The Miles Franklin Newsletter

|

|

From The Desk Of David Schectman

|

|

It’s worth noting that, even though gold is not a ‘productive asset’, the price of gold over the past 20 years has beaten the stock market, including Warren Buffett.

From September 1999 through September 2019, the S&P 500 returned a solid 229%, including dividends. And the stock price of Buffett’s company (Berkshire Hathaway) is up an astonishing 536% over the same period. But the price of gold has surpassed even Buffett, returning 591%.

– Simon Black

The Big 7 traders that are short up the wazoo in the COMEX futures market in both silver and gold didn't make any progress at all during the past week and, according to Ted in his weekly review on Saturday..."their total open losses actually increased by $100 million to $3.7 billion at Friday's close."

It is, as always, the resolution of these short positions by these traders that will determine where precious metal prices go from here. Can they cover most of all their losses by engineering new low prices...or will they be forced to cover and book enormous loses...driving prices sky high in the process? And as Ted correctly points out...this is all that matters at the moment.

– Ed Steer 10/8/19

"

In a global system of failed monetary policies and a long and difficult path to fiscal policy, there is only one other tool left in the box for the global economy and that is lower the price of global money itself: the U.S. dollar

."

"

Weakening the Killer Dollar will likely put the final nail in the coffin of the grand credit cycle that started in the early 1980s, when the U.S. balance sheet was reset, and the USD was anchored by Volcker's victory over inflation after Nixon abandoned the gold standard in 1971

."

- Saxo Bank's Steen Jakobsen

In the field of economics, for example, many are the new things that have come along in the last 100 years.

Exchange-traded funds (ETFs), algorithmic trading, the Fed's dynamic stochastic model, negative rates, Keynesianism, Modern Monetary Theory (MMT), data dependence, hedonic price adjustments - and much, much more.

But none of these breakthroughs and innovations are going to prevent average Americans from going through Hell in the next few years. Instead, they're going to make it worse.

– Bill Bonner

David's Commentary (In Blue)

Donald Trump is speaking today in Minneapolis at the Target Center (where I watch my Timberwolves games). My best friend called me a week ago and said that he and his wife and another couple were going to listen to Trump speak and asked me if I wanted to join them. That’s not my thing – I can read about it or watch it on TV, but then he said, he had hired an off duty police man to accompany them as a bodyguard. That is unbelievable? Here, in Minneapolis, you have to be worried about your safety just because you want to hear the President speak? Unbelievable, but he is being proactive. Just think how far our country has slid for something like this to even be considered. Unbelievable!

For the last two days, the markets were relatively quiet, due to traders taking time off for Yom Kippur. Besides the Yom Kippur holiday, the China trade news Thursday could lead to crazy moves, the levels of support and resistance are solid. Gold is resting just below its 50-day moving average and silver is slightly above its 50-day MA.

Many people who own gold and silver actually believe that the stock market is outperforming gold and that’s why they are reluctant to add to their positions. They say they will wait until the stock market plunges.

Like anything, it depends on the time frame used, but I put much emphasis on the last year’s performance. What happened 8 or 9 years ago has little effect on what is going on now.

Look at the following and see if you agree – the stock market is not outperforming gold.

Let’s start with gold.

Here is gold’s one-year performance. Gold is UP $300 an ounce, and the trend is UP.

|

|

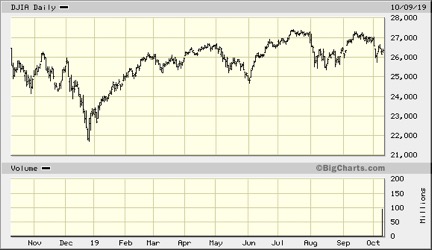

Now, let’s check out the Dow.

|

|

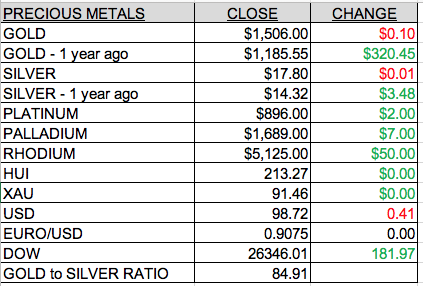

One year ago today the Dow was 25,998.74. The Dow closed yesterday at 26,346.01. And its trend is flat. Even with the help of falling interest rates and the Fed’s new QE programs, it is not moving up.

The Dow is up just over 1% in the last 12 months while gold is up 26%.

Let’s expand it a bit and use a 5-year time frame.

|

|

This chart looks about the same as the 1-year chart. Gold is up almost $300 or 25%.

Five years ago today the Dow was 16,544.10. It trended up, peaking at 26,616 on Jan 26, 2018. Since then it has gone nowhere.

I can understand why so many people are gun shy and still think gold is not performing nearly as well as the stock market, but that simply isn’t true. Gold is rising BEFORE the stock market crashes. Could it be that it is telling us something? Is it acting like the “canary in the coalmine? I say yes it is.

It shouldn’t be long until gold is rising rapidly and the stock market is falling hard both at the same time. That’s when people will return to the gold and silver market. The evidence is there, if you care to look, that the place to be – now – is in cash and precious metals. Before this trend of a stock market that refuses to rise (and if something can’t go up it will go down) and a gold and silver market that are already up over 25% in the last year.

I am amused reading the headlines on Kitco every day and whenever gold falls a few bucks they say, “Gold is down as risk aversion wanes.” Give me a break. Risk aversion wanes every other day and people actually sell and buy their gold based on Trump’s latest Tweet? All the people I know and our client base hold onto their gold and do not trade it. It’s the funds, trading in and out every day, trying to make a profit on small moves with highly leveraged positions that move the market. It is not the retail buyer, people like you who are reading this newsletter.

Gold and silver move up and down based on the activities of the 7 big COMEX traders. Recently they found themselves on the wrong end of their record-sized short position and even now, after pushing gold down by $70 and silver by nearly $2, cutting their losses by nearly $2.3 billion, their current unrealized open loss sits around $3.8 billion. Should they lose control of the price and gold and silver start moving up again, they will have to go long to avoid even steeper losses and that is when the gun goes off and the horses leave the starting gate.

Ted Butler sums it up as follows:

“

That we have to endure and wait out the near term resolution is somewhat regrettable, but it is more encouraging that we’ll get to see which it will be – either one more manipulative shakedown followed by the real liftoff in price or a liftoff without a final shakedown. Short-term price movements and outside news developments don’t provide much real clue as to which outcome it will be. They don’t matter much to the eventual resolution.”

My grandson Josh (Andy’s boy) is in his second year at the University of Michigan’s business school. He recently called me and said he had an assignment in one of his classes and asked me if he could interview me on the topic of The 1960s. That’s right up my wheelhouse. I was Josh’s age in 1961. I was in college from 1959 through 1964. The 60s came in just like the 50s but by the time the decade was over, everything had changed. There was never anything like it before, or after. The 60s were an amazing time and I feel blessed that I was able to live through this change. I told Josh that what made the 60s so unique is that in the 60s everything changed. Before then, everything was the same. Values, fashion and morals, - we were like our parents and their parents. Everyone had the same rigid patch to follow and never questioned it. There was not much room for individualism. We went to college (everyone could afford it then), got married. When we graduated, got a job with a large corporation, moved into the suburbs, had two children and two cars and lived happily ever after. That was the template. But then it all changed.

The 60s are often referred to as the age of drugs, sex and rock and roll. And for many people that’s exactly what they were – but prior to the 60s none of that came into play. The two defining events were both protests: My generation fostered the movement to get out of Viet Nam, and the Civil Rights movement.

Music evolved from the jazz and classical music of the 40s and 50s and the early rock and roll pioneered by Elvis Presley and the Everly Brothers to Woodstock and Crosby Stills Nash and Young with their war and drug anthems. Black blues became mainstream. The music revolution came from Great Britain (The Beatles, the Rolling Stones and Led Zeppelin) and they were influenced by American black blues. In 1959 and 1960 I used to listen to a black blues radio station that broadcast from the Deep South. I could only tune in late at night, after AM radio stations were allowed to increase their wattage and then the AM signal could travel all the way to Minneapolis.

My wife Susan marched with a group of women who burned their bras and men burned their draft cards. I had long hair, in an Afro style, and lived the era to the fullest. It was incredibly liberating, at least for me. My life was totally transformed. I was 28 going on 17 and most of my friends were 28 going on 60. I cast off my three-piece suits and ties and moved to bell-bottom jeans and paisley print shirts.

The 60s were not the same experience for everyone. A majority of the population trucked on as they always had, but not me. I have always been a free spirit and an individual thinker. In 1971 I was the only person in Target’s corporate buying office with long hair. I was a rebel. Perhaps that’s why the precious metals industry, which is certainly not mainstream, appealed so strongly to me. I always questioned everything and did things different from my peers. I have the ability to “see around corners.” The path we are on in America is very clear to me. I can see how it ends up. You should be able to too. What I can’t see is

“when”

it all comes tumbling down. You could put the following on my tombstone: “He was almost always right, but early.” Maybe that’s a good thing, because the last thing any of us needs is $5,000 or $10,000 gold. We should have had it already, but along with it will come very bad times. But isn’t that exactly what we buy “insurance” to protect against? And who wants to collect on their fire insurance or life insurance – or financial insurance?

Tearing everything down was easy for us rebels in the 60s. But my generation never figured out what to replace the values we rejected with. Most of the “hippies” of the 60s, with their flower decals, long hair and Volkswagen vans eventually settled down and melted back into the “system.” There are still a few holdouts and you can party with them at Grateful Dead concerts.

In spite of Susan and I being very free-spirited and unfiltered in the 60s, we managed to raise two stable, successful and decent children. Yes, you can test the limits, and still have a successful life. And the 60s gave some of us a once in a lifetime opportunity to do just that.

One of the most significant things that put an end to the free life style of the 60s was when Nixon “closed the gold window” and removed gold as backing for the dollar. As a result, Inflation raged in the 70s and suddenly it took two incomes to maintain the lifestyle that one wage earner could do in the 60s. Women had to go to work (including my wife). It became too expensive to be a hippy or beach bum. Personally, I would have loved to be a professional student. I loved my time at the U of Minnesota and hated to leave it for the workplace.

|

|

In 1975, long before I knew anything about economics or inflation, I purchased a limited edition, signed print titled

The Failure of Capitalism

by Michael Bedard. It sits on the wall behind my desk in the office, below a picture of Susan. How appropriate was that. It shows two ducks sitting on a mountain of dollar bills staring off into the sunset, which is a dollar sign sinking into the ocean. Little did I know at the time that my industry would be based on this very concept.

|

|

|

O.K., back to the newsletter’s main thrust. Look at the following graph and ask yourself how can this continue and the dollar hold its value? Come to think about it, the dollar is NOT holding its value. Using my 60s example, I purchased a new Corvette in the late 60s for less than $5,000, a new Mercedes 280SL roadster for $9,500, a new four bedroom colonial in the suburbs for $30,000 and my job at Target paid me less than $10,000 a year. The dollar, since the 60s is worth just a few percent of what it was when I was young. But gold, which was around $40/ounce then now costs 38 times more. Remember, gold did not go up; it is the dollar that lost purchasing power so it takes 38 times more dollars to buy the same thing.

|

|

For me, ultimately it’s all about the dollar. The dollar is rapidly losing its privileged status as the world’s Reserve Currency and as a Petro Dollar. That will spell the end of the good times and free lunch that we have all benefited from in our lifetimes. Our grandchildren will not be so lucky. I choose to have my wealth in gold and silver knowing how this will all end. The following two articles are an example of how this is starting to unfold.

|

|

|

|

Zero Hedge

There is a

strong current of change

affecting the international political arena. It is the beginning of a revolution brought on by the

transition from a unipolar to multipolar world order

...

|

|

|

|

Fox Capital Management

The End Game for Fiat Currency. Conclusion…

At the end of the day, financial investments and fiat currencies turn to ash while hard assets and tangible resources hold their intrinsic value (but skyrocket in terms of paper money). Initially, however, stocks, corporate debt and sovereign debt will likely be caught in a tug of war between deteriorating fundamentals and relentless central bank buying, making it very difficult for bullish and bearish investors alike. What is certain, though, is that volatility for all financial asset classes will increase substantially in stark contrast to the last decade, and it is only a matter of time before central banks lose all control and credibility. At that point, the game is finally up. Meanwhile, natural resources and hard commodities will be the best stores of value as this chapter reaches its conclusion.

So, while the path ahead is wildly uncertain, the final destination is clear. Decades of excess debt creation financed by the world’s central banks has led us across the Rubicon, and the only valid solution is a coordinated sovereign debt restructuring accord coupled with the creation of a new global monetary system. Given the international discord that will likely accompany and probably lead to this crescendo, any new construct will have to guarantee trust to its participants. Gold, the only reliable monetary constant, which spans millennia, is the logical ballast.

|

|

Corporate stock buybacks are very much a reason why the stock market hasn’t yet imploded.

|

|

|

|

When it comes to politics, one thing is certain: it is all about fake news, and how it is spun. Which is why some people prefer finance: after all, when it comes to math-based financial data, reality is either a 1 or a 0.

Unfortunately, it now turns out that even financial "data" can mean whatever one wishes to read from it. Case in point: today's CNBC appearance by Goldman's chief equity strategist David Kostin, who when commenting on the fate of the market in the context of trade war, warned that stock buybacks - the primary driver of stock upside together with the Fed in the past decade - "are getting muted" and thus clients are turning cautious.

There is just one problem with Kostin's statement: it is dead wrong

, at least according to the latest buyback data from Bank of America's trading desk.

As BofA's Jill Carey Hall writes in her latest client flow trends, "corporate buybacks accelerated to their strongest weekly level in our data history since 2009", led by Tech buybacks for the fifth week. This is in line with BofA's expectations, which had predicted that tech would benefit from a ramp up in buybacks YTD given the high announced/completed buyback ratio for the sector heading into the year.

As a result of this burst in stock repurchases, cumulative YTD buybacks are now +25% YoY, with 3Q to date buybacks +39% YoY and stronger than normal seasonal trends (which typically slow through late Sept and pick up over the next ~6 weeks amid earnings season).

And since a substantial portion of the proceeds is used for stock buybacks, it should not come as a surprise that we just saw a record week for stock buybacks... and why stocks are surging today even as both PMIs now suggest the U.S. is headed for a recession.

But if companies are buying every share of their stock they can find - with no price discrimination - who are the sellers? We know that answer too

: as we reported a week ago, corporate insiders - typically CEOs, CFOs, and board members, but also venture capital and other early state investors - sold a combined $19BN of stock in their companies through to mid-September. Annualized, on track to hit $26BN for the year, which would mark the most active year for insider sales since 2000, when executives sold $37bn of stock amid the idiotic frenzy of the first tech bubble. That 2019 total would also set a post-crisis high, eclipsing the $25bn of stock sold in 2017.

Finally, as for Goldman once again completely misrepresenting reality and peddling "fake news", we hope that by now that comes as no surprise to any of our regular readers.

|

|

As Jim Sinclair said, “QE to Infinity.” The Fed can never stop or the game is over.

|

|

|

|

The short-term repo funding turmoil that cropped up in mid-September continues to be discussed at length. The Federal Reserve quickly addressed soaring overnight funding costs through a special repo financing facility not used since the Great Financial Crisis (GFC). The re-introduction of repo facilities has, thus far, resolved the matter. It remains interesting that so many articles are being written about the problem, including our own.

The on-going concern stems from the fact that the world's most powerful central bank briefly lost control over the one rate they must control

.

What seems clear is the

Fed measures to calm funding markets, although superficially effective, may not address a bigger underlying set of issues that could reappea

r. The on-going media attention to such a banal and technical topic could be indicative of deeper problems. People who understand both the complexities and importance of these matters, frankly, are still wringing their hands. The Fed has applied a tourniquet and gauze to a serious wound, but permanent medical attention is still desperately needed.

The Fed is in a difficult position. As discussed in Who Could Have Known - What the Repo Fiasco Entails, they are using temporary tools that require daily and increasingly larger efforts to assuage the problem.

Taking more drastic and permanent steps would result in an aggressive easing of monetary policy at a time when the U.S. economy is relatively strong and stable

, and such policy is not warranted in our opinion. Such measures could incite the most underrated of all threats, inflationary pressures.

The Fed is hamstrung by an economy that has enjoyed low interest rates and simulative fiscal policy and is the strongest in the developed world. By all appearances, the U.S. is also running at full employment. At the same time, they have a hostile President sniping at them to ease policy dramatically and the Federal Reserve board itself has rarely seen internal dissension of the kind recently observed. The current fundamental and political environment is challenging, to be kind.

This

commentary/opinion piece

was posted on the

Zero Hedge

website at 2:10 p.m. on Thursday afternoon EDT -- and it's from Brad Robertson as well. Another link to it is

here

.

Russia never wanted to turn away from the U.S. dollar but American policies have forced it, as well as many other countries, to do so, President Vladimir Putin told participants of the Russian Energy Week forum on Wednesday.

The U.S.' attempts to weaponize its national currency and use dollar settlements as an instrument of political pressure is a great mistake, according to the Russian president. He explained that Washington's actions have already forced many countries, including U.S. allies, to reconsider the greenback as a reserve currency, while dollar settlements have already slid from 50 percent to 45 percent.

"The dollar enjoyed great trust around the world. It was almost the only universal currency in the world. For some reason, the United States began to use dollar settlements as a political tool, to impose restrictions on the use of the dollar," Putin told the audience.

"They [the U.S.] are biting the hand that feeds them," he said, adding that sanctions only "undermine the trust in the dollar, isn't it clear, that they are destroying it with their own hands?"

Moscow has recently slashed by half the share of the U.S. dollar in its foreign currency reserves.

However, such a move is not Russia's choice, but the result of Washington's sanctions and restrictions as Moscow and its allies want to protect themselves and diversify settlements, according to Putin. Thus more than 70 percent of settlements between the members of the Russia-led Eurasian Economic Union (EAEU) are in rubles, while many other countries are switching to payments in national currencies instead of the dollar.

The above paragraphs are all there is to this article that showed up on the

rt.com

Internet site at 2:33 p.m. Moscow time on their Wednesday afternoon, which was 7:33 a.m. in Washington -- EDT plus 7 hours. I thank George Whyte for sending it our way -- and another link to the hard copy is

here

.

Egon von Greyerz

DON’T HOLD GOLD AT HOME, IN ETF, IN BANK incl. BANK SAFE DEPOSIT BOX

Gold held for wealth preservation purposes must be held in physical form and outside the banking system. The more counterparties between yourself and your gold, the higher the risk. But there must always be one counterparty. If you hide your gold in a hole in the ground, the hole is your counterparty. Someone might steal the gold or threaten your wife or children to find out where the gold is hidden.

When you hold gold to protect against all the risks in the world, you clearly don’t want to hold it in a bank.

We have seen so many examples of the bank not having the physical bars when clients intended to move the gold from the bank vault to private vaults. So even when the banks tell the client they have allocated physical gold, the gold is sometimes not there. Until now, the bank has rectified the situation by buying new bars. But one day when the system is under pressure, there might be no gold available or the bank is under financial distress and is not in a position to buy new gold.

Gold in personal bank safe deposit boxes is not advisable either since you might not get access to it for a very long time if the bank closes. Also, the contents of a safe deposit box is not insured and the bank does not take responsibility, if the contents is stolen. There are also multiple examples of safe deposit boxes being drilled open by the authorities for various reasons.

Many gold investors buy gold ETFs. This is a very big market with 2,800 tonnes held in total by gold ETFs. This represents a value of $135 billion.

Both institutions and wealthy individuals use gold ETFs to invest in gold. But since gold is the ultimate wealth preservation assets it should not be held in paper form.

Let me explain some of the drawbacks with gold ETFs:

- It is paper gold. All the investor has is a piece of paper saying he owns X shares in the ETF.

- The investment is held within the financial system and in case of a default, the investor might not get his investment back.

- In theory, the ETF should have 100% gold backing, but in reality very few do. If you read the fine print, they don’t have to hold the physical gold but can have a commitment or IOU from a bullion bank.

- Recent trading in the physical market proves this point. In August, gold ETFs increased their holdings by 122 tonnes or $6 billion. This is an increase of 5%, which is substantial for one month. The total increase for the period June to August was 312 tonnes or 12%. Yet, Swiss refiners have reported extremely low physical outflow and no buying from ETFs during that period.

- Gold ETFs normally never buy in the open market or from refiners. So where do they get their gold from. Well it is really just book entries. The custodian of the biggest gold ETF, called SPDR or GLD, is HSBC bank. Sub-custodians are LBMA banks like JP Morgan, Barclays or even the Bank of England.

- These custodians also hold Central Bank Gold. So when the ETFs need to acquire additional gold, like in August, the custodians just do a few book entries, using the gold they hold for central banks. It is very likely that some or much of this gold is double counted and belongs to more than one party. This is why there is no physical movement from refiners.

- Most ETFs don’t allow that clients take physical delivery. In theory, a holder of at least 100 GLD shares can take delivery. But this means a minimum of $14 million. GLD also has the right to settle in cash.

- GLD gold held with sub-custodians cannot be inspected.

- GLD gold is not insured.

It is extremely difficult to understand that major investors can accept to hold a wealth preservation asset and insurance against a rotten financial system in paper form like a gold ETF. If there is a financial crisis they are unlikely to get their hands on neither the gold nor the cash that the gold represents.

Why take this risk when you can hold physical gold outside the financial system in for example the safest vault in the world in the Swiss Alps. The holder of the gold holds it directly in his name with direct access to the gold. Also, the cost is similar to GLD but it includes insurance and the investors own physical gold that he has direct access to.

CRYPTOS ARE NOT WEALTH PRESERVATION

Cryptos and Bitcoin are often mentioned as the new gold. Especially the younger generation today often believe that cryptocurrencies is the safest money you can hold as well as the best way to avoid government control. A cryptocurrency can have some advantages as a method of payment. But there are so many drawbacks that make it totally unsuitable as wealth preservation.

Here are some of the problems with cryptos:

- A cryptocurrency is an electronic entry on a number of computers. As such, it can be hacked or lost. Over $1 billion was stolen in 2018. In 2019 so far, $4 billion has been stolen. Some of that might be recovered.

- If a crypto is stolen or lost, it is gone forever. You won’t get it back and there is no insurance. Some exchanges do have insurance but it is unclear if effective.

- Yes, you can take your crypto offline into cold storage, but every time you put it back online for transactions, you are exposed.

- Cryptos are often compared to gold but we must remember that total market cap of all cryptos is $215 billion against total value of all gold in existence is $8.5 trillion.

- Governments are unlikely to ever allow cryptos to be an alternative to fiat (paper) money without their approval and control. Cryptos can easily be banned by closing down all exchanges and making all trading illegal.

- Yes if it is banned, a black market of peer to peer trading would still be possible even though illegal. Conversion to fiat would be made a criminal offence and every illegal transaction could be declared null and void. So if you bought a house with cryptos, it would be confiscated.

- In the end, governments are likely to ban private cryptos and issue their own to replace current paper/electronic money. This will be a wonderful way for governments to totally control all money, to tax every transaction directly and to turn off the system or certain accounts at will. This is a very likely development in the Big Brother is Watching era we are currently in.

- One of the biggest threats to cryptos is Google’s and other technology firms ability to decrypt it. Most cryptos, including Bitcoin, use 256-bit encryption. Google can already break 53-bit encryption and another firm 128-bit. Google expects to break 256-bit encryption within a couple of years maximum and then 400-bit etc.

- With new Quantum Processors a computing task that would have taken 10,000 years on a supercomputer now takes a mere 200 seconds with a Quantum Computer.

- Thus any method of encryption could be worthless within the next few years. It is obviously likely that encryption will become more advanced but so will Google’s Quantum processors ability to break these advanced systems.

- So Bitcoin and other cryptos might be obsolete in the next couple of years and so will all other encryption including military and government secrets. Instead, Google will be ever more powerful controlling all systems and governments. With AI (Artificial Intelligence) and robots, mankind will have an ever-diminishing purpose and possibly even be extinct in the future.

- Quite a frightening development but certainly possible.

GOLD AND SILVER TO REACH MULTIPLES OF CURRENT PRICES

Let’s go back to the present and look at the short term and the areas, which we normal mortals can influence.

So I have in this article explained that from a wealth preservation perspective, neither gold ETFs nor cryptos can function as a true insurance against the severe problems, which the world will encounter in coming years.

Physical gold and silver, safely stored, is certainly not a panacea for all the problems, which the world will encounter, in the next few years. But it is the best economic and financial insurance that you can hold today in a world where most assets will crash.

As I have made clear in recent articles and interviews, gold and silver has started the next strong up-leg towards multiples of current prices.

The small correction we are seeing currently will end shortly. Thereafter, we will see a fast move in the precious metals that will surprise most people.

Investors must not focus on price but instead on the importance of holding protection against a financial system, which is unlikely to survive in its present form.

Founder and Managing Partner

Matterhorn Asset Management

Zurich, Switzerland

Phone: +41 44 213 62

|

|

Buffet is wrong. Gold has outpaced his Berkshire Hathaway fund. Hard to believe, but its true. From September 1999 through September 2019, the S&P 500 returned a solid 229%, including dividends. And the stock price of Buffett’s company (Berkshire Hathaway) is up an astonishing 536% over the same period. But the price of gold has surpassed even Buffett, returning 591%.

|

|

|

|

Simon Black

Maybe it started with his dad

– Congressman Howard Buffett of Nebraska – who, as a staunch advocate for the gold standard, argued to his colleagues on Capitol Hill that

“paper money systems have always wound up with collapse and economic chaos.”

Warren himself acquired a record-setting 128 million ounces of silver back in the late 1990s… which he later sold at a profit in the early 2000s.

But to listen to him talk about precious metals these days, he’s always negative.

Buffett often quips that if you took the world’s entire supply of gold and melted it together, it would form a cube of about 68 feet (~21 meters) per side and be worth around $9 trillion.

With that same $9 trillion, you could buy every share of Apple, Disney, Google, Microsoft, JP Morgan, Exxon Mobil, all the farmland in the United States, all the developable land in Manhattan, and still have more than a trillion dollars left over.

This is Buffett’s central argument: gold doesn’t produce anything. So it’s much better to invest in a productive asset like a business, farmland, etc.

Sure, I’d rather own a profitable, productive asset than a pile of metal.

But Buffett is completely wrong to compare gold to productive assets… they’re apples and oranges.

Gold isn’t an ‘investment’. It’s an insurance policy against paper currencies will lose value over time. So a MUCH better comparison for gold is CASH.

Using Buffett’s same thought experiment, would an investor with $9 trillion rather have all that money sitting in a bank earning 0%? Or buy all the productive assets I mentioned above?

Clearly it’s more attractive to own productive assets than cash sitting in a bank.

Now, most people obviously don’t have hundreds of billions or trillions of dollars to invest.

But foreign governments, pension funds, central banks, and Sovereign Wealth Funds do.

And if it were so easy to simply buy up all the farmland in the United States, or every share of Disney, etc. they would have done it already.

But life isn’t so black and white. Negotiating and closing a very large investment deal takes a lot of time and hard work.

Buffett himself understands this. That’s why he made only ONE major acquisition in 2017 (a chain of gas stations called Pilot Flying J) and ZERO in 2018.

Buffett’s company has $700 billion in assets and over $100 billion in cash; it’s extremely difficult to find enough large, credible deals to invest that much capital.

And large institutions like central banks and foreign governments have the same problem.

I have friends who are senior executives at some of these institutions who manage hundreds of billions of dollars; they’re constantly on the lookout for sensible deals where they can invest billions of dollars at a time.

But those opportunities are rare. And in the meantime, they need to park the money somewhere.

Just like Warren Buffett’s father, many of these institutional managers understand that paper money loses value over time.

Especially now, in places like Europe and Japan, interest rates are actually NEGATIVE. And any large fund that has a mountain of euros or yen is bleeding money due to negative yields.

So let’s go back to Buffett’s analogy:

Imagine you’re a large Sovereign Wealth Fund with $500 billion in cash.

Of course you’re searching for high quality, productive assets that you can acquire. But you know it’s going to take 10-15 years to fully invest that capital.

So in the meantime, do you:

(A) keep the $500 billion in a paper currency that has a 100+ year track record of losing value and being abused as a political prop?

Or

(B) keep at least a portion of the investment capital in gold– an asset with a 5,000+ year history of maintaining its value?

For large institutions, Option B is extremely compelling.

And THAT’S what has been primarily driving gold prices over the past year.

Central Banks and foreign governments like China, Russia, Turkey, Qatar, Colombia, etc. have been loading up on gold because it’s a better, safer, long-term alternative to holding dollars and euros.

As a result, the price has risen.

Clearly they’re still holding plenty of dollars (and euros). But they’re increasingly diversifying their reserves.

They can see that the US government will continue having $1+ trillion deficits. They can see that the Federal Reserve will continue debasing the currency with interest rate cuts…

(and the European Central Bank recently made interest rates even MORE negative.)

They can see that diplomatic and trade relations with the US are strained.

So it would be foolish for a foreign government to keep 100% of its reserve assets denominated in US dollars.

They can also see that gold is practically the ONLY asset that isn’t at an all-time high.

Almost ever major stock market, property market, and bond market around the world is at/near an all-time high.

Gold has had a good run lately. But its price (in US dollars) would still need to rise another 25% before surpassing its previous all-time high.

This is what’s likely to keep fueling demand for gold: very large sovereign wealth funds and central banks don’t have a lot of options, and gold is one of the only assets that makes sense for them.

This will likely continue to be the case.

It’s worth noting that, even though gold is not a ‘productive asset’, the price of gold over the past 20 years has beaten the stock market, including Warren Buffett.

From September 1999 through September 2019, the S&P 500 returned a solid 229%, including dividends. And the stock price of Buffett’s company (Berkshire Hathaway) is up an astonishing 536% over the same period. But the price of gold has surpassed even Buffett, returning 591%.

|

|

Private Safe Deposit Boxes

|

|

Unencumbered / Segregated Storage

|

|

About Miles Franklin

Miles Franklin was founded in January, 1990 by David MILES Schectman. David's son, Andy Schectman, our CEO, joined Miles Franklin in 1991. Miles Franklin's primary focus from 1990 through 1998 was the Swiss Annuity and we were one of the two top firms in the industry. In November, 2000, we decided to de-emphasize our focus on off-shore investing and moved primarily into gold and silver, which we felt were about to enter into a long-term bull market cycle. Our timing and our new direction proved to be the right thing to do.

We are rated A+ by the BBB with zero complaints on our record. We are recommended by many prominent newsletter writers including Doug Casey, Jim Sinclair, David Morgan, Future Money Trends and the SGT Report.

For your protection, we are licensed, regulated, bonded and background checked droppable-1564579585984per Minnesota State law.

|

|

Miles Franklin

801 Twelve Oaks Center Drive

Suite 834

Wayzata, MN 55391

1-800-822-8080

|

|

Copyright © 2019. All Rights Reserved.

|

|

|

|

|

|

|