|

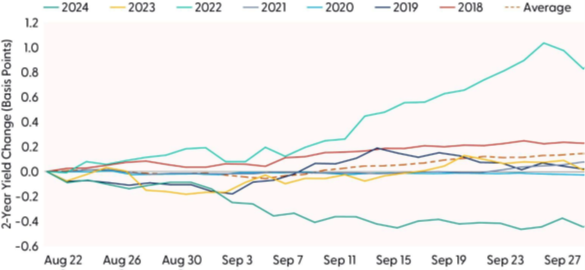

As central bankers, economists, and policymakers gathered last weekend in Wyoming’s Grand Teton National Park for the 2025 Jackson Hole Economic Symposium, the Federal Reserve (Fed) found itself at a critical juncture marked by political pressures, personnel changes, and internal divisions over monetary policy direction. Markets have positioned for dovish signals with 85% odds of a September rate cut, but historical patterns suggest Jackson Hole speeches often trigger reversals, as seen in 2022 when 2-year Treasury yields surged over 100 basis points following Fed Chair Jerome Powell’s hawkish remarks. The Fed’s simultaneous management of interest rate policy, personnel changes, quantitative tightening, and mounting political pressure from the White House represents an unusually complex policy environment. Fixed income investors face elevated volatility across markets as the institution that has long prided itself on independence and consensus navigates both external political pressures and internal disagreements during a period of mixed economic signals.

Jackson Hole Economic Symposium

The Kansas City Fed’s annual symposium, from August 21-23 with the theme “Labor Markets in Transition: Demographics, Productivity, and Macroeconomic Policy,” has long served as the world’s most exclusive economic gathering. What began in the early 1980s as a way to entice Fed Chair Paul Volcker through excellent fly-fishing opportunities has evolved into the premier venue for monetary policy announcements. The symposium’s 100-120 attendees have witnessed landmark moments, including Ben Bernanke’s 2010 signal for a second round of quantitative easing, Mario Draghi’s 2014 groundwork for European stimulus, and Jerome Powell’s 2020 introduction of average inflation targeting. This year’s gathering carried particular weight as Powell delivered what was likely his final Jackson Hole address as Fed chair, with markets placing roughly an 85% probability on a September rate cut before his comments but priced in a near certainty of a cut after his remarks were made public.

Highlights from Jerome Powell’s Jackson Hole Speech:

•Softer employment data has likely pushed the Fed toward rate cuts at their September 17 meeting. A well-telegraphed statement removes some of the uncertainty plaguing investors.

•Yields plummeted and equities rallied from the increased clarity about future rate decisions.

•Since last year’s Jackson Hole event, the upside risks to inflation have diminished and the unemployment rate has increased by almost a full percentage point (3.4% to 4.2%), a development that historically has not occurred outside of recessions. We think recession risks are low despite concerns that Q3 GDP growth will flatline.

•Tariff effects will be short-lived but not necessarily felt all at the same time. “It will continue to take time for tariff increases to work their way through supply chains and distribution networks.” We expect inflation metrics to accelerate over the next several months.

•Although not as exciting, Chair Powell discussed in his speech the four main revisions to the policy framework, a review the Fed does roughly every 5 years. Demographics, fiscal policy, and other factors suggest that the long-term neutral fed funds rate is likely higher than during the 2010s.

Bottom Line: The macro-outlook should convince the Fed to cut rates at the September 17 meeting. The hint of upcoming rate cuts will tamp down yields and bolster markets in the near term. But looking out on the horizon, structural shifts in the economy have created uncertainty about the long-run fed funds rate. Suffice it to say, the neutral rate will be higher than during the 2010s.

Monetary Mayhem at the Federal Reserve

The timing of this year’s symposium coincided with changes in Fed leadership that began earlier this summer and remain ongoing. In early August, Adriana Kugler, who had served as a Fed governor since September 2023, unexpectedly announced her resignation, stepping down six months before her term was scheduled to expire on January 31, 2026. As well, Powell’s chairmanship tenure ends May 2026. President Trump and Treasury Secretary Scott Bessent are vetting potential candidates and are expected to announce the next Fed chair in the coming months. Finally, late last week, accusations of mortgage fraud by Fed Governor Lisa Cook (but importantly, no formal charges have been made) drew Trump’s ire, and he stated that he would fire her if she didn’t resign.

President Trump moved to fill Kugler’s vacancy, announcing on August 7 his nomination of Stephen Miran, the current Chairman of the Council of Economic Advisers, to serve in Kugler’s seat through January 2026. The nomination represents Trump’s first attempt to reshape the Fed during his second term, though notably only on a temporary basis. Trump explicitly stated he would “continue to search for a permanent replacement,” suggesting Miran’s role may serve as a bridge appointment while the administration identifies a longer-term candidate.

Miran brings considerable economic policy experience, having served as a senior adviser at the Treasury Department during Trump’s first administration under Secretary Steven Mnuchin. A Harvard-trained economist, Miran has been instrumental in developing Trump’s tariff policies and is widely credited as a key architect of the administration’s trade strategy. His nomination requires Senate confirmation, which faces timing challenges given the chamber’s current recess schedule and anticipated Democratic opposition. The tight timeline makes it unlikely Miran could be confirmed and sworn in before the Fed’s September 16-17 policy meeting.

These leadership changes are unfolding against the backdrop of growing internal dissent within the Federal Open Market Committee (FOMC), most notably at the July 30, 2025 meeting. Marking the first multiple governor dissents since late 1993, the committee voted 9-2 to maintain the federal funds rate at 4.25-4.50%, with Fed Governors Michelle Bowman and Christopher Waller breaking ranks to advocate for immediate rate cuts of 0.25 percentage points.

The dissents reflected philosophical divisions about the appropriate policy stance amid mixed economic signals. While Chair Powell and the majority maintained a cautious wait-and-see approach, citing “elevated uncertainty” about the economic outlook, particularly regarding tariff impacts, the dissenters pushed for more aggressive accommodation based on concerns about labor market deterioration.

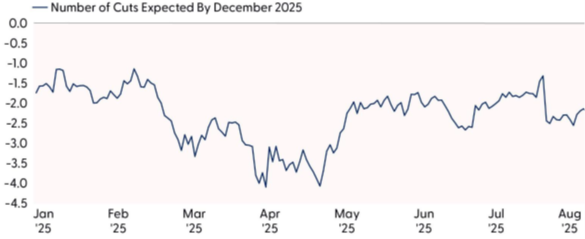

The timing of these dissents proved prescient when weaker-than-expected employment data emerged just days after the meeting. July payrolls showed only 73,000 new jobs added, far below expectations, while unemployment rose to 4.2% and prior months saw significant downward revisions. These developments dramatically shifted market expectations, with the probability of a September rate cut surging from around 50% immediately after the July meeting to over 85% by mid-August with markets now expecting two 0.25% cuts throughout 2025.

Markets Expect Two Rate Cuts This Year

|