Human Resource Consulting From The Business Viewpoint |

|

Human Resource Update | October 2021 |

|

Introduction

Following our September newsletter, I feel that some additional comments in relation to the new tax proposals and how they may affect executives and upper-level management are necessary.

As mentioned in September’s newsletter, anyone whose income exceeds $400,000 or joint filers whose income exceeds $450,000 (“Upper Earners”) will be subject to increased tax rates. Additionally, heightened capital gains rates are coming and more revenue raising proposals are being considered as this is being written.

Immediate Actions

Two actions we talked about in September need to be examined promptly and put into effect before the end of 2021: 1) accelerating bonuses; and 2) deferring income. Further down the list, we also talked about adopting a defined benefit pension plan that would predominately benefit Upper Earners.

While recently talking about the acceleration of bonuses with a client, I suggested that rather than paying only 80%-90% of the estimated bonus in 2021, that paying 100% of the estimated bonus should be paid in 2021. If the amount paid was less than the final calculated amount, the balance would be paid in 2022. If the estimate paid in 2021 exceeded the final calculated amount, the excess would be deducted from future salary in 2022.

Deferred compensation plans should be examined to ensure they provide sufficient flexibility not only in the deferment of such, but in successive deferrals and payments. Deferred compensation plans might also be opened to those at lower income levels as they may be affected by the new Upper Earners taxes on joint income.

Other out-of-this world taxes the new law may bring are: a) a revised surtax of 5% and 8% on incomes of $10M and 25M respectively, thus raising the top marginal rate to 51.4% - and that would be on modified adjusted gross income, or income before deductions (“MAGI”) making the basis for the increased taxes even higher; b) the elimination of the step-up in assets upon the demise of the owner; and c) taxation of unrealized capital gains – which started out targeting those with assets or income in the billions, but are now being talked about for those with assets or income in the millions.

Proposals that affect corporations, but will eventually affect the income of shareholders, are the imposition of an alternative minimum tax on book income of 15%; and a stock buy-back tax of 1% or 2%.

Where is this Newsletter Going?

So, where are we going in this newsletter? Two fully paid corporate perquisites that were offered in the past have been overlooked in recent years: 1) tax/financial/retirement planning; and 2) estate planning. These perquisites were usually reserved for members of the C-suite.

Due to the tremendous changes in the tax law, we are recommending that companies offer these perquisites to all C-suite members before year-end. This may be done by the company annually providing the services of selected planning firms or providing a stipend up to a set amount (and lost if not used). Tax and financial planning are most likely taxable while retirement planning is not. Estate planning may or may not be fully taxable depending on its linkage to the other planning ventures. But even if a planning service is taxable, it is well worth it.

As both the increases in the tax rates and their complications will now apply to more Upper Earning executives and upper-level managers than before, consideration should be given to expanding these perquisites to those immediately below the C-suite.

We would be honored to assist you in the development of any or all these programs. Please call us.

|

|

Michael F. Yates

President

|

|

If you find value in this newsletter please let us know. Feel free to call me with a comment and/or ask a question at any time (908-689-4200) or send me an email ([email protected]). We offer this timely information as another benefit of your relationship with our company. If you feel a friend or colleague would benefit from receiving our newsletter, please feel free to forward a copy.

You can view all of our newsletters by clicking the 'newsletter archives' link at our company website www.mfyco.com.

|

|

Daylight-saving time will end on Sunday, November 7, 2021, when clocks will be set back one hour at 2:00 a.m.

Keep in mind, shift workers who are on duty at that time will actually work an additional hour, for a total of nine hours of work. Employees must be paid for all nine hours. They also are entitled to overtime pay for all hours worked during the week in excess of 40, including the extra hour worked during the conversion to standard time.

|

|

Background Checks

Six Steps to Establish An Effective Background Screening Program

|

|

More than 90 percent of employers use some form of background screening on applicants or employees when making employment decisions. There can be several reasons for using them: ensuring safety in the workplace; reducing exposure to liability and legal costs; verifying information provided by applicants and employees; and ensuring position fit. While these value-adds may make a strong case for conducting employment background screenings, the legal landscape of this area is constantly evolving, which means that unsuspecting employers can easily find themselves in a minefield of trouble.

In order to successfully navigate that legal minefield, employers need to ensure that their employment-screening processes result in decisions that are ultimately based upon qualifications and job match.

Mathew A. Parker, a partner at the law firm of Fisher Phillips, shared the following six steps that can help employers lay the groundwork for a fair, consistent, and effective background-screening program:

-

STEP 1: Create Your Written Background Screening Policy. Your written background screening policy should contain certain key details about your organization’s background screening process. Reducing your policy to writing will help to ensure that it will be applied consistently across your organization. It will also create a process for applicants and employees that is fair and transparent, and help to avoid potential private litigation and governmental enforcement actions. At the very least, your policy should cover:

- what kinds of background screens you will conduct and for whom they will be conducted;

- how you will use the results in making employment decisions; and

- when you will conduct background screens.

You should not adopt any blanket policies refusing to hire applicants with any type of criminal or disciplinary record.

-

STEP 2: Check that Your Policy is Legal. Once you have created your written background screening policy, you will need to confirm that it is legally compliant. Background screening for employment purposes is regulated by a patchwork of federal, state, and local laws. The failure to comply with any one or all of them, as may be applicable, can result in a nightmare of costly penalties or fines, private or governmental lawsuits, and expensive settlements. There are four common compliance pitfalls to keep in mind:

-

Failure to Provide Written Notice and Obtain Written Authorization: Under the Fair Credit Reporting Act (FCRA), employers are required to provide written notification of a background screen for employment purposes. It must be clear and conspicuous, and perhaps most importantly, contained in a stand-alone document. The written authorization form is the applicant’s or employee’s acknowledgment that the employer will conduct a background screen and is authorized to do so. It must be signed by the employee. Neither the notice nor authorization should contain any extraneous information, such as liability waivers relating to the hiring process, the background screening results, or any employment decisions. Though seemingly simple, the statutory requirements for a compliant disclosure and authorization have resulted in a multitude of class action lawsuits and federal court decisions.

-

Failure to Follow the Multi-Step Pre-Adverse and Adverse Action Process: In addition to above, the FCRA also requires an employer to follow a multi-step process of providing additional notices to applicants or employees when the employer intends to make an adverse employment decision based upon the results of a background screen.

-

Failure to Consider Ban-the-Box and Fair Chance Laws: Ban-the-Box and Fair Chance laws are popping up all over, and there are a variety of them. However, most tend to require that employers wait to run a background screen or ask about criminal history until after a conditional offer of employment is made, and often require specific considerations before making employments decisions on a background screen.

-

Failure to Consider Anti-Discrimination Laws: In all instances, employers must ensure that they are applying the background screen process consistently and equally. It is illegal to conduct a background screen on an applicant or employee simply because of something like their race, age, national origin, sex, religion, or disability.

-

STEP 3: Consider Partnering with an Accredited Background Screening Company. A background screening company may be able to guide you through the logistics of the background screen process as well as aspects of compliance. For example, many of them will offer additional service offerings such as built-in pre-adverse and adverse action process workflows, among others. These can help take a lot of legwork off of your staff so that they can focus on other things. The key, however, is choosing the right one. An accredited background screening company can, most importantly, offer you more confidence that the results of a background screen are legally compliant and accurate. Employers, of course, remain responsible for employment related compliance documents and platforms that may be provided by your selected background screening company.

-

STEP 4: Perform Individualized Assessments and Allow for Clarification of Any Mistakes. Under guidelines established by the U.S. Equal Employment Opportunity Commission (EEOC), you have an obligation to consider whether the results of a background screen are directly pertinent to the job in question — in other words, whether they will actually impact the applicant or employee’s performance on the job. This usually comes up in the case of a criminal or disciplinary history. In making a decision regarding whether such history will exclude someone from employment, the EEOC’s guidelines provide that you should consider individualized evidence, such as: the facts and circumstances surrounding the offense or conduct; the age at the time of the offense or conduct; performance of similar work, post offense or conduct, with no known instances of criminal or disciplinary conduct; rehabilitation efforts; and employment or character references. Thus, the point is to consider whether there is a clear link between the results of the background screen and the job duties in question. In addition to the EEOC’s guidance, under the FCRA’s multi-step process described above, you must offer applicants or employees an opportunity to refute or explain any unsatisfactory information before making a final employment decision.

-

STEP 5: Make a Fully Informed Decision. You are now ready to make a fully informed and legally compliant decision. This should enable you to ensure the quality of your employment decisions and mitigate the risks associated with them.

-

STEP 6: Conduct Annual Self-Assessments of Process. Finally, you should conduct an annual audit of your background screening program. Many employers fail or forget to do so, which in turn means they miss out on a key opportunity to learn whether the program is effectively satisfying their employment decision and risk mitigation needs. An annual audit can also help you to stay current on the ever-evolving federal, state, and local laws in this area.

Employers should review their background screening process to ensure that it has all of the key attributes described above. Given the complexity and changing nature of the laws at play, consider seeking legal counsel for assistance in reviewing the process to ensure that it is legally compliant and meets the organization’s hiring needs.

Source:Wolters Kluwer, Cheetah News, HR Compliance Library What’s New, October 25, 2021; Analysis and Guidance, Background Checks 81,124. (Mathew A. Parker)

|

|

AMERICAN RESCUE PLAN ACT OF 2021

New IRS Guidance for Single-Employer Defined Benefit Pension Plans

|

|

BACKGROUND

We have previously identified some of the pension provisions contained in the American Rescue Plan Act of 2021 (ARPA). In a recent article, we touched on how this law liberalized certain of the funding rules that apply to single-employer defined benefit plans.

These new liberalized defined benefit pension rules are in sections 9705 and 9706 of ARPA and affect two of the basic components of minimum funding, which are:

- Calculation of the minimum yearly contribution necessary to pay off the “Funding Shortfall” that might occur during a year. Under previous rules, the payoff period was seven years. The new rule is fifteen years.

- Interest rates that are specified in the minimum funding calculations. The new rates are higher, which results in lower minimum funding requirements.

The above changes result in significantly lower minimum contribution requirements, as well as significantly higher funded ratio percentages. These funding ratios, referred to as “Adjusted Funding Target Attainment Percentages” (AFTAP) are extremely important and have a profound effect on plan administration. For example, an AFTAP of 100%, which generally means assets are equal to the value of earned plan benefits, is considered very good. However, if the AFTAP is at 80% or below, then the plan becomes subject to restrictions, such as not allowing lump sum distributions or amendments that increase the value of benefits.

If a plan has a history of low AFTAP’s, then in all likelihood the plan sponsor would have made plan administrative decisions necessary to be in compliance with the restrictions of the low AFTAP’s. Oftentimes these decisions would involve, for example, the reduction of existing prefunding or carryover balances, making additional contributions to avoid benefit restrictions or possibly denying a lump sum distribution to someone otherwise eligible.

The reason for the AFTAP discussion above is that for plans with low AFTAP’s and a history similar to that described above, then ARPA could favorably affect the last few years of plan administration. This could happen due to the retroactive feature of the above two rule changes, to 2019 for the Funding Shortfall amortization period and to 2020 for the higher funding interest rates. This means that for those plan sponsors who have suffered under plan restrictions or made painful decisions due to low AFTAP’s, relief may be available.

This possible relief is provided in new IRS guidance, Notice 2021-48, which describes how those restrictive situations may be alleviated retroactively.

Here is a link to the Notice.

MANNER AND TIMING OF PLAN SPONSOR ELECTIONS

The retroactive relief for the longer fifteen year Funding Shortfall must start with a plan sponsor election which provides written notification to both the plan’s enrolled actuary and the plan administrator. This election must be signed and dated by the plan sponsor and must include the following information:

- The name of the plan;

- The plan number;

- The name of the plan sponsor;

- The plan sponsor’s mailing address;

- The plan sponsor’s employer identification number; and

- The first plan year for which the 15-year amortization period will apply.

The election for the interest rate changes takes a different approach. If a plan with a history of high AFTAP’s would not benefit from the retroactive application of the changes, then the plan sponsor has the right to defer making those changes until the 2022 plan year. However, this decision to defer must be documented by the same type of election form described above, with the same information shown in items 1. through 5.

For this election form, however, the new items 6. must state that:

6. If the election is made for a plan year beginning in 2020, a statement of whether the election not to have the amendments made by section 9706 of the ARPA apply is being made for all purposes or solely for purposes of determining the AFTAP under section 436 of the Code for the plan year (i.e. the Code provisions pertaining to benefit payments).

or

6. If the election is made for a plan year beginning in 2021, a statement of whether the election not to have the amendments made by section 9706 of the ARPA apply is being made for all purposes or solely for purposes of determining the AFTAP under section 436 of the Code for the plan year (i.e. the Code provisions pertaining to benefit payments).

These elections must be made by the later of the last day of the plan year beginning in 2021 or December 31, 2021.

IMPLEMENTATION

A plan sponsor wishing to adopt these changes will need to work with the plan’s enrolled actuary as well as the company’s tax preparer. Depending on each plan and company’s unique set of characteristics, amended Form 5500’s, Schedule SB’s, revised AFTAP’s and amended tax returns may be necessary.

The plan sponsor must ensure that any plan corrective actions that result from implementation of the changes are made. An example of this might be a prohibited 2020 benefit payment not made because of a low AFTAP ratio in 2020 that becomes payable with a higher AFTAP under the new rules.

|

|

Jury Awards $10 Million in Discrimination Lawsuit |

|

A white male and former senior vice president of marketing and communication at Novant Health in Mecklenburg County, N.C., said he was fired due to the company's efforts to diversify top leadership positions. The jury determined that Novant Health failed to prove that it would have dismissed the plaintiff, who said he was replaced by a black woman and a white woman, regardless of his race. The jury’s $10 million award should serve as a wake up call and companies should ensure they are properly balancing their diversity equity and inclusion (DE&I) programs with anti-discrimination laws. |

|

IRS Updates

Q&A on Retirement Plan COVID-Related Relief

|

|

The IRS recently updated its questions and answers regarding COVID-related relief for retirement plans and IRAs.

The IRS originally made the Q&A available in accordance with relief contained in Section 2202 of the CARES Act, enacted on March 27, 2020, which provides for special distribution options and rollover rules for retirement plans and IRAs and expands permissible loans from certain retirement plans.

Specifically, the IRS added the following two questions related to rehires following bona fide retirement and in-service distributions.

Rehires Following Bona Fide Retirement; In-Service Distributions

Q1. A qualified pension plan that does not provide for in-service distributions commences benefit distributions to an individual who applies for retirement benefits and experiences a bona fide retirement. If the plan sponsor rehires the individual due to unforeseen hiring needs related to the COVID-19 pandemic, will the rehire cause that individual's prior retirement to no longer be considered a bona fide retirement? (added 10/22/2021)

A1. Generally, no. Treasury regulations generally require a qualified pension plan to be maintained primarily to provide systematically for the payment of definitely determinable benefits over a period of years, usually for life, after retirement or attainment of normal retirement age. See Treas. Reg. § 1.401(a)-1(b)(1)(i).

Accordingly, a plan that does not permit in-service distributions may commence benefit distributions to an individual only when the individual has a bona fide retirement. Although the determination of whether an individual's retirement under a plan is bona fide is based on a facts and circumstances analysis (in the absence of plan terms specifying the conditions under which a retirement will be considered bona fide), a rehire due to unforeseen circumstances that do not reflect any prearrangement to rehire the individual will not cause the individual's prior retirement to no longer be considered a bona fide retirement under the plan. For example, if a public school district sponsoring a qualified pension plan experiences a critical labor shortage due to the COVID-19 pandemic that was unforeseen at the time of an individual's prior bona fide retirement, the public school district rehires the individual to help ease the labor shortage, and the plan terms do not define a bona fide retirement in a way that prevents the rehire, the individual's reemployment would not cause the prior retirement to fail to be a bona fide retirement. Consequently, if plan terms permit, benefit distributions could continue after the rehire.

In addition, if the sponsor of a qualified pension plan wishes to rehire a retired employee to fill an unforeseen hiring need related to the COVID-19 pandemic, the sponsor should analyze the impact of the rehire under the plan by taking into account any plan terms, including any need for plan amendments, relating to rehires. For example, plan sponsors should review any plan terms requiring that an individual who retires and commences benefit distributions not be rehired within a specified period, any plan terms relating to the suspension of distributions upon rehire, and any other plan terms that may have an impact on the pension benefit of a rehire.

Q2: May a qualified pension plan permit individuals who are working to commence in-service distributions? (added 10/22/2021)

A2: Yes. A qualified pension plan generally may allow individuals to commence in-service distributions if the individuals have attained either age 59½ or the plan's normal retirement age. See Internal Revenue Code section 401(a)(36) (in-service distributions generally permitted at age 59½); final regulations on distributions from a pension plan upon attainment of normal retirement age (Treas. Reg. § 1.401(a)-1(b), TD 9325, 72 FR 28604); proposed regulations on the applicability of the normal retirement age regulations to governmental pension plans (Prop. Treas. Reg. § 1.401(a)-1(b)(2)(v), 81 FR 4599); and Section F of Notice 2020-68, 2020-38 IRB 567 (regarding recent changes to in-service distribution rules under § 401(a)(36).

However, distributions commencing to an individual before age 59½ may be subject to a 10% additional tax under Internal Revenue Code section 72(t), unless the distributions fit within an exception to that tax (for a description of the exceptions to the 10% additional tax under section 72(t), see Retirement Topics - Exceptions to Tax on Early Distributions).

Click here for the complete list of Q&As.

Click here for the complete text of the CARES Act.

Taken From IRS.com/newsroom

|

|

What Would You Like To See In A Future Issue? |

|

|

JUST OUT FROM THE IRS

Payroll Taxes

|

|

IRS reminds employers to e-file payroll tax returns timely

WASHINGTON — The Internal Revenue Service today reminded employers that the next quarterly payroll tax return is due November 1, 2021. The IRS urges employers to use the speed and convenience of filing the returns electronically.

E-filing is the most accurate method to file returns and saves taxpayers time by performing calculations and auto-populating forms and schedules with a step-by-step process. The IRS acknowledges receipt of e-filed returns within 24 hours, giving taxpayers reassurance that their return was not misplaced or lost in the mail. Electronically filed returns reduce processing time and have fewer errors, which reduces a taxpayer's chance of receiving an IRS notice. E-file users also receive missing information alerts.

Two options for electronically filing payroll tax returns:

The IRS requires all authorized IRS e-file providers to ensure only authorized users have access to secure information. Only the business owner, authorized signers and reporting agents can apply for an online signature PIN. Third parties (such as attorneys, CPAs, tax return preparers or other tax professionals) can't request a PIN on behalf of the business, nor can they use the PIN to sign returns on behalf of their clients. For more information on electronic filing of payroll tax returns, see the E-file Employment Tax Forms page.

COVID-related Employer Tax Credits

The employer tax credits for qualified sick and family leave wages gives all American businesses with fewer than 500 employees funds to provide their employees with paid leave, either for the employee's own health needs or to care for family members. The American Rescue Plan of 2021 further amended and extended the tax credits (and the availability of advance payments of the tax credits) for paid sick and family leave. See Notice 2021-24 for guidance on the ability to reduce deposits and request advances for the credits for periods of leave through September 30, 2021.

The Employee Retention Credit is a refundable tax credit against certain employment taxes equal to 50% of the qualified wages an eligible employer pays to employees. The modified and extended credit is available for qualified wages paid before January 1, 2022. Generally, the rules for the Employee Retention Credit for the second quarter of 2021 and the third and fourth quarters of 2021 are substantially similar. For more information about other coronavirus-related tax relief, visit IRS.gov/coronavirus.

The IRS encourages employers to help get the word out about the advance payments of the Child Tax Credit. Employers have direct access to many who may receive this credit. More information on the Advance Child Tax Credit is available on IRS.gov. The website has tools employers can use to deliver this information, including e-posters, drop-in articles (for paycheck stuffers, newsletters) and social media posts to share. For more information see Advance Child Tax Credit Payments.

Taken from e-News for Tax Professionals 2021-42

Page Last Reviewed or Updated: 20-Oct-2021

|

|

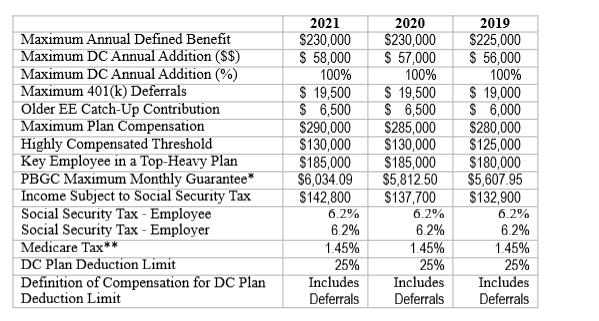

2021 Retirement Plan Limits |

|

All limits are based on the calendar year. |

|

If you have not received our business card with these numbers printed on it and would like one, please let us know! We would be happy to mail you one (or a few to share!) |

|

-

Michael F. Yates & Company, Inc. can help you with a variety of services ranging from retirement plans to providing results-oriented survey instruments, training and development programs for your employees. Our products and services are intended to help you maximize the effectiveness of your Human Resources function.

- These products and services incorporate our years of experience so that you receive rapid results and exceptional value. From onsite consulting, to strategic business integration, to Web enablement, we understand how Human Resources can be applied to solve your problems and achieve your goals. As a result, we can help you get the most out of your investment and turn your most precious resource into a competitive advantage.

- We offer Consulting, Retirement Planning, Pension and 401(K) both qualified and non qualified Plans, Welfare Plans, Communications, Computer Systems, Executive Plans, Compensation, Mergers, Acquisitions, Divestitures and Other Services.

- We offer a true and honest, Client Partnership.

|

|

Our staff and firm are proud members of the following professional organizations:

Society of Actuaries

American Society of Pension Professionals & Actuaries

Society for Human Resource Management

(Sussex-Warren NJ Chapter)

GAPS (Global Association Pension Services)

WorldatWork

American Management Association

National Federation of Independent Business

Better Business Bureau

|

|

101 Belvidere Avenue

P.O. Box 7

Washington, NJ 07882-0007

908-689-4200

|

|

Terms of Use

The site ("from the HR perspective" hence herein referred to as MFYCO.com) is made available by Michael F. Yates & Company Incorporated. All content, information and software provided on and through 'from the HR perspective' and MFYCO.com ("Content") may be used solely under the following terms and conditions ("Terms of Use".) YOUR USE OF THIS WEBSITE CONSTITUTES YOUR AGREEMENT TO BE BOUND BY THESE TERMS AND CONDITIONS. IF YOU DO NOT AGREE TO THESE TERMS, YOU SHOULD IMMEDIATELY DISCONTINUE YOUR USE OF THIS SITE.

Michael F. Yates & Company, Inc. believes strongly in protecting the privacy of its users. Click here to view our privacy policy.

As always, any statements regarding federal tax law contained herein are not intended or written to be used, and cannot be used, for the purposes of avoiding penalties that may be imposed under federal tax law or to market any entity, investment plan or arrangement.

|

|

|

|

|

|

|