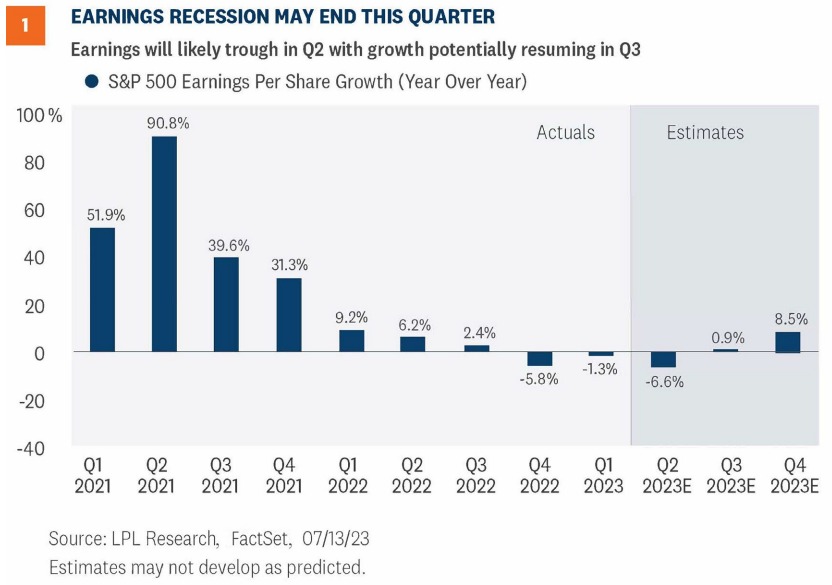

INDICATORS POINT TO SLIGHTLY ABOVE AVERAGE SURPRISE

To get a sense for whether results might diverge from that baseline expectation, we look at several factors that have correlated with earnings surprises historically:

1) Pre-announcements. So far, about 41% of S&P 500 companies providing second quarter guidance have issued positive guidance, in line with the five-year average but higher than the 10-year average of 36%. This points to a typical beat.

2) Early reporters. The average upside surprise for the 30 S&P 500 companies that have reported is 9%, with a 77% beat rate. This relatively strong start points to a modestly bigger-than-average beat.

3) Estimate trends. The consensus second quarter EPS estimate for the S&P 500 fell 3% during the quarter, slightly better than the five and 10-year averages of -3.4% and pointing to slightly above average surprises

4) Economic surprise indexes. Whether looking at Citi’s version or Bloomberg’s, these popular measures of the frequency with which economic data beats expectations have both surged recently to historically high levels, pointing to an above-average beat.

5) Manufacturing activity. This indicator points in the other direction. The Institute for Supply Management (ISM) Manufacturing Index averaged 46.7 during the second quarter, signaling earnings weakness. An earnings decline is consistent with this indicator and widely expected, and the economy has become increasingly services driven, so we would only slightly lower earnings expectations relative to consensus based on this one data point. Also note earnings beat by more than 5% last quarter when the ISM reading averaged 47.1.

ENERGY IS THE KEY DETRACTOR

From a sector perspective, the energy sector is projected to detract the most from earnings growth, with consensus estimates showing a 48% decline in profits amid the significant drop in oil prices over the last year. Conversely, the consumer discretionary and communications sectors are the only two sectors projected to record double-digit earnings growth (27% and 13%, respectively). The big names in consumer discretionary (Amazon/AMZN) and communications services (Meta Platforms/META and Alphabet/GOOG/L) are responsible for the majority of the anticipated earnings growth in these sectors. At the industry level, entertainment, hotels, restaurants and leisure, and wireless telecom are also expected to be material contributors.

FUNDAMENTALS MATTER

As valuations in the market remain fairly rich by most accounts, and interest rates—though inching lower as the Federal Reserve (Fed) prepares to potentially stand down—are still elevated, there are concerns the market won’t be able to absorb earnings misses as well as they have when valuations were more reasonable.

Accordingly, focusing on fundamentals will be more important during this earnings season as analysts will examine results from the top down and the bottom up amid questions about the effects of disinflation on the top line and margin pressures on the bottom line.

FOCUS ON GUIDANCE

Corporate guidance, which looks ahead and provides a glimpse of what it sees with regard to the broader economy, coupled with insights regarding specific customer trends, will allow the market to form an educated judgment of where the economy is headed. Here are some things to watch during earnings season to help leverage these insights:

The macro picture. Given the focus on whether or not the economy is poised for a recession later this year, there will be an inordinate focus on how companies characterize the behavior of their primary customer base. This applies to both retail customers and corporate clients across a broad spectrum of industries.

Banking environment. In terms of the banking sector, the data that is provided on loan growth and loan payments can help assess the health of the broader economy. Similarly, credit card information offers an important profile on consumer debt and overall payment issues. Typically, large money center banks offer a general assessment of economic conditions, while smaller and regional banks provide a more in-depth examination of the economic landscape from their respective locations. Together, analysts can form a more reliable perspective on the health of the economy. Favorable comments about the lending environment from JPMorgan Chase (JPM) and Wells Fargo (WFC) in their earnings releases last week were reassuring.

Cost-cutting trends. Investors will be on alert for indications that companies need to cut costs in order to maintain their operating margins, because this typically involves trimming payrolls. With a still resilient labor market underpinning the consumer, any signs that companies need to reduce headcount could adjust projections for a marked economic slowdown or a recession.

With consumer spending responsible for approximately 68% of GDP, corporate guidance is increasingly important during this period.

LOOKING AHEAD TO THE SECOND HALF

As we noted in the Midyear Outlook 2023: The Path Toward Stability released last week, we expect earnings to decline slightly this year. But analysts have continued to underestimate corporate America’s ability to generate revenue and control costs. Even though inflation is coming down, higher prices boost revenue and consumers continue to absorb elevated prices relatively well. In addition, S&P 500 companies saw an unexpected, albeit slight, uptick in margins overall in the first quarter, suggesting additional pressure on margins may be limited. Also encouraging is consumer inflation, though falling, is well above wholesale inflation. Expect companies to use their efficiency playbooks in the second half to continue to mitigate margin compression from waning demand and lingering cost pressures.

For now, given heightened economic uncertainty, we use a weighted probability approach to forecast earnings for this year. Based on estimated probabilities of these scenarios, as shown in Figure 2, we arrive at our 2023 S&P 500 earnings per share forecast of $213, slightly below 2022 levels. Though the market’s expectations for earnings have improved of late, we still see sufficient pessimism to support modestly higher stock prices if actual results come in near our bull case “soft landing” scenario. But the bar has been raised.