|

Win $50!

|

|

There are two member numbers spelled out within the text of this eNewsletter. Find your number and give us a call at (888) 387-8632 to claim $50!

|

|

|

|

|

Jen learns about good and bad spending habits.

|

1: APR = Annual Percentage Rate. Loan amount and terms subject to approval; your rate may be different depending on loan amount, term, credit score and other factors. Your rate will be disclosed prior to funding. Daily periodic rate for 7.9% APR is .02165. Minimum payment on a 1st Line of credit with a limit up to $2,000.00 is $50.00 per month. Maximum limit is $20,000.00 with a minimum payment of $475.00. Rates are subject to change.

|

President's Corner

|

Albert H. Wiggin did what very few people did - he made millions of dollars during the 1929 stock market crash and subsequent Great Depression. Mr. Wiggin, then head of Chase National Bank, shorted 40,000 shares of his own company stock and made $4 million in the process for the transaction which was a huge number back then. By shorting stock, Mr. Wiggin bet on Chase Bank to lose but won lots of dough while much of the world lost their life savings, and in some cases their lives.

This sort of insider trading was legal in 1929 but made illegal in 1934 when Congress revised the Securities Act, the revision famously referred to as the "Wiggin Act." The Securities Act slowed down but did not eliminate insider trading, which made stock traders Ivan Boesky, Michael Milken, Dennis Levine, and Martin Siegel infamous. The first celebrity to get caught with their hand in the stock market cookie jar was Martha Stewart, who sold shares in a pharmaceutical company based on insider knowledge just before the stock price dropped. Ms. Stewart baked cookies in a federal prison for five months, and her reputation was never fully repaired.

We are currently in the midst of probably the most bizarre insider trading case in our nation's history. This individual is neither a banker, stock trader, politician, nor TV celebrity. He does have a number - 56 - his uniform number with the Seattle Seahawks NFL football team. Mychal Kendricks, a linebacker by trade, has admitted to receiving non-public information regarding certain technology stocks from a Goldman Sachs employee in exchange for cash and game tickets when he played for the Philadelphia Eagles in 2014-15. Mr. Kendricks purchased call options contracts hoping the stock prices would rise and sold them at a $1.2 million gain which translates to returns ranging from 79% to 393%, not a bad day's work but also not a realistic return for an amateur investor unless they knew something.

Mr. Kendricks and the Goldman Sachs employee even used football terminology to code text messages between them. Based on the civil complaint filed by the Securities and Exchange Commission, Mr. Kendricks seemed preoccupied with getting capital gains tax breaks. At this point, Mr. Kendricks is claiming he was duped by his friend, who represented himself to be a Harvard graduate, who gave "a false sense of confidence."

Mr. Kendricks has pleaded guilty and is awaiting sentencing, which is due coincidentally after the football season. According to several sources, he is looking at a prison sentence of up to 25 years and a fine of $5.3 million, which dwarfs his 2018 salary of $790,000. Whether he has a 2019 salary will depend on the U.S. Department of Justice attorney prosecuting the case, the federal judge, and of course the NFL which must address this no-win situation. They appear to have policies dealing with domestic violence and drug use, but probably nobody inside 345 Park Avenue in Midtown Manhattan ever thought they would be dealing with a player convicted of insider trading. The only previous experience they had in white collar crime was suspending Paul Hornung and Alex Karras for the 1963 season for betting on football games and associating with gamblers.

Insider trading poses a threat to financial markets because it compromises the public's trust in those markets. If investors cannot trade on a level playing field, everyone loses - the buyers, sellers, and customers and employees of publicly-held companies. The strange financial saga of Seattle Seahawk Mychal Kendricks highlights one of life's truism: If it sounds too good to be true, it probably is.

David M. Green

President/CEO

(925) 335-3802

|

Stat of the Month

|

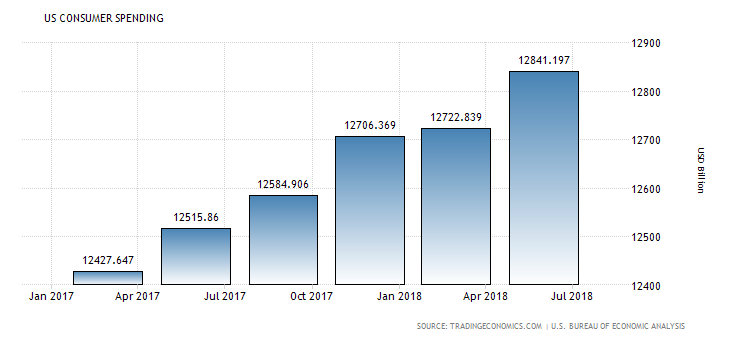

U.S. CONSUMER SPENDING AND PERSONAL SAVINGS RATE

JANUARY 2017 - JULY 2018

As housing costs and healthcare continue to take a larger slice of most consumers' budgets, it follows that consumer spending on more discretionary items would decline. However, this spending has been rising as shown in the chart above. Consumer spending has become a significant factor in continued economic improvement.

While consumers have not realized real wage gains for a number of years, they are definitely feeling more confident about maintaining their employment. Therefore, the conjecture is that consumers are spending from their savings and, at least for the last several months, the savings rate chart above seems to bear this out.

(SEVEN TWO TWO SEVEN THREE)

|

|

|

New Branch Now Open!

We are pleased to announce that

we have opened a new branch in the

Pittsburg Century Plaza next to Target

4261 Century Blvd., Pittsburg, CA 94565

We have closed our branch at 1870 A Street in Antioch.

Click

here for other convenient branch and

surcharge-free ATM locations near you.

If you have any questions, please contact us at 925-293-1785.

|

1st Alerts

|

- If you have @ccessOnline Home Banking with us, you can transfer a payment to your Visa card. Setting up a regular payment using Bill Pay in @ccessOnline Home Banking will generate a check and that will delay your payment. Instead, you can set up a single or recurring transfer. A transfer is immediate.

|

1st in the Community

|

Backpack Drive

Kaleo Mendoza, a little guy with a BIG heart! First, we'd like to thank everyone who helped make our 2018 Backpack Drive a huge success - we delivered 15 backpacks full of supplies to Operation Backpack and the Benicia Family Resource Center. But super-duper, big-time special thanks goes out to Kaleo Mendoza - this story really made an impression with our staff. Check this out... Kaleo visited our Muir Station branch with his dad and used the coin machine to process all the cha

nge he'd collected from around the house. This was Kaleo's money - he'd earned it for sure. Come to find out, while at the branch, Kaleo heard about our Backpack Drive and upon leaving the branch he told his dad that he wanted to spend his money on backpacks and supplies for less fortunate kids. AND THAT'S EXACTLY WHAT HE DID! What a cool kid - so proud to know there's sweet kids in our community willing to help others. Thanks Kaleo!

|

*APY = Annual Percentage Yield. Rates as of 10/1/18 and are subject to change. Fees or other conditions could reduce the earnings on the account. A penalty may be imposed for withdrawals before maturity. See Cost Recovery Fee Schedule for more details.

|

Ten Tax-Smart Strategies to Consider in 2018 & Beyond

By Jason Vitucci, CFP® & Gene A. Schnabel

- Invest in municipal bonds to generate tax-free income

Even with reduced tax rates, municipal bonds may still be attractive on a relative tax basis for higher-income taxpayers, especially those who find themselves subject to the 3.8% surtax on net investment income. The tax equivalent yield, i.e., the yield an investor would require in a taxable bond investment to equal the yield of a comparable tax-free municipal bond, is higher for those taxpayers.

- Utilize strategies to reduce or avoid taxable income Contributing to a retirement plan or IRA, funding a flexible spending account (FSA), or deferring compensation income can reduce adjusted gross income (AGI) and prevent a taxpayer from reaching key income thresholds that may result in a higher tax bill. Conversely, be mindful of transactions, such as the sale of a highly appreciated asset, which may increase your overall income above thresholds for the 3.8% surtax, impact taxability of Social Security benefits, or result in higher Medicare premiums.

- Consider Roth IRA/401(k) contributions or conversions

A thoughtful strategy utilizing Roth accounts can be an effective way to hedge against the threat of facing higher taxes in the future. Younger investors or taxpayers in lower tax brackets should consider using Roth accounts to create a source of tax-free income in retirement. It is virtually impossible to predict tax rates in the future or to have a good idea of what your personal tax circumstances will look like years from now. Like all income from retirement accounts, Roth income is not subject to the new 3.8% surtax and is also not included in the calculation for the $200,000 income threshold ($250,000 for couples) to determine if the surtax applies. IRA owners considering a conversion to a Roth IRA should carefully evaluate that transaction since the option to recharacterize, or un-do, a Roth IRA conversion is no longer available.

- Maximize deductions in years when itemizing

With the large increase in the standard deduction and the scaleback of many popular deductions, fewer taxpayers will choose to itemize on their tax return going forward. Some taxpayers may benefit by alternating between claiming the standard deduction some years and itemizing deductions other years. If possible, it would make sense to "lump" as many deductions into those years when itemizing. For example, taxpayers may want to consider making a substantial charitable contribution during a tax year when itemizing instead of making regular, annual gifts. In addition, with the repeal of the "Pease rule," there are no phaseouts on itemized deductions at higher income levels.

- Be mindful of irrevocable trusts and taxes

Because of the low-income threshold ($12,500 for 2018), which will subject income retained within an irrevocable trust to the highest marginal tax rates and the 3.8% Medicare surtax, trustees may want to reconsider investment choices inside of the trust (municipal bonds, life insurance, etc.). Or, maybe trustees should consider (if possible) distributing more income out of the trust to beneficiaries who may be in lower income tax brackets.

- Review estate planning documents and strategies

The increase in the lifetime exclusion amount for gifts and estates (projected at $11.2 million per individual in 2018) may have unintended consequences for some individuals and families with wealth under that threshold. They may think that they do not have to plan for their estate. However, taxes are just one facet of estate planning. It is still critical to plan for an orderly transfer of assets or for unforeseen circumstances such as incapacitation. Strategies to consider include proper beneficiary designations on retirement accounts and insurance contracts, wills, powers of attorney, healthcare directives, and revocable trusts.

- Plan for potential state estate taxes

While much attention is focused on the federal estate tax, certain residents need to know that many states have estate or inheritance taxes. There are a number of states that are "decoupled" from the federal estate tax system. This means the state applies different tax rates or exemption amounts. A taxpayer may have net worth comfortably below the $11,200,000 exemption amount for federal estate taxes, but may be well above the exemption amount for his or her particular state. It is important to consult with an attorney on specific state law and potential options to mitigate state estate or inheritance taxes.

- Develop a strategy for low cost-basis assets

Ensure stepped-up cost basis is maintained when property is transferred at death. For example, careful consideration should be made around lifetime gifts that may jeopardize a step-up in cost basis on property at death. When property is gifted, the party receiving the gift generally assumes the original cost basis. Additionally, certain trust provisions may be utilized to ensure that property receives a step-up in cost basis at death.

- Expand use of 529 accounts for education savings

529 colleges savings plans retain existing tax advantages. Account earnings are free of federal income tax, and a special gift tax exclusion allows you to make five years' worth of gifts to a single beneficiary in one year without triggering the federal gift tax. Qualified education expenses were expanded in recent years to include laptops, computers and related technology. The new tax law allows families to use up to $10,000 annually for K-12 tuition.

- Consider the charitable rollover option if you are a retiree

Retired IRA owners (age 70.5 and older) may benefit from directing charitable gifts tax free from their IRA. Since even more retirees will claim the higher standard deduction, they will not benefit tax-wise from making those charitable gifts unless they itemize deductions. Account owners are limited to donating $100,000 annually, which can include the required minimum distribution (RMD), and the proceeds must be sent directly to qualified charity.

To learn more about how the financial planning process, with tax planning included, can help you define and implement your saving goals, contact our office today. We help our clients navigate through the confusing maze of financial issues as it relates to retirement planning. If you feel that we may be a good fit to work together, please don't hesitate to contact our office. As a valued 1st Nor Cal member, we invite you to contact us for a complimentary financial analysis. We also invite you to attend any of our Retirement Planning workshops that we hold. For more information about our practice, or to make an appointment, please call us at (925) 370-3750 or visit our website at www.vitucciintegratedplanning.com.

Vitucci Integrated Planning

Securities through First Allied Securities, a registered broker dealer, member FINRA/SIPC. Advisory services offered through First Allied Advisory Services, Inc. Registered Investment Advisor. Investments not FDIC or NCUA/NCUSIF insured, not insured by Credit Union, may lose value. Products offered are not guarantees or obligations of the Credit Union, and may involve investment risk including possible loss of principal.

1st Nor Cal CU, Bay Area Retirement Solutions and First Allied are all separate entities.

Jason Vitucci CA

Insurance Lic.: 0F59894, Gene A. Schnabel CA Insurance Lic.: 0663016

Consult a qualified tax or legal professional and your financial advisor to discuss these types of strategies to prepare for the risk of higher taxes in the future. Personal circumstances vary widely so it is critical to work with a professional who has knowledge of your specific goals and situation.

|

Insurance Tips

|

What You Should Know About Flood Insurance

As you may know, your Homeowners Insurance does not cover flood damage. According to NFIP, nearly 25% of their claims occur in moderate to low risk areas. The good news is that there are now two options for Flood insurance. They are as follows:

NFIP (National Flood Insurance Program)

- This is a national program is backed by FEMA.

- The cost is based on government mapping of zones and their likelihood to flood.

- If you are in a "higher" frequency flood zone, you are required to obtain an Elevation Certificate. These certificates can be quite expensive.

- Unless coverage is being required by a lender at the close of escrow, there is a mandatory 30 day waiting period.

- Maximum amount of coverage available is $250,000 on the Building and $100,000 on Contents. Loss of Use is NOT available.

- Requires annual payment in full.

Private Flood Insurance

- Not backed by FEMA - but you are protected by the California Insurance Guarantee Association as long as the carrier is licensed to do business in the state of California.

- Rates are based at the location level, which means lower rates in many instances.

- No Elevation Certificate.

- No 30 day waiting period.

- Coverage limits in excess of $1M available. Optional Loss of Use up to $50,000.

- Payment options available.

If you don't currently have Flood insurance, now is a great time to think about it. If you do have Flood Insurance, but it is currently thru the NFIP, I would encourage you to call us for a No-Obligation quote!

As an added benefit of your 1st Nor Cal membership, we at Lou Aggetta Insurance will help you review the things that are important to you and provide you with options for reducing risk in your life. We are an independent insurance agent and can provide you with home, auto, umbrella, earthquake, flood, business, and many other types of insurance coverage.

Contact us today to schedule your free review.

Denia Aggetta Shields

Lou Aggetta Insurance, Inc.

2637 Pleasant Hill Road

Pleasant Hill, CA 94523

(925) 945-6161

|

FREE Financial Counseling

|

Are you in need of financial counseling?

1st Nor Cal is here to help. Timely and honest debt advice is available to our members at no cost or obligation. Learn how to manage your finances.

Make your appointment TODAY!

Just a reminder, you can annually request FREE Credit Reports from all 3 credit reporting agencies online by going to:

For FREE Financial Counseling, don't hesitate to contact:

Shelley Murphy

Senior Vice President of Lending & Collections

(925) 228-7550 Ext.824

(TWO ZERO ZERO SEVEN FOUR)

|

Did you know we're on Social Media?

|

|

|