|

After decades of stagnant rental supply, in 2018, CMHC announced construction financing programs that brought life to the rental market. Not only did CMHC provide the light, they also provided the gasoline to go with it.

The ACLP and MLI Select programs were a huge success and have delivered hundreds of thousands of new rental homes across the country. So much supply, that today, we can actually see some softening of rents and an increase to vacancy rates. Two things the housing industry was working hard for, for a long time.

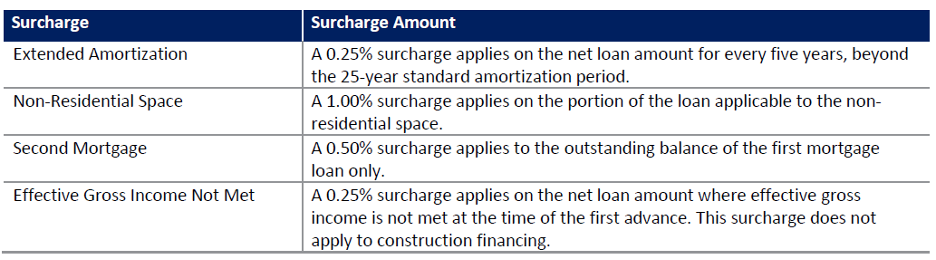

Over the past two years, CMHC has announced change after change that continues to push new challenges on rental developers. Implementing immediate and sometimes costly changes to the previously robust construction programs that developers rely upon to deliver new rental housing.

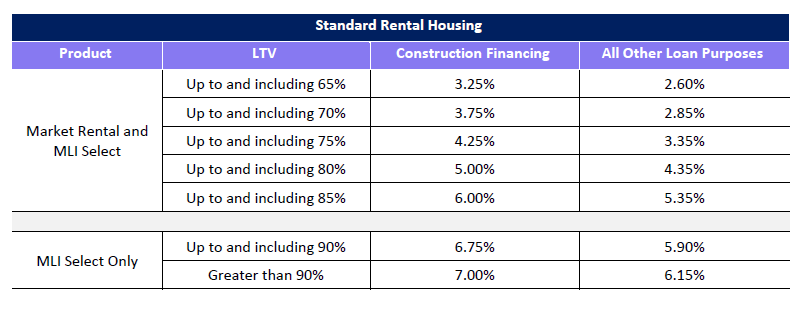

July 3rd, 2025 was no different. CMHC announced two changes. One of which, makes the MLI Market construction program a bit more enticing (if less leverage is an option) while the other change will add further costs to projects that rely on MLI Select for viable financing.

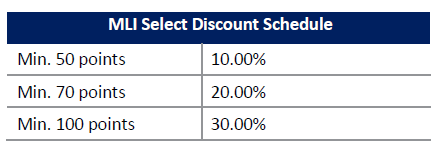

The changes to the MLI Select program will not affect leverage, but it will add to the costs.

Citifund, on behalf of its clients, has successfully navigated each and every CMHC policy change by analyzing and maximizing the available options. These new changes are no different.

Citifund is here to help. Do not hesitate to call.

|