|

OHFA TIC and Net Assets Under HUD’s Threshold

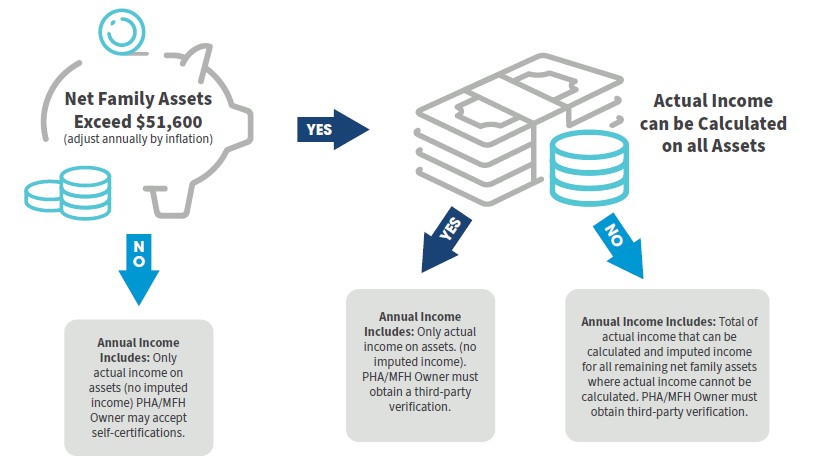

Should all net family assets be listed on the OHFA TIC even if they are under HUD’s threshold amount? If so, what value of each asset should be listed on the TIC?

Effective immediately, if all net family assets are less than the threshold amount, $0 must be listed as the value of each asset on the TIC. If the net family assets are greater than the HUD threshold, then owners/management agents must list the actual value of each asset on the TIC. Importantly, income from an asset(s) is always counted regardless of whether it is under/over HUD’s threshold amount.

Example #1:

Mary has a checking account balance of $800, and a savings account value of $900, which has a 1.5% interest rate. Since the value of the assets is less than the threshold amount ($800 + $900 = $1,700), owners/management agents will list both assets on the TIC but the value will be $0 for each. The income from the savings account interest accrued, $13.50 (i.e., $900 x .015), will be counted as income and listed on the TIC.

Example #2:

Chris has a checking account balance of $1,000, a savings account value of $2,000 with a 2% interest rate, and a plot of land worth $49,000. Total net family assets are $52,000 (i.e., $1,000 + $2,000 + $49,000). Owners/management agents must list and show the actual value of each asset on the TIC because the net family assets are over the current HUD threshold amount, which is $51,600. The asset income amount of $40 ($2,000 x .02) from the savings account must also be listed on the TIC.

Important Key Steps: Because actual income cannot be determined on the plot of land and checking account, owners/management agents must impute income for the plot of land and checking account.

Total Imputed Income: $265

- $50,000 (checking account + plot of land) x .0045 (current passbook rate) = $225

- The $225 then must be added to the income from the savings account ($225 + $40) = $265. This amount will be listed on the OHFA TIC as asset income.

|