| Partners |

| (click on logo to link to website) |

|

|

|

| |

President's Perspective

~~~~~~~~~~~~~~~~~~

SEC structural changes to Rule 2a-7 of the Investment Company Act of 1940 take effect tomorrow, October 14th. These changes alter the manner in which prime institutional money market funds (MMFs), such as the CalTRUST Heritage MMF, operate and will now:

- Require prime institutional MMFs to transact at a variable, or "floating" NAV, rather than the traditional $1.00 share price; and

- Authorize prime institutional MMF Boards to impose redemption gates and fees in times of market illiquidity.

In response to these changes, CalTRUST added a Government Money Market Fund to our offerings to provide an investment option with a stable NAV and same-day liquidity. The CalTRUST Government MMF gives local agency investors:

- A stable $1.00 NAV, with no redemption gates or fees;

- Same-day liquidity for purchases and redemptions until 1 pm PT;

- "AAAm" and "Aaa-m" ratings from S&P and Moody's, respectively;

- Highly competitive money market rates;

- Best available expense ratio in Select Class shares; and

- Full compliance with all provisions of Rule 2a-7 governing SEC-registered MMFs.

With Economic Data Trending Modestly Stronger, CalTRUST Funds Are Positioned For Challenge Of Higher Rates

As expectations build for a hike in rates by the Fed, and modestly rising rates in the economy, fixed income investors face challenges - whether they be individuals or institutional investors like public agencies. The low yield environment since the 2008 financial crisis has presented investors with near zero yields for short-maturity securities and -- comparatively -- modestly higher yields for longer maturity investments. Given the persistence of this low rate environment, it is understandable that many investors have been tempted to look to longer maturity securities to boost the yield on their portfolios.

This "reaching for yield", however, exposes investors to interest rate risk. Since bond prices move in inverse relationship to yield and the general direction of rates, as rates rise the price of fixed income securities falls. In a rising rate scenario, this inverse relationship can result in negative rates of total return on an individual security or a portfolio; even on "safe-haven" instruments such as US Treasuries.

Public agency investors tempted to "reach" for additional yield by extending the maturity of their holdings need to understand the additional risk they are assuming. At CalTRUST, we are very mindful of this risk, and have positioned the CalTRUST Short- and Medium-Term portfolios toward the lower-end of their target durations, so as to manage this risk, to ensure sufficient liquidity to meet participants' cash needs, and to provide the flexibility to take advantage of higher rates when they do arrive.

For

more information on the CalTRUST funds, please contact me by email at the address listed below, or contact:

Lyle Defenbaugh

Wells Fargo Asset Management |

(916) 440-4890 |

Laura Labanieh

CSAC Finance Corporation |

(916) 650-8186

|

Norman Coppinger

League of CA Cities |

(916) 658-8277 |

Neil McCormick

CA Special Districts Association |

(916) 442-7887 |

Chuck Lomeli is CalTRUST President

and Solano County Treasurer

|

Financial Markets Update

~~~~~~~~~~~~~~~~~~~~

History Indicates That Equity Markets Will Keep Rising in 2017 -- If Earnings Growth Exceeds The 10-Year Treasury Yield

In his most recent

Economic & Market Perspective

, WellsCap Chief Investment Strategist, Jim Paulsen looks at the relationship between the US stock market and bond yields in the post-WWII era.

Jim shows that the equity market has done fine, even in periods of rising rates, provided the annual growth rate in earnings per share (EPS) exceeds the 10-year Treasury bond yield. To illustrate the point, Jim looks at the Earnings-Yield Indicator (EYI) - the annual growth in trailing 12-month S&P 500 EPS minus the 10-Year yield.

Looking at the history of the EYI since 1950, Jim finds that, when the EYI was above zero the stock market generated:

- Annualized returns more than twice as great as when the EYI was below zero -- 11.6% versus 4.7%;

- Positive monthly returns 62% of the time compared to only about 55% of the time when the EYI was below zero.

Moreover, in months when the 10-year bond yield rose and the EYI was above zero, the S&P 500 Index increased at almost a 10% annualized rate, versus only a 0.61% pace when the EYI was negative.

In looking forward to 2017, with commodity prices having stabilized and begun rising modestly, Jim sees a modest pickup in earnings growth and a positive EYI. This is probably sufficient to keep the market rising -- even in the face of Fed rate hikes.

Jim's complete

blog post

can be accessed

here.

|

CalTRUST Portfolio Snapshot (as of September 30, 2016)

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

1. CalTRUST Short-Term and Medium-Term and LAIF yields are net of fees. Merrill 1-5 Year Indexes are unmanaged; and do not reflect any deduction for administrative fees or expenses.

2. CalTRUST and LAIF returns are net of all investment advisor, administrative and program fees.

3. Annualized.

4. The CalTRUST Short-Term and Medium-Term portfolios commenced operations on February 13, 2005.

|

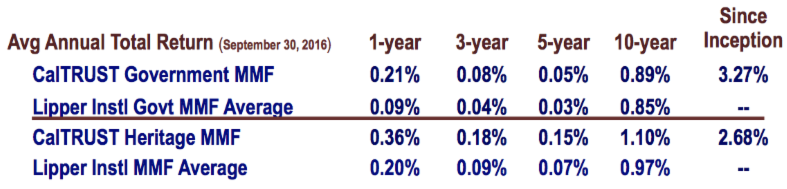

CalTRUST Government & Heritage Money Market Funds

~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~~

|

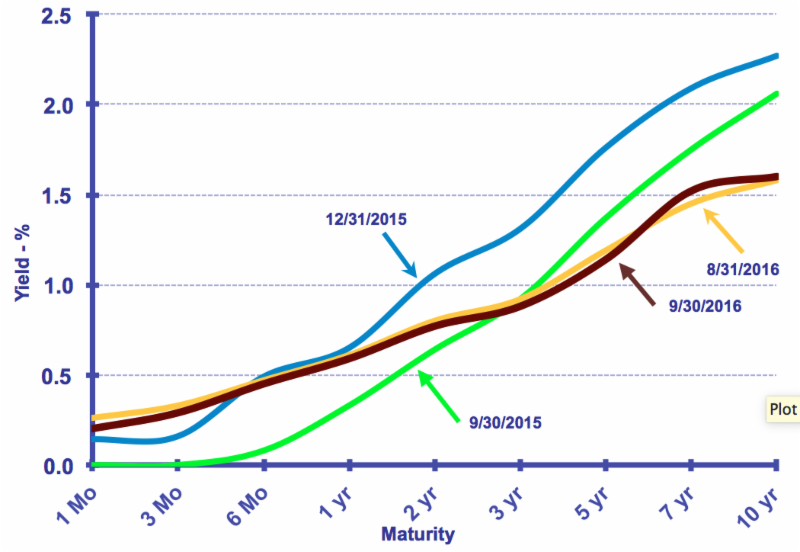

Treasury Yield Curve

~~~~~~~~~~~~~~~~

|

2016 Calendar

~~~~~~~~~~~

November 11 Veterans Day Closed for Trading November 24 Thanksgiving Closed for Trading November 25 Thanksgiving Holiday Early Closure - 10:00 am PST December 23 Observed Christmas Eve Early Closure - 10:00 am PST December 26 Christmas Observed Closed for Trading December 30 New Year's Eve Observed Early Closure - 10:00 am PST January 2, 2016 New Year's Day Observed Closed for Trading |

|

| |

|