Enterprise Value Compared to Net Transaction Proceeds

Enterprise Value (EV) is the measure of a company’s total value. It looks at the Company's overall market value rather than just its equity value. EV can be thought of as the effective cost of buying a company. When deal values are reported, we see Enterprise Values for those transactions quoted as a multiple of EBITDA or revenue. EV is an important metric because it enables buyers to value the company based on actual operational performance, regardless of its capitalization. EV is also a consistent way to compare competing offers.

When selling a company, EV is only the starting point. Deal terms can significantly alter the actual value of the offer. Other factors include the type of transaction. Is it a complete buyout or a recapitalization with rollover equity? Equity preferences and interest rates can make two similar EVs vastly different from a long-term perspective. Even when comparing two offers of 100% buyouts, there are many factors that sellers should consider in addition to the headline Enterprise Value.

We look to equate all offers to a Net Transaction Proceeds amount for our clients during the decision-making process. In other words, once the deal closes, how much will the shareholders collectively receive from the transaction net of closing adjustments, debt, escrows, and other transaction expenses? As a founder considers a potential liquidity event, they need to fully understand the Net Transaction Proceeds amount to plan for the future and make an informed decision on whether a transaction at the stated Enterprise Value trumps another competing offer or outweighs the benefits of retaining the business.

Sellers should understand the variables that affect EV and approach negotiations early in the process to maximize their net transaction proceeds.

Here is an example Letter of Intent (“LOI”) offer that shows how an EV of $100 million EV translates into net transaction proceeds of $94 Million. The LOI will likely be worded as follows:

“We propose to acquire 100% equity of the company, on a cash-free, debt-free basis, at an Enterprise Valuation of $100 Million. The Enterprise Valuation is based on the Trailing Twelve Months EBITDA of $10 Million. The Purchase Price, subject to standard closing adjustments, will be paid to the Sellers upon completing the definitive transaction documents.”

The remainder of the LOI will discuss the proposed closing terms and adjustments, which generally include: escrow amounts and release, indemnification amount with cap and basket, origination and management fees, due diligence period and costs, working capital adjustments, and any seller notes or equity terms.

During due diligence, language will be negotiated in the Purchase Agreement to formalize the terms and amounts of the closing adjustments. Each of these variables will have separate definitions in the Purchase Agreement.

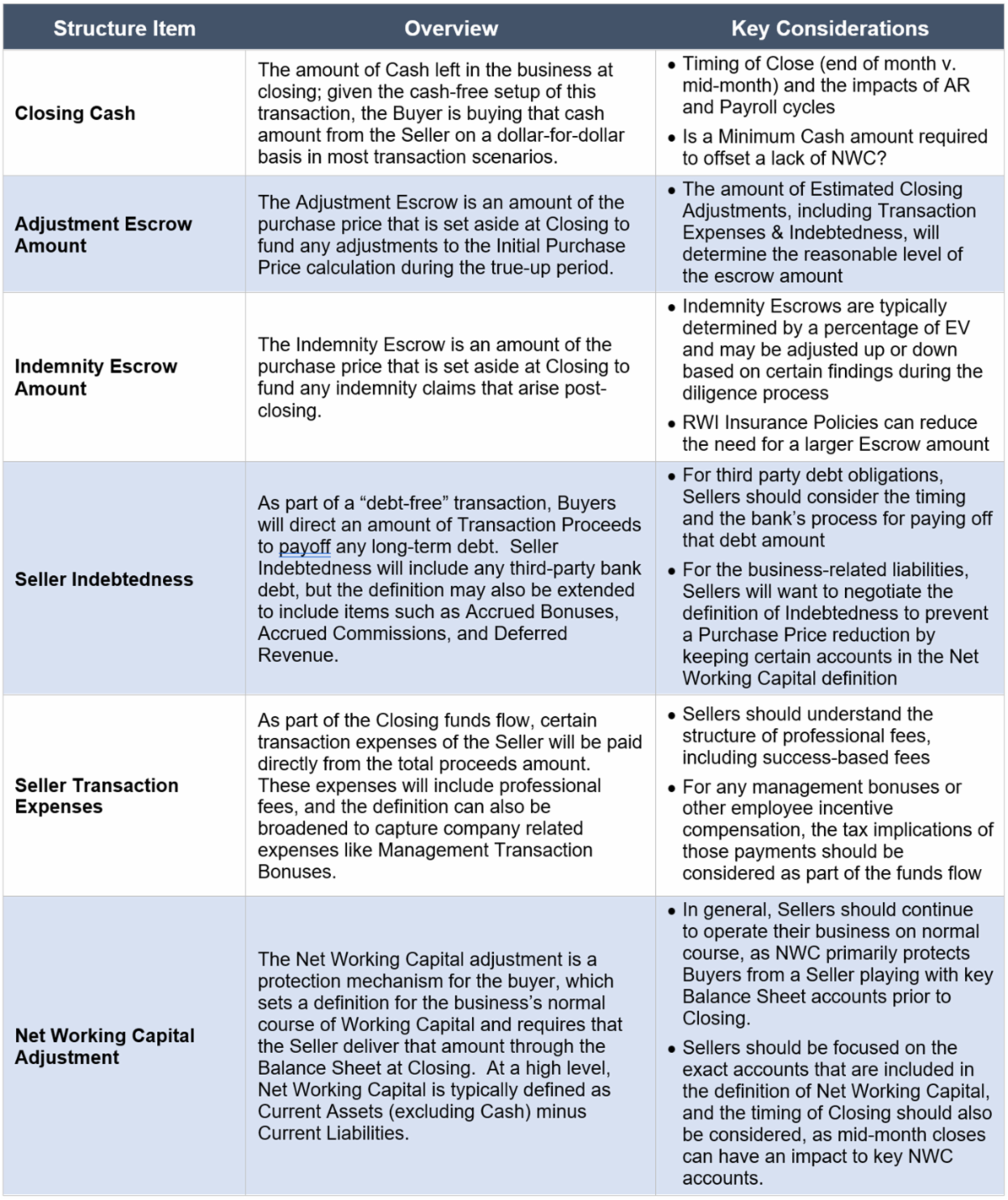

The chart below highlights common closing adjustments and some key considerations that impact the net transaction proceeds amount.