1701 K Street, NW

Suite 650

Washington, DC 20006

Andrea Ball,

General Inquires:

|

|

Your annual membership provides you with an array of opportunities that you should take advantage of:

-

Discounts on regional lunch programs

-

Access to the CCTI resource library, the IdeaBank

-

Discounts on job postings in our Career Corner

-

Access to the Online Member Directory

-

Participation in our members-only LinkedIn Group

Or call: 703.823.7234

|

|

|

|

Happy Thanksgiving from CCTI!

|

We Want Your Opinion!

The 2018 CCTI Member Survey

Launches November 28th!

Dear Member,

Happy Thanksgiving! We hope you take time to enjoy the holiday with your family and friends! We'd also like to thank you for your continued participation to your member association!

As we look to 2018, the CCTI board of directors would like your opinions as we fine tune our programming and benefits for the coming year.

Next Tuesday, November, 28th, the CCTI 2018 member survey will be sent to all CCTI members. Please participate in this short electronic questionnaire, which will take less than 10 minutes of your busy day.

If you are unable to give your opinions online, we will be follow up via phone in the next few weeks with those members who have not clicked through and will interview you to get your input.

Again, thank you and Happy Thanksgiving! If I can be of personal or professional assistance, my direct contact information is below or feel free to reach out to our staff at

[email protected] or 703-823-7234

With Gratitude,

Andrea Ball

CCTI Executive Director

301-335-2715 - mobile

|

|

|

|

Major containerboard producers say box shipments in October were up 4-5% from tough year ago comp

US corrugated box demand was strong in October and the containerboard market remains relatively tight, particularly for export, major producers said in their recent earnings calls. International Paper (IP) and

WestRock (WRK) both said that their per-day box shipments for most of October were up around 4% from a year ago, and Packaging Corp of America (PCA) said its volume was up 5%.

This would be against a difficult comparison a year ago when October 2016 industry shipments jumped 4.5%, driven by an end-of-year surge in e-commerce holiday spending. The same strong fourth quarter pattern of last year seems to be repeating again this year, recent management comments suggest.

The box market "feels very strong to us right now," said IP Industrial Packaging of the Americas Sr VP Tim Nicholls, in response to an analyst's question.

Nicholls said box shipments for most of October were up 4%. This followed growth of 1.6% in the third quarter, which was less than the 4.2% overall industry growth that was reported by the Fibre Box Assn (FBA).

He indicated that IP's customer base was shifting in the quarter, with some box business "moving out," while new business "hasn't fully ramped up." He added: "Our growth numbers will go up as we go through the next couple of quarters with those wins coming in."

IP 'tight all year.' IP's mill system has been "tight all year" starting with Hurricane Matthew last fall, then working through the Pensacola, FL, mill outage last February and two hurricanes this fall, Nicholls noted. But he added the company is "getting better at how we manage it and we're on steady footing at the moment ... and can run with lower (inventory) levels than we've carried in the past."

He cautioned that "if supply chain delivery times start stretching out, then we will need to start working with more inventory to supply our network."

|

|

|

China increases contaminants rule to 1.0% on recovered paper, eliminates imports for small mills

China announced a final determination on a set of rules for recovered paper imports, with the new rules expected to be effective in about mid-January.

The most important of the new rules is a 1.0% contaminants level for recovered paper imports, according to contacts. China had earlier stated a 0.3% rule. US suppliers complained, admitting that they would not be able to make recovered paper bales with less than 0.3% contaminants. Also, the government in China said that mills in China with less than 300,000 tonnes/yr of capacity would not be allowed to import recovered paper. Further, the government said that traders of recovered paper would no longer be allowed unless they own a paper or board mill.

These rules become effective two months after they are published. Contacts expected them to be officially published soon.

One US supplier said the changes would result in a shut of some smaller mills in China and thus reduce China's overall demand for recovered paper.

For the 1.0% rule, the supplier added: "It gives us a certain relief that they're going to be reasonable about this and we can transact business."

With these rules announced on Nov. 7 in the USA, US recovered paper players still await the Chinese government's release of import licenses for 2018.

|

|

|

US containerboard mills look for strong fourth quarter, with only slight impact from hurricane in September

The North American containerboard market has been "quiet" after last month's attempted $50/ton fall price hike attempt by two producers failed to gain support from other major players. But box demand remains strong moving into the fourth quarter and containerboard supply remains balanced and even tight for some grades, according to contacts.

"I don't know of a single independent converter that is not busy or extraordinarily busy," one containerboard seller said.

Two recent hurricanes seemed to have only a "muted effect" on September industry statistics. US box shipments declined 1.0% on an actual basis to 31.790 billion ft

2 in September, but average-week increased 4.0% from a year ago, when adjusted for one less shipping day in the latest month, the Fibre Box Association (FBA) reported.

Analysts noted that on a "blended basis," box shipments grew 1.5%, averaging the change in actual and average week. They also noted last month's shipments were against a difficult September 2016 "comp," when both average and actual shipments were up 2.3% from the prior year.

"It's hard to see much impact from the hurricane on box shipments since the South Central region was one of the strongest in September, while the Southeast was one of the weakest, but it has been that way all year," one contact said.

Another strong fourth quarter? "Major integrated producers expect box demand in the fourth quarter to be a mirror image of last year, but up 1-2% from a year ago," one contact said.

That would be a strong performance since fourth-quarter 2016 average-week box shipments spiked up 4% from a year ago, driven by a surge of e-commerce buying before the holiday season. Last year box shipments began to pick up strength in August and the higher level of shipments has continued through this year, which analyst attribute to the "Amazon effect," and rebound of agriculture and strong overall economy in the West.

Year-to-date box shipments through September were up 2.3% on an actual basis and 3.4% higher average-week, adjusted for two less shipping days in 2017, or up 2.9% blended.

|

|

|

Monday Economic Report - November 20, 2017

Courtesy of the National Association of Manufacturers...

There were several reports out last week highlighting strength in the U.S. economy. Along those lines,

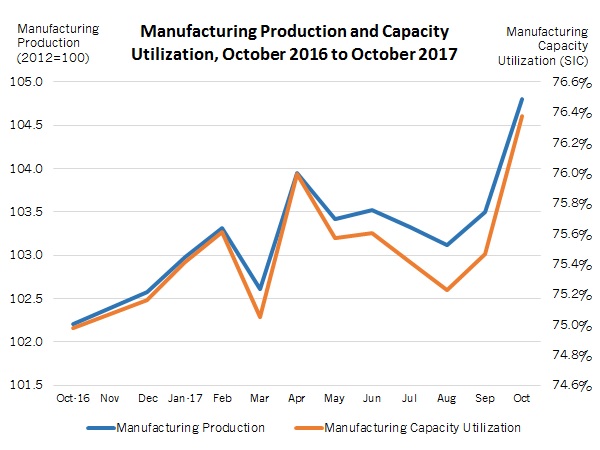

manufacturing production expanded robustly in October, up 1.3 percent, its fastest monthly pace of growth since April. In October, durable and nondurable goods production rose by 0.4 percent and 2.3 percent, respectively, with the latter rebounding from significant declines in activity in August and September in the chemicals and petroleum and coal products segments due to Hurricanes Harvey and Irma. As a result, manufacturing production has risen by 2.5 percent over the past 12 months, the best year-over-year rate since August 2014. In a similar manner, manufacturing capacity utilized soared from 75.5 percent in September to 76.4 percent in October, a reading not seen since May 2008.

At the same time, manufacturing activity in the

Kansas City,

New York and

Philadelphia Federal Reserve Bank districts continued to expand at rather robust paces despite a little softening in each of the most recent surveys. The Kansas City and New York reports reflected some easing from multiyear highs in the previous release, with still-high rates of expansions for new orders, shipments and employment in all of the regional Fed surveys so far in November. More importantly, manufacturers continued to be very optimistic in their outlook for the next six months. In terms of downsides in the current data, those completing the latest surveys once again cited challenges in attracting talent, and raw material costs have trended higher in recent months. (More on that topic below.)

In addition to manufacturing, there were also healthy figures for the housing and retail markets. For instance, new

housing starts jumped 13.7 percent to 1,290,000 units at the annual rate in October, its fastest pace in 12 months. That is encouraging news, and yet, it is worth noting that the bulk of that increase stemmed from better multifamily activity, which can often be highly volatile from month to month. Multifamily housing starts soared from 302,000 to 413,000 in this release, the best reading since January. New single-family construction was also higher, up from 833,000 to 877,000, an eight-month high. Single-family starts have largely trended in the right direction, averaging 841,300 year-to-date in 2017 versus 778,200 in the same time period in 2016. Housing permits and

builder optimism numbers suggest that residential activity should continue to improve in the coming months, which is promising.

Consumer spending has been a bright spot in the economy, but there was more caution in the data in the summer months than we might have preferred. The good news is that Americans have opened their pocketbooks more since then. Indeed,

retail spending edged higher in October, up 0.2 percent, building on September's strong 1.7 percent gain. On a year-over-year basis, retail sales have risen 4.6 percent since October 2016, off just slightly from 4.8 percent in the previous report, which was a six-month high. There has been robust growth in motor vehicle and parts sales in the past two months, up 4.6 percent and 0.7 percent in September and October, respectively, with the segment benefiting from hurricane-related replacements. Excluding automobiles, retail sales were up 0.1 percent in October, with year-over-year growth of 4.3 percent.

Meanwhile,

producer prices for final demand goods and services rose by 0.4 percent in October for the second straight month. Overall, producer prices have increased 2.7 percent since October 2016, up from 2.5 percent year-over-year last month and a pace not seen since February 2012. Raw material costs have accelerated over the course of the past 12 months, as the year-over-year rate was 1.2 percent one year ago. Nonetheless, core producer prices-which exclude food, energy and trade services-continue to be modest at 2.2 percent, up from 2.1 percent in September. For comparison purposes, core producer prices were 1.6 percent year-over-year in October 2016.

Similar trends exist for

consumer prices, which edged up by 0.1 percent in October. The consumer price index increased 2.0 percent year-over-year in October, down from 2.2 percent in September. In addition, core consumer prices, which exclude food and energy costs, have risen 1.8 percent over the past 12 months, inching up slightly from 1.7 percent in the prior release. As such, overall pricing pressures remain mostly under control for now, even with some acceleration. Nonetheless, the Federal Open Market Committee is still likely to raise short-term interest rates at its December 12-13 meeting, mostly on improvements in the macroeconomy and from general tightening in labor markets.

|

|

|

Linerboard: North American producers upgrading white top mills to improve quality, cut costs

North American containerboard producers are targeting more capital spending to increase capacity, improve product quality, and reduce cost of their mills supplying the white top linerboard market.

The high margin 2.2-million ton/yr North American white top market is dominated by three major producers (WestRock, International Paper, and Georgia-Pacific) and has been fairly static in recent years despite facing a changing retail environment and more competition from imports.

"The increased spending is a good thing to improve the competitiveness of North American suppliers," one contact said.

Three upgrades planned. The most dramatic recent move was International Paper's (IP) announcement to spend $300 million to convert the No. 15 machine at its Riverdale Mill in Selma, AL, from uncoated freesheet to 450,000 tons/yr of white top kraft linerboard and containerboard.

Georgia-Pacific last spring announced that it would spend $50 million to rebuild the 305,000 tons/yr No. 2 white top kraft linerboard machine at its Brewton, AL, mill. The project is mainly designed to improve quality, but could include a shoe press that could add some incremental capacity, according to contacts.

This followed a $388-million energy improvement project at Brewton, which also reduces energy costs for its No. 1 machine, which makes 195,000 tons/yr of bleached board.

West Rock may spend more than C$25 million upgrading the washing and bleaching systems at its La Tuque, QC, mill to reduce energy costs. The Quebec government said would provide C$10 million in financial assistance, according to a local news reports. The mill has capacity to produce about 347,000 tons/yr of white top, of which 53,000 tons/yr is coated. Also, contract negotiations with the 240 workers at the La Tuque mill were underway with a mediator present after the union rejected an earlier offer, reports said this week.

IP to focus Riverdale on white top. In IP's earnings call on Oct. 26, Industrial Packaging Sr VP Tim Nicholls told analysts the converted No. 15 machine at Riverdale would produce "a very high-quality" two-ply sheet and would be in the "first quartile" in North American production costs, and should achieve "very attractive returns."

Some analysts had pointed out that the capital cost per ton of the Riverdale project is $676/ton, which is twice as high as the cost of Packaging Corp of America's recently announced conversion of an UFS machine at Wallula, WA.

But CEO Mark Sutton noted that "comparing white and brown projects really doesn't make a whole lot of sense" and that there will be "systems effects" from the Riverdale investment that makes capital cost per ton "a little deceiving."

Would 'free up' Mansfield for brown. Nicholls said the project would allow the company to "free up" two other machines in IP's mill system that today make white top on a swing basis. Those machines would then be able to focus on producing brown containerboard, and increasing efficiency and adding incremental capacity.

IP is producing an estimated 250,000 tons/yr recycled white top linerboard on the No. 3 machine at Mansfield, LA, mill and about 94,000 tons of kraft white top on the No. 2 machine at its Springfield, OR, mill.

CEO Mark Sutton pointed out that IP must today buy white fiber, mainly sorted office paper along with pulp substitutes, for Mansfield to make recycled deinked white top "at a mill which was designed to make brown linerboard."

Mansfield's total containerboard capacity is nearly 1.6 million tons, while Springfield's capacity is 1.5 million tons/yr.

IP reportedly must trade to gain all of the white top it needs for its box plant system and supposedly has a deal with WestRock. This would not be surprising since WestRock is the largest white top producer with 1.3 million tons of capacity and an estimated 63% share of the North American market.

|

|

|

FDA Issues Guidance to Allow "Co-Manufacturers" Additional Time to Implement Certain Supply-Chain Program Requirements

Today, the U.S. Food and Drug Administration (FDA) announced the availability of a guidance designed to give certain co-manufacturers more time to meet supplier approval and verification requirements under three FDA food safety regulations.

Three of the rules created to implement the FDA Food Safety Modernization Act (FSMA) - Preventive Controls for Human Foods, Preventive Controls for Animal Food, and the Foreign Supplier Verification Programs - have requirements for a supply-chain program for certain raw materials and other ingredients. This program is designed to address hazards requiring a supply-chain-applied control.

This guidance is intended for participants in "co-manufacturing" agreements in which a brand owner arranges for a second party to manufacture or process food on its behalf. The rules require co-manufacturers to whom the supply-chain program applies to approve their suppliers of certain raw materials/ingredients and conduct supplier verification activities. While the co-manufacturer is required to approve its suppliers, there is some flexibility in the rules that allows the co-manufacturer to rely on a brand owner's supplier verification activities.

To meet the requirements of the supply-chain program, the co-manufacturer may need detailed information from the brand owner. Based on input from the food industry, FDA has determined that the industry needs more time to establish new contracts that will allow brand owners and co-manufacturers to share certain information, such as audits of suppliers.

The guidance states that FDA does not intend to take enforcement action for two years against a co-manufacturer that is not in compliance with certain supply-chain program requirements related to supplier approval and supplier verification. This enforcement discretion is conditional on the supplier approval and verification activities being divided between the brand owner and the co-manufacturer.

This guidance, entitled "Supply-Chain Program Requirements and Co-Manufacturer Supplier Approval and Verification for Human Food and Animal Food: Guidance for Industry," is immediately effective. You may submit electronic or written comments regarding this guidance at any time, as well as find more information, at

https://www.regulations.gov.

|

|

|

CCTI launched a new website in the fall of 2017. In addition to a more robust members only area and better navigation, a

reas of interest includes news articles and meeting information, Ask Vinny, and the members only section, which includes a member directory, links to CCTI's technical documents and other member benefits.

|

|

|

Industrial Paper Tube, Inc., located in Bronx, NY, has automatic spool machinery available for sale. Please contact Howard Kramer at 718-893-5000 for prices and more information

Industrial Paper Tube, Inc., located in Bronx, NY, has automatic spool machinery available for sale. Please contact Howard Kramer at 718-893-5000 for prices and more information

Industrial Paper Tube, Inc.

1335 East Bay Avenue

Bronx, NY 10474

Phone: 1-800-345-0960

Fax: 718-378-0055

Email:

[email protected]

Link

|

|

|

|

YOU NEED TO ADVERTISE WITH CCTI!

The CanTube Bulletin offers an excellent marketing opp

ortunity for companies in the tube, core and composite can industry.

The CanTube Bulletin offers an excellent marketing opp

ortunity for companies in the tube, core and composite can industry.

The CTB is published online on a monthly basis. and our distribution list consists of all CCTI members and their employees.

Monthly ads are $50 or an annual commitment is $500 for 12 issues. For more information call the office or email us at...

|

|

|

|

|