|

©2025 YCharts

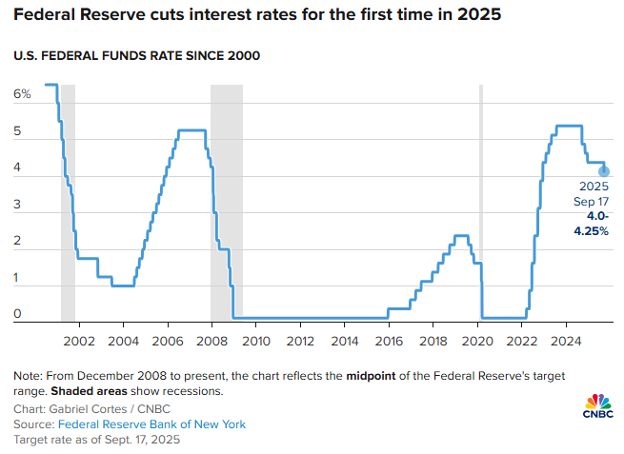

The Federal Reserve cut interest rates on Wednesday, September 17, 2025, its first cut of 2025, and hinted that two more cuts will happen before the year ends. The Federal Open Market Committee, a 12-member group that makes these decisions, lowered the benchmark interest rate by a quarter percentage point. In its official statement, it said that “uncertainty about the economic outlook remains elevated.”

So, what does that really mean? Do Fed officials just announce a cut and watch the market follow along? Not quite. They use specific tools to change how much it costs banks to borrow money from each other — and those costs then spread through the economy in different ways and at different speeds.

How the Rate Cut Actually Works

When we say interest rate cut, which interest rate are we talking about? The specific rate the Fed focuses on is called the federal funds rate. This is the interest rate that banks charge each other for overnight loans. To change this rate, the Fed buys or sells short-term government bonds, like Treasury bills. When it buys bonds, it pumps money into the banking system, which makes borrowing cheaper. When it sells bonds, it pulls money out, which makes borrowing more expensive.

Once the Fed moves the federal funds rate, other borrowing costs tend to change too, but not in the same way or at the same time. Auto loans and personal loans often react quickly because they’re closely connected to short-term borrowing costs. Credit card rates, however, are much more “sticky.” Because these loans are unsecured and carry higher risk, lenders are slow to lower rates — often waiting weeks or longer, and even then, the reductions are usually small.

Mortgage rates work differently. The popular 30-year mortgage rate is tied more to the yield on the 10-year Treasury note than to the fed funds rate. That yield shows what investors expect about long-term growth and inflation. If investors think inflation will stick around, they demand higher yields, which keeps mortgage rates high even if the Fed cuts the federal funds rate.

Does This Work, and What’s Different Now?

History shows that rate cuts don’t always produce the same results. After the dot-com bubble burst in the early 2000s, aggressive Fed cuts led to a housing boom and broad economic growth. But during the 2008 financial crisis, even near-zero rates couldn’t unfreeze frozen credit markets, so the Fed had to try new tools like quantitative easing — buying longer-term bonds to push down mortgage rates and encourage lending. In 2020, rapid cuts paired with emergency programs stabilized markets and supported a quick recovery during the pandemic.

That background matters today. Normally, the Fed avoids cutting when inflation is high. But the current situation is more complicated. Inflation is still above the Fed’s 2% goal, but it has cooled significantly from its 2022 peak. Core inflation, which excludes food and energy, is also trending lower. Meanwhile, growth is slowing, job creation is getting weaker and households and businesses are struggling with high borrowing costs. The Fed faces a tough choice: keep rates high to crush inflation completely or begin cutting to prevent a recession. It looks like it’s more worried about the recession risk.

It has hinted that two more cuts may come this year, but critics warn that easing too soon could let inflation come back, especially if energy prices or wages climb. Others argue that keeping rates too high risks hurting growth, investment and employment. Housing affordability is a clear example of this tension: despite Fed policy moves, mortgage rates remain high because they track the 10-year bond yield.

In today’s situation, a Fed rate cut is less about saying “mission accomplished” on inflation and more about balancing two goals: keeping prices stable and supporting growth. Whether it works depends on how banks, investors, businesses and households respond. History offers a clear lesson: Rate cuts are powerful, but not magic. They work best when confidence is strong, and inflation is seen as under control. Right now, the Fed is trying to walk a fine line, and the outcome could shape the economy and financial markets for years to come.

The latest FOMC meeting was also marked by unusual political drama, which is rare for an institution that usually operates quietly with little disagreement. The Fed’s independence has deep historical roots and good reasons behind it, though that’s a discussion for another time.

|