Check Us Out on Social Media! |

|

Back in March, we provided insight on many of the ongoing updates surrounding the Coronavirus. But since then things have been rapidly changing; Frontline has been busy changing, too!

As part of our ongoing efforts to protect our clients (thank you for being one, by the way!) we have made rental applications a major focal point.

As we progress into the post-shutdown society we are finding that, more and more, applicants are attempting to forge their documentation in order to achieve approval for rental property. This uptick in forged documentation comes mostly in the way of income verification and is largely due to the increased number of people who are taking advantage of the additional unemployment benefits that rolled out due to the economic effects of COVID.

Unfortunately for them, they are now finding themselves stuck while trying to find a new place to call home. Many are turning to one of the hundreds of free pay stub templates that are available online.

In order to combat this, our applications department has become well versed in the available templates and has been conducting reverse image searches through Google to determine the authenticity of the documents. These steps are taken in addition to contacting the applicant's employer through the official business number rather than relying on the number provided by the applicant.

You and your investment(s) are Frontline’s top priority and we will continue protecting your Frontline to increase your bottom line!

A few more updates…

|

|

The Texas Rent Relief Program

Back in March, we provided you with information regarding the rollout of the Texas Rent Relief Program. As of 5/11/2021 Frontline has successfully helped our tenants collect a total of $57,441.01 in assistance from the program. We are still working with numerous others and expect this amount to increase exponentially before the expiration of the program on 9/30/2021.

Click here for more details on the Texas Rent Relief Program.

|

|

CDC Eviction Moratorium

On February 25th, 2021 U.S. District Judge John Barker issued a ruling stating that the eviction moratorium issued by the CDC surpassed the federal government’s constitutional authority. Since then many others have ruled in a similar manner, including U.S. District Court Judge Dabney Friedrich. However, The Department of Justice stated on Wednesday the 5th that “it would appeal a federal judge’s order vacating a nationwide freeze on evictions.”

|

|

|

|

Jay Hartley MPM®, RMP®

Owner - Managing Partner

|

Office | 817.377.3190

Direct | 817.288.5546

Frontline Property Management, Inc.

3000 Race Street, Suite 132

Fort Worth, TX 76111

|

|

|

|

COVID-19 Impact Projections on Texas' Economy |

|

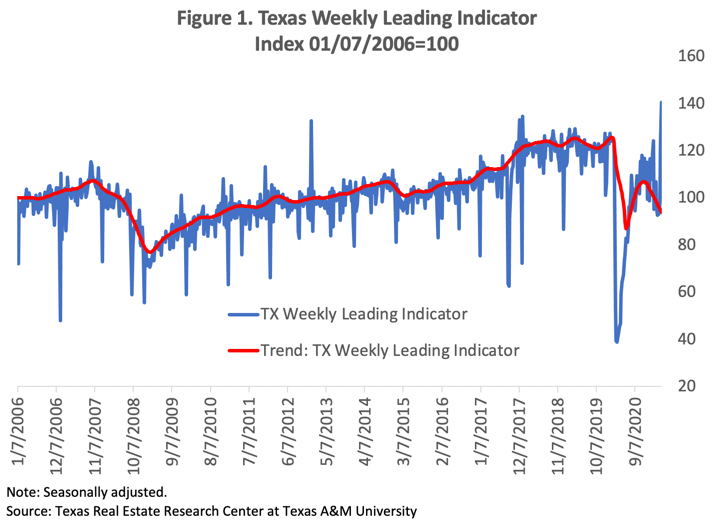

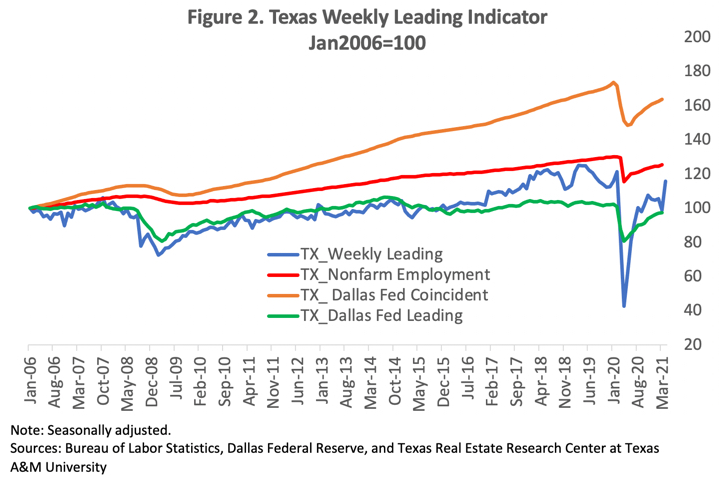

The Texas Weekly Leading Index increased for a fifth straight week (Figures 1 and 2), marking two straight weeks of sizeable increases. The weekly index has been gathering impetus and is pointing toward higher future economic activity. The recovery's pace continues to be hindered by the incomplete reopening of the economy and future uncertainty regarding the pandemic.

The increase was mainly due to a decrease in the number of people filing for unemployment insurance. It was offset by a decrease in the number of new business applications. Even though the number of new business applications fell, the number of applications remains high, signaling business activity remains strong.

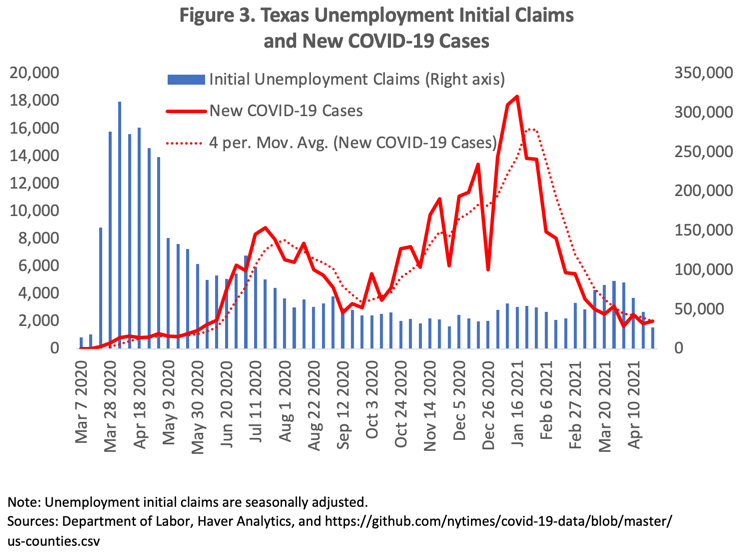

Initial jobless claims in Texas decreased considerably the week ending April 24, falling 19,441 claims to 27,353. This marks three straight weeks of significant drops and the lowest level of initial unemployment claims since before the pandemic. Continuing unemployment claims decreased to 275,943 the week ending April 17. Despite the decreases, levels of both initial and continuing claims remain around 1.6 and 1.8 times higher, respectively, than their pre-COVID-19 levels.

Gov. Greg Abbott lifted the mask mandate and increased capacity of all businesses and facilities in the state to 100 percent starting March 10, 2021. Still, prospects for the state economy's full reopening and recovery depend on dwindling cases and hospitalizations and increasing vaccination rates. Reopening and recovery improved as the number of cases continue to trend downward up to the week ending April 24 (Figure 3). In addition, vaccination rates are increasing. This could benefit consumer behavior, increasing business activity while reducing the number of layoffs going forward and allowing people to return to the labor force.

In addition, both an increase in the real price of West Texas Intermediate (WTI) oil, and a decrease in the real rate for the ten-year Treasury bill (which continues to exhibit a negative return in real terms) contributed to the increase in the weekly index.

As mentioned, the rebound in Texas' economic activity could be hindered by possible upsurges in COVID-19 cases as economic and social activity increases. Further waves of infections can reverse increased mobility and spending, affecting the path to recovery.

|

|

About This Report

The COVID-19 health crisis is unlike any crisis the economy has experienced before. The economy is currently going through a self-induced, sudden stop to contain and stabilize the spread of the virus and save lives. The size of the economic shock will likely result in losses that overshadow losses from the 2008-09 financial crisis.

The Texas economy is not immune to the pandemic. In fact, the state's economy will be hit even harder than the world and the rest of the United States due to the simultaneous downturn in the oil industry.

This crisis has created a need for up-to-date economic indicators that can help forecast economic changes. The Real Estate Center at Texas A&M University has constructed a high-frequency economic activity index for Texas that estimates the timing and length of future upswings and downturns on a weekly basis.

New weekly data series (also called high-frequency data) and new methodologies to seasonally adjust the data on a weekly basis have allowed for the development of weekly coincident and leading economic indicators. The Center has a successful track record in estimating monthly residential and nonresidential construction leading indexes for Texas. Both indexes have proven useful in signaling directional changes and forecasting key indicators like single-family home sales, apartment vacancy rates, and commercial vacancy rates.

The Center evaluates economic data to determine:

- economic significance,

- statistical adequacy (in describing the economic process in question),

- timing at expansion and recessions,

- conformity to historical business cycles,

- smoothness, and

- currency or timeliness (how promptly the statistics are available).

However, the indexes do have some weaknesses. Underlying indicators are subject to revision, and while errors often cancel out across indicators, revisions impact the index and future monitoring of business cycles. In addition, although leading indicators often show the direction of a business cycle, they do not measure the magnitude of the change.

Even with these caveats, leading indicators are useful for measuring business cycles. Seven variables were evaluated for this report. Four (business applications, high-propensity business applications, business applications with planned wages, and business applications from corporations) are business market variables that are tied to state business activity. One variable, weekly initial unemployment insurance claims, is tied to state employment. Another, West Texas Intermediate (WTI) real oil price deflated by the all-urban consumer price index, is related to the oil industry. The last variable, the real ten-year Treasury bill estimated using same-period inflation expectations, represents the cost of credit in the economy.

Based on statistically reliable criteria, four variables were selected as economic activity leading indicators: business applications, initial unemployment insurance claims, real WTI oil price, and real ten-year Treasury bill. These variables demonstrated a significant leading relationship with Texas nonfarm employment. All other variables were found not to be statistically valuable or to perform below the business applications variable for the leading index.

Detecting turning points in any leading index on a month-to-month basis is difficult, because not all downturn (upturn) movements point toward recessions (expansions). It's even more difficult to do on a weekly basis. The Center has converted the weekly leading economic activity index into a monthly leading index to evaluate its predictive usefulness.

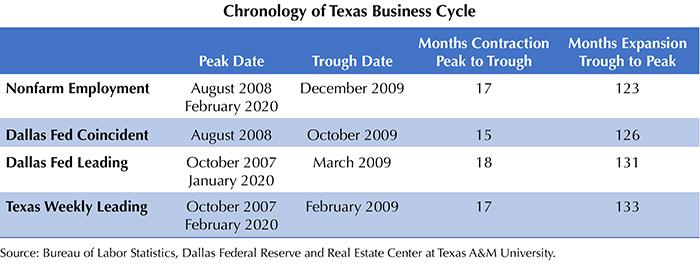

Based on the National Bureau of Economic Research methodology, Texas nonfarm employment and the Dallas Federal Reserve Texas coincident indicator are used as references of peaks and troughs to measure the state's business cycle (see table). This makes it possible to see if the weekly economic leading indicator can predict changes in Texas business cycles.

|

|

The Texas weekly leading index signaled a directional change in October 2007, 11 months before the prolonged downturn in employment that started in August 2008. Similarly, it signaled a recovery turning point in February 2009, 11 months before employment turned toward recovery in December 2009.

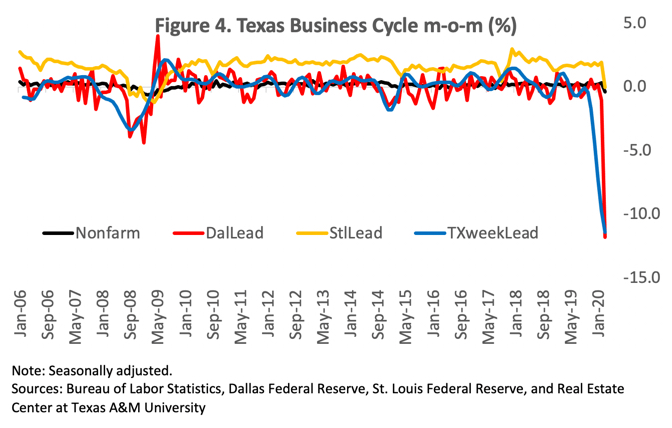

In addition, it predicted turning points and duration of expansion and contraction more accurately than another institution's leading indicator–the one produced by the St. Louis Federal Reserve (Figure 4).

|

|

Overall, the leading index is regarded as a good indicator to predict turning points in Texas employment, even leading both the Dallas Federal Reserve's coincident and leading indicators for the state's economy.

One major problem in evaluating the index was the short time period. For a more accurate evaluation of business cycle relationships, it's best to study the relationships over many business cycles. Because the predictive ability of the leading index was evaluated over a short time, it's possible that the relationship might not hold in the future. Thus, the leading index for economic activity will be best evaluated based on its ability to lead Texas employment in the future.

|

|

Source: Dr. Torres is a research economist with the Texas Real Estate Research Center at Texas A&M University. |

|

Disclaimer: This is designed to provide general information regarding the subject matter covered. It is not intended to serve as legal, tax, or other financial advice related to individual situations. Consult with your own attorney, CPA, and/or other advisor regarding your specific situation. |

|

|

|

|

|

|