|

High and persistent inflation continues to inflict harm on Americans.

-

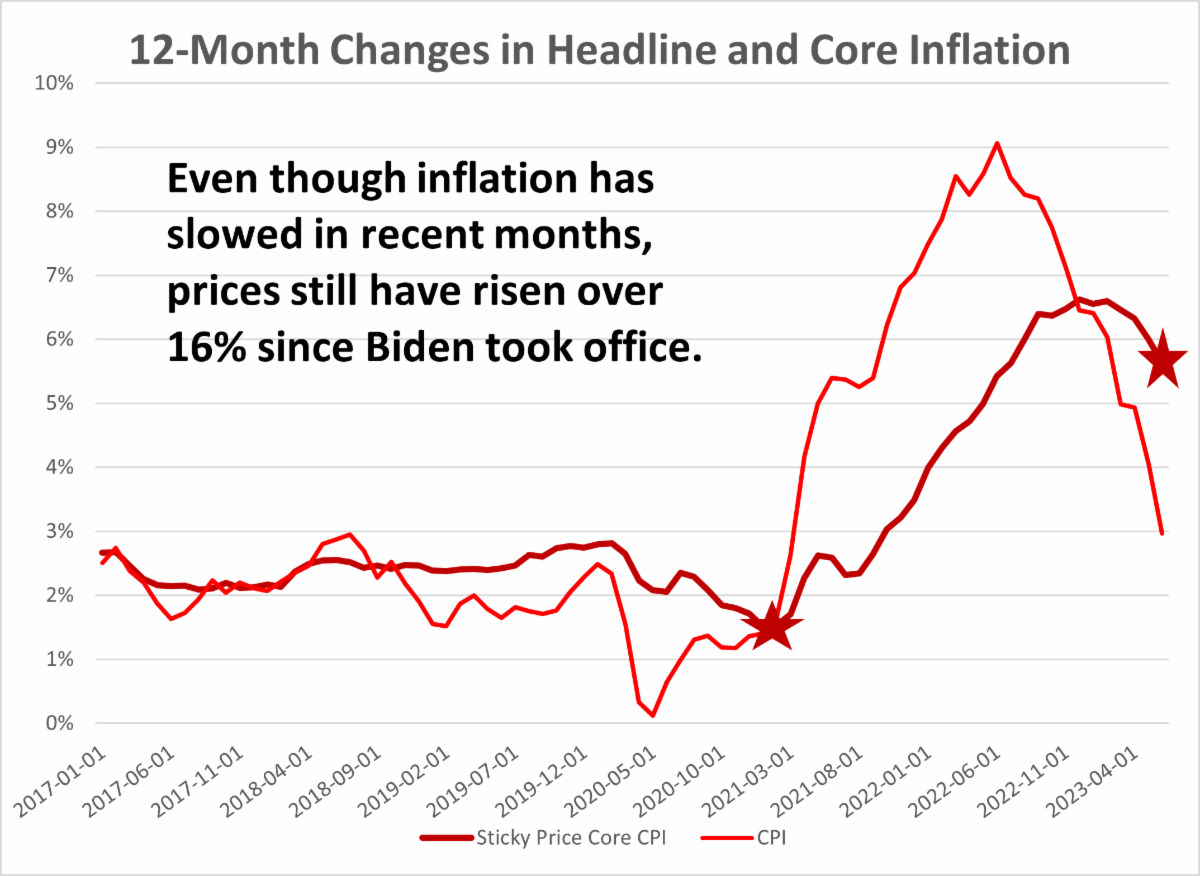

The BLS announced today that inflation increased in June at 3 percent from the same month last year. Core inflation that excludes food and energy rose 4.8 percent over the past 12-months, continuing to burden American budgets with higher living costs.

-

Core inflation in services, which comprises most of the total consumption basket for households, remains elevated and showed little improvement in slowing.

-

Since the Biden administration took office, prices have increased over 16 percent, and the annual cost of inflation has been estimated to harm American households upwards of $8,900. This will continue to inflict harm as inflation remains elevated.

-

Unless wages increased above the 16 percent rise in inflation, Americans have had an effective pay cut, reflected in part by the quarterly contraction in real hourly compensation since mid-2021.

-

While the rate of inflation growth has slowed from a peak of 9.2 percent last June, inflation is still meaningfully above the Federal Reserve target rate of inflation of 2 percent. Fed Officials have indicated that it could take several more years for inflation to slow to the Fed’s 2 percent target.

|  | |

High inflation has led to economic uncertainty and recessionary conditions.

-

High inflation imposes long-run costs on the economy, making it harder for households to save and invest in the future, and disrupting businesses’ ability to plan. The economic uncertainty impacts key business decisions, whether to invest in new plant, equipment, and other forms of physical and human capital that drive innovation, productivity growth, and ultimately overall standards of living.

-

Small businesses continue to report inflation and labor quality as the top challenges, with owners citing that they continue to raise prices at the level of inflation to deal with higher costs of inventory, labor, and energy.

-

U.S. manufacturing activity contracted in June for the eighth straight month, declining 0.9 percentage points from May. This is the longest period of contraction in U.S. manufacturing since the Great Recession, and reflects greater uncertainty and slower economic conditions, with households and businesses facing elevated borrowing costs, dampening credit, and lending conditions.

-

In June, the BLS reported that manufacturing labor productivity decreased 2.5 percent for the first quarter of 2023, instead of the initial estimated decrease of 1.3 percent. The revision accounts for a 1.5 percentage point downward change to output and a 0.2 percentage point downward revision to hours worked. Manufacturing job growth was flat in June.

-

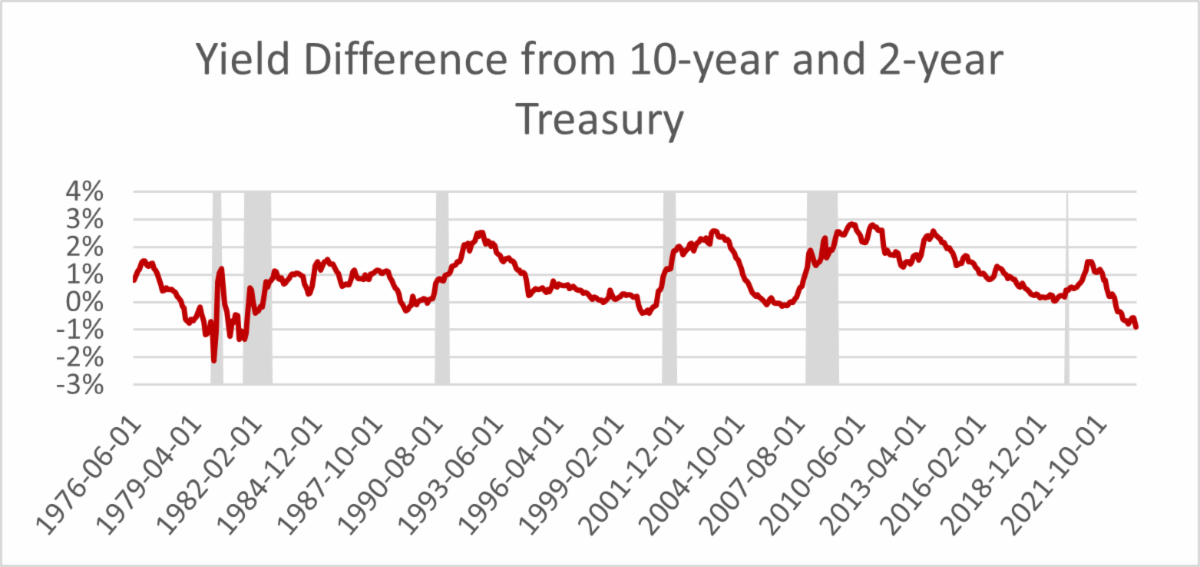

The Treasury yield curve inversion continues to steepen, marking the longest stretch of rate inversion since the 1980s. The Federal Reserve recession model, based on the inverted yield curve, estimates a 71 percent probability of a technical recession in the next 12-months.

-

Financial risks continue to mount in the economy. Corporate bankruptcies rose to the highest level since 2010 in the first half of the year, and insolvencies are expected to increase over the remainder of the year. By June, there were 340 corporate bankruptcies, 93 percent higher from the same period last year, and above the level in 2020 during the Covid pandemic recession.

-

Two key metrics used by the National Bureau of Economic Research (NBER) in its determination of a technical economic recession continue to decline. The annualized real (inflation-adjusted) Gross Domestic Product (GDP) rate slowed from 2.6% in the fourth quarter of 2022 to 2.0% in the first quarter of 2023, and real Gross Domestic Income—an alternate measure of total economic activity to GDP—was negative 3.3% in the fourth quarter of 2022 and remained at negative 1.8% in the first quarter of 2023.

|  | |