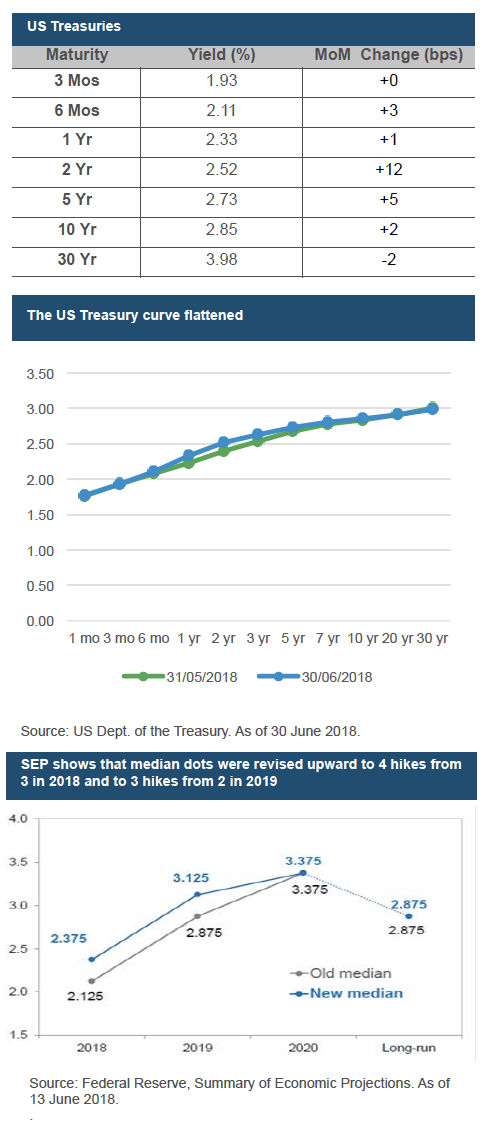

Summary: In June the market saw a continuation of the intertwining dynamic between robust economic growth juxtaposed with the escalating trade tensions coming to the forefront. On the back of this risk-off sentiment, 10-year Treasuries rallied as much as 11 bps intra-month, before ending the period modestly higher at 2.85%. This further exacerbated the flatness of the yield curve, with the 2s10s spread reaching 33 bps, its tightest level since September 2007.

June FOMC Meeting: As widely expected, the FOMC raised the target range for the federal funds rate by 25 bps, bringing the Fed's benchmark rate to a range of 1.75% to 2%. The Fed's outlook for the economy remains quite positive with the 2018 and 2019 median dots for projected rates moving up 25 bps, to 2.375% in 2018, and 3.125% in 2019. The FOMC collectively moved its expected growth rate for 2018 up by 0.1% to 2.8% and raise its core inflation forecast from 1.9% to 2%.

ECB Meeting: The European Central Bank announced that it will end its QE program in December this year, with the final pace of asset purchases being tapered down to €15 billion per month for the final quarter (from the current €30 billion monthly pace). In addition, the market was taken by surprise with the clarity and change to its forward guidance - the ECB stated that it does not expect to raise rates until after next summer.

US Non-farm payrolls: May non-farm payrolls gained 223K jobs, well above expected 188K. The unemployment rate fell to 3.8%, an 18-year low (May 2001). The average hourly earnings increased 0.3% (MoM) and 2.7% (YoY). Additionally, March print was revised up from 135K to 155K and April ended worse from 164K to 159K.

US Q1 GDP (3rd Revision): The third revision of US Q1 GDP was revised downward yet again to 2% from an initial first reading of 2.3%. The latest revision was driven by another reduction in consumer spending, which only rose by 0.9% compared to 1%. Also, spending on services came in lower with a reading of 1.5%, which compares to an initial estimate of 1.8%. Lastly inventories and net exposure also detracted from Q1 growth.

ISM Manufacturing (June): The ISM manufacturing index surprised to the upside increasing from 58.7 to 60.2. This positive report was primarily driven by production, supplier deliveries and new export orders, while inventories and employment remained unchanged.

CPI: As expected, the headline CPI print came in at 0.2% (MoM), and at 2.8% (YoY), while the core measure rose 0.2% (mom), and 2.2% (YoY). At the headline level, CPI was driven by an increase in energy prices (0.9%). The core measure was driven primarily by shelter and medical care prices.