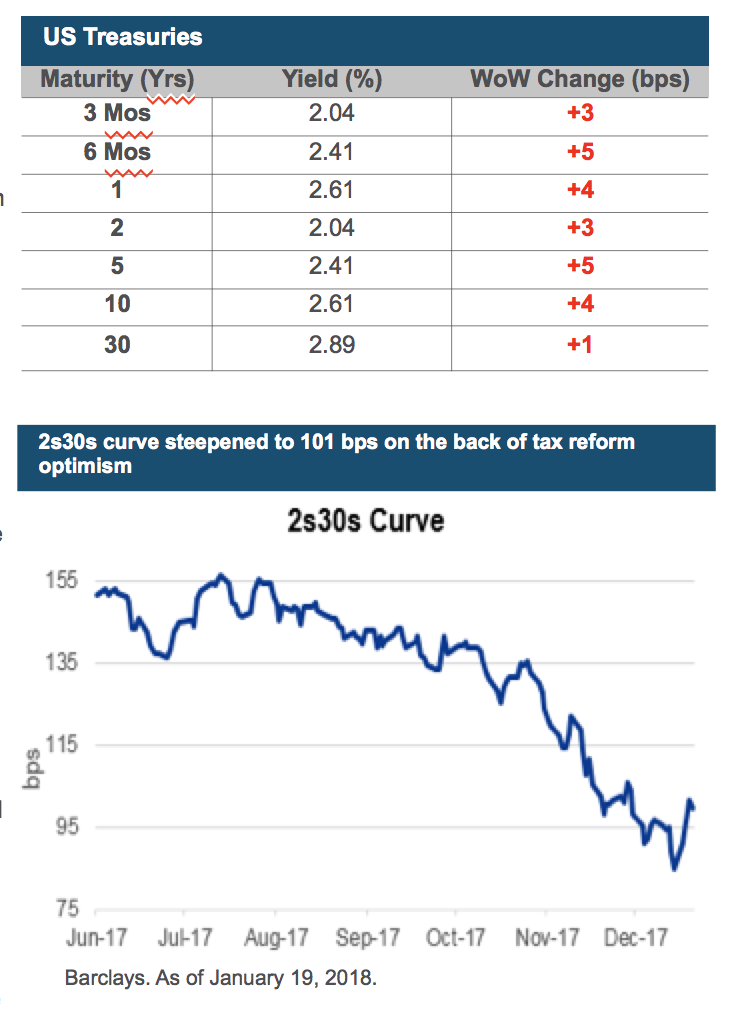

Summary: This week Congress successfully passed the largest tax overhaul in three decades and President Trump is expected to sign the bill on January 3rd. Now, legislative attention turns to keeping the U.S. government open. Late on Wednesday, House leaders released a plan that would maintain funding for the government through January 19th. A House vote could come later today, and both chambers have to pass the spending bill before midnight Friday to avert a partial shutdown of the US government. In rates, 2s30s steepened on tax reform optimism. In the US, new and existing home sales came in better than expected and the third quarter GDP was revised slightly lower on weaker consumer spending.

Tax Reform: This Wednesday Congress passed the tax bill which now heads to President Donald Trump for his signature. Nearly all of the tax changes (such as a decline in the individual's top tax rate, from 39.6 t to 37% and the corporate rate's permanent cut to 21%) will take effect at the start of 2018.

US 3Q GDP: The third estimate of Q3 GDP contained a 0.1 pp downward revision, and the economy is now reported as having grown by 3.2% versus 3.3% in the second estimate. In the third estimate the revision primarily came from personal consumption, particularly in the services component. However, some of the downward revision in services consumption was offset by spending on goods which was pushed higher to 4.5% from 4.1%.

Consumer Confidence: In the preliminary reading for January, the University of Michigan index of consumer sentiment edged lower, to 94.4 from 95.9, below expectations of 97.0. The main sub-component that drove the overall index lower was the current conditions index which showcased that consumers are reacting to rising prices for big-ticket purchases, such as vehicles and homes.

Short Duration Portfolio Positioning: Holistically our duration position remains muted versus the benchmark with a slight curve flattener bias. This week our new issue buys coincided with a mild rate back-up creating a tactical opportunity to add a little interest rate risk and more yield. We optimized our Agency book by selling December 2019 US Agency paper and extending into Jan 2021. We also added International Finance Corporation paper within the SSA sector maturing in Jan 2021 and yielding 2.25%.