Contributing today for a better tomorrow. | | Relevant news, updates, and resources for your retirement planning! | | Message from the Administrator/CEO | | |

Greetings Esteemed Readers,

In this, our first newsletter of 2026, we take a moment to reflect on the year behind us and the resolve that brought us forward. 2025 had its share of challenges, uncertainty, and loss – including the passing of a colleague, whose memory we honor.

Throughout last year, our ongoing Pension Benefit System update required sustained focus, patience, and perseverance. There were challenging moments, but forward movement continued because of steadfast commitment and unwavering effort. The work accomplished during this update is significant and establishes a critical foundation for the future of GERS.

At the same time, GERS continued to strengthen its physical assets and operational readiness. Plans are underway to enhance the Havensight property, with improvements designed to modernize the space, enhance the overall experience, and reinforce its role as a vital economic and community destination. These efforts reflect a renewed vision for the property and a long-term commitment to stewardship and growth.

In support of safety and operational efficiency, GERS also invested in new security vehicles, reinforcing its commitment to protecting employees, tenants, visitors, and assets. These additions enhance visibility, responsiveness, and preparedness, ensuring that the Havensight Mall remains secure and well supported.

Progress, much like flight, does not begin in the air. It begins on the runway with preparation, discipline, and confidence. Each lesson learned strengthens our footing and builds the lift needed to move forward. We are not starting over. We are advancing with experience, clarity, and purpose.

The course ahead in 2026 is set. Momentum continues to build, and the focus now turns to direction, lift, and sustained forward motion. The work before us is informed by the challenges we have faced and strengthened by the dedication that has brought us to this point.

Thank you to our employees, retirees, active members, and external stakeholders whose commitment and professionalism continue to move GERS forward. I am proud of what has been accomplished and confident in where we are headed.

| | |

On December 12, 2025, Team GERS participated in its annual Staff Development and Employee Recognition. The team participated in team-building activities which strengthened relationships, improved communication, and enhanced collaboration.

This year's theme was “In the Kitchen.” And like every good kitchen that prepares something good, we know our employees are the key ingredients. Working together, they created pepper bottles that will be enjoyed later.

| | St. Croix Agricultural Fair 2026 | | The GERS participated in Agrifest 2026 - Agriculture and Food Fair on St. Croix, February 14-15, 2026. Over 260 active and retired members visited our booth to obtain pre-retirement counseling, review their contribution history, submit requests, and engage in friendly conversations. Members also gained access to their GERS account via Member Self-Service. We were excited to assist members, address inquiries, and foster connections within our community. The event provided a valuable opportunity for members to stay informed and receive personalized support. | | Active members and retirees were also encouraged to scan a QR code to answer a few GERS questions, where winners received unique gifts. Other members and retirees also received trinkets, participation gifts, popcorn and welcoming items to help spread the love of the Valentine’s Day weekend. | | | |

Do you have questions about your membership, service credit, retirement eligibility, online self-service registration, or GERS Educational Webinars? Get in touch with Customer Service today. We are here to serve you.

Call us directly at 340-693-3939 or send an email to customercare@usvigers.com. Kindly allow up to 24 hours for a response to emails sent outside of our regular office hours.

The Customer Service Team provides real-time communication via telephone, email, and in person. Overall, the team's goal is to provide you with accurate, courteous, accessible, and responsive service.

Follow us on social media for the latest updates.

Facebook: https://www.facebook.com/gersvi1959

X (Twitter): https://www.twitter.com/gersvi1959

LinkedIn: www.linkedin.com/in/gersvi1959

YouTube: https://www.youtube.com/@governmentofthevirginislan1118

| |

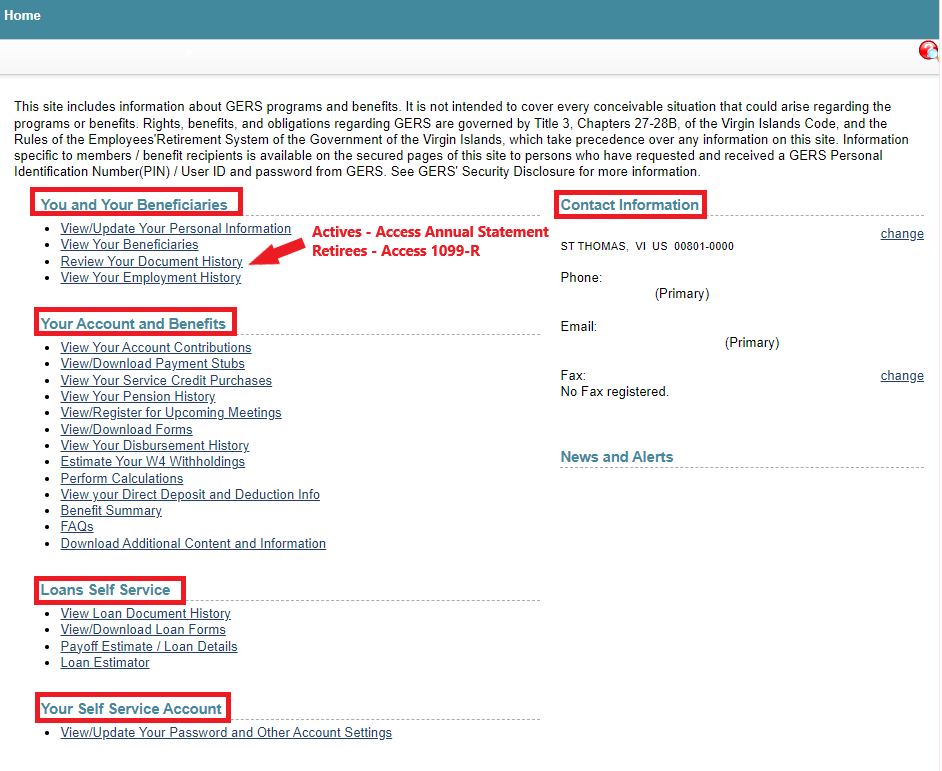

- How much do you have in your retirement account?

- Do you have beneficiaries listed?

- Does GERS have my employment history?

- Where can I locate a copy of my 1099R?

The answer your looking for is Member Self Service.

| |

To sign up, please refer to the following instructions.

Go to www.usvigers.com and click on "Member Self-Service.

| |

Enter your Username and Password and click on Log In

If you do not have a Member Self-Service account, click on Register and be guided by the prompts (enter your Social Security Number, Last Name, Date of Birth, and then click on Validate.)

| If you've forgotten your password, please contact Customer Service by telephone at (340) 693-3939 or via email at customercare@usvigers.com. | |

To update your primary address, phone number(s) and email(s), click on "Change" under "Contact Information".

You can also update your personal information by selecting "View/Update Your Personal Information" under "You and Your Beneficiaries".

| |

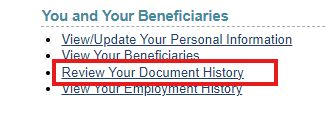

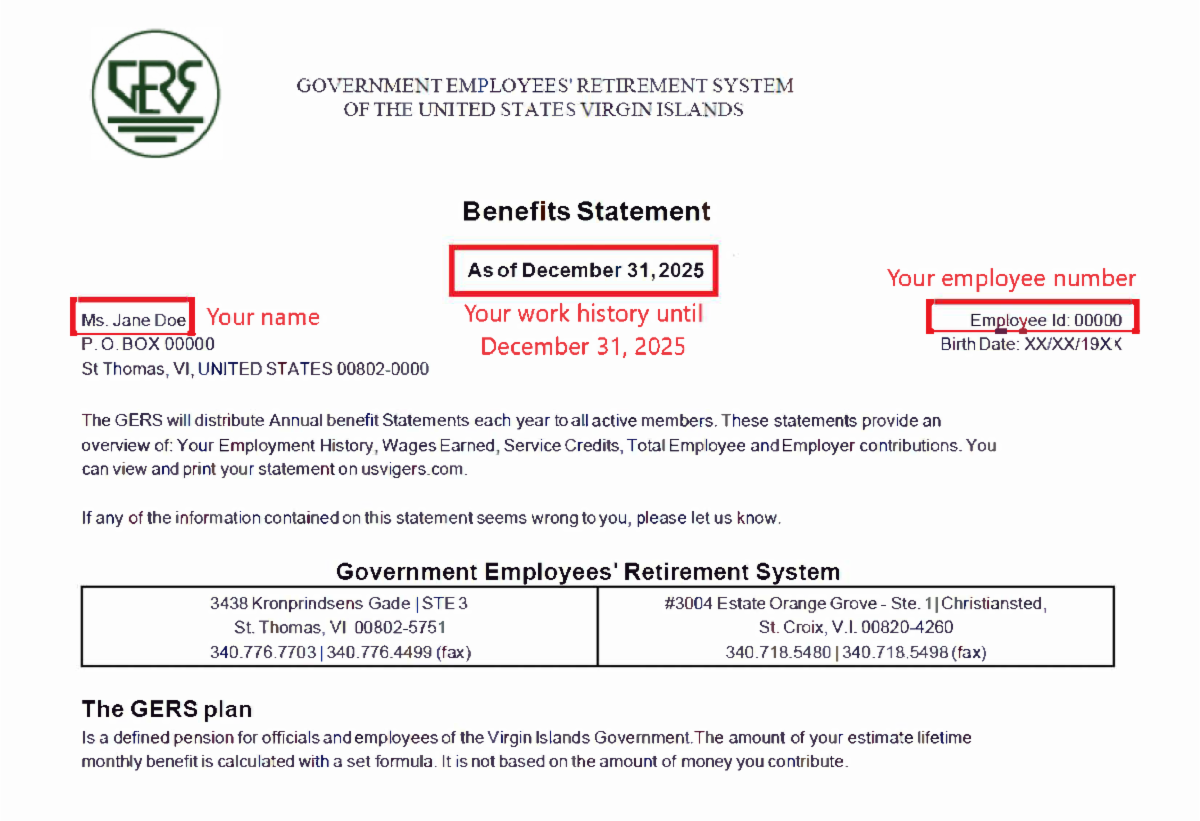

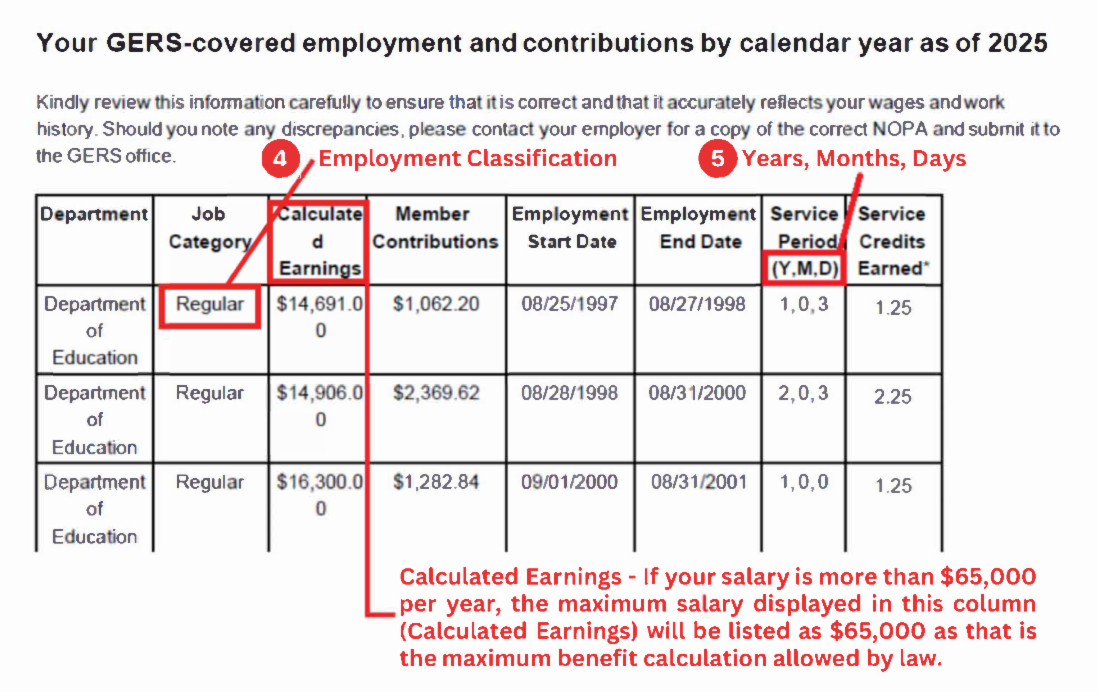

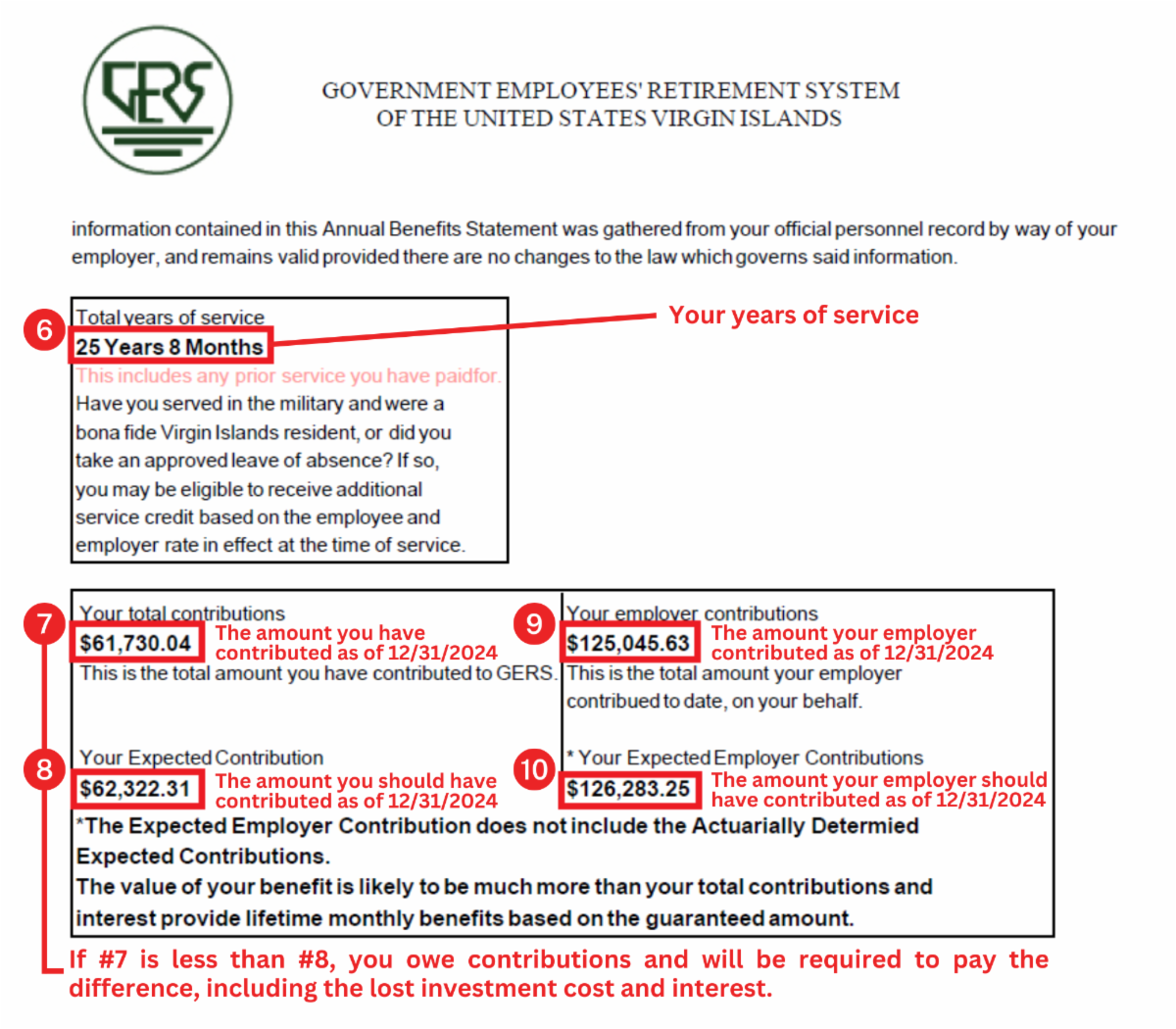

Active members, be on the look out for your annual statement from email V3locity SMTP - v3smtp@usvigers.com. We have begun distributing the Annual Statements by agency.

To ensure you receive your Annual Statement, log into your Member Self-Service and update your email and mailing address.

To access or print your Annual Statement, click on Review Your Document History under You and Your Beneficiaries in Member Self-Service. Please review your Annual Statement and report any inaccuracies to the Customer Service Office.

Remember, your employer's contributions is as of December 31, 2025.

| If you prefer a hard copy of your Annual Statement, from 2026 onward, please send an email to our Customer Service office at customercare@usvigers.com. | | | Final Countdown to Retire Early in 2026 | | |

By Jacob Schroeder

Source: https://www.kiplinger.com/retirement/retire-early-this-year-is-this-the-year-you-take-the-leap

Here's how to retire early in 2026, with a month-to-month checklist of achievable goals.

It’s said that waiting for the right moment is just procrastination in disguise. What if 2026 is the year you finally prepare for early retirement and start living it by December 31?

Retiring before 62, or even by 55, is an exciting but daunting goal, as many traditional benefits aren’t yet available to you. How do you access retirement accounts without penalties? Will you have enough income without Social Security? What’s your plan for health coverage?

Retire early in 2026 (or at least by year's end)

There’s no Goldilocks moment in this story. You have to trust the work you’ve already done — whether it’s saving half your income, living modestly or building multiple streams of income. As self-help author Napoleon Hill put it: “Don’t wait. The time will never be just right.”

If you’re done waiting but aren’t sure what the final steps are, this monthly early retirement checklist is for you. By December 31, 2026, you can ceremoniously update your LinkedIn profile headline to include one very satisfying word: “former.”

January: Review your retirement readiness

| |

Since this year’s resolution is greater than dropping a few pounds, there’s no time to waste. Brett Spencer, CFP® and founder of Impact Financial, advises, “Retirement planning can be overwhelming, especially dealing with the nuances of early retirement. Just like a new year’s workout program, getting started is key.”

Here’s what to tackle first so your goal doesn’t collect dust like an unused gym membership.

Assess your target. How much do you need? The Rule of 25 is a simple formula: Multiply your estimated annual retirement expenses by 25. This provides a target number that could allow you to withdraw 4% annually while preserving your nest egg. For greater accuracy, try our retirement calculator.

Build a budget. Include essentials such as housing and food, as well as fun stuff such as travel. Recognizing many high-income workers in the FIRE (financial independence, retire early) movement, Worth Pointe partner and CFP® John Chapman says, “High earners may not need to budget while working, but in early retirement, it’s a must.”

Get a plan and run projections: A financial adviser can stress-test your plan for worst-case scenarios, ensuring your money outlasts you — not the other way around.

February: Build a health care plan

| | |

Instead of your sweetheart, focus on your own heart this year — literally. Medicare doesn’t kick in until 65, so health care is often a major planning hurdle for early retirees.

Explore options. Look into COBRA, ACA marketplace plans or joining a spouse’s plan. Among these, enrolling in a spouse’s plan often proves most cost-effective, providing a bridge to Medicare eligibility. Chapman notes, “Premiums depend on income, so understanding coverage is critical.” You can also use funds in a health savings account (HSA) when you retire.

Schedule checkups. Knock out physicals, dental visits and specialist appointments while you’ve got coverage.

March: Organize your financial accounts

| |

Madness is for basketball, not your finances. This month, simplify.

Consider consolidating accounts. It might make sense to combine investment and retirement accounts for easier management. Make sure you know which financial and tax documents to keep and how to store them safely.

Pay off high-interest debt. “Eliminating debt, including your mortgage, lowers fixed costs and adds peace of mind,” Chapman says. Try some of our tips for how to pay off credit card debt.

Build cash reserves. Save six to 12 months of expenses in a high-yield savings account or money market account. “Since early retirees may not access retirement accounts without penalties, it’s important to hold at least a year’s worth of expenses in cash reserves,” Chapman adds. “Also, build up significant non-retirement investments to fund spending before tapping into retirement accounts.”

April: Maximize tax opportunities

| |

This is the rare year when tax season brings joy. Spencer says, “Beyond filing, it’s a great time to take advantage of any tax benefits and plan for the year ahead.”

Boost retirement accounts. For instance, you can max out 2025 IRA contributions by April 15, 2026. Spencer also recommends “maximizing 401(k) contributions and considering contributing to an HSA or FSA for additional tax deductions.”

Consider Roth conversions. “Once you retire early, your taxable income may drop significantly,” Chapman says. This creates a great opportunity for Roth conversions — transferring funds from pre-tax ("traditional") IRAs or 401(k)s to Roth IRAs at potentially lower tax rates. He suggests consulting a tax adviser to determine the right amount to convert without triggering unintended tax consequences.

May: Optimize your withdrawal strategy

| | |

You’re not quite done with the IRS. If you’re under 59½, accessing retirement accounts without tax penalties takes strategy. At the same time, you’ll want to ensure your portfolio is balanced and your withdrawals can sustain your lifestyle.

Create a withdrawal strategy. Explore options such as the Rule of 55 or SEPP 72(t) exceptions to tap your accounts penalty-free. Determine which accounts to draw from first (e.g., taxable accounts before IRAs) and at what rate to maintain tax efficiency and sustainability. Create an early retirement withdrawal strategy for the long haul.

Review asset allocation. Spencer emphasizes diversification to reduce downside risk: “Bonds aren’t the only diversifier. Understanding true diversification is critical.”

June: Evaluate housing needs

| | |

Some things might not change: Housing is the biggest expense for retirees, just as it is for workers, according to government data. Where do you see yourself living in retirement?

Assess your situation. Would downsizing or relocating improve your lifestyle and budget? Dreaming of a beachfront bungalow or van life?

There are so many options to consider, all of which will affect your pocketbook. For example, sometimes joining a retirement community when you're younger might save you money down the road if you need assisted living. On the flip side, if you're hearty and adventurous, you might consider retiring abroad.

You'll also need to think through whether you retire in place, buy a new home or rent in retirement. Check out our list of the best places to retire in the U.S. Now’s the time to plan.

July: Make lifestyle preparations

| |

As you set off fireworks to celebrate America’s independence (and maybe annoy your neighbors), reflect on your own financial independence. What will you do? Who do you want to become? Early retirees can experience a loss of identity or purpose, especially when they feel there’s still more to contribute to the world.

Test your budget. Try living on your retirement income for a month and adjust as needed.

Explore interests. Start hobbies or volunteer work now to avoid post-retirement identity crises. Thinking of launching a business? Dip your toes in now.

August: Create or review your estate plan

| |

It’s not just for older folks. If you have assets, you need an estate plan.

Update legal documents. Refresh your will, power of attorney and health care directives. “Some employers offer group legal benefits,” Spencer notes. “Use them to get started on your estate planning or other legal needs before retirement.”

Verify beneficiaries. Double-check the beneficiaries you named on retirement accounts and life insurance policies. Make their lives easier by organizing your estate planning documents for your heirs.

September: Review your progress

| |

Cue Europe’s 1986 hit, “The Final Countdown,” because you’re in the final quarter.

Check your plan: “If you have tax or year-end strategies to implement, now’s the time,” Chapman says. “Logistics for implementing them can take weeks.”

Verify Social Security and pension details: Even if you’re years from filing, ensure that your Social Security records are accurate. Make sure you understand how Social Security might reduce payments starting in about 2033 if Congress doesn't act. If you’re eligible for a pension, ensure that payout options are clear to you.

October: Lock down insurance

| | |

Don’t let spooky surprises catch you off guard.

Confirm health coverage. Open enrollment often occurs in the fall, so now is when to finalize your post-retirement plan.

“Reassess your health coverage needs for the last few months before retirement, too,” Spencer says. “If you want to get money into an HSA before retirement, this may be a good opportunity.”

Review other insurance. Ensure long-term care, life and property policies align with your needs.

November: Notify your employer

| | |

This might be the easiest or hardest step, depending on your relationship with your company and coworkers.

Give your boss notice. Provide at least 60 days’ notice or longer if required. Use this time to wrap up responsibilities and plan your transition.

Use up benefits. Take advantage of any remaining vacation days, wellness funds or other perks. Alternatively, consider getting paid for any unused PTO you might have accrued.

Consider part-time work doing something you love. If the thought of no earned income makes you nervous, now is the time to think about a high-paying side gig or a transition to a part-time or freelance job that interests you.

December: Finalize and celebrate

| | |

You could spend the month debating whether Die Hard is a Christmas movie (it is), but there are better ways to use this time. Now’s the moment to finalize the details so you're ready to pop the champagne by year's end.

Adjust tax withholding. Ensure retirement withdrawals don’t trigger surprise tax bills.

Set up disbursements. Plan your first withdrawals for January.

Celebrate. Whether it’s a trip, a party or simply savoring the satisfaction of achieving your goal, take time to mark this milestone. It can help make the transition smoother.

Even the best plans hit bumps, but with this checklist, you’ll be ready to start 2027 focused on your bucket list instead of your to-do list.

Source: https://www.kiplinger.com/retirement/retire-early-this-year-is-this-the-year-you-take-the-leap

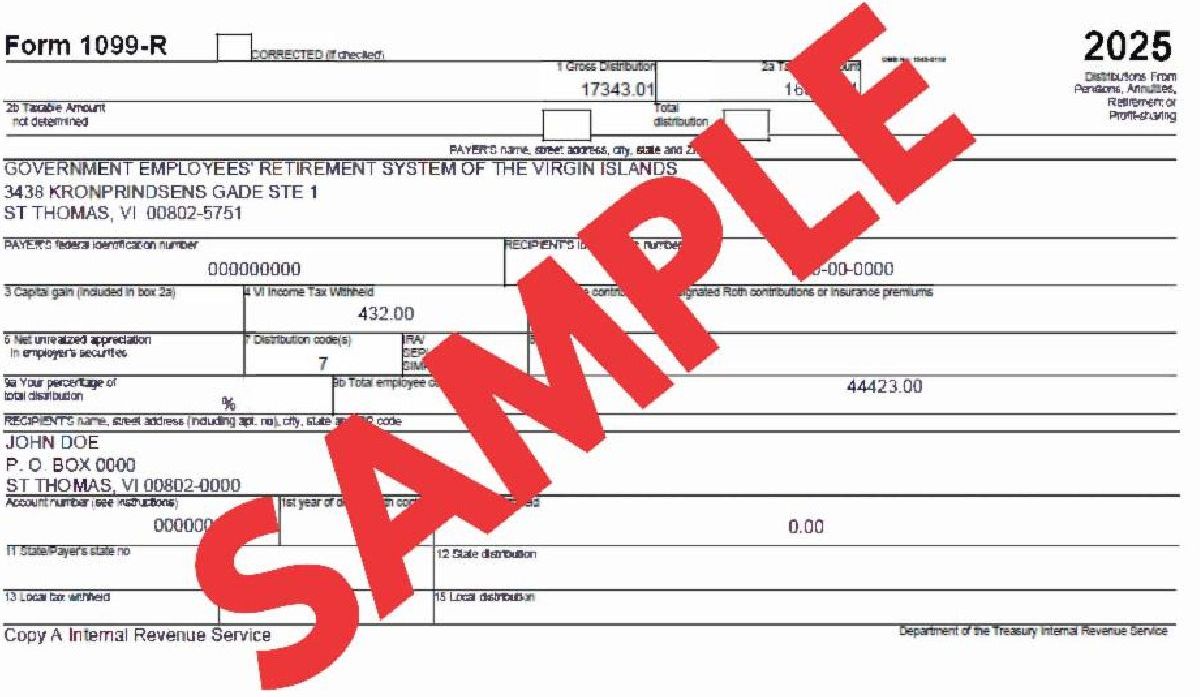

| | Retirees, your 1099-R form has been mailed out to your address on file. Please make sure that your email and/or mailing address on file is correct today. If you do not receive your 1099-R form by March 31, 2026, please call our Customer Service office at (340) 693-3939 or email customercare@usvigers.com. You can also access a copy of your 1099 in Member Self-Service via our website, www.usvigers.com. | | IRS Announces New Tax Rates for 2026 | |

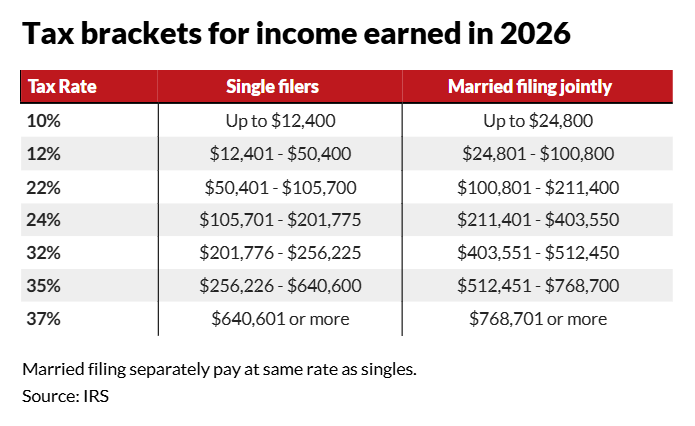

New Tax Rates Announced for 2026

In the U.S. tax system, income tax rates are graduated, so you pay different rates on different amounts of taxable income. There are seven federal income tax rates in all: 10 percent, 12 percent, 22 percent, 24 percent, 32 percent, 35 percent and 37 percent. The more you make, the more you pay.

A tax bracket is a range of income that’s taxed at a specified rate. Importantly, your highest tax bracket doesn’t reflect how much you pay on all of your income. If you’re a single filer in the 22 percent tax bracket for 2026, you won’t pay 22 percent on all your taxable income. You will pay 10 percent on taxable income up to $12,400; 12 percent on the amount between $12,401 and $50,400; and 22 percent above that (up to $105,700).

In addition, the 2026 standard deduction will be $16,100 for single filers and $32,200 for married couples filing jointly, up from $15,750 and $31,500, respectively, for the 2025 tax year. The standard deduction is the fixed amount the IRS allows you to deduct from your annual income if you don’t itemize deductions on your tax return. The lower your taxable income is, the lower your tax bill.

There’s even more good news for older taxpayers. Single filers 65 and older can increase their standard deduction in 2026 by $1,650; individuals who are unmarried and not a surviving spouse can increase their standard deduction by $2,050. In total, a single taxpayer 65 or older can claim a standard deduction of up to $18,150.

Moreover, the One Big Beautiful Bill Act offers a temporary extra deduction of $6,000 for people ages 65 and older with an adjusted gross income of $75,000 or less for single filers and $150,000 or less for married couples filing jointly. The deduction is reduced for higher earners, up to $175,000 for a single filer and $250,000 for a couple. (Above those thresholds, you don’t qualify.) This extra deduction runs through the 2028 tax year.

You can also itemize individual tax deductions such as charitable donations, but they must add up to more than the standard deduction to make itemizing worthwhile.

If you have been hit with a big tax bill in the past, consider consulting a tax adviser about how to reduce your next one. A good first step is to look at how much tax is being withheld from your paycheck. It might be easier to have a little more money withheld from each paycheck than to face a big lump-sum bill at the end of the tax cycle. The IRS has a free withholding estimator that can tell you how much you should have taken out.

See the full tax table document here.

Source: https://www.irs.gov/newsroom/irs-releases-tax-inflation-adjustments-for-tax-year-2026-including-amendments-from-the-one-big-beautiful-bill

| | Table Source: AARP (https://www.aarp.org/money/taxes/income-tax-brackets-2026/) | | St. Croix Retiree Holiday Social | | |

GERS Administrator and Chief Executive Officer, Angel Dawson, led the conga line at the St. Croix retiree social. Staff, retirees, and attendees gathered to dance and join in on the fun, highlighting the importance of togetherness during the holidays and taking a moment to bask in happiness and celebration.

The beauty of the moment was also shared with a wider audience online, gaining 132K views and 293 shares on Facebook proving that the power of Soca, culture, and good vibes will forever be embraced and noticed by Virgin Islanders and nonlocals alike. Click the video below to watch!

| | St. Thomas Retiree Holiday Social & Friday Night @ Havensight - November 28, 2025 | | |

Last year, we tried something a little different. On Black Friday, November 28, 2025, we combined the St. Thomas Retiree Holiday Social with Friday Night @ Havensight, creating a festive evening of celebration, connection, and holiday cheer.

Retirees gathered to celebrate themselves and one another while enjoying delicious holiday treats in a warm and festive atmosphere. The event also coincided with Havensight’s lively Black Friday festivities, where participating stores offered generous discounts.

Those in attendance had the perfect opportunity to get first dibs on their favorite items and kick off their holiday shopping, all while enjoying a memorable evening with fellow retirees and members of the community. Click the video below to enjoy more photos of both events.

| | Regular Meeting of the Board Trustees on February 26, 2026 | | March through June schedule. | | Pre-Retirement Workshops for Actives | | |

Successful retirement planning begins with member education. The GERS is excited to announce the 2026 pre-retirement workshops, which are designed to help you better plan your retirement. Currently, we provide three workshop topics, rotating twice per month.

-

The Transitioning to Retirement Workshop is open to active members who are 6 months to 1 year away from retirement.

-

The Pre-Retirement Workshop is open to active members at any stage in their career.

-

The Countdown to Retirement Workshop is open to active members who are at least 2 years away from retirement.

| | AARP Financial Wellness Workshops | The AARP VI Financial Wellness Series 2026 are virtual financial education classes, presented by AARP Virgin Islands in collaboration with the Government Employees' Retirement System (GERS) of the Virgin Islands, which shares tips on saving and financial planning, managing and protecting your assets, planning for retirement, and estate-planning strategies. The sessions are FREE and open to the public, 18 and older. | | Do you prefer an in-person workshop to learn more about GERS benefits and your retirement options? GERS is excited to collaborate with you. We offer onsite presentations and outreach events to keep your team informed. Contact us today at (340) 693-3939 or email membereducation@usvigers.com to schedule a session! | | |

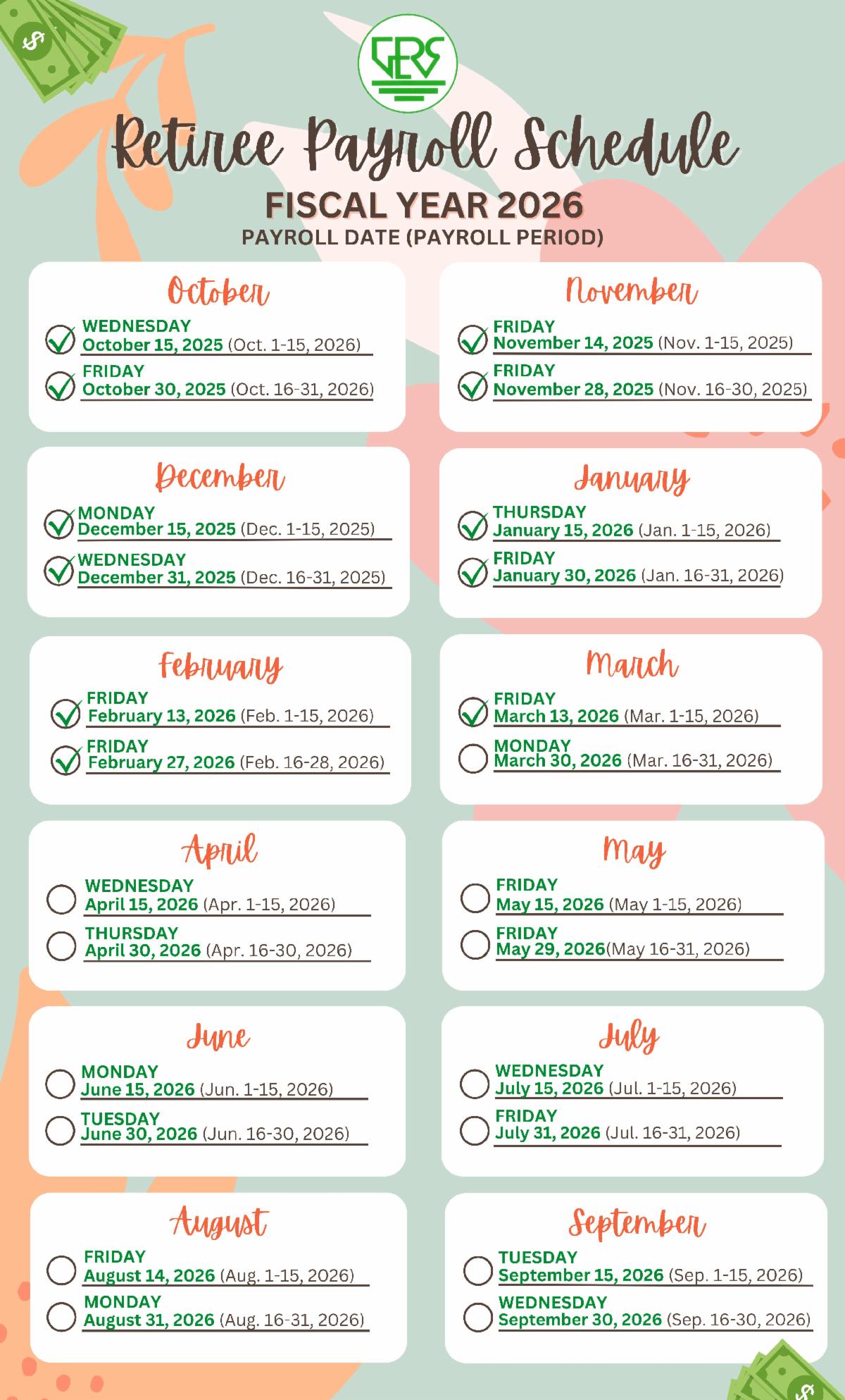

GERS' Bottom Line as of

February 13th Payroll

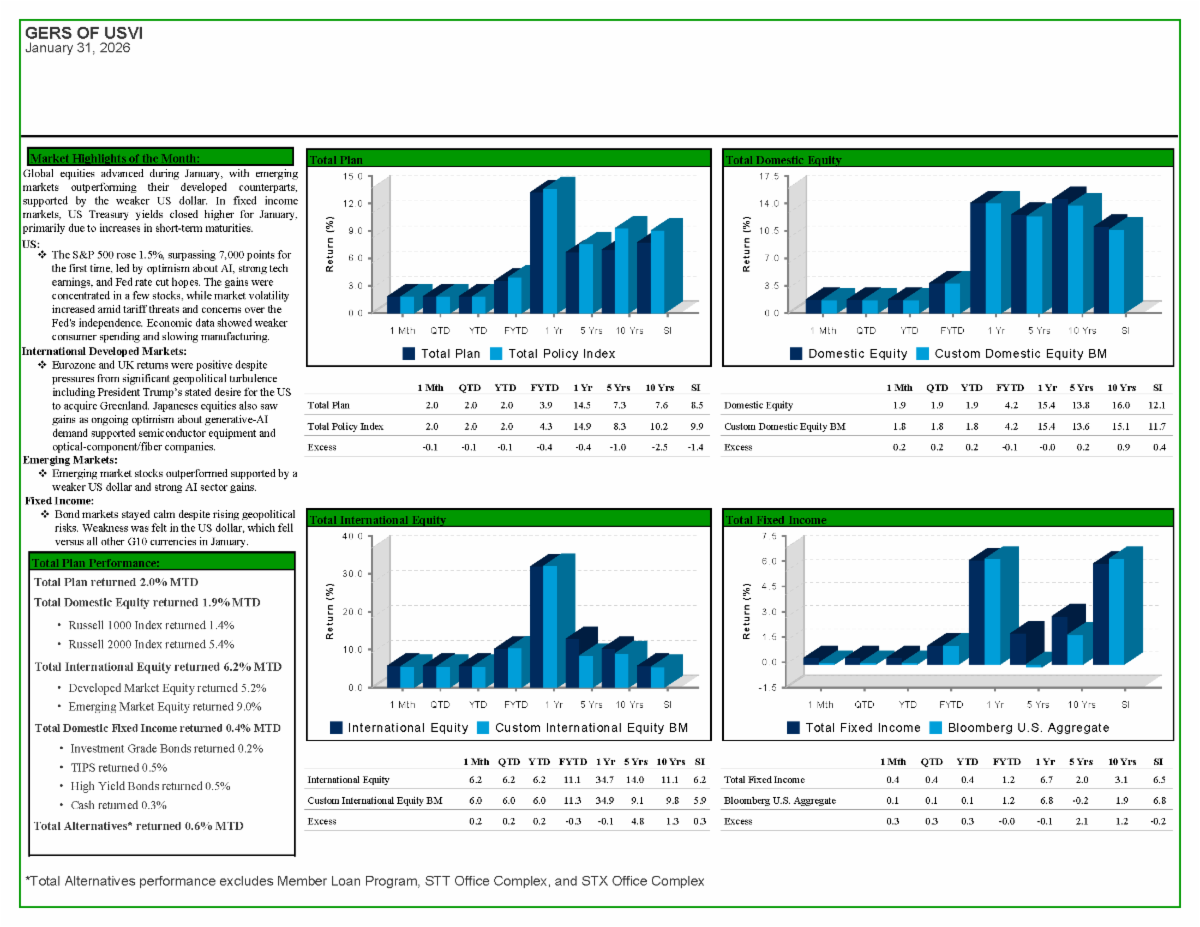

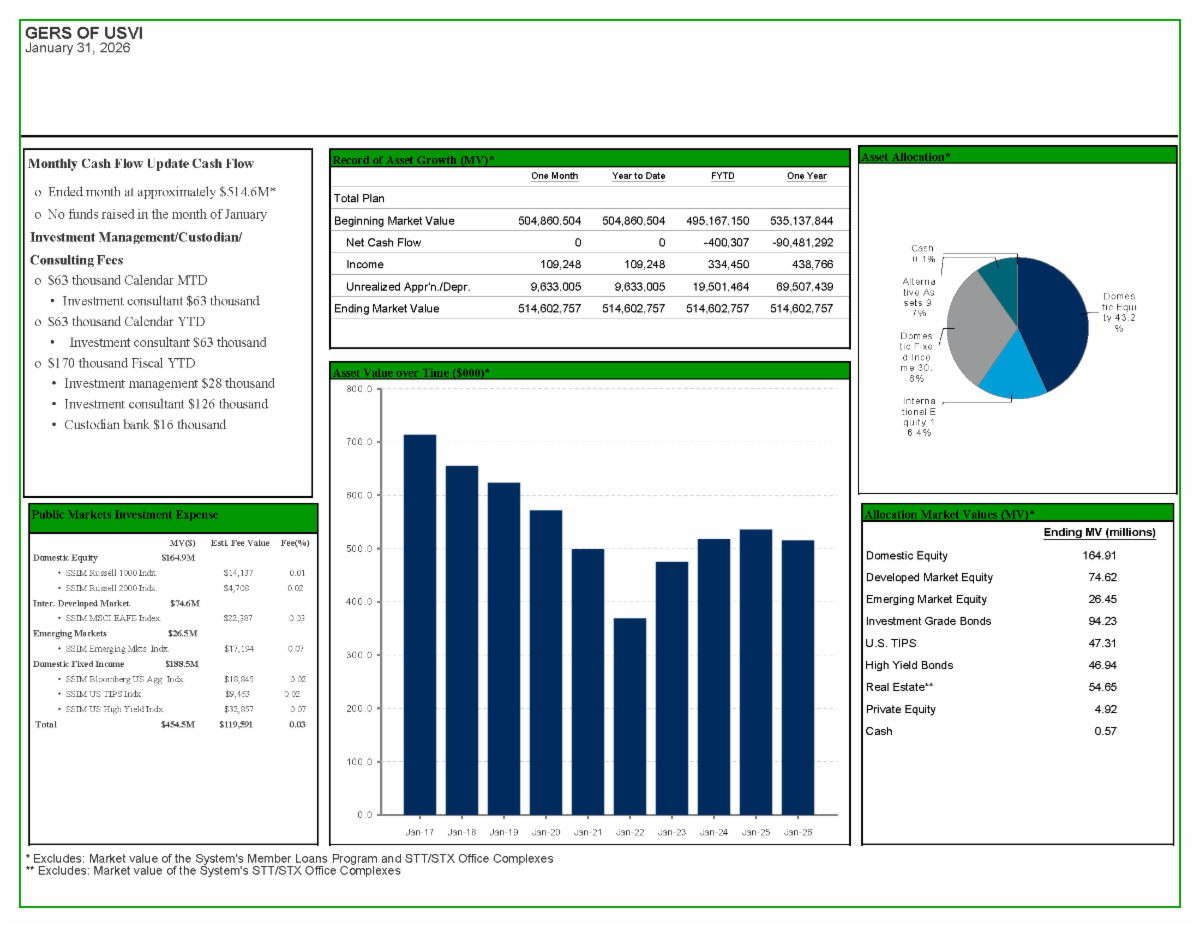

| | | Total Actives | 9,036 | | Total Retirees | 8,763 | | Bimonthly-Retiree Payroll | $11,418,605.84 | | FY Total Number of Refunds | 36 | | Total Refunds Paid | $459,212.34 | | Total Death Benefits | 6 | | Death Benefits Paid | $201,618.05 | | Fiscal Year to Date Total Return Ending | 3.9% as of January 31, 2026 | | | The GERS funded status, is the level of accumulated assets that have been set aside for the payment of retirement benefits to employees. The GERS funded status is at 13.2%. | | |

Portfolio Assets include loans, stocks, bonds, buildings and property, and alternatives investments.

Note: Return numbers exclude the GERS office buildings. They are however included in the total portfolio assets. All figures are estimates.

| | |

Havensight Mall is best known as a vibrant shopping and entertainment destination, offering a blend of local culture, unique shopping experiences, and exciting events. Visitors can explore a variety of stores featuring locally made crafts, jewelry, fashion, and souvenirs. In addition to shopping, Havensight Mall offers convenient amenities, including ample parking, a variety of food options, and scenic views of the harbor. It is a wonderful place for visitors to experience the island’s hospitality while enjoying an afternoon of shopping, dining, and live entertainment.

Havensight Mall also serves as a venue for an innumerable number of events, including the Governor’s Children’s Christmas Party, Deck the Halls. Schoolchildren of all ages attended the event with their families and friends, eagerly waiting in line for a treat from Santa and a warm welcome from Governor Albert Bryan Jr. Gifts were distributed to children ranging from infancy to 12 years old, and families were greeted by local dancers who added to the holiday cheer. See below for quick snapshots of the event.

| | Deck the Halls & Governor's Children Christmas Party - December 9, 2025 | | Havensight Mall: Security Update | | |

We are excited to share an update regarding the GERS security vehicles at Havensight Mall another new addition to the ongoing enhancements at the mall, alongside the highly anticipated hotel development.

The new security vehicles will be operated by the mall’s security staff. Both vehicles display the mall’s new logo, building anticipation for the official name change coming in March. The inspiration behind the logo is to encourage both tourists and locals to confidently seek assistance, with the logo prominently featured around the mall and worn by staff.

These new developments are poised to elevate the guest experience at this prime location for anyone looking to enjoy the mall’s stores, restaurants, and events further contributing to the area’s exciting enhancements.

We are also pleased to report that the highly anticipated hotel development is now 100% complete. This innovative project, funded by Haven Development, progressed remarkably.

| | |

SIGN ME UP!

Or send an email to communications@usvigers.com, including your name in the email.

| |

| Did you enjoy this edition of the GERS Update? | | |

| |

Customer Service

Phone: 340-693-3939

Email: customercare@usvigers.com

St. Thomas

3438 Kronprindsens Gade, Ste. 1

St. Thomas, VI 00802-5750

Phone: (340) 776-7703

Fax: (340) 776-4499

St. Croix

3004 Estate Orange Grove, Ste. 1

Christiansted, St. Croix

VI 00820-4260

Phone: (340) 718-5480

Fax: (340) 718-5498

| | | | |