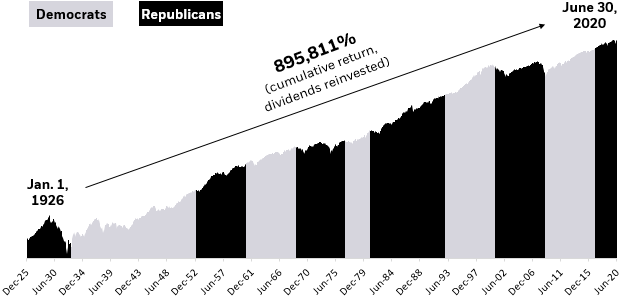

Source: Morningstar as of 6/30/20. Stock market represented by the S&P 500 Index from 1/1/70 to 6/30/20 and IA SBBI U.S. large cap stocks index from 1/1/26 to 1/1/70. Past performance does not guarantee or indicate future results. Index performance is for illustrative purposes only. Index performance does not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Past performance does not guarantee future results.

Additionally, as vaccines continue to roll out across the United States and globally, and more of the population becomes vaccinated, it should allow a continuing acceleration in restarting business activities that have been slowed by social distancing and quarantines. We have seen this play out once again as recent economic data has slowed due to the most recent spike in COVID-19 new cases and deaths.

Over and above this, the Federal Reserve Bank has pledged to keep interest rates near zero for the next several years; even if it means allowing inflation to run above their 2% target. This is an important change in Fed policy that was articulated by Fed chairman Jerome Powell in August.

Added to all of this is a massive amount of both fiscal and monetary stimulus that has been thrown at the economy since the pandemic took hold in March of 2020 with the recent $908B of additional stimulus passed by Congress and signed into law by President Trump in early January. This brings the total fiscal stimulus passed by the government this year, to more than $3.5 TRILLION with a “T”. In addition, the Federal Reserve Bank has seen its balance sheet balloon from $4T to $7T due to purchases of over $3T of bonds, mostly Treasury bonds and mortgages to backstop liquidity in the bond market and provide support to the banking system. Over time, this should be additive to asset prices in the stock market, real estate and commodity markets.

From a technical standpoint, the market is showing signs of being overbought in the short-term. There is also excessive levels of positive investor sentiment and optimism, which tends to be a contrarian indicator. From a historical basis, this tells us that we should not be surprised to see a short-term pullback or even correction, in what has been an incredibly strong market surge over the last nine months. Volatility and pullbacks should not be a surprise, and are a regular occurrence in a successful, long term investor's life. We believe that with the above factors in place, investors should not panic and should view any temporary downturns as opportunities to add to their positions at slightly lower prices, as we believe risk markets will continue to appreciate during the 2021 calendar year.

After an unforgettable 2020, many people are looking forward to better times in 2021. We agree. We think that we should be optimistic, but not greedy in our overall outlook. In addition to having the opportunity to buy low when markets pull back, we would suggest that clients continue to sell when markets are near all-time highs to create any cash they will need for liquidity or withdrawal purposes over the next 6 to 12 months, or even perhaps a little further out if you want to be more conservative.

If you have questions about how these issues affect your personal financial situation, please do not hesitate to reach out to your financial advisor. The team at Horizon Advisor Network continues to appreciate your trust and confidence in our team and process and we are here for you, our trusted friends and clients.

Sincerely,

Jesse W. Hurst, CFP®, AIF®

Certified Financial Planner