The quarterly inflation adjustment for all OAS benefits (including the guaranteed income supplement) is based on the difference between the average CPI for two periods of three months each:

- the most recent three-month period for which CPI is available, and

- the last three-month period where a CPI increase led to an increase in OAS benefit amounts.

The payments starting in the first quarter of 2023 were indexed by 0.3%, bringing the total increase for the year to 7.0%.

The decision on when to begin taking OAS involves factors such as employment and other income, life expectancy and inflation. We’ll use three case studies to examine the choice.

If only Sam had known

Sam, 70, met the qualifications for automatic OAS enrolment: he had a Canadian address, had participated in the CPP for 40 years or more, and had been approved for CPP. Service Canada advised him that his OAS payments would start in December 2017, the month after he turned 65. Unfortunately, Sam didn’t know he could defer his OAS. In December 2017, he automatically received his first payment of $585.49. He continued to work and most of his OAS was clawed back.

Had Sam deferred his OAS for the maximum five-year period, he could have received $932.28 (the maximum of $685.50 for the fourth quarter of 2022, increased by 36%) as his first payment. Since he’s now retired and no longer receiving employment income, there would have been no clawback. And Sam would have been paid this higher amount, adjusted each quarter for inflation, for life.

Understandably, he’s unhappy that he hadn’t given due consideration to the deferral option.

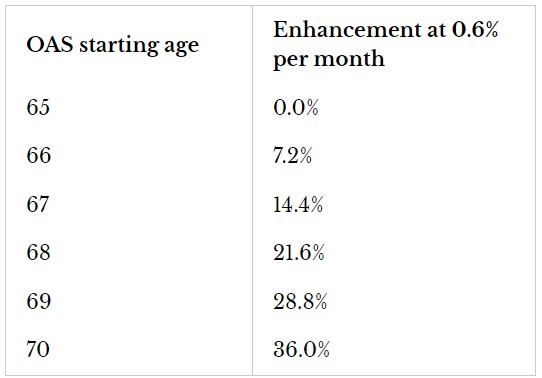

Not only is there an enhancement for each month of OAS delay — it’s the inflation-adjusted amount that’s enhanced, making the amount received at the later date even larger. Had Sam deferred his start for the maximum period, his initial payment would have been 59.3% larger: $932.28 versus $585.49.

Canadians have been able to defer their OAS since 2013. Surprisingly few do so: only 4% of the first cohort, according to CRA data for the 2014 to 2018 taxation years. The average length of deferral was 23 months. One-third deferred for one year or less, and more than 60% for two years or less. Only 20% deferred for two to three years, while the remainder deferred for more than three years.

As expected, most of those who deferred had — like Sam — either continued to work or had high incomes.

Unfortunately, many retirees underestimate their life expectancies in determining when to start OAS (and CPP/QPP) benefits. The CPP’s most recent actuarial valuation estimated the average life expectancy for a man born in 2019 is 80.0 and 84.6 for a woman.

According to the 2014 Canadian Pensioners’ Mortality Table, a man who lives to 65 has a 50% probability of reaching 89, a 25% probability of living to 94 and a 10% probability of celebrating his 97th birthday. For women, the equivalent ages are 91, 96 and 100. (Note that members of pension plans generally outlive the broader population.)

Another case study shows the value of deferring OAS.

Karl’s patience pays off

Karl is retired and quickly approaching his 65th birthday. He is debating whether to start OAS at 65 (January 2023) or to defer until he’s 70. Karl has met the 40-year requirement and therefore is entitled to maximum OAS.

He is also aware that the government will increase his OAS benefits by 10% at 75. If he delays his OAS, the 10% increase is based on both the enhancement and inflationary increases.

Someone receiving the maximum OAS in 2022 would have received approximately $7,929. This works out to an average monthly OAS benefit for the year of approximately $660. We will assume that monthly average OAS payments will increase by 5% for 2023, and thereafter by the Bank of Canada’s 2% target inflation rate.