|

Win $50!

|

|

There are two member numbers spelled out within the text of this eNewsletter. Find your number and give us a call at (888) 387-8632 to claim $50!

|

|

|

|

|

Learn about mortgages from a hermit crab!

|

President's Corner President's Corner

|

Sometimes, life imitates art. A good example comes from the 1986 movie classic, Ferris Bueller's Day Off. The following represents several scenes combined of a high school history teacher (played by Ben Stein, who is still a frequent commentator on political and economic issues as well as an actor, lawyer, and writer) trying to explain tariffs to an obviously bored class:

In 1930, the Republican-controlled House of Representatives, in an effort to alleviate the effects of the - anyone, anyone - Great Depression, passed the - anyone, anyone - the tariff bill, the Hawley-Smoot Tariff Act, which - anyone - raised or lowered - anyone - raised tariffs in an effort to collect more revenue for the federal government. Did it work? - anyone, anyone know the effects? It did not work, and the United States sank deeper into the Great Depression.

Dartmouth College economist Doug Irwin noted on a recent episode of NPR Morning Edition the Hawley-Smoot Act was originally written to protect farmers, but other industries jumped on the bandwagon to protect their products. More than 1,000 economists signed a public statement arguing against the Hawley-Smoot Bill, but to no avail. Other countries levied their own tariffs. The result was a significant drop-off of global trade, massive worldwide unemployment, and ultimately Senator Smoot, Congressman Hawley, and President Hoover being voted out of office in 1932.

Before the federal income tax was instituted in 1914, tariffs were the greatest source of revenue for the federal government. The myriad of tariffs imposed in American history came with generally the same justifications we are hearing today from Washington, D.C. - protect certain industries from cheaper products flooding our markets from foreign countries. One notable situation was President Lyndon B. Johnson's retaliatory tariff in 1964 against then West German Volkswagen vans to offset their tariff of U.S. chicken. According to a 1997 New York Times article, President Johnson cut a deal with the United Auto Workers to support his civil rights platform in exchange for the Volkswagen tariff. Once again, politics trumps economic reality.

U.S. Commerce Secretary Wilbur Ross was quoted earlier this year saying tariffs actually level the playing field, especially in industries "plagued by excess capacity, which led to dumping, led to displacement of domestic markets, led to all sorts of bad things."

Tariffs have led to bad things like decreased imports resulting in higher prices for consumers, loss of jobs, and the decline in the U.S. dollar. More often than not, tariffs have become the precursor to economic recessions and depressions.

The logical answer to tariffs would be free trade which is the complete absence of import restrictions such as tariffs and quotas and of export subsidies. In theory, all countries would be trading on a level playing field. A pure trade system with no tariffs, no quotas, no subsidies, and no politics sounds great in theory, but until it has been tested, we will never know if it works.

Until then, we will just be talking to ourselves, not unlike Ben Stein's character when he was calling the class role. Bueller...Bueller....Bueller....Bueller.

David M. Green

President/CEO

(925) 335-3802

|

Stat of the Month

|

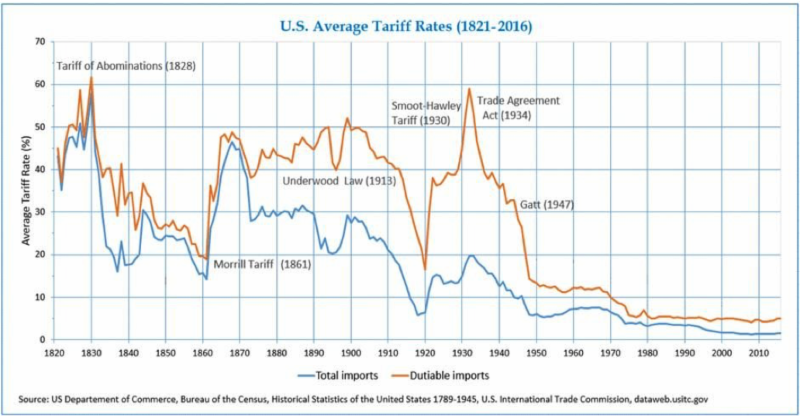

U.S. Average Tariff Rates 1821-2016

This chart traces the amount of imports and durable imports over the last 95 years. Durable goods include business machinery, automobiles, appliances, and big-screen TVs. Demand for durable goods are more volatile than other goods such as food and gas because purchases can be delayed when consumer funds are tight. Tariff rates have been declining since the Great Depression in the 1930s in order to reignite the U.S. economy. Typically, when tariffs are low, imports are higher because the probability that American consumers will buy both durable and nondurable goods is higher. An increase in tariffs increases the cost of the product to the consumer and will eventually slow down demand.

|

Credit Corner

|

|

According to the National Association of Realtors 2018 Home Buyer and Seller Generational Trends

report, 34% of all home buyers are first-time buyers. In addition, 65% of those first-time, would-be homeowners are under the age of 37.

Don't shop without a pre-approval:

Having your cash (down payment and closing costs) ready and a pre-approval letter from a lender gives you an advantage when offers are submitted to the seller. To stand out among other offers, you might want to include your own letter as to why you feel you would be the best buyer.

Make sure you get inspections:

Trying to save a few hundred dollars for an inspection now can cost you thousands later. This is your opportunity to discover any potential problems with the home before you buy.

Don't change jobs or make any other financial moves:

It's not over until the closing is done. Lenders will look at your credit just before closing to make sure your financial situation hasn't changed. Wait until you have those keys in your hand before making any big purchases or career moves.

Research the neighborhood:

Check the web for proximity

to criminal activity. Find out about the local schools. Drive by the home at different times of the day (and night) so you can see what kind of activity is going on in the neighborhood. Broken down cars on the street? Bars on windows? Or just too much traffic passing by? The price may be right, but the location may be all wrong. Your home is a huge financial and emotional commitment and should be a peaceful, pleasurable place to go to at the end of your working day.

Lastly, banks are often willing to pre-approve you for more than you think you can afford. Stick to your gut and only shop in the price range that YOU feel comfortable in. Only you know your lifestyle and true expenses. Don't become trapped in higher house payments, unable to take a weekend trip or go to dinner whenever you want.

A house is a 30-year commitment... make sure you will be comfortable in that home, with those payments over the long haul!

Our Credit Union will listen to your needs and can offer great advice about this serious financial move.

(925) 335-3870

|

New Branch Coming Soon!

|

We are pleased to announce that we will be opening a new Pittsburg/Antioch branch this Summer in the Pittsburg Century Plaza, next to Target. In the interim, please feel free to visit our branch at 1870 A Street in Antioch, or any of our other branch locations.

(SEVEN ZERO ZERO TWO THREE NINE EIGHT)

|

1st Alerts

|

- If you have @ccessOnline Home Banking with us, simply transfer a payment to your Visa card. Setting up a regular payment using Bill Pay in @ccessOnline Home Banking will generate a check and that will delay your payment. Instead, you can set up a single or recurring transfer. A transfer is immediate.

|

1st in the Community

|

Animal Shelter Donation Drive

We want to extend a huge thank you to our membership and all those involved for your donations to our 2nd Animal Shelter Drive.

The employees at the Animal Services of Contra Costa County and 1st Nor Cal are so grateful for your generous support and gifts.

Pictured here are 1st Nor Cal employees, Jennifer, Kristina, and Juliet while making the drop-off at the animal shelter.

|

Car Buying Tips

|

Check out these car buying tips before you start shopping!

- Do your research before you walk into the dealership.

- Used cars have a Kelley Blue Book value. Visit www.kbb.com before you go to the dealer.

- Use Autocheck or CarFax to check out the car.

- Negotiate on the value of the car/truck, not the monthly payment.

- For the best value, instead of a new car or truck, buy used with low mileage.

- Never pay "sticker price". Everything is negotiable!

- Know your credit score and demand the best interest.

*Annual Percentage Rates (APR) are subject to change. Rate, maximum term, maximum loan amount and advance amount are based on credit qualifications. Maximum terms vary based on loan amount. We reserve the right to determine collateral value based on industry recognized guidelines or full appraisal. Must be 18 years old or older to apply for a loan. Loans are subject to all Credit Union policies and procedures. Auto loan at 3.20% APR requires a minimum FICO® 750 Credit Score. 72 months term at 3.20% APR is $15.29 per $1,000.00 borrowed.

|

Tips for Teens

|

Use Direct Communication to Save on Frustration

The year is 2011. The iPhone 4S made its debut, Adele was slaying Billboard's hot 100 with "Rolling in the Deep", and I was given my first cell phone as I moved from elementary into middle school. It was a Motorola Razer, capable of withstanding drops with its scratch/crack anxiety proof screen, and equipped with a battery life lasting days, not hours. It also lacked emojis, but made up for it with cool emoticons. Like all phones, it served its purpose. Well, at least until it was eventually retired. I sent it into solitary confinement until I needed to use it again while my newer phone was in repair. Moto's Razer was made before apps became mainstream, so I had to go back to no Instagram or Snapchat. It also meant telling my friends to dust off their SMS app and get used to seeing green in iMessage for the foreseeable future. As for me, I had to get used to using :) instead of the smile emoji again.

Communication since then has come a long way, getting more and more advanced as time goes on. Recently Google announced Google Duplex, an addition to their Google Assistant that is capable of placing phone calls on the user's behalf to schedule hair appointments, reserve a table at a restaurant, or check to see if a business is open during a holiday. In other words, Google Duplex calls businesses and talks with live people for you to accomplish simple tasks with no human intervention necessary. Unless, of course, it absolutely can't figure out how to solve an unforeseen issue, such as a random question not pertaining to the nature of the call or a logical error.

Google Duplex proves that human interaction is necessary. Effective communication is at the center of everything we do, but communication can be complex. The use of body language (i.e. facial cues and hand movements) and auditory cues (i.e. tones, pitch, force) facilitates the expression of what it is we're trying to convey, which can be lost when we use text. According to a 2014 survey by the Pew Research Center, 75% of teens connect with a close friend either by text or social media while only 10% connect though a phone call (Pew Research Center Teens Relationships Survey). In other words, as more communication happens over text, the more important it becomes to effectively convey the meaning and intent of our message. How many times has a text gone south because it was misread or misinterpreted?

Taking the time to stop and think about the most straightforward way of phrasing something is key to avoiding mishaps. Sometimes, we as the audience can't understand the author's intent, so we have to make assumptions based on the contextual clues. Rather than making the audience assume the intent, it's okay to take a stand and express an opinion directly; this incites debate and conversation which ultimately leads to a broader understanding of a topic. Oh, and don't forget to use emojis in text messages to help express the tone a little better.

When in doubt, just say what you need to say. It will make more sense then beating around the bush.

Happy Emoji Day and RIP Toys R Us.

Luis Dominguez

Student Social Media Intern

1st Nor Cal Credit Union

|

Insurance Tips

|

Should you buy Rental Car Insurance?

It's vacation time!

If your plans include renting a car, it's a good idea to determine whether or not you need to purchase any additional coverage before you are at the rental agency counter so that you can make an informed decision.

Generally, if you are renting in the U.S. or Canada most insurers will offer you the same liability coverage as you have on your own policy. This coverage extends to all covered drivers listed on the policy and the rental contract as drivers. If you are renting a car outside of the U.S. or Canada, you should purchase insurance with the rental as a standard auto policy does not provide any coverage for damage, loss, or liability in Mexico or around the globe.

When it comes to comprehensive and collision, if you carry this coverage on your regular auto policy, typically the coverage and deductibles would also apply to the rented car. It is important to note that there are some things that probably won't be covered by your regular auto policy, such as Loss of Rental Income (could be as much as $50/day for each day that the vehicle not available for rental), Loss of Value or Administrative fees that the car rental agency may charge you.

A note on specialty rentals: There is rarely liability, collision or damage coverage provided by your Auto policy on Motor Homes, Moving Vans or large Trailers. It would be wise to evaluate what the rental agency offers and make the choice to purchase that coverage.

Don't get surprised after the fact - always check with your agent or company to verify coverage before you rent. It is also worthwhile to check with your credit card company because some credit card companies extend coverages on a rental vehicle as an extra perk. Keep in mind that you have to use that card to pay for the entire rental.

As an added benefit of your 1st Nor Cal membership, we at Lou Aggetta Insurance will help you review the things that are important to you and provide you with options for reducing risk in your life. We are an independent insurance agent and can provide you with home, auto, life, health, business, and many other types of insurance coverage.

Contact us today to schedule your free review.

Denia Aggetta Shields

Lou Aggetta Insurance, Inc.

2637 Pleasant Hill Road

Pleasant Hill, CA 94523

(925) 945-6161

|

Catch-Up Retirement Contributions

By Jason Vitucci, CFP® & Gene A. Schnabel

A recent survey found that 17% of people were very confident about having enough money to live comfortably through their retirement years. At the same time, 36% were not confident.2 Congress in 2001 passed a law that can help older workers make up for lost time. But few may understand how this generous offer can add up over time.3

The "catch-up" provision allows workers who are over age 50 to make contributions to their qualified retirement plans in excess of the limits imposed on younger workers.

How It Works

Contributions to a traditional 401(k) plan are limited to $18,500 in 2018. Those who are over age 50-or who reach age 50 before the end of the year-may be eligible to set aside up to $24,500 in 2018.4

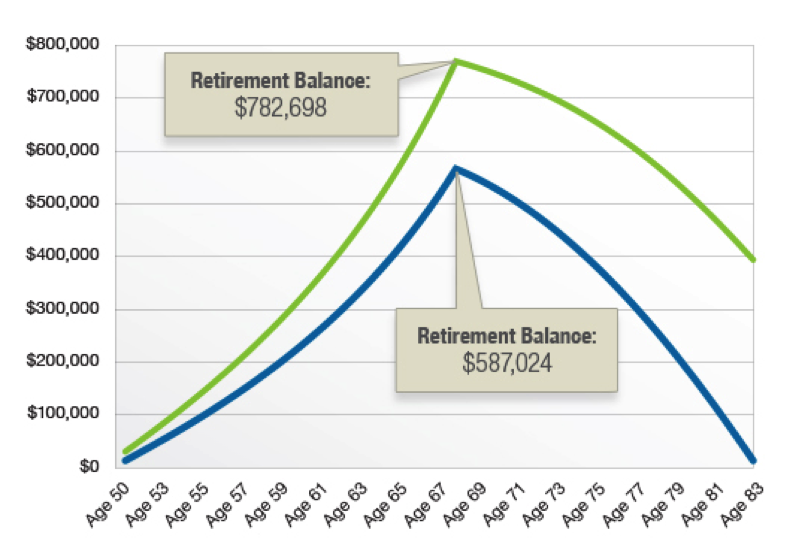

Setting aside an extra $6,000 each year into a tax-deferred retirement account has the potential to make a big difference in the eventual balance of the account. And, by extension, in the eventual income the account may generate. (See accompanying illustration.)

Catch-Up Contributions and the Bottom Line

This chart traces the hypothetical balances of two 401(k) plans. The blue line traces a 401(k) account into which the maximum regular annual contributions are made each year, but no catch-up contributions. The green line traces a 401(k) account into which the maximum regular and full catch-up contributions are made each year.

Upon reaching retirement at age 67, both accounts begin making payments of $4,000 a month.

The hypothetical account without catch-up contributions will be exhausted by the time its beneficiary reaches age 83.

If you have concerns about how you'll fund your retirement, and if catch-up contributions make sense for you, then please feel free to contact us. We help our clients navigate through the confusing maze of financial issues as it relates to retirement planning. If you feel that we may be a good fit to work together, please don't hesitate to contact our office. As a valued 1st Nor Cal member, we invite you to contact us for a complimentary financial analysis. We also invite you to attend any of our Retirement Planning workshops that we hold. For more information about our practice, or to make an appointment, please call us at (925) 370-3750 or visit our website at www.vitucciintegratedplanning.com.

Vitucci Integrated Planning

Securities through First Allied Securities, a registered broker dealer, member FINRA/SIPC. Advisory services offered through First Allied Advisory Services, Inc. Registered Investment Advisor. Investments not FDIC or NCUA/NCUSIF insured, not insured by Credit Union, may lose value. Products offered are not guarantees or obligations of the Credit Union, and may involve investment risk including possible loss of principal.

1st Nor Cal CU, Bay Area Retirement Solutions and First Allied are all separate entities.

Jason Vitucci CA

Insurance Lic.: 0F59894, Gene A. Schnabel CA Insurance Lic.: 0663016

The image is a hypothetical example used for comparison purposes and is not intended to represent the past or future performance of any investment. Fees and other expenses were not considered in the illustration. Actual returns will fluctuate.Both accounts assume an annual rate of return of 5%. The rate of return on investments will vary over time, particularly for longer-term investments.Contributions to and withdrawals from both accounts have been increased 2% each year to account for potential 2% inflation.Distributions from 401(k) plans and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions.

2

:

EBRI, 2018 Retirement Confidence Survey

3:

Economic Growth and Tax Relief Act of 2001

4: IRS, 2018. Catch-up contributions also are allowed for 403(b) and 457 plans. Distributions from 401(k) plans and most other employer-sponsored retirement plans are taxed as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Generally, once you reach age 70½, you must begin taking required minimum distributions.

|

FREE Financial Counseling

|

Are you in need of financial counseling?

1st Nor Cal is here to help. Timely and honest debt advice is available to our members at no cost or obligation. Learn how to manage your finances.

Make your appointment TODAY!

Just a reminder, you can annually request FREE Credit Reports from all 3 credit reporting agencies online by going to:

For FREE Financial Counseling, don't hesitate to contact:

Shelley Murphy

Senior Vice President of Lending & Collections

(925) 228-7550 Ext.824

(EIGHT ZERO ZERO NINE)

|

Did you know we're on Social Media?

|

|

|