Human Resource Consulting From The Business Viewpoint |

|

Human Resource Update | September 2021 |

|

Will the new tax proposals pass? Will they pass in whole or in part? While we do not know if they will pass in whole, the odds are that they will pass in part, not because there is agreement to fund the many new programs being proposed, but to fund the real infrastructure programs that are desperately needed. At this moment, it appears that whatever is passed will not have an effective date in 2021, but a date, probably January 1st, in 2022.

WHO ARE THE TARGETS

Both individuals and businesses are targets. We will address individuals at this time as our suggestions relate to what individuals and companies can do to lessen the impact of the proposals on individuals.

As you will see, the proposals impose burdensome taxes on not only an individual basis but on a joint filer basis. Most of the new proposals target those with incomes over $400k for singles and $450k for joint filers. We will refer to them collectively as “Upper Earners”. This makes two things evident that go against our normal way of thinking: 1) a married couple may be better off if they divorce and file as two single individuals and, 2) compensation programs that are the territory of upper-level executives might be offered to mid-level and possibly lower-level management. We are not advocating (1) and will cover (2) as well as other suggestions later.

BY THE NUMBERS AND SUGGESTIONS

INDIVIDUAL RATES

Individual tax rates will reach as high as 39.6% for Upper Earners. Plus, a 3% tax on AGI income over $5m. When State income taxes are added to this, the residents in some States will have a top marginal rate of over 61%. While there are discussions that could eliminate the SALT deduction exclusion (State And Local income Tax), that elimination may be hobbled for anyone who is an Upper Earner.

Suggestions

Accelerate Income - If you are an Upper Earner you should consider accelerating as much income possible from 2022 into 2021. This is particularly important if you are a joint filer. Companies should consider paying bonuses that are normally paid in the first part of 2022 in December 2021. If the exact amount of the bonus cannot be determined, a percentage of the estimated bonus, such as 80% or 90% could be paid. In determining to whom this acceleration should apply, remember that an Upper Earner now includes the income from a joint filer. Of course, deferred income that is scheduled to be paid in 2022 cannot be accelerated.

Defer Income - If you are an Upper Earner and can defer 2022 income to a later year or years in which you project the applicable marginal rate on the payment of such deferral and any earnings thereon will be less, you should do so. Again, when deciding how much to defer, remember that an Upper Earner now includes the income by a joint filer. If your deferred compensation plan does not include a provision to re-defer previously deferred amounts, you should have your plan amended to include this type of provision. A plan may permit an unlimited number of such re-deferrals provided they meet the criteria prescribed by regulation. Also remember that the election to defer must be made before any income to which it applies is earned. The law contains two exceptions: there is a 30-day exception for newly eligible participants and, a participant may defer an annual performance related bonus at least six months before the performance period ends.

Open Up Deferred Income Plans - The change in the taxation of joint (usually married) filers means more individuals will be taxed at higher rates. This means that it is possible that mid-level and even lower-level management would benefit from a deferred compensation plan.

Of course, a company’s board must approve the creation or extension of a plan and any deferral must be done in conjunction with such plan or individual employment agreement. This should be brought to the attention of the COO and CEO as soon as possible. If it is not possible to implement a plan before 2022 begins, compensation earned after the date of adoption can still be deferred.

LONG-TERM CAPITAL GAINS RATES

For Upper Earners, Long-Term Capital Gains Rates will increase to 25% (28.8% when the 3.8% surtax on investment income is added) if the transaction occurs after September 12, 2021, unless you have a signed sales agreement prior to September 13, 2021. Other more onerous proposals have been made but seem to have waned at this moment.

While many may think this increase will not apply to them, the sale of their principal residence may trigger this higher rate if after the $250k/500k exclusion there is a good profit.

Suggestions

Hold or Match - If you believe the investment was made is sound and you can hold it until your income level drops, or you can, and probably should have already, matched losses to gains.

Gift - If you have children to whom you would be gifting money, if they are not Upper Earners, you can give them the stock rather than selling it and then gifting the proceeds on which you would pay taxes at a rate higher than theirs.

1031 - You can also use a 1031 exchange, that is rolling over the investment proceeds from one property to another within 180 days.

Donate - A gift to charity in lieu of cash may also be a good idea.

RETIREMENT PLANS

If you are an Upper Earner and if assets in a traditional or Roth IRA, and defined contribution accounts, in the aggregate, exceed $10m at the end of a year, no matter the individual’s age(s), there is a minimum required distribution of the previous year’s contribution. If the aggregate balance is over $20m there is a mandatory distribution of the excess over $20m in addition to the foregoing.

In brief, if you are an Upper Earner, rollovers to a Roth IRA will no longer be permitted.

After tax employee contributions to employer sponsored (tax qualified) plans will be discontinued.

At this moment, there is no proposal to include the present value of a defined benefit plan in the calculation of the aggregate value that would require a mandatory distribution.

Suggestions

Deferred Compensation - Consider deferring all future amounts via a deferred compensation plan.

Defined Benefit (“DB”) Pension Plan – Many companies have eliminated or set aside their DB plan. While not many companies do so, the establishment of a DB plan for highly compensated individuals with a lower benefit for a portion of non-highly compensated employees may be possible. This requires the existence of a defined contribution plan, for example a 401(k) plan to which the company makes contributions for all non-highly compensated employees using a “safe-harbor” type of contribution. This combination of benefits must be actuarially tested each year to ensure the deductibility of the contributions.

CONCLUSION

We will continue to monitor the proposed law and comment as soon as practical. In the meantime, please remember that this letter is not to be considered personal tax advice and we suggest that you seek such from your tax advisor or counsel.

As always, if we can help in any way, please reach out.

|

|

Michael F. Yates

President

|

|

If you find value in this newsletter please let us know. Feel free to call me with a comment and/or ask a question at any time (908-689-4200) or send me an email ([email protected]). We offer this timely information as another benefit of your relationship with our company. If you feel a friend or colleague would benefit from receiving our newsletter, please feel free to forward a copy.

You can view all of our newsletters by clicking the 'newsletter archives' link at our company website www.mfyco.com.

|

|

Future Prospects for Employee Health Care Costs |

|

Dazed, shell shocked survivors, stumbling out blinking into the sunlight, picking through the rubble, wondering how they can rebuild their shattered world ….

No, this article is not about the brave inhabitants of Tornado Alley. Instead, it concerns another group of brave, shell shocked survivors, i.e. current day business owners and human resource managers. Its goal is to assist this group, having survived the past year and a half of economic mayhem, as they survey the present-day environment and attempt to plan for the future.

One of the major areas for planning is employee benefits, and in particular, the costs for employee health care. The year 2020 saw many behavioral changes that were imposed upon the American public in response to the COVID pandemic. These behavioral changes led, in turn, to business changes, which taken all together, could have significant effects on future health costs.

Studies have been published that take into account these new developments from 2020 and estimate their impact on future health costs. An example of this is from PwC’s Health Research Institute (HRI) which makes a projection of the medical cost trend rate for 2022. Here is an excerpt from that study:

“PwC's Health Research Institute (HRI) is projecting a 6.5% medical cost trend in 2022, slightly lower than the 7% medical cost trend in 2021 and slightly higher than it was between 2016 and 2020. Healthcare spending is expected to return to pre-pandemic baselines with some adjustments to account for the pandemic’s persistent effects.”

This projected trend rate was calculated considering the new 2020 behavioral changes that tend to INCREASE health costs and also those that should DECREASE costs. Some examples are:

INCREASE

1. Necessary care that was postponed during the pandemic will resume being performed currently.

2. Mandated stay-at-home requirements increased problems associated with sedentary behavior.

3. Mental health and drug abuse cases are projected to increase.

4. Increased expenses as health care providers and suppliers make capital investments to become better equipped for future medical emergencies.

5. Health providers are moving to replace on-site patient care with remote digital access. The net result is anticipated improved communication and outcomes, but overall higher initial expense.

DECREASE

1. The remote digital access between doctor and patient discussed above will decrease the need for real estate and physical offices, since much of the care will be done remotely from home.

2. Technology-based expenses should also be lower as these remote work-from-home arrangements will become more common.

An outline of the HRI study can be accessed by clicking here.

The projected trend rate information contained in this report could possibly assist owners and managers in constructing their budget estimates for 2022.

|

|

Form 5310 Electronic Submission

IRS Form 5310, Application for Determination for Terminating Plan, must be submitted electronically online at www.Pay.gov. Paper submissions will be returned to the applicant.

The current user fee is $3,500 ($4,500 for multiple employer plans.) Some plans may qualify for the zero-dollar user fee. See Revenue Procedure 2021-4 for information on the latest procedures and user fees for determination letter requests.

Multiemployer Plans Receiving PGBC Assistance

Notice 2021-38 (PDF) provides guidance under the American Rescue Plan Act of 2021 about the special assistance paid by the Pension Benefit Guaranty Corporation to eligible multiemployer defined benefit plans that are financially at risk.

|

|

Form I-9: Updated Receipts Guidance |

|

Over the past several months, the Department of Homeland Security (DHS) has worked with its inter agency partners Immigration and Customs Enforcement (ICE) and the Department of Justice’s (DOJ) Immigrant and Employee Rights Section (IER) to provide employers with updated guidance on acceptable receipts.

- When employees present a receipt showing that they applied to replace a List A, B, or C document that was lost stolen or damaged, they should show their employer the replacement document for which the receipt was given. However, this is not always possible due to document delays, changes in status, or other factors.

- If the employee does not present the original document for which the previously provided receipt was issued but presents, within the 90-day period, another acceptable document (or documents) to demonstrate his or her identity and/or employment authorization, employers may now accept such documentation.

- In cases where an employee presents a document (or documents) other than the actual replacement document, the employer should complete a new Section 2 and attach it to the original Form I-9. In addition, the employer should provide a note of explanation either in the Additional Information box included on page 2 of the Form I-9 or as a separate attachment.

|

|

Federal Contractors Must Be Vaccinated by December 8th |

|

Click here to see the guidance issued by President Biden on September 24th.

|

|

Cryptocurrencies are currently one of the hottest topics in the world, and for good reason. Bitcoin’s fluctuations over the past year – from $10,000 in July 2020 to $63,000 in April 2021 and now settled to around $41,000 – has some employees and retirees asking to include cryptocurrencies in their employer-sponsored 401(k) retirement plans. The potential for negative valuation swings, on the other hand, has others saying they might be too risky for retirement savings. This Insight will provide six key considerations for Plan sponsors before considering including a cryptocurrency option in your retirement plans.

General Overview of 401(k)s

Plan sponsors hold in trust the retirement assets of 401(k) plans they’re responsible for overseeing. According to the Employee Retirement Income Security Act of 1974 (ERISA), individuals making decisions about the plan serve as fiduciaries. It is well-settled law that fiduciaries must act exclusively in the best interest of the plan participants and beneficiaries. This includes ensuring that plan assets are diversified, understanding the fee structures to ensure reasonability, and carefully selecting and monitoring managers and service providers.

ERISA does not dictate which specific types of investment options must be included in a 401(k). Rather, the law instructs fiduciaries to show the care, skill, prudence, and diligence that a prudent person would exercise when choosing an investment option to minimize the risk of large losses. The focus is on the process, rather than the investment returns.

Many employers utilize an Investment Policy Statement (IPS) to help govern the 401(k) management by the plan fiduciaries. An IPS will often contain provisions for the fund selection process, the frequency and factors used in monitoring performance, and asset allocation targets. Deviation from the IPS guidelines can serve as evidence of a breach of fiduciary obligations. This could result in employer and individual liability.

Four Cryptocurrency Risks With 401(k)s

In a typical 401(k), an employer offers its employees limited investments, such as ETFs, mutual funds, and sometimes company stock. This is because of the employer’s role as a fiduciary and the risks associated with making inappropriate investment choices. Indeed, one of the most common reasons 401(k) participants sue their employers is due to inappropriate investment choices.

Cryptocurrency as a 401(k) investment option would be an exotic choice by current standards, and would present several risks, including:

-

Cryptocurrency doesn’t quite fit the definition of traditional investment vehicles. Depending on how it is drafted, the IPS might be construed as prohibiting cryptocurrency, even if it does not expressly do so.

-

The IPS guidance for selecting investments to offer may not speak to the unique issues involved in evaluating cryptocurrencies and amendments may be required.

-

Cryptocurrencies have a history of dramatic declines in value, putting the fiduciaries at risk for losses and risking the employer’s public reputation.

-

If fees associated with offering cryptocurrency in the plan are significantly greater than those of the other investments available, the fiduciaries may be at risk for a breach of duty claim (an issue currently pending before the United States Supreme Court).

Why Consider a Crypto 401(k)?

Given the potential risks, employers may ask: why bother? There are several reasons why, as an employer, you may want to consider giving your employees the option to invest in cryptocurrency through their 401(k):

Cryptocurrencies are Available

Cryptocurrencies are not prohibited as an investment option in a 401(k) plan by ERISA. In addition, as cryptocurrencies such as bitcoin and ether become more mainstream, regulating bodies have taken note. For example, the Office of the Comptroller of the Currency (OCC) recently ruled that national banks can hold cryptocurrency and can manage cryptocurrencies in the way they manage other assets.

Cryptocurrency-Related Benefits Could Attract Talent

Simply put, more employees want to invest in cryptocurrency, and they want to use retirement accounts to do so. Most employers are not yet providing their employees with this option. Employers that do may be at an advantage when it comes to attracting and retaining talent, especially at a time when many employers are struggling to do so.

401(k)s Provide Tax Advantages

Utilizing a 401(k) to buy cryptocurrency allows employees to take advantage of 401(k) tax incentives, whether they use a tax-deferred 401(k) or Roth 401(k). Buying cryptocurrency in a traditional 401(k) of Roth 401(k) means that employees could invest in cryptocurrencies without needing to worry about the complexity of tracking cryptocurrency trades to calculate any taxes they may owe resulting from buying or selling.

Six Crypto 401(k) Considerations for Employers

Before deciding to offer cryptocurrency in your 401(k) plans, you should consider the following six concepts:

1. You should confirm with your 401(k) provider whether providing cryptocurrency is an option.

2. You should evaluate the IPS to insure there are no provisions expressly prohibiting cryptocurrencies from inclusion in the plan.

3. You should ensure that fiduciaries follow all steps in their IPS for selection and performance monitoring of new asset class.

4. You may want to consider some type of limit on the amount an individual can commit to crypto to reduce potential risk associated with volatility.

5. You should keep participation in a Crypto 401(k) optional. Ideally, employees would be able to choose from among a list of cryptocurrencies which they want to hold in their 401(k) portfolios – but most importantly, they must be able to choose whether they want to include them at all.

6. Decisions related to retirement investments are arguably the most important an individual can make in their lifetime. You should be sure that you, or your retirement benefits provider, can give employees necessary informational materials on cryptocurrencies to ensure employees aren’t going it alone when making critical investment decisions for their future. Despite the increased popularity of cryptocurrencies, it should not be assumed that a would-be investor knows the difference between a meme coin and the more established coins.

Conclusion

The world and the employment space continue to change rapidly. Employees want to have autonomy in everything they do, including their retirement options. As cryptocurrency continues to gain adoption and the number of cryptocurrency retirement providers continue to grow, we expect more employees will begin asking about the availability of cryptocurrency retirement accounts.

Crypto retirement plans, however, are not without risks. As a result, substantive evaluation with legal counsel trained on these issues is necessary before making a determination about which path is right for you.

|

|

What Would You Like To See In A Future Issue? |

|

|

As the Biden Administration commemorated the 31st anniversary of the ADA, the Departments of Justice (DOJ) and Health and Human Services (HHS) jointly published guidance on how "long COVID" can be a disability under the ADA, Section 504 of the Rehabilitation Act and Section 1557 of the Affordable Care Act. The guidance also explains how these laws that protect people with disabilities from discrimination may apply. Although the guidance is not targeted to the employment landscape, it offers information that will help employers understand "long COVID" and how it may impact employees and give rise to the need for a reasonable accommodation in the workplace. Although the EEOC has not yet provided guidance related to long COVID, the Department of Labor has published a blog addressing the sort of workplace accommodations to which employees with long COVID may be entitled.

Long COVID. Some people continue to experience symptoms that can last weeks or months after first developing COVID-19, the guidance notes. This can happen to anyone who has had COVID-19, even if the initial illness was mild. People with this condition are sometimes called "long-haulers," and the condition they have is known as "long COVID."

According to the CDC, people with long COVID have a range of new or ongoing symptoms that can last for weeks or months after they are infected with the virus that causes COVID-19. The symptoms can worsen with physical or mental activity. Some of the common symptoms of long COVID include:

- Tiredness or fatigue

- Difficulty thinking or concentrating (brain fog)

- Shortness of breath or difficulty breathing

- Headache or Dizziness on standing

- Fast-beating or pounding heart (heart palpitations) or Chest pain

- Cough

- Joint or muscle pain

- Depression or anxiety

- Fever

- Loss of taste or smell

Some people also experience damage to multiple organs including the heart, lungs, kidneys, skin, and brain.

Long COVID can be a disability. Long COVID can be a disability under the ADA, Section 504, and Section 1557 when it substantially limits one or more major life activities. Under these laws and their related rules, a person with a disability is defined as an individual with a physical or mental impairment that substantially limits one or more of the major life activities of the individual (actual disability); a person with a record of such an impairment (record of); or a person who is regarded as having such an impairment (regarded as). A person with long COVID has a disability if the person’s condition or any of its symptoms is a "physical or mental" impairment that "substantially limits" one or more major life activities. The new guidance addresses the "actual disability" part of the definition, but not the "record of" and "regarded as" parts.

Physical or mental impairment. A physical impairment includes any physiological disorder or condition affecting one or more body systems, including the neurological, respiratory, cardiovascular, and circulatory systems. A mental impairment includes any mental or psychological disorder, such as an emotional or mental illness.

According to the guidance, long COVID is a physiological condition affecting one or more body systems. Some people with long COVID experience:

- Lung damage

- Heart damage, including inflammation of the heart muscle

- Kidney damage

- Neurological damage

- Damage to the circulatory system resulting in poor blood flow

- Lingering emotional illness and other mental health conditions

Thus, long COVID is a physical or mental impairment under the ADA, Section 504, and Section 1557, the guidance states.

Substantially limits a major life activity. Long COVID can also substantially limit a major life activity. The guidance notes that situations in which an individual with long COVID may be substantially limited in a major life activity are diverse and offers the following possible examples:

- A person with long COVID who has lung damage that causes shortness of breath, fatigue, and related effects is substantially limited in respiratory function, among other major life activities;

- A person with long COVID who has symptoms of intestinal pain, vomiting, and nausea that have lingered for months is substantially limited in gastrointestinal function, among other major life activities; and

- A person with long COVID who experiences memory lapses and "brain fog" is substantially limited in brain function, concentrating, and/or thinking.

Individualized assessment required. Long COVID is not always a disability, the guidance points out, advising that an individualized assessment is necessary to determine whether a person’s long COVID condition or any of its symptoms substantially limits a major life activity. The CDC and health experts are working to better understand long COVID, according to the guidance.

Reasonable accommodations for the public. People whose long COVID qualifies as a disability are entitled to the same protections from discrimination as any other person with a disability under the ADA, Section 504, and Section 1557. This may mean that businesses or state or local governments will sometimes need to make changes to the way that they operate in order to accommodate a person’s long COVID-related limitations. For people whose long COVID qualifies as a disability, reasonable modifications may include:

- Providing additional time on a test for a student who has difficulty concentrating;

- Modifying procedures so that a customer who finds it too tiring to stand in line can announce their presence and sit down without losing their place in line;

- Providing refueling assistance at a gas station for a customer whose joint or muscle pain prevents them from pumping their own gas; or

- Modifying a policy to allow a person who experiences dizziness when standing to be accompanied by their service animal that is trained to stabilize them.

Reasonable workplace accommodations. As to what workplace accommodations an employee with long COVID may seek, the DOL’s blog provided some general categories of accommodations:

- Providing or modifying equipment or devices;

- Part-time or modified work schedules;

- Reassignment to a vacant position; and

- Adjusting or modifying examinations, training materials or policies.

The DOL also provided a list of things that employers are not required to do:

- Remove essential job functions;

- Lower production standards;

- Provide personal needs items such as hearing aids and wheelchairs;

- Provide any accommodation that creates an undue hardship; and

- Provide an employee’s preferred accommodation as long as the employer provides an effective accommodation.

Documentation and further information. As to the information that an employer may request when an employee asks for an accommodation, the DOL said that employers can ask the employee to provide limited medical documentation to show that they are covered under the ADA if it isn’t obvious that they have a disability or need an accommodation. Employers can also ask questions to help clarify why the employee needs an accommodation and to explore alternative accommodations, if necessary.

Employers cannot ask for documentation that is unrelated to determining the existence of the employee’s disability and the necessity for an accommodation, according to the DOL. Employers also may not ask about other medical conditions that the employee might have or request their complete medical records.

Temporary and changing limitations. Can an employee get an accommodation if they only need it temporarily or if their limitations change over time? Yes, the DOL said. "If you are a qualified individual with a disability, your employer must consider providing accommodations for any limitations you have related to your disability, even if temporary or episodic, for when they are needed," the blog states.

More resources. The DOJ/HHS guidance, along with a directory of resources available through programs funded by the Administration for Community Living (ACL), was shared by the White House as part of a comprehensive package of resources for people with long COVID. The Department of Labor also has a webpage that includes comprehensive resources.

Source: Wolters Kluwer, Pension News July 29, 2021, by Pamela Wolf, J.D.

|

|

Thank God it’s Thursday - Making the Case for a Four-Day Workweek |

|

Americans are widely credited with working longer hours than their global counterparts, and the constant demands of technology and 24/7 communication mean work is harder to turn off.

But a growing number of companies and workplace experts are pushing back against the relentless pace of work, suggesting the four-day workweek is not just the key to happiness, but the answer to creating a more productive workforce.

“Employers are much more aware that there is a work-life balance that employees seek,” says Ryan Gatto, district president for Robert Half, an employee staffing agency. “Employees have been able to prove that they can be just as productive in a condensed week because people are looking to have a healthy balance between your professional life and your personal life.”

While the policy has made headlines recently, with Microsoft Japan reporting success with the revised schedule, shifting to a shorter week has been a workplace prediction for decades. In 1956, then Vice President Richard Nixon predicted the four-day workweek would eventually become part of work culture.

But Americans have traditionally been overworked. In the early part of the 20th century, employees were expected to work six or seven days a week for 10 hours or more, and workers had little protection or rights. In one devastating incident in 1911, 145 workers were killed in a fire because they were trapped inside the Triangle Shirtwaist Factory. The factory owners had locked their employees in the building to keep them working.

In 1914, the Ford Motor Co. made a surprising decision for the period: announcing it would pay its male factory workers a minimum wage of $5 per eight-hour day, a rise from the previous rate of $2.34 for nine hours. In 1926 Ford became one of the first companies in the country to adopt a five-day, 40-hour week.

But it would take decades of lobbying and organizing, along with legal changes, before other employers would do the same. The 40-hour workweek became the standard in 1940, and even now a majority of employers expect their workers to adhere to a Monday through Friday schedule.

But with burnout rates on the rise and workplace productivity losses costing money, employers may want to consider transitioning to a condensed schedule.

While just 15% of employers currently offer this schedule, according to the Society for Human Resource Management, the rise of flexible and remote working arrangement as well as advancements in technology and automation are pushing this idea toward becoming reality for more workers.

“With all the tools that we have available for people to work more remotely, employees can lean on technology if they're working from home or if they take one additional day off,” Gatto says.

Andrew Barnes, founder of the New Zealand-based investment advisory firm Perpetual Guardian, was curious about his own company’s workflow after he read a startling statistic that employees were productive for only two and a half hours a day.

His solution? Implementing a four-day workweek at the firm. Employees had the opportunity to take a day off, while still receiving their usual five-day salary. “I thought if I offered my staff a day off a week, would they change the way they worked so they could be as productive in four days rather than five?” Barnes says.

It didn’t take long to see results: after 12 months, the program was so successful that the firm decided to make it a permanent part of the employee experience. Almost 80% of the staff at Perpetual Guardian has opted for the four-day workweek program.

“Because we’ve seen the benefits in our own business, we think it’s something worth pushing,” Barnes says. “We got a 40% improvement in engagement, stress levels dropped by 15% and more people said they were better able to do their job.”

Work-related stress plagues 83% of employees, according to data from the American Institute of Stress. Stressed out employees are less effective at work and struggle with mental health issues like depression and anxiety.

“Feelings of overwork can take a toll on healthy behaviors like sleep, exercise and eating, as well as emotional and cognitive well-being,” says Carrie Bulger, a psychology professor at Quinnipiac University. “For most people, overwork also results in some performance issues, like making more errors or taking longer to complete tasks than they normally would.”

Wildbit, a fully remote staffed software company, is going into its third year on a four-day work schedule. CEO Natalie Nagele says the change has improved productivity and employee wellness, while also teaching the organization about the way employees work.

“After the first year, we reflected and all agreed that we had delivered more of our product than we had in previous years,” Nagele says. “We accounted a lot of that to the four-day workweek because we were so intentional in the work that we were doing.”

Employees had to commit to and change certain behaviors in order to meet those goals and make the most out of that third rest day.

“There’s no natural law that says we have to work 40 hours a week,” Nagele says. “We’ve only been doing that a short time, historically. And if anything we should be scaling that down consistently. There’s no reason to hold on to it so tightly like they do in the corporate world.”

Other employers have been experimenting, with promising results. Microsoft Japan saw a 40% increase in productivity when the organization implemented a four-day workweek over the summer.

“Work a short time, rest well and learn a lot,” Microsoft Japan president and CEO Takuya Hirano said in a statement on Microsoft Japan’s website. “I want employees to think about and experience how they can achieve the same results with 20% less working time.”

Shake Shack announced in November that it would be expanding its four-day workweek test after positive feedback from restaurant managers.

“The recruiting possibilities are huge,” Shake Shack CEO Randy Garutti said during the company’s earning call, according to reports. “This is not something you take lightly or roll out too quickly. We are cautious about it. We are excited about it. We’re looking to learn.”

As interest in the success of these programs has grown, Barnes and his business associate Charlotte Lockhart founded 4 Day Week Global, a nonprofit platform for like-minded people who are interested in supporting the idea of the four-day week as a part of the future of work. The organization provides employers with research and strategy recommendations for implementing a four-day workweek.

“We developed 4 Day Week Global to be that community and help create a more coordinated repository for information and help,” says Lockhart, who serves as the organization’s CEO.

Not everyone who experiments with the four-day workweek will decide they ultimately want to keep it. Ryan Carson, founder and CEO of the programming company Treehouse, established a four-day schedule for his employees in 2015, but ended up returning to a five day schedule in 2016.

There was a fundamental decline in the work ethic as a result of the reduced schedule, Carson told GrowthLab’s Ramit Sethi. This ended up being a detriment to the business and its mission, he says in a video of their conversation.

“The challenge for many employees is that it's not a one size fits all and it almost needs to be based upon individual performance, individual accountability, and not rolled out as a blanket statement for their entire workforce,” says Gatto, of Robert Half. "By compressing the workweek to four days, you are empowering those that can be responsible and accountable to their work. But, of course, there could be those individuals who take advantage of it and are not as productive."

Even positive results don’t happen overnight. For employers unsure where to begin, Barnes suggests running a trial. During that time, offer a shorter workweek and measure employee productivity and engagement and listen to their feedback.

“The trial is your safe space,” Barnes says. “The worst that can happen is an employer sits down and has a conversation with employees and says, ‘Hey, we’re going to try this and see if it works.’”

Barnes says it gives management the opportunity to work out the productivity benchmarks. It is also a good way of identifying problems in the business that are acting against getting the best productivity. But, despite the benefits, Barnes and Lockhart still say employers are reluctant to embrace the idea because they can’t see it working at their organization.

And even the employees are cautious at first. At Perpetual Guardian, Barnes said employees were skeptical that the company would actually pay them for five days when they work only four.

“What this is really about is having a very mature and open conversation with your employees,” Barnes says. “There is personal responsibility from both a leadership perspective and an employee perspective.”

Wildbit’s Nagele says the success of the four-day workweek has allowed her to reflect and reassess her purpose and goals. “My mission is to create a business that services human beings,” she says. “To be able to experiment and say, ‘Hey, can we do the same work in less time and I don’t have to dock anybody’s pay’ and to see it succeed is extremely rewarding. I believe the fulfillment for workers comes from being given the space to do the work that they’re hired to do.”

Taken from: Employee Benefit News, January 24, 2020

By Amanda Schiavo, Associate Editor with additional reporting by Alyssa Place

|

|

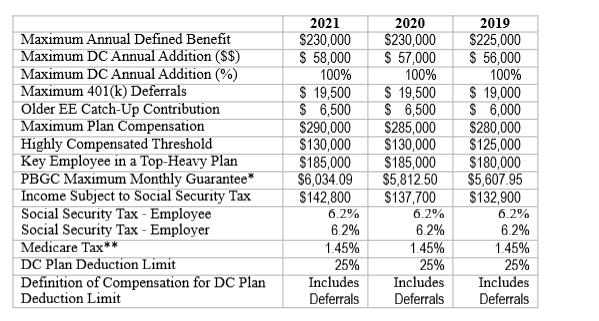

2021 Retirement Plan Limits |

|

All limits are based on the calendar year. |

|

If you have not received our business card with these numbers printed on it and would like one, please let us know! We would be happy to mail you one (or a few to share!) |

|

-

Michael F. Yates & Company, Inc. can help you with a variety of services ranging from retirement plans to providing results-oriented survey instruments, training and development programs for your employees. Our products and services are intended to help you maximize the effectiveness of your Human Resources function.

- These products and services incorporate our years of experience so that you receive rapid results and exceptional value. From onsite consulting, to strategic business integration, to Web enablement, we understand how Human Resources can be applied to solve your problems and achieve your goals. As a result, we can help you get the most out of your investment and turn your most precious resource into a competitive advantage.

- We offer Consulting, Retirement Planning, Pension and 401(K) both qualified and non qualified Plans, Welfare Plans, Communications, Computer Systems, Executive Plans, Compensation, Mergers, Acquisitions, Divestitures and Other Services.

- We offer a true and honest, Client Partnership.

|

|

Our staff and firm are proud members of the following professional organizations:

Society of Actuaries

American Society of Pension Professionals & Actuaries

Society for Human Resource Management

(Sussex-Warren NJ Chapter)

GAPS (Global Association Pension Services)

WorldatWork

American Management Association

National Federation of Independent Business

Better Business Bureau

|

|

101 Belvidere Avenue

P.O. Box 7

Washington, NJ 07882-0007

908-689-4200

|

|

Terms of Use

The site ("from the HR perspective" hence herein referred to as MFYCO.com) is made available by Michael F. Yates & Company Incorporated. All content, information and software provided on and through 'from the HR perspective' and MFYCO.com ("Content") may be used solely under the following terms and conditions ("Terms of Use".) YOUR USE OF THIS WEBSITE CONSTITUTES YOUR AGREEMENT TO BE BOUND BY THESE TERMS AND CONDITIONS. IF YOU DO NOT AGREE TO THESE TERMS, YOU SHOULD IMMEDIATELY DISCONTINUE YOUR USE OF THIS SITE.

Michael F. Yates & Company, Inc. believes strongly in protecting the privacy of its users. Click here to view our privacy policy.

As always, any statements regarding federal tax law contained herein are not intended or written to be used, and cannot be used, for the purposes of avoiding penalties that may be imposed under federal tax law or to market any entity, investment plan or arrangement.

|

|

|

|

|

|

|