|

OHFA Releases a HOTMA Compliant TIC with NAHMA 8.0 Standards: What You Need to Know

On May 5, 2025, OHFA published a revised HOTMA TIC with the mandated NAHMA 8.0 standards. Due to these changes, there are many new categories including Event Types, Unit Identity, Non-Asset Income, Asset Income and HOME units (if applicable). This message will assist our partners in selecting the correct category and provides definitions to understand the meaning of each of the categories.

Note #1: Examples provided below are not exhaustive. If a category does not contain a definition or an example, it is because it is self-explanatory. Information on HOTMA assets, income, verifications and more can be found in OHFA's LIHTC Compliance Manual.

Note #2: OHFA has also developed Guidelines for a HOTMA Compliant TIC. The guidelines contain screenshots to aid in selecting each Event Type for each category. The guidelines can be found here.

| | |

Event Type

The following Event Types are changed or new as follows:

Select this for a Student Update, Rent Adjustment, Composition Change

Select this only if the project is a resyndication (i.e., project receives a second allocation of credits in the extended use period). Use this for in-place residents who are qualifying the unit.

| | |

The HOTMA TIC categories and definitions are as follows:

Employment Type

Select this if none of the other categories apply such as sporadic, seasonal and gift income.

Agriculture encompasses a wide range of professions, from traditional farming to specialized scientific and business roles. Some examples include farmers, farm managers, agronomists, veterinarians, food scientists, agricultural engineers, and agricultural economists. Other specialized fields include soil scientists, horticulturists, beekeepers and foresters. Within agriculture, there are also roles in sales and marketing (i.e., agricultural sales representative), education (i.e., agricultural science/management) and research.

Examples of business office jobs include administrative roles like receptionist, administrative assistant, and office manager, as well as customer service representative and accounting-related positions. Other examples include data entry clerk, account manager and marketing management roles.

- FTS – FT Student, No Special Conditions

This category means a member of the household does not meet any of the LIHTC student rule exceptions. Excess financial aid income should be listed here regardless of whether the household meets the LIHTC student rule exceptions or not.

- GS – Government/Public Service

Examples include law enforcement, emergency services, education, public health, and social services, as well as more specialized roles like budget analysts, city planners, and public health nurses.

- IM – Industrial/Manufacturing

Industrial manufacturing jobs involve tasks like operating machinery, assembling components, inspecting products and maintaining equipment.

- NS – Not Skilled/Unskilled

Unskilled professions generally involve jobs that require minimal specialized training or skills, often focusing on physical labor or basic administrative tasks. Examples include janitors, warehouse workers, fast food employees, delivery driver, cashier, food preparation worker or retail clerks/associates.

Skilled professions require specialized knowledge, training and experience to perform specific tasks. Examples include doctors, nurses, dentists, engineers, teachers, professors, lawyers, architects, mechanics and skilled trades like welders, plumbers, and electricians. These roles often involve complex tasks and require ongoing learning and adaptation to new technologies and techniques.

-

TP – Technical/Professional

Technical professions encompass a wide range of careers requiring specialized knowledge and skills in technology, engineering, or other technical fields. Examples include software development, data science, cybersecurity, web development and engineering roles. These roles often involve tasks like coding, designing, analyzing data or securing systems.

| | |

Income Type

- Adoption Assistance Payments

Money earned from the core activities of a business, such as selling goods or providing services. This includes distributed profits and net income from business, business owners, or self-employment.

Note: Dollar amount must only be what is received

- Distributions from a Retirement or similar account

Under HOTMA, retirement accounts recognized by the IRS ARE NOT considered assets under the HOTMA rule. However, distribution of periodic payments from retirement accounts is included as income. Retirement accounts include IRAs, employer plans, such as 401(k) or 403(b) plans and retirement plans for self-employed individuals.

Wages which are controlled by federal FSLA laws or a job with the federal government. This category does not include military pay.

General Assistance (GA) is a safety net program providing cash or voucher payments to individuals, especially adults without minor children, who have limited means and don't qualify for other cash assistance programs.

Note: Select this category if not using safe harbor or “means-testing” for income verifications. This category includes programs such as SNAP, WIC, HEAP, HWAP or other sources of income. Do not select for TANF as this source has its own category.

- Income From Assets Not Listed

Other asset income not included in the asset section of the TIC. It does not include retirement income.

An "Indian trust" refers to a legal system where the United States government holds land and assets in trust for the benefit of American Indian and Alaska Native tribes and individuals. Examples include trust lands, mineral rights and hunting and fishing rights held by the Department of the Interior.

Military pay includes basic pay, special and incentive pays, and allowances. Do not include a dollar amount for hostile fire payments.

Wages not subject to federal wage laws such as state government or privately owned businesses. This includes salaries, tips commission bonuses and other income from employment.

Non-wage income, also known as unearned income, is income derived from sources other than employment such as investments, rental income and assets. This category includes alimony or unemployment benefits or anything not defined in any of the other categories.

Examples are veterans pensions, military retirement and income from all other pensions.

- Safe Harbor Income Source

Under HOTMA, in lieu of conducting their own income calculations, owners/management agents may rely on an income determination completed for another Safe Harbor "means-tested” form of federal public assistance within the previous 12-month period.

Note: Select this category ONLY if the owner/management agent is using Safe Harbor as income verification. OHFA’s Safe Harbor Income Verification form must be used.

-

Supplemental Security Income

Includes SSI and state programs administered by the Social Security Agency

Temporary Assistance for Needy Families

| | |

Income Verification

- Copy of Benefits/Payment Check

A common example of a benefits payment or check is a check from an employer for retirement plan contributions, employer-paid insurance premiums or government provided benefits such as SS. This could also be an Explanation of Benefits (EOB) document from a health insurance provider, outlining payments made for medical expenses.

- Bank/Trustee Verification

- Check Stubs/Earning Statement

Income cannot be verified. Select this category when a tenant/applicant provides a sworn statement or affidavit.

Select this for anything that is not included in the other categories/selections.

- Payer/Benefactor Affidavit

This document describes the asset and the value or income source from the asset at the time of asset transfer.

- Benefits Provider Verification

Select this category to verify a Health Reimbursement Arrangement (i.e., HRA, Health Savings Account, or Flexible Spending Account.

Note: Amounts received by the family specifically for, or in reimbursement of, the cost of medical expenses for any family member is excluded from income.

- Separation/Divorce Settlement

-

Tax Returns – Individuals

| | |

Asset Type

- Cash/Demand Deposit Accounts

A demand deposit account is a type of bank account that allows the account holder to withdraw funds at any time without prior notice or penalty. These accounts are typically used for everyday transactions and include common types like checking accounts and savings accounts.

Marketable securities are financial instruments, like stocks, mutual funds, annuities and bonds, that can be easily bought and sold in the market.

Jewelry used in religious/cultural celebrations and ceremonies (i.e. wedding ring) is Necessary Personal Property (NPP).

Note: NPP is not included in the value of net family assets.

Jewelry that is expensive without religious or cultural value or which does not hold family significance is Non-Necessary Personal Property (NNPP).

Considered NNNP

Considered NNNP

Considered NNNP

- Lump Sum Receipts (i.e., lottery winnings) (Not income)

Excluded from net family assets.

Note: Periodic lottery winnings are included as income.

- Trust/Available Principal

Select this for any asset type not listed in any of the other categories/selections.

| | |

Asset Type

- Non-Necessary Personal Property (NNPP)

Excluded from net family assets when the amount is equal to or less than the current HUD asset threshold (adjusted annually for inflation).

- Real Property Suitable for Occupancy

Included in net family assets. Includes land or a home.

Select this for real property not suitable for occupancy or property in which the family does not have legal authority to sell such property. In this case, the real property is excluded from the cash value of net assets.

- Federal Tax Refund or Credit

For a period of 12 months after receipt by the household, the tax refund/credit amount must be subtracted from the total net family assets regardless of where the amount is deposited. Reference pages 125-126 of OHFA’s Compliance Manual for further information on tax refunds.

| | |

Asset Income Type

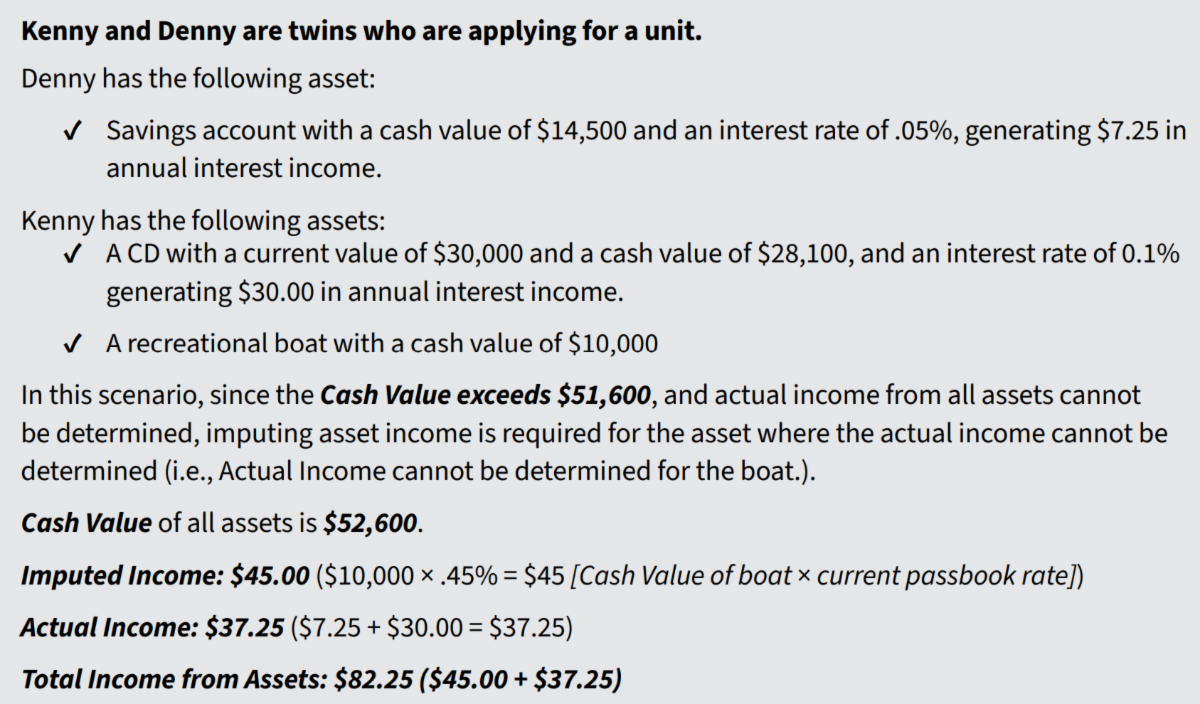

Imputed income must be calculated for specific assets, not all assets, when three conditions are met:

- The value of net family assets exceeds the current HUD asset threshold (adjusted annually for inflation).

- The specific asset is included in net family assets; and

- Actual asset income cannot be calculated for a specific asset. Following is an example:

| | |

Actual income is the real money generated by assets (i.e., interest payments).

| | |

Asset Status

Select if the household currently owns or holds the asset

Select if the household has divested or disposed of the asset. If an asset is disposed of for less than fair market value (FMV), the asset must be included for two years from the date of disposal.

| | |

Asset Verification Source

A legally binding statement, similar to a financial affidavit, but specifically prepared and verified by an accountant. It verifies the accuracy of financial information.

Legal document that verifies a person’s relationship with a financial institution, includes name, financial institution, amount owned and interest

- Account/Earnings Statement

A bank account statement or an earnings statement (a financial report that summarizes a revenue, expenses, and resulting net income (profit) or net loss over a specific period).

- Published Market Standards

A class of securities, a marketplace on which the securities have traded that discloses, regularly in a publication of general and regular paid circulation or in a form that is broadly distributed by electronic means. The prices at which those securities have been traded. An example is if the household owns stock.

Income cannot be verified. Use this category when a tenant/applicant provides a sworn statement or affidavit.

Select for a verification that does not fall in any of the other categories/selections.

A legal document signed by the seller of a particular property and provided to the buyer and title company that provides proof of ownership of said property and provides factual information with regards to the legal status as it pertains to bankruptcy, liens, agreements or judgments against the property.

An appraisal document prepared by a qualified appraiser in accordance with generally accepted appraisal standards.

| | | | |