Everyone wants financial independence backed by stability and security, and FSG's Financial Planning Team can help you achieve this. Whether it's investment/retirement planning, estate planning, or disability/life insurance, our team provides trusted advice with the goal of protecting and growing your assets. Contact Mike Edwards at (720) 858-6289 to learn how we can help.

|

Need workers' comp and employee benefits, while also considering a PEO option? We can help!

We've teamed up with

Bene-Fit Solutions to provide competitive rates for worker's comp and employee benefits, while also providing the convenience of a PEO. For more information, please contact

Mitch Laycock at

(720) 858-6297.

|

|

|

|

HSAs: What They ARE and What They are NOT |

Health Savings Accounts (HSAs) have been around for about 13 years, but they are still often misunderstood. HSAs are

not employer-sponsored health plans, and they are

not checking accounts. They are more accurately described as individually owned, tax-exempt trusts or custodial accounts available to individuals covered by an HSA eligible health plan.

What is an "eligible" health plan? The plan must meet the deductible and out-of-pocket requirements set by the Internal Revenue Service (IRS), and must have the words "qualifying high-deductible health plan" or a reference to the Internal Revenue Code Section 223 in the declaration page of the policy or other official communication from the insurance company. If this documentation is not provided or available, it is

not a qualifying plan. Not all high-deductible plans are HSA-qualified even if they meet deductible and out-of-pocket requirements.

HSAs have two components, a cash component and an investment component, both under the tax sheltered umbrella. Depending on the insured's need in a particular year, they have the opportunity to benefit from both. Contributions into an owner's HSA are not taxed, interest paid is not taxed, nor are any distributions for qualified medical expenses.

The IRS sets contribution limits each year, and for 2018 the maximum contribution for "single coverage" is $3,450 and $6,900 for "family coverage," unless you are over 55, in which case you can contribute an additional $1,000 to your HSA.

Also, contributions to an HSA are NOT use-it-or-lose-it like flexible spending accounts, and you have until tax day (April 15th) to contribute into an HSA in order to get the tax benefit for the prior year.

One of the most important elements employers and individuals should consider when evaluating an HSA offering is whether the medical plan will work for them. HSA-qualified plans typically offer lower monthly premiums than "traditional" health plans, however, the insured is responsible for all costs (except preventive care) until the deductible is met. With this in mind, insureds should analyze their needs and budget, both for themselves and family, to choose a plan best for them.

We are happy to assist with this important decision, so please feel free to call COPIC FSG for help.

Contact

Andrea Levine

at (720) 858-6287 with your questions.

|

|

Data Breaches in the Headlines |

Local health care:

Hackers may have gained access to the personal data of more than 3,000 patient families at Children's Hospital Colorado

One of the greatest risks that medical professionals and medical facilities face today is the loss or misuse of sensitive patient data. In addition, as medical practices rely on networked devices, electronic health records, and external business associates handling patient and financial data, they become more susceptible to cyber threats including computer viruses, malware, hacking, or lost or stolen mobile devices.

The largest reported health care data breaches that occurred in 2017 have potentially affected nearly 1.5 million people, with hacking being the leading cause of the breaches:

- Kentucky: Confidential info taken from nearly 700,000 Med Center Health patients

- Michigan: Airway Oxygen Inc. Ransomware Attack Impacts up to 500,000 Individuals

- Pennsylvania: Security Breach at Women's Health Care Group Affects 300,000 patients

Contact us today to review your current data breach coverages and be confident about your cyber security. Contact

Mitch Laycock

at (720) 858-6297 for help to make sure you are appropriately insured.

|

|

3 Financial Tips for Unmarried Couples |

If you are in a long-term, committed relationship, you have many of the same financial concerns as married couples. However, you lack many of the legal protections and advantages that married couples enjoy. Here are some tips that can help you and your partner stay on the road to financial security.

- Talk about your finances: How will you handle your finances, separately or jointly? Discuss each other's financial values, priorities, and goals. Being open and honest helps to avoid future arguments about money.

- Plan for retirement: Unmarried partners are not eligible for spousal benefits from social security nor defined pension plans. But there are other ways like beneficiary designations on 401(k)s and IRAs that can help provide funds in retirement.

- Make estate planning a priority: Unmarried couples do not receive the protection married couples do and without proper planning, your estate may be disposed of in a manner against your surviving partner's wishes.

Read the article from Woodbury Financial to learn more about financial planning for unmarried couples and contact Mike Edwards at (720) 858-6289 for assistance in executing a financial planning strategy that's best for you.

___________________________________________________________

Securities and Investment Advisory Services offered through Woodbury Financial Services, Inc., Member FINRA, SIPC and Registered Investment Adviser. COPIC Financial Service Group and Woodbury Financial Services, Inc. are not affiliated entities.

|

|

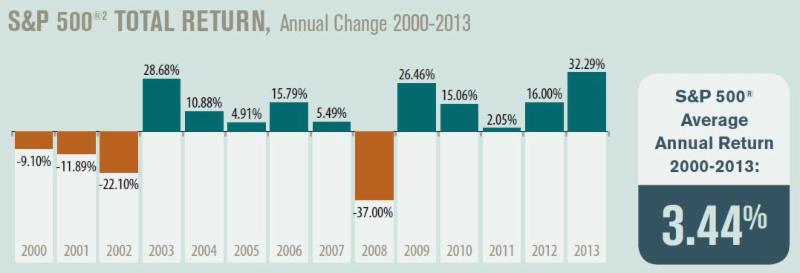

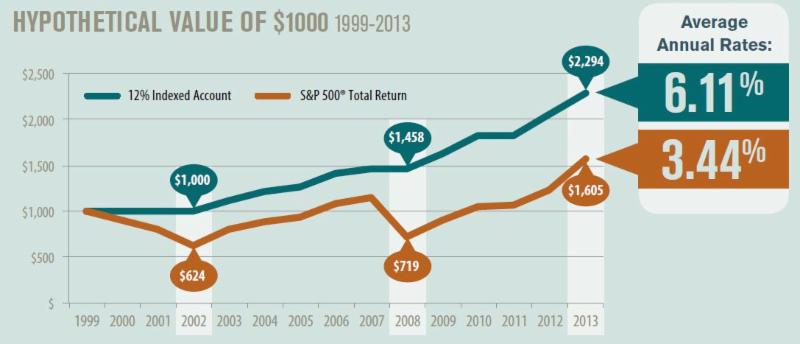

The Potential Power of Indexed Universal Life Insurance |

Indexed universal life (Indexed UL) provides life insurance protection plus the benefit of an index-based interest crediting strategy.

In 1999, the stock market had finished a truly remarkable decade, and equity-linked products of all kinds were all the rage. However, in the 14 years since, the S&P 500 has only averaged 3.44%, including dividends:

If you could have eliminated the losses, capped any one year's growth at 12%, and even removed the benefit of dividends, the average annual crediting rate would have been 6.11%.

___________________________________________________________

Securities and Investment Advisory Services offered through Woodbury Financial Services, Inc., Member FINRA, SIPC and Registered Investment Adviser. COPIC Financial Service Group and Woodbury Financial Services, Inc. are not affiliated entities.

|

|

The Ups and Downs of Health Insurance |

As headlines continue to report the battle surrounding the Affordable Care Act and the individual market, there is some good news in the employer sponsored market. For the sixth year in a row, the Kaiser Family Foundation has reported a fairly modest increase in premiums, based on their annual survey.

While individual carriers are taking a 27% price increase on average, we have learned that at least one carrier will have zero increase in rates for the first quarter of 2018, and may even have a small decrease. We hope this translates to good news in the form of renewals, and that you are able to continue to recruit and retain quality employees by offering valuable benefits at affordable prices.

COPIC FSG works to stay apprised of the changing landscape so we can provide the best options for your specific situation. Contact

Andrea Levine at (720) 858-6287 for more information.

|

|

End-of-Year Insurance Review

|

Now is the time to schedule what many business owners have called "the most valuable 30-minute visit a practice can make."

Schedule a complete insurance summary review to be certain your personal assets are shielded from your business-related exposures and liabilities. We are happy to meet with you in-person or via telephone conference. In the meantime, ask yourself these questions regarding your business owners' and workers' compensation policies. An insurance review helps to identify any gaps in coverage and can reassure that your policies are the best for your situation.

Contact

Mitch Laycock

at (720) 858-6297 for more information.

|

|

Even if you are not currently in the market for insurance

products, we are always available to help make sure you are

getting the best coverages at the best prices. Call us at

(720) 858-6280!

Sincerely,

Sue Swanson

President, COPIC Financial Service Group

Please add us to your "safe-senders" list! Add

[email protected] to your address book to ensure that our messages to you don't get stuck in your spam filter!

|

|

|