|

Aaron Scheuer

803.540.7729

|

|

|

|

|

HSB Insider's Perspective: The Impact of High Millage Rates

By Gary Morris

Many communities are having to increase millage rates in order to fund essential services. The millage rates across the state generally range from 250 mills to over 500 mills. If a property is located within a municipality, the municipal millage is added to the county millage. As a result, the millage in some communities may even exceed 600 mills. To put this in perspective, the annual tax bill for a $1 million investment in a commercial real estate venture could range from $15,000 (250 mills) to $36,000 (600 mills). This is a substantial difference. For larger investments, the difference would be even more substantial.

There are a variety of reasons for the increase in millage rates. Growth in the commercial or industrial base may be stagnant or decreasing. Some communities have numerous tax-exempt properties (i.e., government offices, university facilities, and non-profits). The result is that, for whatever reason, these communities do not have a sufficient commercial and industrial base to support the tax burden created by the services provided by such communities. In such cases, these communities may lose the competitive edge to attract commercial or industrial businesses unless they are able to grant incentives to induce such commercial or industrial enterprises to locate in the community.

Property tax incentives are routinely granted to manufacturers, but many communities are adverse to granting incentives to commercial enterprises. The problem is that developers and commercial owners are now paying more attention than ever before to property tax burdens. If property taxes are too high, it may not make sense for a developer or commercial owner to build or locate a facility in that community.

So what is the answer? It is a tough call, but I believe communities will need to reduce spending or increase incentives to both commercial and industrial projects until such time as the millage rates become more reasonable.

|

General Assembly Overrides Veto of Economic Development Legislation

In a special legislative session earlier this month, the SC General Assembly overrode the Governor's veto of S.1043. Among the provisions contained in the bill are an extension of the sunset date for abandoned building tax credits, a new tax credit program for agribusinesses, and an expansion of SC's job development credit (JDC) program. Below is a brief summary:

Abandoned Buildings Credit

The legislation extends the credit's sunset date by two years to December 31, 2021; increases the credit amount available for rehabilitating certain historic structures for commercial apartments; and broadens the credit's carryforward and allocation provisions.

Textile Mill Credit

The legislation expands the area of the textile mill site for certain textile mills located in economically distressed areas. The credit now excludes rehabilitation expenses that increase the square footage of existing buildings by more than 200%.

Historic Structures Credit

The legislation broadens the credit's carryforward and allocation provisions.

New Agribusiness Tax Credits

The legislation establishes a tax credit program for agribusinesses that increase purchases of products certified as South Carolina-grown by a minimum of 15 percent per year to claim an income tax credit or employee withholding credit in an amount determined by the S.C. Coordinating Council for Economic Development. The base year total dollar purchases that are certified as South Carolina-grown must exceed $100,000 for a taxpayer to be eligible.

Expansion of Job Development Credit

The legislation modifies SC's job development credits (JDCs) program, reducing the job and wage thresholds applicable to qualified service-related facilities for the highest three tiers. The new law also allows businesses engaged in legal, accounting, banking or investment services and certain retail businesses to apply for JDCs.

The new legislation can be found

here. For more information on the new legislation, please contact a member of HSB's ED team.

|

Opportunity Zones: Investors Eagerly Await Guidance

South Carolina investors are anxious for the U.S. Treasury Department to issue regulations clarifying many aspects of the new Opportunity Zone program. As we previously

highlighted, t

he Opportunity Zone tax incentives present tremendous opportunities for tax savings for taxpayers who are able to qualify for the incentives. However, much uncertainty remains regarding how to make qualifying investments, and investors and tax professionals alike are hoping the regulations will provide the needed guidance. Once the guidance becomes available, HSB will be holding a series of seminars to discuss in more detail how the Opportunity Zone program will work.

|

General Assembly Passes Tax Conformity Bill

In a special legislative session earlier this month, the SC General Assembly passed a tax conformity bill adopting the Internal Revenue Code (IRC), as amended through February 9, 2018. This year's conformity legislation took longer than usual due to the significant changes made to the IRC last December under the Tax Cuts and Jobs Act (TCJA). South Carolina adopted substantial portions of the TCJA. A few notable TCJA provisions not adopted include:

- IRC § 199A deduction for qualified business income;

- IRC § 118(b)(2) taxable contributions to a corporation by a governmental entity;

- IRC § 163(j) interest expense deduction limitation; and

- Various foreign tax provisions.

In addition to conformity provisions, the legislation also provides for full inflation adjustments for SC's income tax brackets (previously SC's brackets were adjusted at 50% inflation) and an additional state dependent exemption. The full conformity bill can be found

here.

|

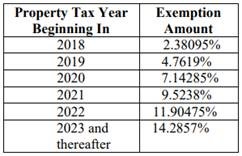

SCDOR Publishes Ruling on Manufacturers Property Tax Liability Abatement

The South Carolina Department of Revenue recently published SC Revenue Ruling #18-13 dealing with the abatement of certain property tax liability for manufacturers under

SC Code 12-37-220(B)(52). This partial exemption can apply to:

- Non-FILOT manufacturing property (not utility property) which is used "in the conduct of the business of a manufacturer," including M&E, office equipment, computers and real property;

- Existing and new property;

- Property that is subject to Special Source Revenue Credits but not a negotiated FILOT;

The partial exemption will be phased-in according to the chart copied below, and should be applied automatically when a company files a PT-300. However, companies should check their assessment notices and tax bills carefully to ensure that the exemption is being properly applied. Contact a member of the HSB Tax or ED team if you have any questions regarding the exemption.

|

SCDOR Issues Final Wayfair Sales and Use Tax Guidance for Remote Sellers

SCDOR has issued final guidance implementing the Department's final sales and use tax nexus standard and rules for remote sellers with no physical presence in the state. The ruling provides generally that a remote seller whose gross revenue from sales into South Carolina exceeds $100,000 in the previous or current calendar has "economic nexus" with South Carolina. Effective November 1, 2018, remote sellers with economic nexus must begin collecting and remitting sales and use taxes on their taxable sales into South Carolina. The ruling provides important guidance for remote sellers including calculation of the $100,000 economic nexus standard, sales through an online marketplace (e.g. Amazon), registration with SCDOR, and remittance of the tax.

S.C. Revenue Ruling #18-14 (September 18, 2018).

SCDOR also issued updated guidance to clarify that remote sellers with economic nexus must collect any applicable local sales and use taxes administered by SCDOR. The updated ruling includes general information on the various local sales and use taxes administered by SCDOR and provides rules and guidance regarding collection and remittance of these taxes.

S.C. Revenue Ruling #18-15 (September 20, 2018).

For questions regarding sales and use tax compliance after Wayfair, please contact a member of HSB's tax or economic development team.

|

|

|

| Photo credit: Business Facilities |

Congratulations Team SC

Governor McMaster recently accepted Business Facilities' 2017 State of the Year Award on behalf of the state of South Carolina. The award, first announced in February of this year, is based on BF's evaluation of South Carolina's economic development strategy and the economic impact of the top projects the state secured in 2017. Commitments from Volvo and BMW strengthened South Carolina's automotive industry, but BF Editor in Chief Jack Rogers also pointed to the state's commitment to a diversified portfolio. View the full story

here.

|

Johnson Recognized as "Economic Development Lawyer of the Year"

Congratulations

to our own

Will Johnson

on being named the 2019 Economic Development Law Lawyer of the Year-Columbia, SC

by

Best Lawyers®, a legal peer-review guide. Congratulations

to our own

Will Johnson

on being named the 2019 Economic Development Law Lawyer of the Year-Columbia, SC

by

Best Lawyers®, a legal peer-review guide.

Only a single lawyer in each practice area and designated metropolitan area is honored as the "Lawyer of the Year," making this accolade particularly significant.

HSB ED team members Frank Davis, Gary Morris and Ben Zeigler were also listed in

The Best Lawyers in America©. Overall, HSB had 10 attorneys named "Lawyer of the Year" and 60 listed in

The Best Lawyers in America

©.

Click here for the full release.

|

HSB News & Press

Southern Business and Development has named

Haynsworth Sinkler Boyd one of the "

best economic development law firms in the South" in their 25th Anniversary issue. We are very proud of the work we do to help Team South Carolina bring jobs and investment to our state. It's a great place to live, work and play.

Perry MacLennan

recently spoke at the International Association of Young Lawyers Conference (AIJA) in Turin, Italy on the "Do's and Don'ts For Business Visitors" focusing on how foreign companies can utilize the B-Visa Program for their workers that need to travel to the United States for certain purposes such as negotiating contracts, training and more.

Philip Land's article on the "Exclusion from New Tariffs on Chinese Goods" was recently published in the International Tax Newsletter of the Geneva Group International.

Click here to read the article.

|

Employment Law Seminars

HSB will host our annual

Employment Law Seminars

beginning October 23 in Charleston. Additional locations include Columbia (10/24), Myrtle Beach (12/4) and Florence (12/5). Topics include:

-

Implementing a Different Approach to Harassment & Discrimination in the Workplace

-

Aging Workforce

-

Immigration Law Update

-

Concerted Activity & Other News from the NLRB

-

Critical Conversations: Employee Assistance Programs

-

Changing a Culture: Key Elements to Creating a "Culture of Safety" and Ways to Sustain This Culture

Please share this information with your existing industries. Registration and additional event information may be found here.

|

|

|

|

|