Contributing today for a better tomorrow. | | Relevant news, updates, and resources for your retirement planning! | | Message from the Administrator/CEO | | |

Dear Esteemed Readers:

I presented our Annual Overview of Operations to the Virgin Islands Legislature on August 13, 2025. This presentation characterized the Government Employees’ Retirement System of the Virgin Islands as being a “65-year-old patient that has faced life-threatening conditions over the years”. Following a lengthy technical analysis, I characterized the GERS’ condition as having improved from “Critical” to “Serious”.

The Virgin Islands Government’s pledge of $3.8 Billion Funding Note over 30 years was cited as being the most important reason that the GERS’ health improved from “critical” condition. However, it remains in “serious” condition for two primary reasons:

- By design, annual payments from the Funding Note are unevenly distributed, with most of it only to be received by GERS in the last fifteen years.

- Although the rum cover-over rate that supports the $3.8 Billion Funding Note was permanently increased by the United States Congress in July, the amount of Virgin Islands produced rum being exported to the U.S. mainland has been decreasing.

Recently, I announced that I received formal correspondence from the Virgin Islands Public Finance Authority indicating that the October 1, 2025, Funding Note payment was underfunded by almost $22 Million. When added to the combined shortfalls of approximately $90 million for 2023 and 2024, the System is now $112 million behind in revenues pledged from the Funding Note.

The implications of these gaps are far-reaching. Reduced inflows mean fewer dollars available for investment, and the loss of compounding returns diminishes the System’s ability to meet long-term benefit obligations. Over time, these pressures strain reserves and widen the gap between contributions received and benefits paid out.

This fiscal reality is reflected in the System’s most recent actuarial forecast, which projects a potential insolvency window between 2033 and 2039, absent meaningful corrective action. Although the Board of Trustees acted in its fiduciary capacity to increase the employer contribution rate from 23.5 percent to 26.5 percent, the passage of Bill No. 36-0174 removed that authority and permanently set the rate at 23.5 percent by statute. With limited resources available to stabilize revenues, reversing the System’s financial trajectory becomes increasingly difficult.

Despite these challenges, GERS continues to press forward with initiatives that strengthen the System’s long-term position and support the broader community. Among the positive developments is the planned enhancement of the Havensight Mall property. The project will enhance the property, elevate the visitor experience, and reinforce Havensight’s long-standing presence in the community. A new name for the property is also expected to be unveiled next year, signaling a refreshed identity, a renewed direction for this iconic destination, and an overall HAPPY experience.

During a recent St. Thomas/St. John Chamber of Commerce Business After-Hours on October 23, 2025, attendees were given an exclusive preview of Havensight’s transformation, from the upcoming aesthetics to operational improvements, all designed to reinvigorate the property and contribute to sustained economic growth.

As the year 2025 draws to a close, GERS remains steadfast in its commitment to excellence, responsible stewardship, and the well-being of our members. We extend our warmest wishes to all employees, retirees, and stakeholders during this holiday season. May your Thanksgiving be filled with gratitude, your Christmas with light and joy, and your New Year with prosperity and renewed hope. Together, we will continue working toward a strong and secure future for both the Government Employees’ Retirement System and the Virgin Islands community.

Best Regards,

| | |

Do you have questions about your membership, service credit, retirement eligibility, online self-service registration, or GERS' Educational Webinars? Get in touch with Customer Service today. We are here to serve you.

Call us directly at 340-693-3939 or send an email to customercare@usvigers.com. Allow up to 24 hours for a response to emails sent outside of regular office hours.

The Customer Service Team provides real-time communication via telephone, email, and in person. Overall, the team's goal is to provide you with accurate, courteous, accessible, and responsive service.

Follow us on social media for the latest updates.

Facebook: https://www.facebook.com/gersvi1959

X (Twitter): https://www.twitter.com/gersvi1959

LinkedIn: www.linkedin.com/in/gersvi1959

YouTube: https://www.youtube.com/@governmentofthevirginislan1118

| | |

IMPORTANT: With the upcoming V3locity upgrade, active members and retirees are encouraged to be on the look out for the next steps in setting up their new Member Self-Service experience. Please monitor your email and our social media channels for updates. We encourage you to remain informed for a smooth transition.

Also, remember to update your beneficiaries on file.

Are you an active member or retiree of the GERS without a Member Self-Service (MSS) Account? What are you waiting for? MSS was created just for you!

| | |

If you've forgotten your password, please contact Customer Service by telephone at (340) 693-3939 or via email at customercare@usvigers.com.

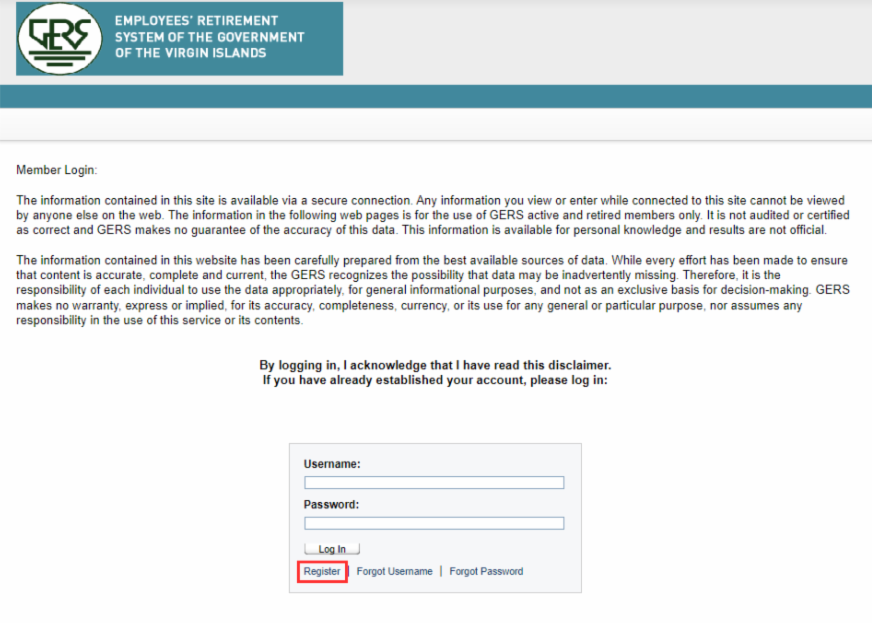

To sign up, please refer to the following instructions.

| Go to www.usvigers.com and click on "Member Self-Service" | |

Enter your Username and Password and click on Log In

If you do not have a Member Self-Service account, click on Register and be guided by the prompts (enter your Social Security Number, Last Name, Date of Birth, and then click on Validate.)

| |

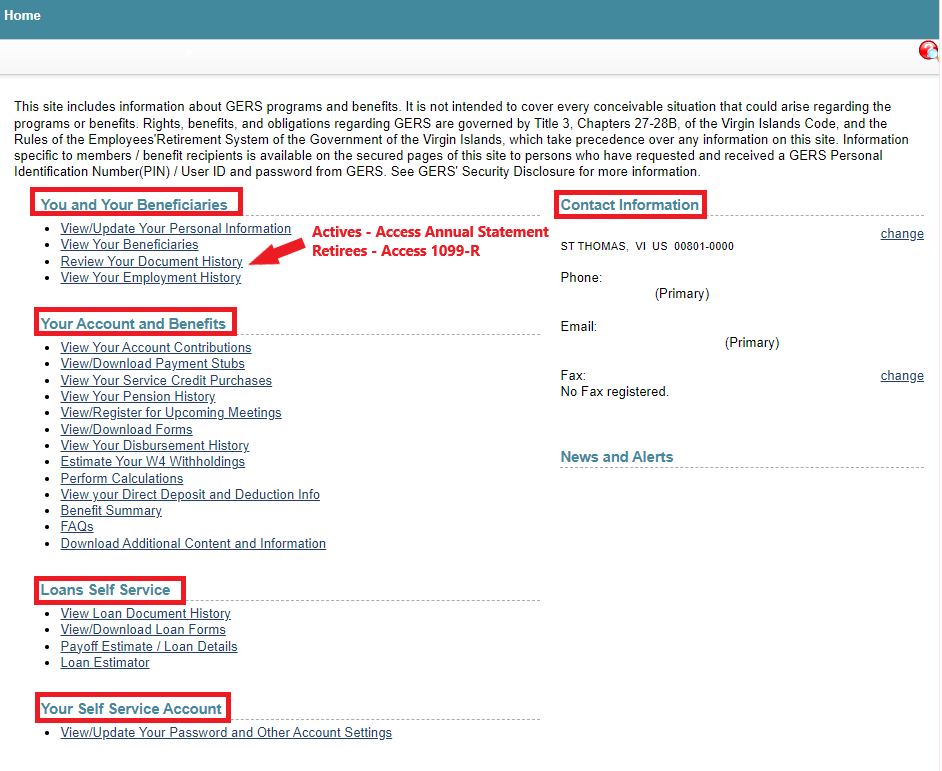

To update your primary address, phone number(s) and email(s), click on "Change" under "Contact Information".

You can also update your personal information by selecting "View/Update Your Personal Information" under "You and Your Beneficiaries".

| | | |

Understanding how transferring service credits from one classification to another may affect your retirement, it is crucial to protect your future benefits. After completing 10 consecutive years of either regular or hazardous/safety employment without a break in service (not even one day), you may transfer credits between these two categories.

For example, if you are working in a regular classification job and are transitioning to a safety/hazardous classification job, you can transfer your service credits from regular to safety/hazardous, provided you have worked in the regular classification for at least 10 years and have no break in service.

If your end date in the regular classification job is on a Friday, the start date of your safety/hazardous job must be the following Monday. If there is a gap of more than one day (excluding weekends and holidays), you will not be able to transfer your service credits between regular and safety/hazardous classifications. Additional costs may apply.

| | It’s just as important to keep your beneficiary information up to date as life events occur such as marriage, birth, divorce, or death. For more details and additional resources, please visit our website at www.usvigers.com. | | Retirement Planning by the Decade: A Savings Guide | |

An article by Charles Schwab

https://www.schwab.com/learn/story/retirement-planning-by-decade-savings-guide

People of all ages should keep an eye on their retirement, but the lens through which you view it depends on your stage of life. Laying a proper foundation in your 20s, for example, is vastly different from balancing competing financial priorities in your 30s and 40s, to say nothing of creating a sustainable income stream in your 60s and beyond.

"Retirement planning isn't a single decision but rather a series of choices each dependent on where you are in your working life, and each requiring its own unique approach," says Michelle Raczek, CFP®, CWS®, a Schwab senior financial consultant based in San Francisco.

Whether you (or a loved one) are just starting out or you're navigating your golden years, here's a multigenerational guide to retirement.

Your 20s: The Time is On Your Side Decade

Retirement is far away, but you'll never be more powerful from a savings perspective.

| |

Retirement may seem impossibly far away when you're just entering the workforce, but that's when many are at their most powerful from a savings perspective. "The younger you are, the more time your money has to potentially benefit from compound growth," says Chris Kawashima, CFP®, director of financial planning at the Schwab Center for Financial Research. "So, saving even small amounts now can pay off big down the line."

Here's how to start:

Put savings on autopilot

Your company-sponsored retirement plan, such as a 401(k), may be your most powerful savings tool. "Many employers automatically enroll new employees in their retirement plans but you still need to make sure you're contributing enough to reach your goals," Chris says. "Ideally, you would aim to save 10% to 15% of your pretax income at this age, but if your income can't stretch that far, at least try to save enough to get the full matching contribution from your employer, if offered."

And don't forget: As your income grows, you can more readily increase your contributions up to $23,500 in 2025 for 401(k) and similar retirement plans.

Keep high-interest, revolving debt at bay

The more of your credit card balance you carry over from month to month, the more of your income goes toward interest payments—and the less is left over for savings.

"While compound interest is a good thing when it comes to your savings, it's a terrible thing when it comes to revolving credit lines," Chris says. "Debt control is essential for building long-term wealth."

Maintain an emergency fund

Likewise, having a pot of money for emergencies like car repairs or an unexpected medical bill means you'll be less likely to reduce or pause your retirement savings to help cover the cost.

Establish a health savings account (HSA)

If your employer offers an eligible high-deductible health plan, you typically can set up an HSA, which offers three distinct tax advantages; Generally, contributions are tax deductible, assets can potentially grow tax-free, and withdrawals are tax-free for qualified medical expenses.

"A young, healthy saver is unlikely to use all the money in their HSA each year, so the remainder can stay invested until they really need it," Chris says. "Of course, investing involves risk, but it can be a great way to save for health care in retirement."

(For 2025, annual contribution limits are $4,300 per individual and $8,550 for families.)

Your 30s and 40s: The spread-a-little-thin decades

Juggling competing goals shouldn't distract you from your future self.

| |

Welcome to the years of competing goals including kids, aging parents, a home, and perhaps even your own business. "It can feel like a lot to juggle but try not to lose sight of your future self," Chris says. "Time is still very much on your side at this stage, so it's important to maintain that momentum." To keep retirement at the forefront of your planning, try to:

Cut back where you can

"Your everyday expenses tend to increase during these years think childcare, a bigger house, a second car," Chris says. "Now more than ever, it's important to be really honest with yourself about what's a need-to-have and what's a nice-to-have."

For example, a hypothetical saver who freed up just $100 a month to invest could potentially have an additional $50,000 saved after 20 years, assuming a 7% annual return.

Avoid lifestyle creep

"As your income grows, avoid the temptation to up the ante on your financial commitments," Chris says. "Think about how much further along you could get by only modestly increasing your expenses and investing the extra money instead."

One of the best ways around this trap is to "pay yourself first" and fund your savings before paying for anything else. If you're already maxing out your 401(k) and can save even more, consider contributing to a tax-advantaged IRA up to $7,000 in 2025 or a taxable brokerage account.

Put yourself first

As parents, we want to do everything we can to support our kids but when it comes to saving for retirement and college, it's important to prioritize your own future.

"That's not to say you shouldn't help fund your kids' education, but you shouldn't do it at the expense of your retirement," Chris says. "After all, you can't borrow for retirement the way you can for college."

What's more, you generally don't need to save 100% of the cost of college. "We like the rule of thirds pay a third with savings, a third with current income, and a third with loans," Chris says.

Don't dip into savings to fund big purchases

Now's also the time when many savers are struggling to cobble together a down payment on a first home or a larger one to accommodate a growing family.

"While it's tempting to tap your retirement savings for a loan, that really should be a last resort," Chris notes. "Taking a big chunk of money out of your 401(k), even if you pay it back with interest, often means missing out on years of potential growth."

Your 50s: The double-down decade

An empty nest often can free up funds for retirement.

| |

This is often when you're at your earnings peak, so you may have extra discretionary income to put toward your retirement savings which ideally should be somewhere between eight and 12 times your salary by the time you reach 60 (see "Progress check").

Now's the time to:

Consider catch-up contributions

In 2025, savers ages 50 and older can contribute an extra $7,500 to a 401(k) plan, for a total of $31,000 and an additional $1,000 to an IRA, for a total of $8,000.

Note, however, that starting in 2026, catch-up contributions must go into a Roth 401(k) account using after-tax dollars if you make more than $145,000 a year.

Plan for taxes

"Most retirees hold the majority of their savings in a traditional 401(k), so any withdrawals in retirement will be taxed as ordinary income," Michelle says. "There's no way of knowing what future tax rates will be, but building in some tax diversity can give you more control over your tax exposure down the road."

To do so, you could:

- Max out your HSA. "Given the rising costs of health care in retirement, building up tax-free savings for such expenses can help keep your taxable income low," Chris says. Plus, once you reach age 65, you can make withdrawals for nonmedical purposes, which will be taxed only at your ordinary tax rate similar to an IRA. In addition to the annual limits, you are eligible for an extra $1,000 catch-up contribution if you're 55 or older.

-

Contribute or convert some funds to a Roth IRA. If you have substantial savings in a tax-deferred 401(k) or IRA, required minimum distributions (RMDs) at age 73 (or 75 if born in 1960 or later) could trigger a large tax bill. To mitigate this, you could start contributing after-tax dollars to a Roth IRA which has no RMDs and whose withdrawals are generally tax-free, so long as you're 59½ or older and it's been at least five years since your first contribution. If you exceed contribution income limits, you could instead convert a portion of your traditional IRA to a Roth IRA. You'll pay income taxes on the converted amounts, but a Roth conversion will reduce the tax-deferred balance subject to RMDs.

- Save more in a taxable brokerage account. While realized gains in such accounts are subject to taxation, the principal is not.

Estimate retirement spending

"Many people count on spending significantly less in retirement but that may not be the case for you," Michelle says. "Work on a realistic spending plan which means not just subtracting expenses you no longer expect, like college tuition and possibly your mortgage, but also adding in those associated with the kind of retirement you're envisioning, like travel, health care, and annual gifts to children or grandchildren."

Consider long-term care insurance

Nearly 70% of those over age 65 will require some type of long-term care often at considerable expense.

"Long-term care insurance can help protect you from having to sell assets to pay for your care," Chris says. "The most cost-effective time to buy is between ages 55 and 65, but—cost aside—you need to be healthy enough to qualify for it, so buying earlier may make sense if you want to insure against long-term care needs."

Progress check

To maintain your current lifestyle in retirement, here's how much you should have in savings at various points along the way.

High earners and those planning to splurge in retirement should consider using the higher end of the multiplier ranges. If you're in between ages, you can use either the multiplier closer to your age or average the multiplier ranges of the ages you fall between to estimate your savings goal.

For example, if your current age is 50 and your current income is $200,000, you should have between $1 million and $1.4 million saved by now.

Your 60s: The homestretch decade

60s & 70s: Smart strategies can help secure a comfortable future.

| |

Even if you're still working, it's time to set the table for retirement—especially since 58% of retirees leave the workforce sooner than planned. Toward that end, you could:

Take advantage of catch-up contributions

Starting in 2025, workers ages 60 to 63 can contribute an additional amount over the regular catch-up contribution amount to their 401(k) or similar plan. This year, that means $11,250, for a total contribution limit of $34,750.

Build up your cushion

In retirement, you want to avoid having to sell assets in a down market to fund your expenses especially early on, which would undercut your remaining years of growth potential.

"Having two to four years' worth of expenses in conservative investments, such as CDs or short-term bond funds, is usually sufficient to ride out a typical bear market," Michelle says.

Plan your retirement paycheck

Now's the time to start figuring out your cash flow from tax-advantaged accounts, taxable accounts, pensions, Social Security, and other sources. The mix may look different early in retirement—before, say, Social Security kicks in (see "Strategize for Social Security")—but a financial professional can help you create a tax-smart cash flow plan.

Strategize for Social Security

You can start taking reduced benefits at 62, but you significantly increase your lifetime benefit by waiting until full retirement age (66 or 67, depending on your birth year). If you can afford to wait even longer, each year you delay past your full retirement age will get you an extra 8% in benefits, up to age 70 after which point there is no incremental benefit.

Apply for Medicare

When you become eligible for Medicare, you must apply during your enrollment window typically the seven-month period starting three months before you turn 65 and ending three months after your birthday or face penalties. However, you may be able to delay Medicare enrollment if you have health insurance through your or your spouse's employer.

Your 70s and beyond: The you-made-it! decades

By now, many people have adjusted to retired life but that doesn't mean your circumstances won't continue to shift.

Here's what to keep on your radar:

Consider your new charitable giving option

At age 70½, you're eligible to make up to $108,000 in qualified charitable distributions (QCDs) from any tax-deferred IRA account in 2025. That can satisfy all or part of your RMDs, and you can exclude your distributions—up to the limit—from your federal taxable income. State taxes may differ.

Start taking RMDs

If you have tax-deferred savings, you must start taking RMDs once you turn 73 or face a penalty of up to 25% on the amount you failed to withdraw. You can delay your first RMD until April 1 of the year after your 73rd birthday, but you still must take your second RMD by December 31—which could trigger an especially large tax bill that year.

Keep an eye on your plan

An annual check-in with a financial planner can help ensure your retirement paycheck is sufficient and sustainable. "If you're a healthy person of means, you should expect to live into your 90s so make sure your plan is designed to go the distance," Chris says.

| | |

The Government Employees' Retiree System invites you to celebrate at our Annual Retiree Holiday Social! Join us for two unforgettable evenings filled with festive cheer, delicious treats, and vibrant local music.

November 28th at Havensight, Enjoy flavorful delicacies, gifts for retirees while supplies last, and live calypso by Top Notch Band. Then the party continues with Obsession Band and Sun De Aqui at Friday Night @ Havensight! Plus, enjoy a special Hampton by Hilton Black Friday offer for just $199 to stay the night.

| | |

December 6th at Time Square, Christiansted, Indulge in Crucian treats, groove to Hartatak Band, DJ Shakey, and marvel at the glowing lantern parade under the Caribbean sky.

Both events start at 4:30 PM and wrap up at 6:30 PM. Let’s embrace the joy of togetherness this season!

Come for the social. Stay for the holiday kickoff fun!

| | Business After Hours: GERS & Havensight Edition | |

An evening dedicated to celebrating our collaboration with the St. Thomas–St. John Chamber of Commerce and unveiling the Havensight Mall rebrand.

Mr. Angel Dawson, GERS Administrator and CEO, shared exciting news about upcoming improvements to Havensight Mall aimed at enhancing the experience for both residents and visitors.

| Mr. Jahmed Mills, Director of Retail, Dining and Entertainment and Property Manager, along with Mr. Moorehead, Chief Security Officer and Assistant Property Manager, joined Mr. Dawson in expressing their enthusiasm for the mall’s new collaboration with its design partner, IDEAS. | The event welcomed business owners, retirees, community members, and mall tenants for an evening of networking, and connection. | Guests enjoyed a cash bar courtesy of the Chamber of Commerce. | The crowd savored an assortment of exquisite dishes prepared by Nibbs Catering, making the event truly memorable. | |

Guests left buzzing with curiosity about the future of Havensight Mall, and a few lucky attendees walked away with door prizes, generously provided by Gourmet Gallery.

The evening wrapped up with a sense of excitement and anticipation for what’s ahead.

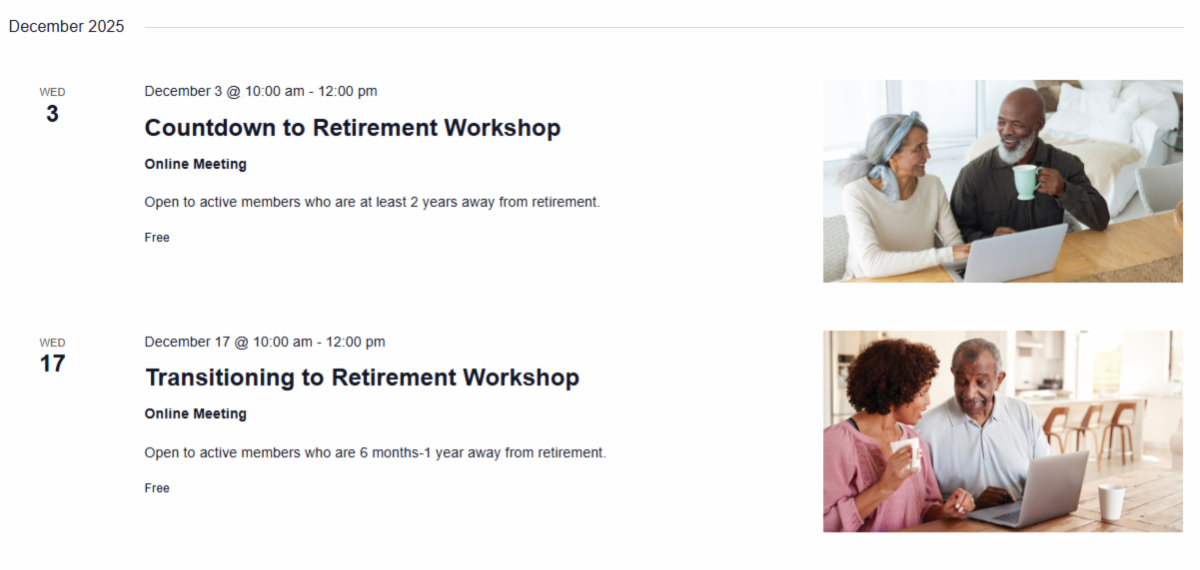

| Pre-Retirement Workshops for Actives | |

Successful retirement planning begins with member education. Our pre-retirement workshops are designed to help you better plan your retirement. Currently, we provide three workshop topics, rotating twice per month.

-

The Pre-Retirement Workshop is open to active members at any stage in their career.

-

The Countdown to Retirement Workshop is open to active members who are at least 2 years away from retirement.

-

The Transitioning to Retirement Workshop is open to active members who are 6 months to 1 year away from retirement.

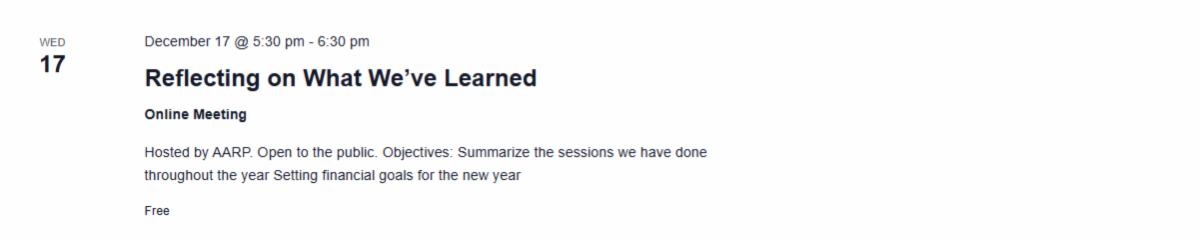

| GERS Partnership with AARP VI | GERS has teamed up with AARP Virgin Islands to offer online workshops for retirees and the general public. Topics include Developing Good Credit Habits, Tax Planning, Financial Planning, and much more. The workshops are held from 5:30 p.m. to 6:30 p.m. AST, and everyone is welcome to participate. The next workshop is scheduled for December 17th - don't miss out! | Bringing our Workshop Directly to You | Do you prefer an in-person workshop to learn more about GERS benefits, including your retirement options? GERS is excited to collaborate with you. We offer onsite presentations and outreach events to keep your team informed. Contact us today at (340) 693-3939 or email membereducation@usvigers.com to schedule your session! |

GERS Bottom Line as of

November 15th Payroll

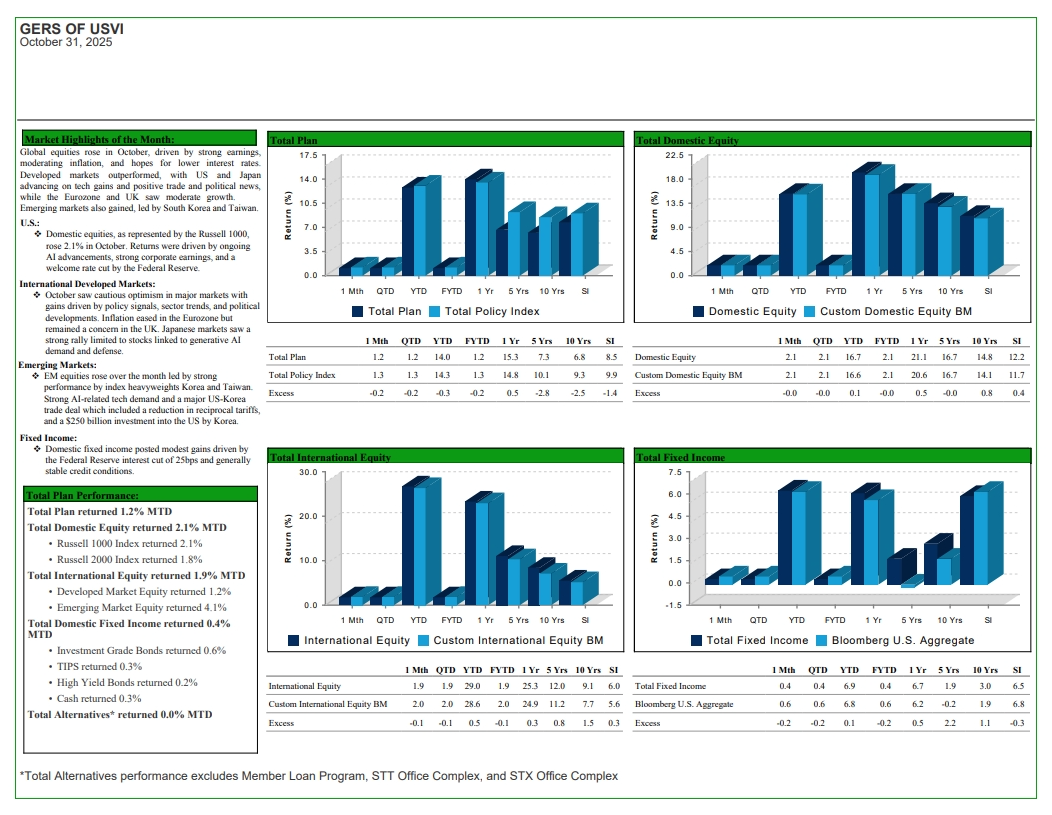

| | The GERS funded status is the level of accumulated assets that have been set aside for the payment of retirement benefits to employees. The GERS funded status is at 10.11%. | | | Total Actives | 9,044 | | Total Retirees | 8,777 | | Retiree Payroll | $11,386,930.67 | | FY Total Number of Refunds | 52 | | Total Amount of Refunds Paid | $684,221.35 | | Death Benefits | 2 | | Total Amount of Death Benefits Paid | $142,096.27 | | Fiscal Year to Date Total Return Ending | 14% | | | |

Portfolio Assets include loans, stocks, bonds, buildings, and property, and alternative investments.

Note: Return numbers exclude the GERS office buildings. They are, however, included in the total portfolio assets. All figures are estimates.

| | Division of Personnel Updates | |

Important Health Insurance Updates

Please be advised that health insurance premiums for active employees and retirees increased effective October 1, 2025. Kindly review the updated rates below and check your pay stub to ensure the correct deductions are being applied.

Premium Changes

Active Employees Rates

- Single Coverage: Increased from $131.83 → $160.44

- Family Coverage: Increased from $232.18 → $283.73

Retirees (UNDER 65)

- Single Coverage: Increased from $176.57 → $206.99

- Family Coverage: Increased from $318.14 →$372.57

- Retiree under age 65, Family over age 65: Increase from $247.27 →$ 289.31

Retirees (OVER 65)

- Single Coverage: Increase from $47.88 →$ 47.98

- Family Coverage: Increase from $97.58 →$ 97.85

- Retiree over age 65, Family under age 65: Increase from $226.28 →$ 256.86

Supplemental Life Insurance

Please note that there are changes to supplemental life insurance deductions. Your payroll deduction should now reflect the premium associated with the current life insurance amount you elected.

Important Reminders for Retirees Approaching Age 65

Medicare Enrollment is required before the 65th birthday. When you turn 65, please submit your Medicare Part A & B card to the Group Health Insurance Unit so that you can be transitioned into UnitedHealthcare (UHC) prior to your 65th birthday. Failure to do so results in termination of your health insurance coverage.

Current UnitedHealthcare Members

The current U-Card will be discontinued at the end of December 2025.

Please use any remaining balance from your U-Card before December 31st.

From December 2025 to January 2026, retirees will start to receive their new UHC cards. New cards received can only be used starting January 2026. For all questions and inquiries related to card and usage, please contact the UHC Representatives on St. Thomas, Ms. Kendra Bernard (340) 693-9907 or Ms. Sarauw (340) 718-9905, or call the customer service line at 866-827-9022.

Additional Benefits

United Health Care offers a FREE gym Membership Program (RENEW) that is available for members enrolled with UHC. If you are not currently enrolled and would like to find out how, please contact the UHC Representatives on St. Thomas, Ms. Kendra Bernard (340) 693-9907 or Ms. Sarauw (340) 718-9905, or call the customer service line at 866-827-9022.

UHC-Free produce distribution coming soon in 2026- Stay alert!

| GVI Wellness Program Updates | |

The GVI Wellness Program is committed to bringing new, exciting, and engaging wellness activities throughout 2025–2026. We encourage all active employees and retirees under 65 to visit the GVI Wellness Website regularly to stay updated and involved. There you will find upcoming activities, events, and wellness initiatives such as, MyBioFix, and the FitForce Program that offers free gym access for employees and retirees under 65. Many participants have already taken advantage of this opportunity! Stay Engaged, Stay Healthy by visiting: www.gviwellness.org.

Important Reminders

Please ensure the following are current in our system:

• Beneficiary information

• Contact information

• Medicare documentation (if applicable)

If you have any questions or need further assistance, please contact the Group Health Insurance Office at: St. Thomas/St. John: (340) 774-8588 or St. Croix: (340) 718-8588

The team is available to support you and ensure you have the information needed to maintain your coverage and benefits.

Thank you for your continued cooperation. Stay active, stay informed, and stay well.

| | |

Friday Night @ Havensight

The first Friday Night at Havensight of the year launched on October 24, 2025, with music, food, and fellowship. The evening opened with the uplifting sounds of Pan in Motion, whose steel pan rhythms created an inviting island ambiance that welcomed guests as they arrived.

| | Local vendors filled the streets with dishes and refreshing beverages, giving attendees a delicious taste of Virgin Islands cuisine. Families, retirees, visitors, and community members strolled through the event, to chat, laugh, shop, and soak in the festive energy. | | Adding to the warmth of the evening, Mr. Angel Dawson, GERS Administrator and CEO, spent time greeting guests personally, sharing laughter and conversation as he joined in the celebration. | | Entertainment began with a captivating performance by Lourdes and the Switch, whose smooth harmonies and original songs had guests dancing, recording videos, and singing along. Everyone in attendance enjoyed the moment. | | |

The excitement grew as When Band took the stage, delivering energetic calypso rhythms that echoed throughout the night. The lead singer engaged the audience by stepping into the crowd, encouraging everyone to dance together, hips swaying in unison to the beat.

The atmosphere was filled with joy, movement, and the unshakable spirit of the Virgin Islands.

| | The technical team ensured that every microphone, speaker, and instrument sounded crisp and clear. | | Thanks to their professionalism and attention to detail, the night unfolded without a single technical glitch allowing the performances and crowd energy to shine uninterrupted. | Many, continued to take to the open spaces to dance, sway, and move to the rhythm proving once again that Havensight is where the community comes alive. | | |

The success of opening night set a positive tone for the upcoming Friday Nights at Havensight and more events! From the music and food to the warm smiles and lively dancing, the evening showcased the strength and unity of the community. It was a joyful reminder that when the Virgin Islanders gather, we celebrate not just for an event but each other.

Click on 'Play' ▶️ icon below to see more photos.

| | |

Ready to take the next step in your career? GERS Havensight Mall is looking for qualified, motivated, and dedicated individuals to join our team!

Vacancy include:

• Security Officer

Submit your resume today and embark on an exciting journey with us. Your next opportunity awaits! Submit your resume to hrdept@usvigers.com.

| | |

SIGN ME UP!

Or send an email to communications@usvigers.com, including your name in the email.

| |

| Did you enjoy this edition of the GERS Update? | | | | |

Customer Service

Phone: 340-693-3939

Email: customercare@usvigers.com

St. Thomas

3438 Kronprindsens Gade, Ste. 1

St. Thomas, VI 00802-5750

Phone: (340) 776-7703

Fax: (340) 776-4499

St. Croix

3004 Estate Orange Grove, Ste. 1

Christiansted, St. Croix

VI 00820-4260

Phone: (340) 718-5480

Fax: (340) 718-5498

| | | | |