provide a financial safety net. Aim to save at least three to six months' worth of living expenses in a separate, easily accessible account. As your income grows this might change but a good starting point is usually $40,000. A high yield savings account is an effective tool as the average savings rate is 0.61% vs a high yield account that averages between 3.5% - 4.75%

Review and Adjust Regularly

What you can save now vs different points in the future will vary. You might have a young family or have recently started a practice. Don't get down on yourself as this is a snapshot in time and your savings rate reflect this. A financial plan will ensure you have the confidence that the decisions you are making now don't have a detrimental impact on your financial future.

|