|

Win $50!

|

|

There are two member numbers spelled out within the text of this eNewsletter. Find your number and give us a call at (888) 387-8632 to claim $50!

|

|

|

|

|

*Annual Percentage Rates (APR) are subject to change. Rate, maximum term, maximum loan amount and advance amount are based on credit qualifications. Maximum terms vary based on loan amount. We reserve the right to determine collateral value based on industry recognized guidelines or full appraisal. Must be 18 years old or older to apply for a loan. Loans are subject to all Credit Union policies and procedures. Auto loan at 2.24% APR requires a minimum FICO® 750 Credit Score. 72 months term at 2.24% APR is $14.86 per $1,000.00 borrowed.

|

President's Corner President's Corner

|

Last month, I talked about the changes we are making in order to remain independent and competitive. Not only do we have to compete against the "Big Five" largest banks, regional banks, community banks, other credit unions, and nonbanks such as Walmart and Quicken Loans, but now our federal regulators are currently reviewing an application from a clean energy company to charter a new credit union to fund clean energy loans for its customers.

"Clean Energy" has become an umbrella term for all the different types of energy that do not pollute the atmosphere when used. In other words, clean energy is any type of energy not originating from coal or oil. Renewable energy includes wind, solar, hydro, geothermal, and to some, nuclear. While this is not a debate on climate change, I think we can all agree less air pollution is good.

The problem is the NCUA, the federal regulator overseeing all federally-insured credit unions in the nation, is considering a charter to an entity for the sole purpose of funding clean energy loans that most credit unions can do today. Many California taxpayers who have financed solar panels on their residences are already experiencing a form of this on their property tax statements. These solar companies hoodwinked the California Legislature into believing they were the only one capable of making these loans. We have seen examples of 90-year olds financing solar panels with 20-year terms that have to be paid off when the borrower/taxpayer dies or their first mortgage loan pays off or is refinanced. Is this responsible financing? I think not.

The solar companies have convinced our state representatives that credit unions are against clean energy. This is a fallacy. Credit unions are very much in favor of clean energy and can do a much better job of financing loans for solar panels, air conditioning systems, wall and attic insulation, LED lighting, and window and door sealing. After all, our business is to lend money to regular people with the personal service they cannot get at larger banks.

There are some other significant areas of disagreement with the NCUA should they approve this charter application. First of all, the proposed credit union will be located in Colorado but will serve a nationwide audience. While virtually every other credit union serves a well-defined community or membership group, the applicants want all 320 million of us as potential members. This smacks right in the face of local operation and ownership and keeping dollars in the community which is the bedrock of the credit union industry. Secondly, there is no defined membership. Being a customer of a clean energy company is not a valid common bond by any measure.

We'll see what happens. If NCUA approves the clean energy company's application, the entire credit union landscape will change. Who will apply next to operate a credit union? Walmart? Amazon? Google? If that happens, there will be some changes that none of us want.

David M. Green

President/CEO

(925) 335-3802

|

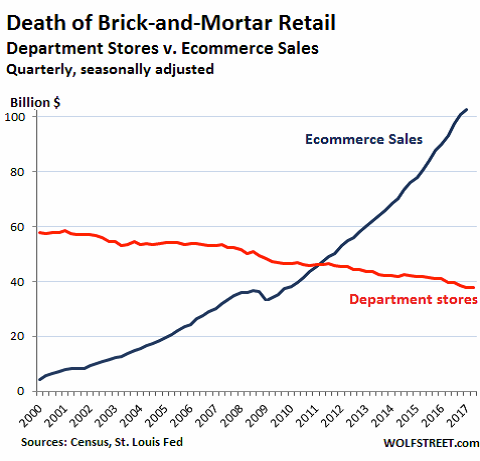

Stat-of-the-Month

|

Source: Tom Slefinger, Weekly Relative Value; Balance Sheet Solutions, an Alloya Company; Week of June 5, 2017

|

1st Alerts

|

- Remember, if you are traveling with your 1st Nor Cal debit or credit card, please contact us ahead of time at (925) 335-3855 to ensure your card(s) work(s) properly wherever you are.

- As part of our debit and credit card security enhancement, our fraud department will now contact you by phone, e-mail, or text to confirm card transactions. If you have any questions, please contact us at (925) 335-3855.

|

1Consult your tax advisor.

|

Credit Corner

|

Sigh of Relief on Credit Reports

The three largest credit bureaus have made several consumer-friendly changes that may increase credit scores of borrowers. This was done as a result of complaints received the Consumer Financial Protection Bureau (CFPB), a federal government agency. The changes were made to ensure that only accurate negative information is reported.

The changes include the following:

- Tax liens and civil debts such as judgments will no longer be reported on credit reports if the information does not include a consumer's name, address, and Social Security Number or date of birth.

- Medical collections will not be displayed until after at least six months after the account becomes delinquent.

- Medical collections paid or are currently being paid by insurance companies will be removed.

The new changes do not affect payment history and credit utilization which accounts for two-thirds of the credit score. Other factors include length of credit history, opening new credit accounts, and credit mix. In order to make sure your credit information is accurate, we recommend getting a free credit report at

www.annualcreditreport.com.

|

Tips for Teens

|

Congrats Class of 2017! Congrats Class of 2017!

"Would you tell me, please, which way I ought to go from here?" said Alice.

"That depends a good deal on where you want to get to," said the Cat.

"I don't much care where-" said Alice.

"Then it doesn't matter which way you go," said the Cat.

"-so long as I get somewhere," Alice added as an explanation.

"Oh, you're sure to do that," said the Cat, "if you only walk long enough."

-

Lewis Carroll, Alice in Wonderland

A big congratulations to all of you who graduated this past June! I hope everyone had a safe and joyous graduation and grad nite - I know I did! Looking back, it really doesn't feel as if 13 years of schooling have gone by, but they have. We're the last class born in the 1900's; the last class to watch

Kim Possible, The Sweet Life of Zack and Cody, Hanna Montana, That's So Raven, Teen Titans, Dexter, and

SpongeBob; the last class to know what spending Friday afternoons at Blockbuster Video felt like, or how to print out a Google Map and directions. We're the last class to know that blowing into a Gameboy, NES, or N64 cartridge does the trick, and what it's like to use a Moto Razor (or any flip/slide phone for that matter). But on a more serious note, you've got your whole life ahead of you. How exiting! Think of all the weekends you'll spend at the beach, all the road trips you still need to take, the late nights you'll enjoy with your friends, all the bonfires yet to be lit, and all the times you'll have to explain to the fire fighters that "it was an accident".

Oh, the Places You'll Go (Dr. Seuss) and the things you'll see!

I recently went down to Disneyland and on the way there I remembered that when I was a kid, when adults asked me what I wanted to be when I grew up, I'd answer, "I'm going to be a Cast Member at Disneyland!" Unfortunately, life forces us to grow up and realize that working at a park can only get you so far. However, despite this, the dream was rekindled. It was on my way to Disneyland that I realized that we are the captains of our destination. We have the right to live out our dreams, however strange or illogical they may seem. We should only have to listen to ourselves, and take the advice of others as just that, advice, and not a direction in which to head towards. Life shouldn't be about finding what job will make you the biggest bucks, life should be fun and fulfilling.

If you are still being asked where you're going next or what career/major you are going into, it's completely okay not to know. A lot of people go through life not really knowing what they're going to be or how to move on, yet in the end, they still make it through fine because they put their best foot forward and gave it their all. They started nowhere and ended up in the best possible somewhere. With this in mind, go out there! Live out your crazy dreams! Put your best foot forward! Give it your all! You'll eventually end up somewhere.

Luis Dominguez

Student Social Media Intern

1st Nor Cal Credit Union

|

Travel Smarts for Your Money and Identity

|

Thieves love tourists. It's nothing personal. They're just looking for an easy target - someone who's carrying cash and credit cards, tablets and cameras, passports and other identification, all while being distracted by the new sights and sounds all around them.

So how do you take it all in without allowing a thief to take off with your money, identity and other valuables? These five travel tips should help:

- Stay aware of your surroundings. This applies to all situations, from your hotel room to crowded public spaces. If a stranger bumps you, check your belongings immediately, even if it seemed accidental. Also use caution if you notice a public disturbance or other commotion - thieves appreciate a good distraction.

- Watch out for digital thieves, too. If you use public wi-fi, only visit secure sites (addresses starting with "https"), and log out of accounts after each session. Need cash from an ATM? Paying for gas at the pump? Watch for "skimmer" devices designed to steal your information. They can be hard to detect, so look for card readers that don't seem to match the rest of the machine.

- Lock up your devices. Make sure your smartphone, computer and tablet all require secure passwords for access. Otherwise, a thief who makes off with your electronics could also make off with your personal information. Leaving devices behind at the hotel? Store them in your hotel room safe.

- Always have some cash. There are situations where cash is just better than credit. If a merchant or barista just doesn't seem trustworthy, use cash. Credit cards are best when you know the location is secure, such as at an airport or chain store, or when you want the purchase protection your card offers for a big-ticket item.

- Think about home. Don't let burglars ruin your return from vacation. Stop your mail and newspaper delivery, put some lights on timers and make your home look occupied. Just in case someone does get in, keep your documents and valuables in a secure area.

- Call your Credit Union. Remember to contact your Credit Union before traveling and have a travel notice placed on your Visa or Master Card. Adding a card travel notification can help minimize the chances of your credit/debit card being blocked or flagged for unusual activity.

Remember, travel is supposed to be fun! Taking just a few common sense precautions will help make sure you're free to wander without worry.

As an added benefit of your 1st Nor Cal membership, we at Lou Aggetta Insurance will help you review the things that are important to you and provide you with options for reducing risk in your life. We are an independent insurance agent and can provide you with home, auto, life, health, business and many other types of insurance coverage.

Contact me today to schedule your free review.

Denia Aggetta Shields

Lou Aggetta Insurance, Inc.

2637 Pleasant Hill Road

Pleasant Hill, CA 94523

(925) 945-6161

|

By Jason Vitucci, CFP & Gene A. Schnabel

In the seemingly complex world of retirement, there are important numbers you should be aware of that could make or break your overall retirement savings. Here we will highlight five numbers that could potentially make or break your retirement.

#1 - 41%. This is a surprising statistic that reveals the percentage of workers (or four in 10) who say they (or their spouse) have tried to calculate how much money they should have saved to live comfortably in retirement, according to a March 2017 Employee Benefit Research Institute's Retirement Confidence Survey3. That's a relatively low number given a good rule of thumb is to plan to have 10 times or more of your final salary in savings for retirement.

#2 - 50. This represents the age at which you can make catch-up contributions to your retirement savings. The benefit of blowing out the candles on your 50th birthday is the ability to increase the amount you save in retirement accounts to the tune of $6,000 additional dollars a year into a 401(k) or an extra $1,000 into an IRA.

#3 - 8%. It may seem like a small number but it could mean big savings for older workers who delay taking Social Security benefits beyond their full retirement age (around 66). Those who delay taking their benefits could increase their overall earnings by an additional eight percent each year until the full retirement age of 67.

#4 - $1,360. This number reflects the average Social Security benefit of approximately 41 million retired workers. It is important to understand that Social Security benefits vary by amount of time worked and the age when you enroll. It is important to sit and speak with someone about your situation before you begin taking your Social Security benefit, without doing so you may miss the opportunity to maximize your benefit.

#5 - 4%. On average, this is the recommended maximum percentage of assets you should plan to withdraw the first year of retirement. This is a general rule of thumb to ensure the nest egg you've worked hard to prepare will last for at least 30 years into the future. For example, if you've saved $1 million, you would plan to withdraw no more than $40,000 (or four percent) that first year. Then to help keep pace with inflation, you could increase that initial dollar amount by the inflation rate each year. Depending on your life events, the economy, and your income requirement, this number may need to be adjusted each year. It is very important to "stress test" your financial plan on an annual basis when in retirement to ensure that your savings will last you through your life time.

At Vitucci Integrated Planning, we would love the opportunity to take a look at your current financial plan. Retirement preparedness varies by age and personal financial situation. If you have questions or concerns about your retirement plan, please give the office a call. As a valued 1st Nor Cal member, we invite you to contact us for a complimentary financial analysis. We also invite you to attend any of our Retirement Planning workshops that we hold. For more information about our practice, our workshops, or to make an appointment, please call us at (925) 370-3750 or visit our website at www.vitucciintegratedplanning.com.

Vitucci Integrated Planning

Securities through First Allied Securities, a registered broker dealer, member FINRA/SIPC. Advisory services offered through First Allied Advisory Services, Inc. Registered Investment Advisor. Investments not FDIC or NCUA/NCUSIF insured, not insured by Credit Union, may lose value. Products offered are not guarantees or obligations of the Credit Union, and may involve investment risk including possible loss of principal. 1st Nor Cal CU, Bay Area Retirement Solutions and First Allied are all separate entities. Jason Vitucci CA Insurance Lic.: 0F59894, Gene A. Schnabel CA Insurance Lic.: 0663016

Citations:

3: https://www.ebri.org/pdf/surveys/rcs/2017/IB.431.Mar17.RCS17..21Mar17.pdf

|

FREE Financial Counseling

|

Are you in need of financial counseling?

1st Nor Cal is here to help. Timely and honest debt advice is available to our members at no cost or obligation. Learn how to manage your finances.

Make your appointment TODAY!

Just a reminder, you can annually request FREE Credit Reports from all 3 credit reporting agencies online by going to:

For FREE Financial Counseling, don't hesitate to contact:

Shelley Murphy

Senior Vice President of Lending & Collections

(925) 228-7550 Ext.824

(FIVE ZERO TWO THREE NINE NINE ZERO)

|

YouTube - How To Series

|

Did you know we're on Social Media?

|

|

|