Weekly update from the National Housing Conference | | News from Washington | By Brittany Webb | | |

White House backs housing inclusion in NDAA

The White House is reportedly lending support to including the Senate passed ROAD to Housing Act into the must-pass annual National Defense Authorization Act (NDAA), which cleared the Senate Banking Committee unanimously earlier this year. This would be a major win for housing policy if enacted. Negotiations on the inclusion remain fluid, with some House conservatives having previously opposed including housing provisions in the bill.

The move follows recent action in the House on a related package. The provisions are aimed at expanding housing supply and lowering costs. Supporters see the defense bill as one of the few viable vehicles remaining this year for major legislative action. Housing policy has become an increasing focus for the Trump administration as it continues to grapple with affordability challenges throughout the country.

“Families across the country are being crushed by soaring housing costs, and Washington cannot continue to sit on the sidelines. The White House has made it clear that affordability is a central priority, and the ROAD to Housing Act is one of the most effective first steps to increase housing access, expand supply, and lower costs,” said Senate Banking Committee Chairman Tim Scott (R-S.C.). “ROAD provides the largest housing reform package in more than a decade – cutting red tape, unlocking supply, and helping families achieve the stability and opportunity that come with homeownership. As congressional leaders finalize the NDAA, now is the time to deliver real affordability reinforcements for the American people. This is a bipartisan, common-sense package that deserves to cross the finish line,” Scott said.

| NHC President David Dworkin and Senator Elizabeth Warren (D-Mass.) | |

House committee examines government barriers to housing

The House Committee on Financial Services held a hearing titled “Building Capacity: Reducing Government Roadblocks to Housing Supply,” bringing forward bipartisan concern over the deepening national shortage of affordable homes. Lawmakers and housing experts pointed to a mix of restrictive zoning practices, regulatory burdens, inflation, and weakened federal fair housing protections as key contributors to America’s worsening affordability crisis for renters and homebuyers.

Committee Chairman French Hill (R-Ark.) opened the hearing with a stark assessment of the housing landscape, emphasizing that the supply shortage has pushed homeownership out of reach for millions. “Housing affordability has rapidly become one of the main issues facing our American families, which have been primarily driven by a persistent lack of supply needed to meet a growing demand,” Hill said. “Rather than helping development, overburdensome building regulations have made it nearly impossible for many housing providers to navigate a maze of federal, state, and local rules, leading to less housing development across the nation

Ranking Member Maxine Waters (D-Calif.) warned that working families are being squeezed harder each year. “The cost of living is skyrocketing, and working-class families are struggling to pay their rent and mortgages,” Waters said, urging Congress to adopt stronger federal interventions to address homelessness and affordability. She stressed the need for substantial investment, adding, “We must move quickly because while Congress bickers, rents are still going up, home prices are still rising, and mortgage rates are still too high.”

Witnesses echoed lawmakers’ concerns about regulatory burdens and economic pressures that inhibit new construction. Julie Smith, Chief Administrative Officer of the Bozzuto Group, testifying on behalf of the National Multifamily Housing Council (NMHC), the National Apartment Association (NAA), and the Real Estate Technology and Transformation Center, warned that building has become increasingly difficult under current economic conditions. “Regrettably, the current economic and regulatory environment makes building incredibly difficult, and that is unlikely to change without action that makes production more economically viable,” Smith told the committee, noting that regulations alone account for more than 40 percent of multifamily development costs.

Nikitra Bailey, Executive Vice President of the National Fair Housing Alliance, described how current federal actions have weakened critical fair housing protections. “Our nation is in the throes of a fair and affordable housing crisis, and it's impacting millions of people,” Bailey said. “Instead of providing everyday people with practical solutions to the housing crisis, the [administration] is removing rungs on the ladder of opportunity for essential workers.” She urged Congress to restore strong fair housing enforcement and pursue comprehensive reforms to ensure that vulnerable communities are not left behind.

Kevin Sears, Immediate Past President of the National Association of REALTORS® and Tobias Peter, Senior Fellow and Codirector of the American Enterprise Institute Housing Center, stressed that years of underbuilding, restrictive zoning, high construction costs, and complex permitting systems have erased affordability and limited the nation’s ability to produce homes at the scale needed. The Committee is expected to consider a package of housing and banking reforms later this month.

| Congressman Emanuel Cleaver II (D-Mo.) | |

Lawmakers press bank regulators on risk and independence

Prudential bank regulators appeared before the House Financial Services Committee in a wide-ranging oversight hearing as lawmakers examined how supervisors are tailoring rules, responding to market risks, and navigating mounting political pressures. The hearing featured testimony from Federal Reserve Vice Chair for Supervision Michelle Bowman, Comptroller of the Currency Jonathan Gould, National Credit Union Administration Chairman Kyle Hauptman, and Acting Federal Deposit Insurance Corporation (FDIC) Chairman Travis Hill.

Committee Chairman French Hill (R-Ark.) framed the hearing as a chance to realign regulation with the needs of lenders and their customers. “Today's hearing is an opportunity for the committee to discuss the recent work of our prudential regulators and to highlight the strong alignment between their current approach under the Trump Administration and our agenda here in the committee to make community banks, all depository institutions of all sizes, great again,” he said. Hill added that the hearing is “about enhancing clear tailored rules of the road, fostering competition and ultimately serving the best interests of consumers and businesses.”

Committee members pressed regulators on issues ranging from digital assets and “debanking” allegations to deposit insurance reforms and the impact of rising interest-bearing stablecoins. At the center of many exchanges were concerns about how regulators are managing systemic risks while adapting outdated frameworks to a changing financial landscape.

Federal Reserve Vice Chair for Supervision Michelle Bowman emphasized the dual mandate of safety and growth in the financial system. “Our supervision and regulation must support a safe and sound banking system that fosters economic growth while also safeguarding financial stability,” she said, noting ongoing efforts to tailor oversight to different types and sizes of institutions and to update outdated regulatory thresholds. “We cannot continue to push policies designed for the largest banks down to the smaller, less risky and less complex banks.”

Bowman also addressed the Fed’s forthcoming Basel III endgame proposal. She signaled that regulators are not committing to a “capital neutral” result and are instead conducting a risk-based review. Bowman stressed that any final approach must avoid unnecessarily impairing mortgage lending, market liquidity, or the broader economy, aligning with her written statement that finalizing Basel III should “reduce uncertainty and provide clarity on capital requirements.”

Acting FDIC Chairman Travis Hill highlighted a shift in focus toward core financial risks and a more transparent regulatory framework. “Over the past ten months, the FDIC has made significant progress in several areas including reforming supervision so it is less process driven and more focused on core financial risks,” he said.

However, Democrats questioned whether regulators could maintain independence under mounting political pressure, raising concerns about the independence of federal banking regulators and urging regulators to assert their independence and restore confidence in the oversight framework.

|

| | |

FHFA announces loan limits and multifamily caps

The Federal Housing Finance Agency (FHFA) announced that the 2026 multifamily loan purchase caps for Fannie Mae and Freddie Mac will be set at $88 billion each, for a combined total of $176 billion to support the multifamily market. At least half of each Enterprise’s multifamily business must be mission-driven affordable housing. Similar to last year, loans that finance workforce housing will be excluded from the 2026 caps while all other mission-driven loans remain subject to the limits. FHFA said it will continue to monitor conditions in the multifamily mortgage market and raise the caps if needed, but it will not lower them even if the market ultimately proves smaller than expected.

"[FHFA’s] 2026 multifamily loan purchase cap will enable us to continue this important work, ensuring people have access to quality, affordable places to live in communities throughout the country. We look forward to partnering closely with our lenders and other stakeholders in the year ahead to deliver housing opportunities where they are needed most,” said Kelly Follain, Executive Vice President and Head of Multifamily at Fannie Mae.

“Freddie Mac Multifamily delivers essential liquidity to create affordable apartment supply around the country each and every year,” said Kevin Palmer, Head of Multifamily for Freddie Mac. “In 2026, we will continue to provide that needed liquidity with our full suite of offerings and continued innovation.”

FHFA also announced the 2026 conforming loan limit (CLL) values for mortgages the Enterprises will acquire next year. In most of the United States, the 2026 CLL for one-unit properties will be $832,750, reflecting a 3.26% increase tied to the change in the average U.S. home price as measured by FHFA’s House Price Index. FHFA noted that due to rising home values, CLL values will be higher in all but 32 U.S. counties or county equivalents. The new ceiling loan limit for one-unit properties in high-cost areas will be $1,249,125, with special statutory provisions setting the baseline and ceiling in certain markets at $1,873,675.

The Housing Policy Council responded to the new loan limits in a press release stating, “As we have stated each of the past four years, and reiterate now, the continued increase in loan limits contributes to house price inflation. Furthermore, loan limits that increase faster than incomes displace mortgages that can and should be produced as purely private market transactions with mortgages backed directly or indirectly by taxpayers.”

| | | |

|

Housing groups sue over CoC changes

A coalition of local governments and nonprofit service providers is formally challenging the planned changes to the Department of Housing and Urban Development’s (HUD) Continuum of Care (CoC) program, arguing the changes are unlawful and jeopardize proven strategies for reducing homelessness. The coalition, including the National Alliance to End Homelessness (NAEH), the National Low Income Housing Coalition, Crossroads Rhode Island, Youth Pride, Inc., as well as several cities and counties, filed suit against HUD’s new rules, arguing that the changes would severely limit the types of interventions communities can fund. The groups assert that the administration’s shift would upend years of established federal policy and undermine programs with strong evidence of success.

NAEH stated in its announcement that the new restrictions threaten “proven solutions to homelessness,” emphasizing that the rules could cut off funding for programs that connect people to housing without preconditions. The coalition, made up of cities, counties, Continuums of Care, and nonprofit organizations that collectively serve thousands of people experiencing homelessness, argues that the new requirements overstep the administration’s legal authority, disregard evidence-based practices, and would force communities to divert resources away from interventions that have demonstrated effectiveness.

The coalition is asking HUD to reverse the restrictions and restore flexibility for local systems to choose approaches backed by research and tailored to community needs. Service providers warn that if the rules stand, they will disrupt ongoing efforts to reduce homelessness and place vulnerable households at greater risk.

| |

CFPB requires new “humility pledge”

The Consumer Financial Protection Bureau (CFPB) announced that all members of its Supervision, Enforcement, and Fair Lending Division will now begin examinations by reading a new “humility pledge.” CFPB Director Russell Vought said the pledge formalizes expectations for examiners and reflects the agency’s responsibility to conduct its oversight duties in a manner that is respectful, prompt, professional, and under budget, without asking “invasive and irrelevant questions” or “demanding expansive information that they do not need.”

The pledge will be read aloud at the start of every examination and will be accompanied by assurances from CFPB staff that the exam process will be collaborative. While CFPB leadership framed the initiative as a step toward rebuilding trust with regulated entities, questions remain among some observers regarding whether the change signals a shift in supervisory posture or is primarily symbolic.

“In sum, the Bureau’s goal is to work collaboratively with the entities to review entities’ processes for compliance and/or remedy existing problems. The Bureau is doing so by encouraging self-reporting and resolving issues in Supervision, where feasible, instead of via Enforcement,” the pledge reads.

The Bureau has not announced any additional adjustments to its exam protocols beyond the introduction of the pledge, but stated that it will continue reviewing its supervision program. Examinations remain halted as CFPB employees have been told to close out all open matters.

|

| | |

Community Solutions publishes impact assessment of FY 2025 HUD CoC NOFO

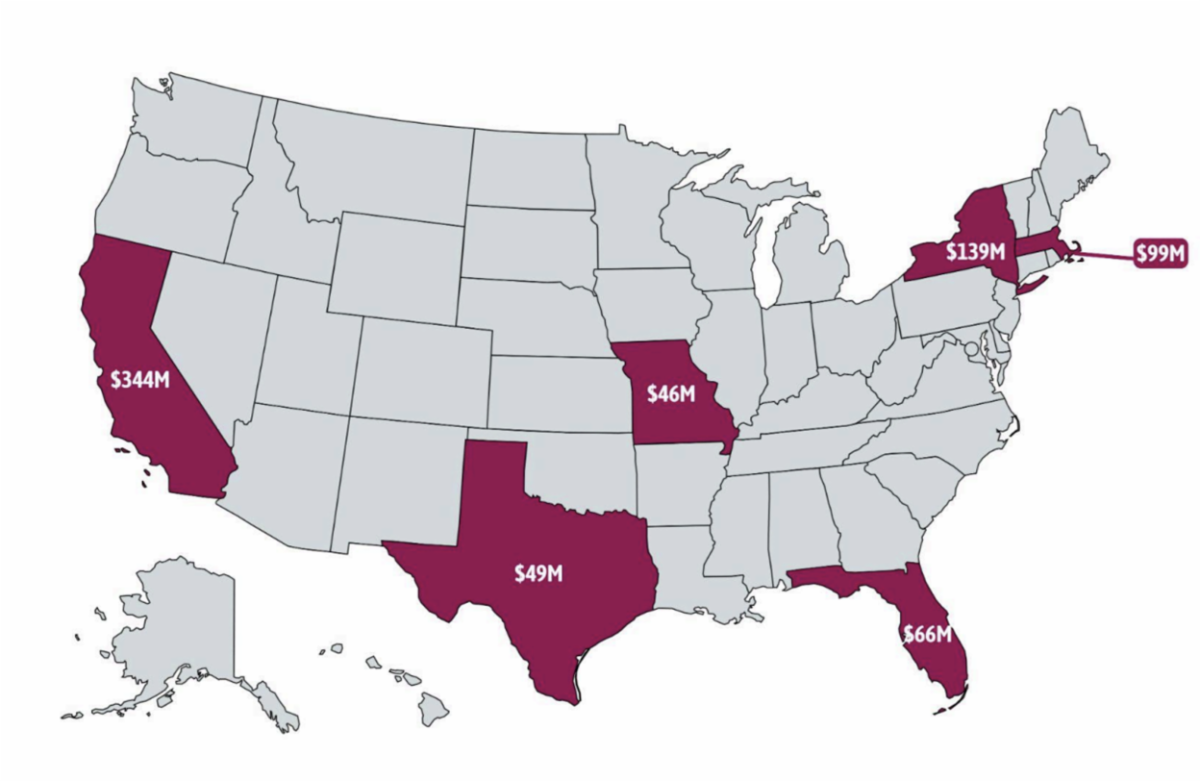

A new impact assessment from Community Solutions warns that changes in HUD’s FY 2025 Continuum of Care (CoC) Program NOFO could destabilize rental markets nationwide—potentially costing small landlords up to $1.8 billion in lost rent and putting tens of thousands of formerly homeless households at risk. The report finds that capping Permanent Housing renewals and sharply reducing Tier 1 protection creates a structural “revenue cliff,” pushing most long-standing housing projects into competitive Tier 2 and making renewal funding far less predictable. Using 2024 Housing Inventory Count data mapped to 2026 Fair Market Rents, the analysis estimates that tenant-based CoC spending is at risk in nearly every state and more than 700 communities. While exposure is greatest in high-cost states like California ($344M), the risk is widely distributed and significant in states such as Florida ($66M), Texas ($49M), and Missouri ($46M).

| | |

Reuters reports that state-backed Fair Access to Insurance Requirements (FAIR) programs, originally designed to provide last-resort property coverage when private insurers withdraw, have expanded rapidly as insurers retreat from disaster-prone regions across the United States. What began as a limited safety net is now becoming a structurally significant and fast-growing segment of the market, concentrating risk in undercapitalized public programs and increasing exposure for taxpayers and state budgets. The article also warns that this shift may distort housing markets and leave many homeowners with costly, fragile coverage that may prove unsustainable as natural disasters intensify.

UC Berkeley’s Letters and Science magazine highlights new research suggesting that while access to stable housing is essential for people experiencing homelessness, mental health and substance use treatment are also critical components of effective long-term support. The piece emphasizes that “housing versus treatment” is a false choice, arguing that evidence-backed models work best when they combine rapid housing with voluntary, sustained mental health and social services rather than making treatment a precondition for shelter. It frames homelessness as a complex problem driven by both structural factors, such as housing affordability, and individual health needs, and calls for integrated interventions that address these dimensions together instead of privileging one over the other.

A message from HUD’s Office of Policy Development and Research offers policy thoughts on how emerging construction technologies can lower housing costs without sacrificing quality. Principal Deputy Assistant Secretary for Policy Development and Research John Gibbs explains that manufactured housing can be produced at roughly half the cost of traditional homes, yet accounts for only a small share of new construction despite expanded access to conventional financing for CrossMod units. It also emphasizes that greater use of factory-built components such as panelized walls and floor trusses could speed construction and improve quality, though builder adoption remains limited. He notes that modular housing represents another promising frontier, offering stronger structures, faster timelines, and potential cost savings, with several states beginning to align around a shared performance-based code to support industry scale.

| | |

Monday, December 8

Coming Back Home Conference | Mayors & CEOs for U.S. Housing Investment and the National League of Cities, 10 AM – 12 PM ET

California Housing Conference & Expo, December 8-9

Tuesday, December 9

NAR Real Estate Forecast Summit, 3:30 – 5 PM ET

Wednesday, December 10

Virtual Workshop: Using Data to Inform Strategic Priorities in Your Community, 1 – 2:15 PM ET

CFA Financial Services Conference, December 10-11

Thursday, December 11

No events listed.

Friday, December 12

No events listed.

| | The National Housing Conference is a diverse continuum of affordable housing stakeholders that convene and collaborate through dialogue, advocacy, research, and education, to develop equitable solutions that serve our common interest. | | Defending Our American Home since 1931 | | Copyright © 2024. All Rights Reserved. | | | | |