Feel free to forward this commentary to family, friends, or colleagues. If you would like us to add them to the list, reply to this e-mail with their e-mail address and we will ask for their permission to be added. |

|

April 27, 2021

This Week from Jesse W. Hurst, II

CFP® CERTIFIED FINANCIAL PLANNER™ • AIF® ACCREDITED INVESTMENT FIDUCIARY

|

|

Investylitics Monthly Report

Horizon Advisor Network Investment Committee

April 20, 2021

|

|

Executive Summary

• Economic growth continues to accelerate, and most reports are coming in above expectations. Many of these are at levels not seen in years, and some are at their best levels ever.

• The US economy created 916,000 new jobs in March, well ahead of expectations, and the unemployment rate dropped to 6.0%. While there are still 4.0 million fewer people working today than there were prior to the pandemic, many economists expect monthly job growth of close to 1M over the next 4-6 months.

• The March Services PMI report came in at an all-time record level of 63.7%. This is extremely important as services make up more than 85% of the US economy. The business activity, new orders and employment components of the report all strengthened significantly.

• There continues to be concern that inflation will rise dramatically over the next 12-24 months. This comes as the economy reopens and consumers are in good shape with near record savings, as well as debt being paid down thanks to government stimulus checks and unemployment benefits. This could continue to put pressure on interest rates in the bond markets.

• The committee believes that this backdrop should continue to be supportive to asset prices in the stock, commodity and real estate markets. Any pullbacks should be temporary and viewed as opportunities to buy at cheaper prices.

The Investment Committee met on the afternoon of April 20th. The six members of the committee shared information and outlooks regarding the economy and market outlook from the various economists and market strategists that we follow.

The committee was happy to report that all our model portfolios have performed in line or above their comparable index-based benchmarks on a risk-adjusted basis over the last one, three, and five years. Recent adjustments to the model portfolios made by the committee seem to be working well and have us positioned for the continued re-opening of the economy.

Economic growth continues to accelerate with many economic reports coming in well above expectations. This was highlighted by the recent unemployment and jobs report, which showed that the U.S. economy created 916,000 new jobs. Not only was this well above expectations for 675,000 jobs to be created, the two previous months were revised upward as well. The unemployment rate dropped to 6.0%. Many economists expect that we will see job growth of more than 1M new jobs monthly over the coming months. This should do a lot of work to bring people back into the work force that lost jobs due to the coronavirus shutdowns, quarantines, and social distancing requirements from the spring of 2020.

Additionally, both the PMI reports on the manufacturing and service side of the economies came in well above expectations. The manufacturing PMI for the month of March registered 64.7%, an increase of 3.9% from the month of February. At the same time, the service sector of the economy, which makes up more than 85% of total economic activity, came in at an all-time record of 63.7%. The business activity new orders and employment components of the report all strengthened significantly.

|

|

There also continues to be concerns about rising inflation as the economy is re-accelerating quickly. This is highlighted by the Federal Reserve Bank’s recent GDP projections. Four times a year, the twelve Fed Governors put out their projections for inflation, unemployment, and GDP growth. In December, the consensus of the Fed was that GDP would grow at 4.2% in 2021, strongest rate we had seen in more than two decades. However, this number was revised upwards by nearly 50% in March, to projected GPD growth of 6.5%. This is a massive revision, as we have not seen GDP in the United States north of 6% since 1984.

All of this leads to the potential for inflation to pick up. Everybody seems to agree this will happen. The big question is whether or not this will be temporary or what the Fed refers to as transitory, or whether it will cause long-term higher inflation. If the latter turns out to be true, it will continue to put upward pressure on interest rates in the bond market. This could cause bond prices to decline.

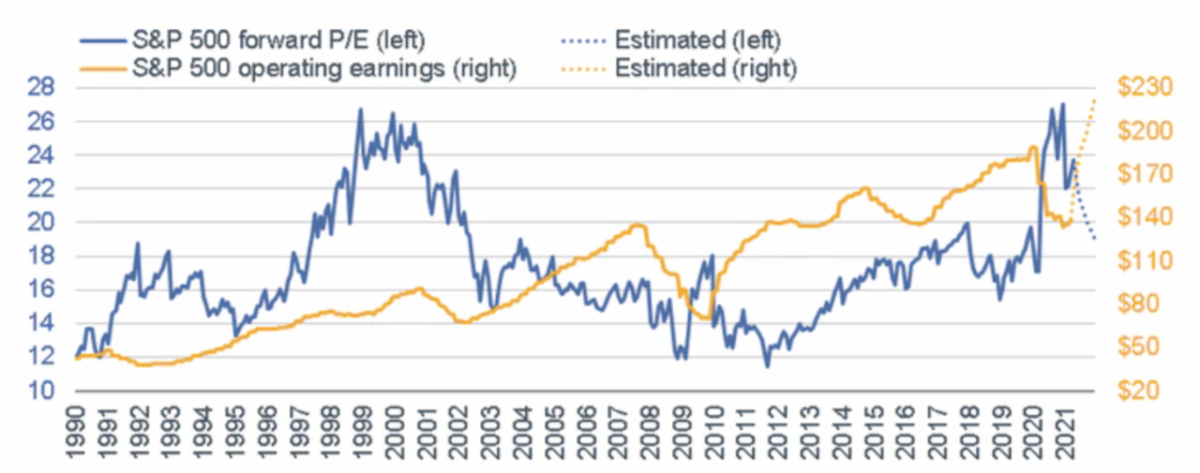

The investment committee believes that the above backdrop should continue to be supportive of asset prices in the stock, commodity, and real estate markets. From a technical standpoint, the stock market is short-term overbought, and valuations are stretched. However, as earnings growth kicks up over the next six months, on easy year over year comparisons, this should ease some of the valuation concerns (see chart below). The market has also, on a technical basis, broken to the upside above long-term resistance levels. This now gives us a floor of support going forward. Any pullbacks should be temporary and should be viewed as opportunities to buy at cheaper prices.

|

|

Source: Charles Schwab, Bloomberg, as of 4/16/2021. For illustrative purposes only.

The investment models from Impel Wealth Management underwent a major restructuring in February and March. This allowed us to shorten bond durations to reduce interest rate risk. We added additional foreign stock exposure, as foreign stocks are cheaper. This should benefit our models if the U.S. dollar falls due to the government printing money for stimulus while the Federal Reserve Bank is keeping interest rates low. We also introduced several bond-like proxies to help reduce interest rate risk in the portfolios. Finally, we added some direct commodity exposure to complement our gold position. This should benefit our models as supply chain constraints, rising input costs and rising inflation pressures endure.

We view managing a portfolio like driving a car. While the reports show our portfolios have done historically great, they are in essence looking through the rear- view mirror. However, we must drive the car looking through the windshield of what the future is bringing us from an economic and political standpoint. That way, we can continue to manage your hard-earned dollars entrusted to us in a reasonable manner.

The committee continues to appreciate and value you, our trusted friends and clients. Should you have any questions regarding these notes, please do not hesitate to reach out to your advisor. We look forward to continuing to serve you and help you reach your financial and investment goals. Thanks, and have a great day.

|

|

INVESTYLITICS TEAM OF HORIZON ADVISOR NETWORK

Jesse Hurst - Chair, Impel Wealth Management

Nathan Ollish - Impel Wealth Management

Clint Gautreau, Horizon Financial Group

Kevin Myers, ATL Global

Joy Schlie, FHT Financial Advisors

|

|

Sincerely,

Jesse W. Hurst, CFP®, AIF®

CERTIFIED FINANCIAL PLANNER™

Financial Advisor

|

|

*Award Recipient Jesse Hurst

*The 2021 ranking of the Forbes’ Best–in–State Wealth Advisors1 list was developed by SHOOK Research and is based on in–person and telephone due–diligence meetings to evaluate each advisor qualitatively and on a ranking algorithm that includes client retention, industry experience, review of compliance records, firm nominations, and quantitative criteria (including assets under management and revenue generated for their firms). Overall, approximately 32,725 advisors were considered, and 5,000 (approximately 15.3 percent of candidates) were recognized. The full methodology2 that Forbes developed in partnership with SHOOK Research is available at www.forbes.com.

1This recognition and the due–diligence process conducted are not indicative of the advisor's future performance. Your experience may vary. Winners are organized and ranked by state. Some states may have more advisors than others. You are encouraged to conduct your own research to determine if the advisor is right for you.

2Portfolio performance is not a criterion due to varying client objectives and lack of audited data. SHOOK does not receive a fee in exchange for rankings.

The views stated in this piece are not necessarily the opinion of Cetera Advisors LLC and should not be construed directly or indirectly as an offer to buy or sell any securities. Due to volatility within the markets mentioned, opinions are subject to change without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results.

|

|

Is there something we can help you with? Please call me at 330.800.0182 or email me directly at [email protected].

|

|

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods. Sources: Yahoo! Finance, MarketWatch, djindexes.com, London Bullion Market Association. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable. |

|

Securities and advisory services offered through Cetera Advisors LLC, member FINRA/SIPC, a broker/dealer and a Registered Investment Adviser. Cetera is under separate ownership from any other named entity. Confidential: This email and any files transmitted with it are confidential and are intended solely for the use of the individual or entity to whom this email is addressed. If you are not one of the named recipient(s) or otherwise have reason to believe that you have received this message in error, please notify the sender and delete this message immediately from your computer. Any other use, retention, dissemination, forward, printing, or copying of this message is strictly prohibited. |

|

P: 330.800.0182 • TF: 844.422.5550 • F: 234.312.0460

|

|

|

|

|

|

|