Feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, reply to this e-mail with their e-mail address and we will ask for their permission to be added. |

|

March 16, 2021

This Week from Jesse W. Hurst, II

CFP® CERTIFIED FINANCIAL PLANNER™ • AIF® ACCREDITED INVESTMENT FIDUCIARY

|

|

Investylitics Monthly Report

Horizon Advisor Network Investment Committee

March 8, 2021

|

|

Executive Summary

- Markets have recently pulled back from their mid-February, all-time highs. Some of the hottest areas of the market, including technology, stay-at-home and emerging market stocks have pulled back the most, as we have seen a rotation toward value stocks.

- Much of the pullback has been driven by sharply rising interest rates. The yield on the 10- year Treasury bond has moved from approximately .9% at the beginning of the year to a high of 1.6% last week. This is a rise of more than 70% in a two-month period.

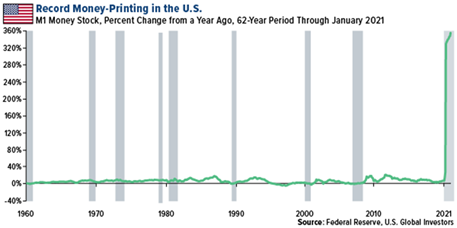

- The increase in economic activity sparked by the rollout of the vaccines, continued low interest rates, as well as support of the bond market by the Federal Reserve bank, and additional stimulus in the pipeline are sparking inflation fears over the next one to two years.

- Adding to these inflation fears, the ISM Manufacturing Report showed a surge in growth. The manufacturing gauge rose to the highest level since February 2018. Anecdotal comments from participants showed supply chain constraints, material shortages and prices rising rapidly.

- The committee continues to believe that the backdrop will remain constructive for risk assets such as stocks, real estate, and commodities over the cyclical horizon. However, we do expect bouts of volatility to continue given our economic and political backdrop.

The committee met on the afternoon of March 8th to review the most recent economic and investment data, and to review the allocation strategies of the portfolios managed by the committee members. We are happy to report that all our model portfolios continue to outperform their risk adjusted benchmarks over the most recent one, three and five year periods of time.

The markets have seen a pull back from their recent highs over the last several weeks. This is not surprising as the markets have moved up dramatically since late October, as the election outcomes became clearer, and as the rollout of the vaccines was imminent. Sectors of the market that have moved up rapidly since the market lows of late March 2020 were also the areas that pulled back the most recently. Technology, stay-at-home and emerging market stocks all pulled back 7-10%.

It seems that the catalyst for the recent pullback is a rise in interest rates sparked by fears of inflation over the next couple of years. Recent projections of economic growth from a number of economists and market strategists that the committee follows suggests that real GDP growth could be as much as 6-8% this year. To put this in perspective, we have not seen economic growth at this level in nearly forty years.

This is being fueled by a combination of factors including the continued rollout of the vaccines, as well as cases and hospitalizations continuing to drop across the United States. This should lead to the economy continuing to reopen, sparking an acceleration of economic activity. Additionally, the Federal Reserve Bank has pledged to keep borrowing costs low, and to continue purchasing $120B per month of both Treasury and mortgage bonds to support low interest rates in the bond market.

|

|

As mentioned last month, the Congressional Budget Office had already factored in much higher growth in U.S. economic activity and additional job growth prior to the passage of the American Recovery Act. This additional $1.9 trillion will throw additional fuel on the fire of an already strongly recovering economy. We shall see if this additional stimulus leads to higher inflation. We know that year over year comparisons will be against depressed levels of activity from the spring of 2020.

|

|

Adding to inflation fears, the ISM Manufacturing Reports showed a surge in growth. The manufacturing gauge rose to the highest level since February 2018. Anecdotal comments from participants showed supply chain constraints, material shortages and prices rising rapidly. See below:

Manufacturing PMI® at 60.8%

February 2021 Manufacturing ISM® Report on Business®

New Orders, Production & Employment Growing

Supplier Deliveries Slowing at Faster Rate; Backlog Growing

Raw Materials Inventories Contracting; Customers’ Inventories Too Low

Prices Increasing; Exports and Imports Growing

From a technical standpoint, the markets are bumping up against several lines of resistance. It is not unusual for the market to take a breather or to have some bouts of short-term volatility and pullback when facing this setup. We believe that the backdrop will remain constructive for the appreciation of risk assets such as stocks, commodities, and real estate over the cyclical horizon.

Against this backdrop, several of the committee members are looking at adjusting their model portfolios that would align them with the above economic outlook. This would include shortening bond maturities in the face of potentially rising interest rates and inflation. There may also be a higher allocation to value stocks which have lower prices than their growth brethren and would benefit from an accelerating economy, more international stocks which could benefit from a falling dollar, exposure to commodities which would benefit from increased demand for materials and supplies, and a potential to look at alternative assets that are not correlated to volatility in either the stock or bond markets. For clients in our discretionary models, you will see trade confirmations come through as adjustments are made.

The committee continues to work hard to meet the investment accumulation and income needs of our trusted friends and clients. We appreciate your confidence and support. As always, should you have any questions, please do not hesitate to reach out to your advisor. Thanks, and have a great day.

|

|

INVESTYLITICS TEAM OF HORIZON ADVISOR NETWORK

Jesse Hurst - Chair, Impel Wealth Management

Nathan Ollish - Impel Wealth Management

Clint Gautreau, Horizon Financial Group

Kevin Myers, ATL Global

Joy Schlie, FHT Financial Advisors

|

|

Sincerely,

Jesse W. Hurst, CFP®, AIF®

CERTIFIED FINANCIAL PLANNER™

Financial Advisor

|

|

*Award Recipient Jesse Hurst

*The 2021 ranking of the Forbes’ Best–in–State Wealth Advisors1 list was developed by SHOOK Research and is based on in–person and telephone due–diligence meetings to evaluate each advisor qualitatively and on a ranking algorithm that includes client retention, industry experience, review of compliance records, firm nominations, and quantitative criteria (including assets under management and revenue generated for their firms). Overall, approximately 32,725 advisors were considered, and 5,000 (approximately 15.3 percent of candidates) were recognized. The full methodology2 that Forbes developed in partnership with SHOOK Research is available at www.forbes.com.

1This recognition and the due–diligence process conducted are not indicative of the advisor's future performance. Your experience may vary. Winners are organized and ranked by state. Some states may have more advisors than others. You are encouraged to conduct your own research to determine if the advisor is right for you.

2Portfolio performance is not a criterion due to varying client objectives and lack of audited data. SHOOK does not receive a fee in exchange for rankings.

|

|

Is there something we can help you with? Please call me at 330.800.0182 or email me directly at [email protected].

|

|

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods. Sources: Yahoo! Finance, MarketWatch, djindexes.com, London Bullion Market Association. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable. |

|

Securities and advisory services offered through Cetera Advisors LLC, member FINRA/SIPC, a broker/dealer and a Registered Investment Adviser. Cetera is under separate ownership from any other named entity. Confidential: This email and any files transmitted with it are confidential and are intended solely for the use of the individual or entity to whom this email is addressed. If you are not one of the named recipient(s) or otherwise have reason to believe that you have received this message in error, please notify the sender and delete this message immediately from your computer. Any other use, retention, dissemination, forward, printing, or copying of this message is strictly prohibited. |

|

P: 330.800.0182 • TF: 844.422.5550 • F: 234.312.0460

|

|

|

|

|

|

|