|

The JUST RELEASED

2024 MID-YEAR OUTLOOK is HERE!

In case you missed it, make sure to take a look at the...

2024 Mid-year Outlook:

Still Waiting for the Turn

**IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. The economic forecasts may not develop as predicted. Please read the full MIDYEAR OUTLOOK 2024: Still Waiting for the Turn publication for additional description and disclosure. This research material has been prepared by LPL Financial LLC.

| |

Fait Accompli \fe takɔ̃ˈpli\ noun: an accomplished fact; a thing already done | |

|

Cornerstone Fait Accompli

Apples float because they are 85% water!

| | |

|

Did you see our latest post? |

Never miss a Cornerstone announcement - make sure you are following us on Facebook!

When you follow us you'll get access to up to date market information, helpful financial planning tools like calculators, and all of the Cornerstone office happenings!

| |

Click on the buttons below and don't forget to like, comment and share our posts! | |

|

How long has Don been with LPL?

Click the button below to find out!

| |

|

When it comes to investing, gold may be the antithesis of artificial intelligence (AI). The precious metal has acted as a store of value for thousands of years with zero technological innovation — gold is discovered, not developed. Gold is also a real tangible asset and can act as a potential hedge against inflation or a safe haven during times of crisis. Given these properties and the backdrop of a risk-on-record-setting equity market, many investors are wondering what’s behind the paradoxical price action of gold’s rally to new highs and how the yellow metal has matched the momentum in AI stocks over the last several months (gold and the equal-weight Magnificent Seven Index are both up around 20% since March). Herein we discuss the key drivers of gold and why this rally is no flash in the pan.

Melt Up in Gold

After consolidating sideways for several years, spot gold prices finally reached record highs in March. The rally continued into the summer months as expectations for a monetary policy pivot from the Federal Reserve (Fed) firmed. Interest rates and the dollar subsequently declined as the market began to price in higher probabilities for rate cuts. This was an expected response from gold, as lower U.S. interest rates and a weaker dollar increased the appeal of non-yielding bullion.

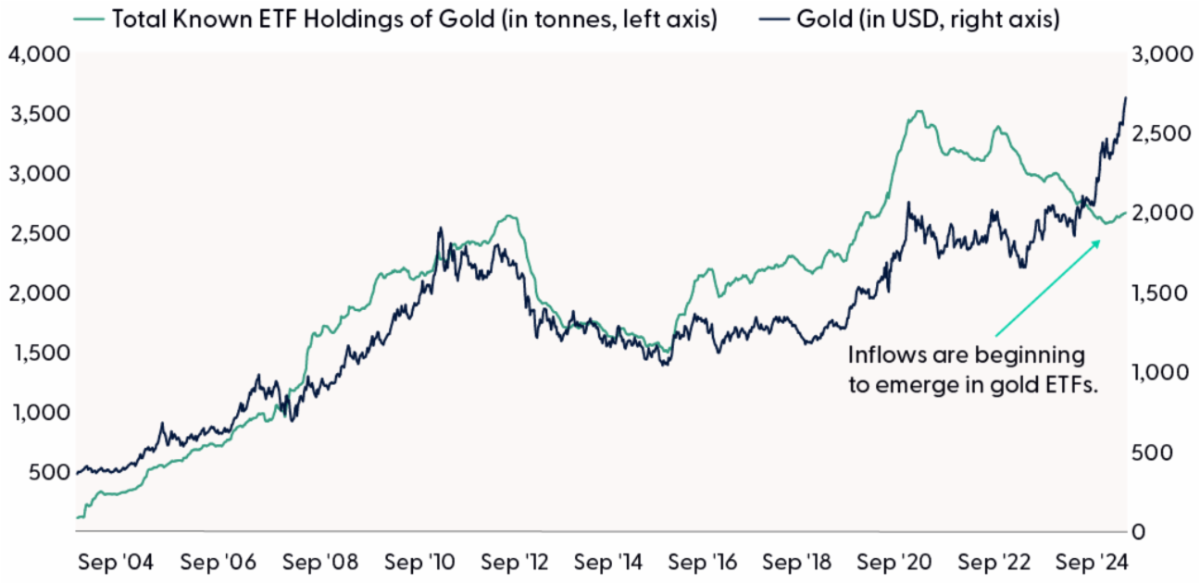

Perhaps more surprising is the lack of demand for gold exchange-traded funds (ETFs). Until recently, ETF holdings of gold had inexplicably decoupled from the precious metal over the last two years. However, with gold breaking out to new highs and creating a lot of headlines along the way, fear of missing out appears to be kicking in. Buyers have returned to chase this rally as gold ETF holdings recently reported seven straight weeks of positive inflows, marking the longest inflow streak since March 2022. History suggests this trend could continue as peaks in gold ETF holdings tend to occur after peaks in gold prices.

Gold Rallies to Record Highs as Inflows Into Gold ETFs Return

| |

|

Source: LPL Research; Bloomberg 09/26/24

Disclosures: Any futures referenced are being presented as a proxy, not as a recommendation. Past performance is no guarantee of future results

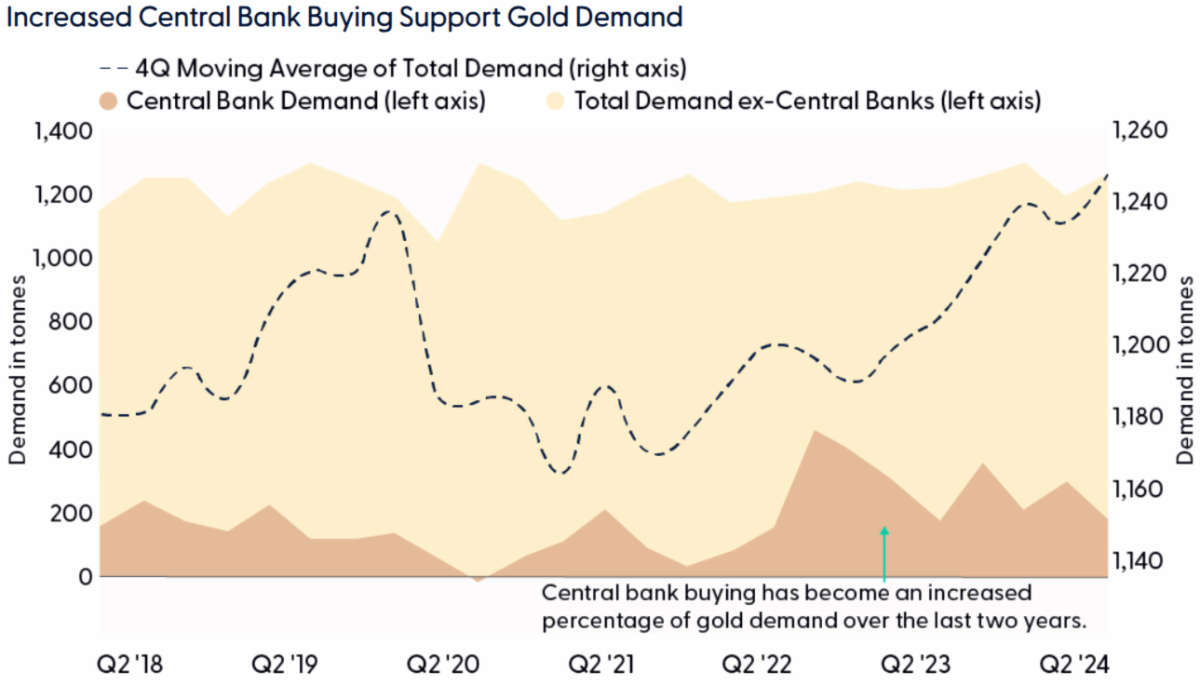

A weaker dollar and declining interest rates have played leading roles in gold’s rally to record highs. However, in recent years, central banks have increasingly played a supporting role. According to the World Gold Council, global central banks purchased record levels of gold in 2022, followed by near-record-level buying in 2023. More recently, global central banks bought 183 tonnes of gold in the second quarter, marking a 6% increase compared to last year. Rising demand has been driven by foreign central banks diversifying away from dollar reserves, partially due to worries about escalating U.S. deficits, and perhaps more significantly, concerns over the potential seizure of reserve assets by the U.S. government — as Russia witnessed after the 2022 invasion of Ukraine.

While the chart below highlights the increased impact central banks have had on aggregate gold demand, they are not the only ones buying the precious metal. According to the Commodity Futures Trading Commission (CFTC), managed money long positions (typically speculators, hedge funds) in gold recently reached their highest level since March 2020. Over-the-counter demand for gold has also jumped higher. India, the world’s second-largest consumer of gold jewelry, cut the import tax on gold to 6% from 15% in July. Imports of gold tripled the following month as Indian buyers ramped up purchases ahead of Diwali and wedding season this fall, where gold is often given as a traditional gift.

Increased Central Bank Buying Support Gold Demand

| |

|

Source: LPL Research, World Gold Council 09/26/24

Disclosures: Past performance is no guarantee of future results.

Rate Cuts vs. Gold

Rate cuts generally imply lower yields and a potentially weaker dollar — a recipe for stronger gold prices as other income-generating safe haven assets become less competitive and the commodity becomes cheaper to purchase. And while inflation is falling, potentially reducing the allure of gold as an inflation hedge, the direction of interest rates, central bank demand, and the geopolitical climate tend to have more of an impact on the yellow metal.

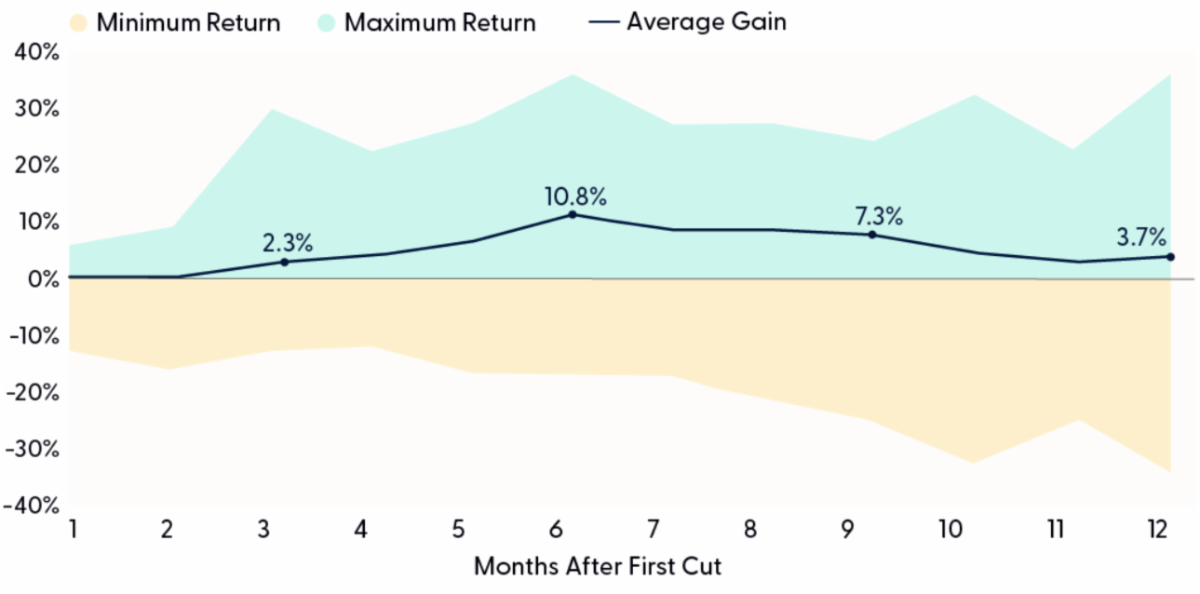

Of course, the Fed has a significant impact on interest rates, and with the pivot to rate cuts officially underway, we analyzed how gold performed after the Fed started cutting rates. Based on the last nine major rate-cutting cycles since the 1970s, gold has generated an average 12-month gain of 3.7% following the first rate cut. The peak in gold performance has historically been around the six-month window, where average gains reached 10.8%, suggesting current upside momentum could continue at least into the first quarter of next year.

Rate Cuts Supportive of Gold

|  | |

Source: LPL Research, Bloomberg 09/26/24

Disclosures: Any futures referenced are being presented as a proxy, not as a recommendation. Past performance is no guarantee of future results. Progression data based on first Fed rate cuts in 1974, 1980, 1981, 1984, 1989, 1995, 2001, 2007, 2019

Summary

Gold has climbed to new highs amid a backdrop of building broad-based demand, falling yields, a weaker dollar, and elevated geopolitical risk. Momentum could continue as the yellow metal has historically posted strong six-month returns after rate-cutting cycles begin. LPL’s Strategic and Tactical Asset Allocation Committee (STAAC) maintains a positive outlook on precious metals.

The Committee maintains its neutral stance on equities, though, with a slightly negative bias in the very short term based on the S&P 500 approaching overbought levels with deviating market breadth, historical seasonal weakness in October during election years, and political and geopolitical uncertainty. The STAAC expects volatility to remain elevated in the coming months as the market waits for more clarity on the economy, elections, and a better seasonal setup. For fixed income, the STAAC recommends a modest overweight, funded from cash, with an up-in-quality approach and benchmark-level interest rate sensitivity.

| |

Etymology /edəˈmäləjē/ noun: the origin of a word and the historical development of its meaning.

| |

Tulipmania: This was the first major financial bubble, which peaked in March 1637. Investors began to purchase tulips madly, pushing their prices to unprecedented highs; as prices drastically collapsed over the course of a week, many tulip holders instantly went bankrupt. | |

Have you taken advantage of

CAPS

yet?

Don't miss out!

Many of our clients ask how they benefit from taking action and initiating a Financial Plan for themselves.

When you sign up for our CAPS program, you will get access to:

A personalized financial plan, a place to keep all of

your accounts in one location and a secure place to store your

important documents.

| |

Le commentaire \ˈkɒmɛnt\ masculine noun: a French word meaning a remark or comment

| |

|

Cornerstone Commentaire

"Winter in an etching, Spring a watercolor, Summer an oil painting, and Autumn a mosaic of them all."

- Stanley Horowitz

| |

Stay Safe, Stay Kind, Stay Strong, Stay Well | |

|

P.S. Please feel free to forward this commentary to

family, friends, or colleagues.

+++++++++++++++++++++++++++

The highest compliment

you can give us would be the

referral

of your friends or family!

| |

Disclosures

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index.

Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

All investing involves risk, including possible loss of principal.

Commodities include increased risks, such as political, economic, and currency instability, and may not be suitable for all investors.

All index data from Bloomberg.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered inv estment advisor and broker -dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment a dvice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-0001819-0824W | For Public Use | Tracking #637565 (Exp. 09/2025)

| | | | |