INFLATION IS QUIETLY & RELENTLESSLY COMING IN DIFFERING WAVES

As we outlined in this month's LONGWave video we expect Stagflation to be on the economic horizon as a direct result of the forces of: Covid-19, De-Globalization, the Global Recession and De-Dollarization. These events will be the catalytic drivers for the decreases in GDP, increases in unemployment, a fall in demand & profits as well as mounting inflation pressures.

In the immediate term we see confirming signals of growing inflation pressures based on the following:.

1- FED IS SIGNALING INFLATION ABOVE 2% IS OK?

Top Fed officials made it known to the Wall Street Journal last week that they would no longer make 2 percent inflation their target. They are of the belief that the target limits their ability to centrally plan economic growth and therefore the Fed officials decided to abandon it.

"In the next few months, the Federal Reserve will be solidifying a policy outline that would commit it to low rates for years as it pursues an agenda of higher inflation and a return to the full employment picture that vanished as the coronavirus pandemic hit.

Recent statements from Fed officials and analysis from market veterans and economists point to a move to "average inflation" targeting in which inflation above the central bank's usual 2% target would be tolerated and even desired.

To achieve that goal, officials would pledge not to raise interest rates until both the inflation and employment targets are hit." - CNBC

2- FED TO PRINT ANOTHER $1.8T or 2.5X MORE THAN CURRENTLY EXPECTED BY YE 2020 2- FED TO PRINT ANOTHER $1.8T or 2.5X MORE THAN CURRENTLY EXPECTED BY YE 2020

My esteemed colleague Richard Duncan has just released his typical well researched and accurate predictions on what the Fed is likely (and will be forced) to do between now and the end of the year.

If the Treasury borrows $2,163 during the second half, that would amount to an average of $360 billion per month. The Fed, however, has led the market to believe that it will create "only" $120 billion per month, which would amount to $720 billion during the second half.

If the Fed does only create $120 billion per month, that would be far too little to finance what the government intends to borrow. In that case, the government would have to borrow $240 billion per month ($360 billion - $120 billion) from the private sector.

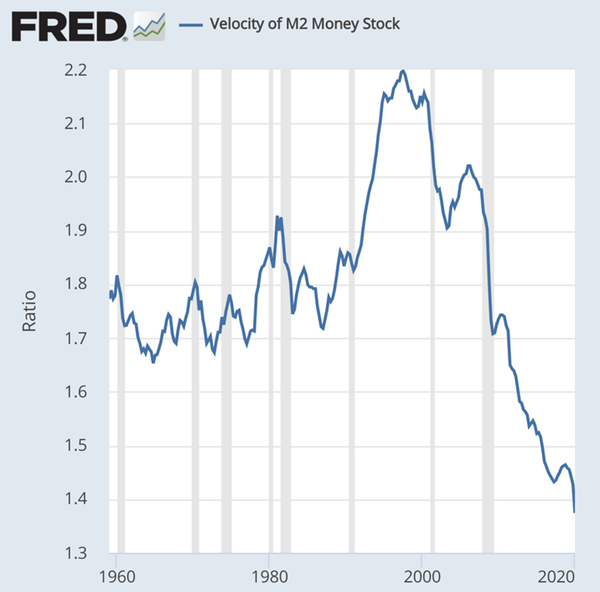

3- VELOCITY OF MONEY LIKELY TO NORMALIZE SLIGHTLY HIGHER (INFLATION)

In this month's LONGWave I spelled out that the money banks are handing out today is now going straight to businesses and consumers. Generally, they are not currently spending it, but as lock-downs lift this will have an impact. We can expect the Velocity of Money to likely normalize back to around 1.4 (currently ~0.8) sometime next year (see Addendum II below). Given the money supply we have already seen, this would give you an inflation rate of 4%. Plus, there is no reason Velocity should stop at 1.4, it could easily rise above 1.7 again.

"The chosen solution to a debt crisis is more debt. There is no escaping it. You cannot cut it back unless you can create a tremendous amount of economic growth to offset it. There is nothing the central banks can do.... You don't solve a debt problem with more debt!" --- Hans Mikkelsen, a credit strategist at Bank of America.

AUGUST UnderTheLens Video

- VIDEO: 20 Minutes with 39 supporting slides. STAGFLATION INVESTING

|

|

|

ADDENDUM TO THE AUGUST LONGWave VIDEO

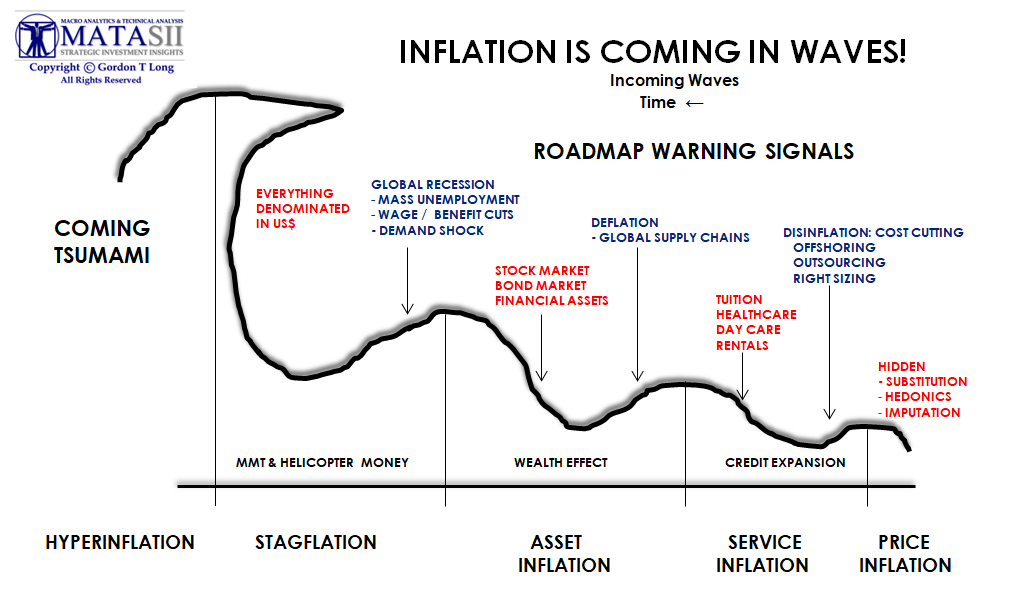

1- INFLATION COMING IN INCREASING WAVES

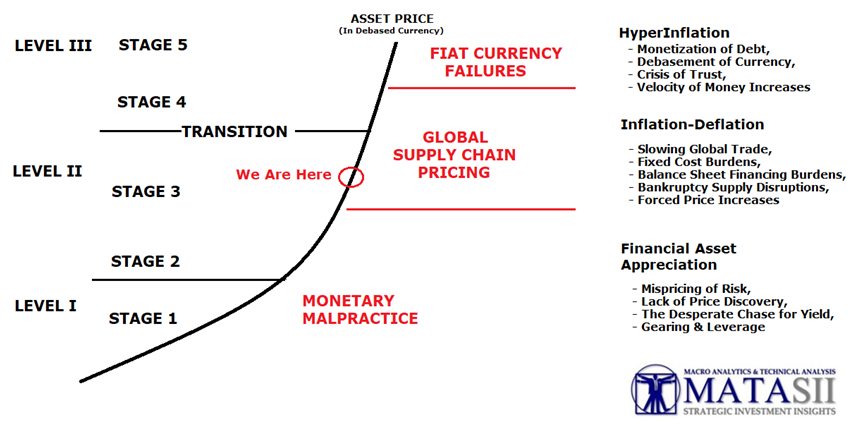

Due to Monetary & Fiscal Policy intended to offset lack of economic growth and forestall the impacts of business cycle impacts on an over-leveraged and over indebted financial system, the Central banks have been trapped into ever increasing inflationary waves.These waves are bringing inflation to an ever broadening global economic constituency.

STAGES OF INFLATION / DEFLATION WAVES

We view Inflation and Deflation as best viewed simplistically as taking hold in sequential and increasing waves as illustrated below and marked by larger peaks visibly lead by:

- Price Inflation,

- Services Inflation,

- Asset Inflation,

- Stagflation,

- Hyperinflation.

The Monetary/ Fiscal Policy stages could be encapsulated as 1-Credit Expansion, 2- Wealth Effect, 3- MMT & Helicopter Money and 4- Hyperinflation

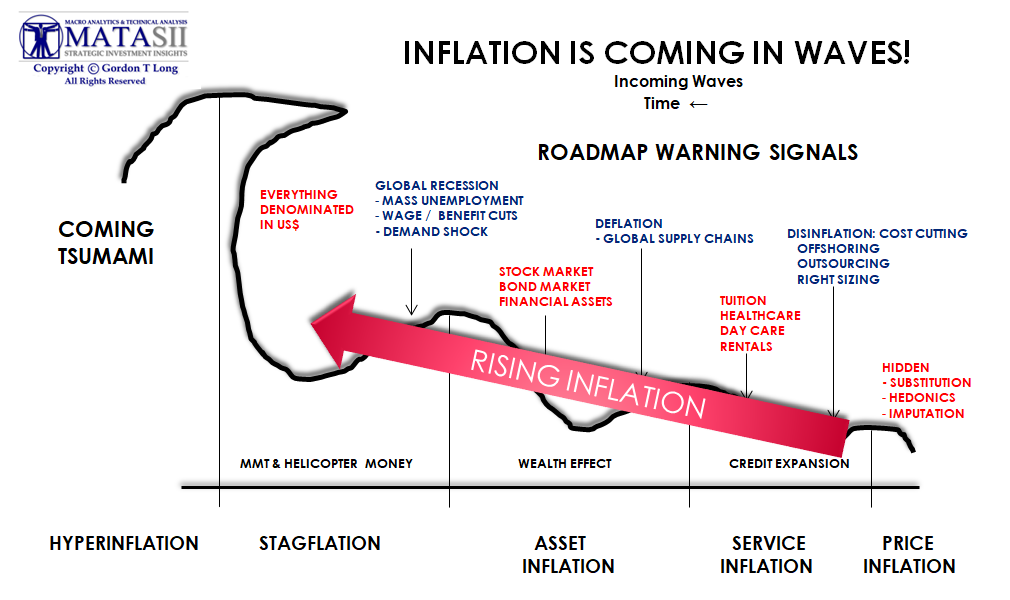

INFLATION WAVES HAVE BECOME INCREASING LARGER & MORE BROAD BASED

Due to Monetary & Fiscal Policy intended to offset lack of Economic Growth and forestall the impacts of business cycle impacts on an over-leveraged and over indebted financial system, the Central banks have been trapped into ever increasing inflationary waves.These waves are bringing inflation to an ever broadening economic constituency.

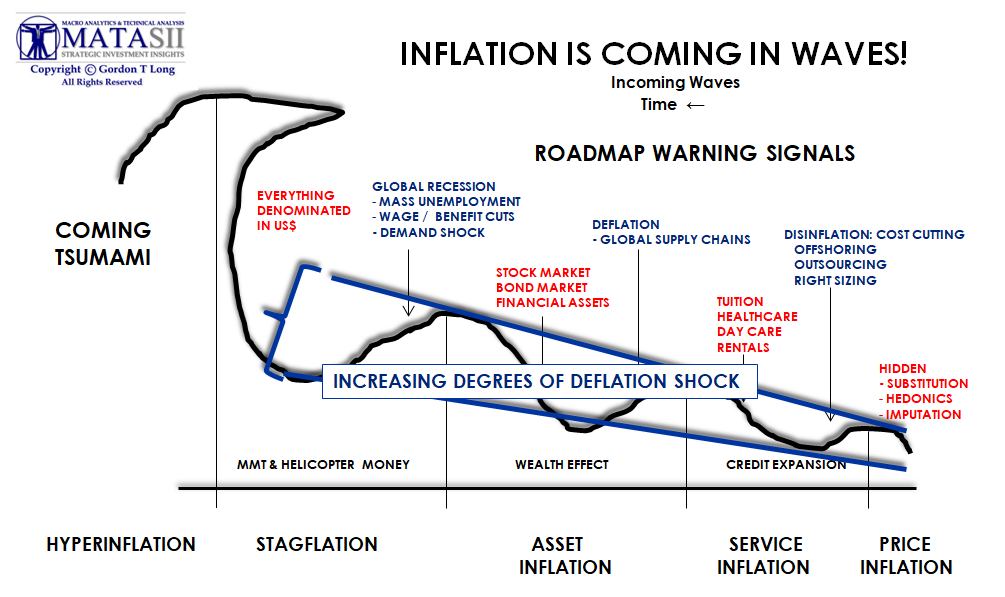

DEFLATIONARY WAVES ARE ARE INCREASINGLY GLOBAL & SYNCHRONIZED ACROSS MORE COUNTRIES

On the other hand the effects of coordinated central bank policies have taken hold of the increased globalization of the world's economy. This in turn has increased and broadened the impact of Deflationary forces..

The end game will eventually result in fiat currency failures or more hopefully a New Coordinated Bretton Woods Global Financial System.

2- VELOCITY OF MONEY NORMALIZATION

The We should expect that by YE 2020 to see the Velocity of Money to normalize back to rates slightly higher than we are currently experiences due in large part to massive stimulus "floating" out in the global economy.

EXPECT POST COVID-19 MONEY VELOCITY TO NORMALIZE SLIGHTLY HIGHER

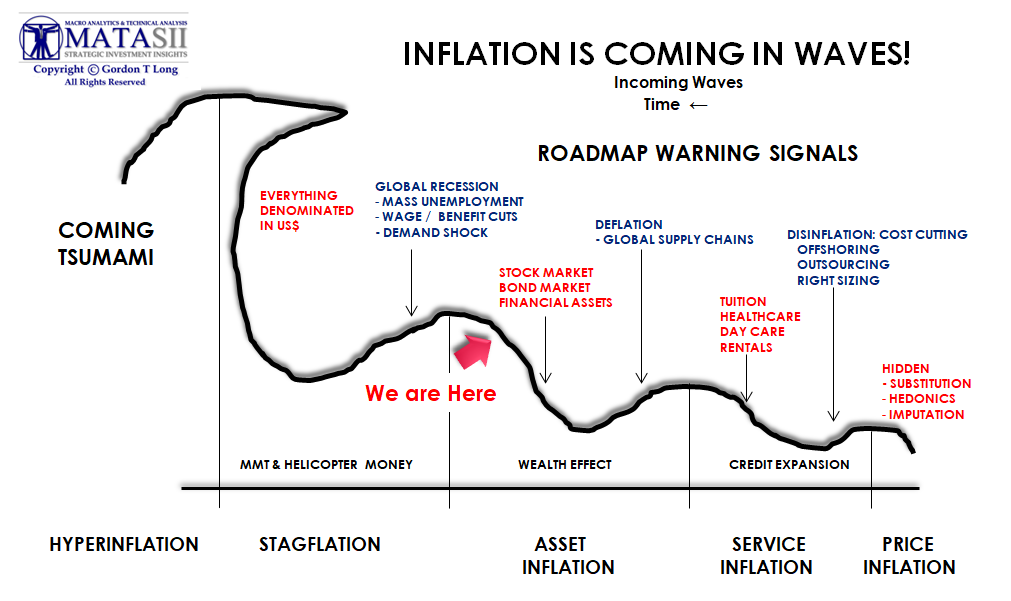

We are presently likely living through another deflation shock but by 2021 inflation could easily be at or near 4% in the US and most of the developed world by 2021.

-

- This projection is primarily based on expectations of a normalization of the Velocity of Money.

- Velocity in the US is probably at around 0.8 right now. The lowest recorded number before that was 1.4 in December 2019, which was at the end of a multi-year downward trend.

- Quantitative easing was an important factor in that shrinking velocity, because central banks handed money to savings institutions in return for their Treasury securities. And all the savings institutions could do was buy financial assets.

- They couldn't buy goods and services, so that money couldn't really affect nominal GDP.

The money banks are handing out today is going straight to businesses and consumers. They are not spending it right now, but as lock-downs lift, this will have an impact. The Velocity will normalize back to around 1.4 sometime next year. Given the money supply we have already seen, that would give you an inflation rate of 4%. Plus, there is no reason Velocity should stop at 1.4, it could easily rise above 1.7 again.

Additionally:

- For the last three decades, China was a major source of deflation.

- We are at the beginning of a new Cold War with China, which will mean higher prices for many things.

|

|

MATASII'S STRATEGIC INVESTMENT INSIGHTS

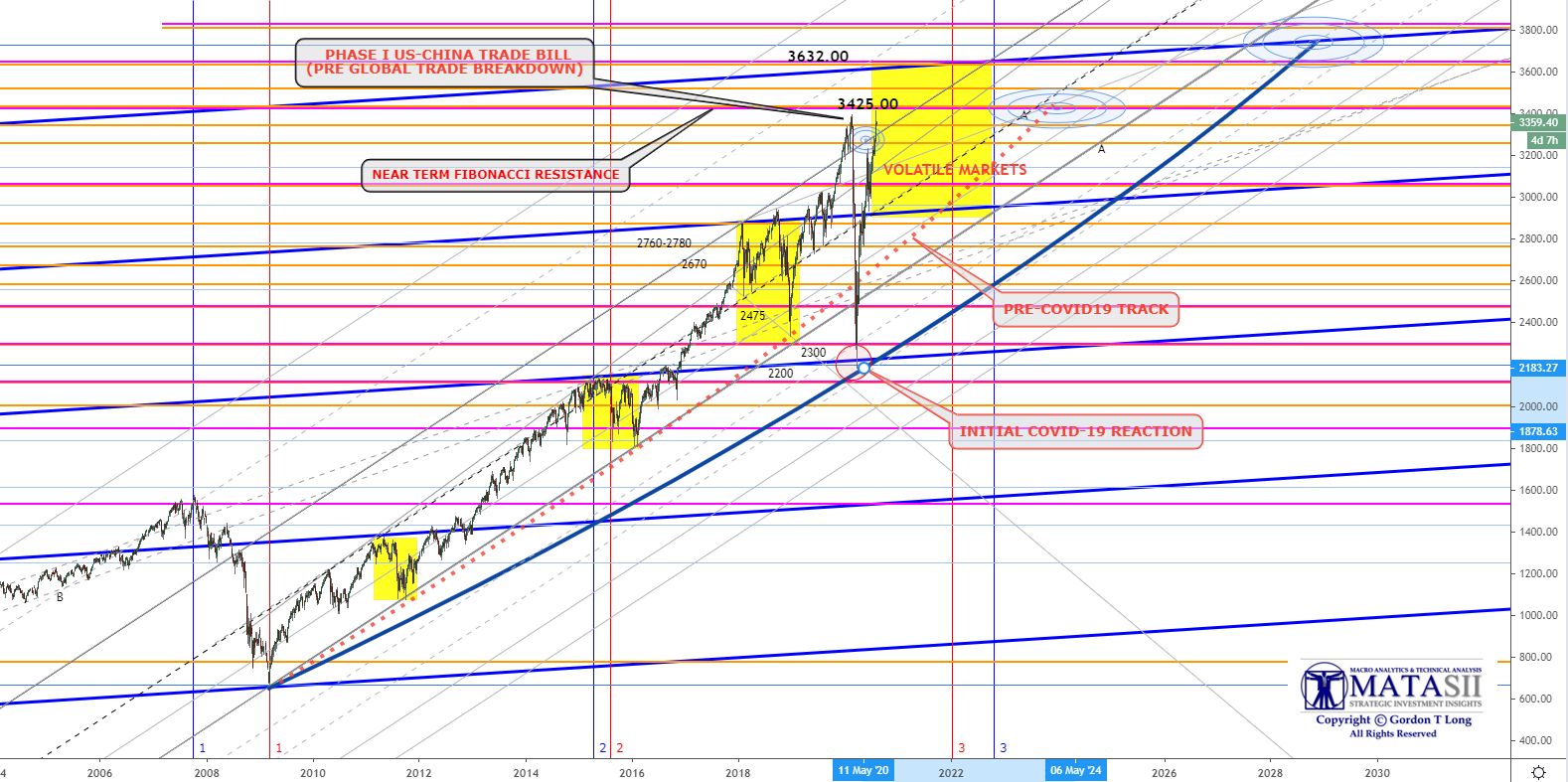

MORE MARKET UPSIDE BEFORE NEXT DEFLATIONARY CYCLE TAKES HOLD

WE ARE SETTING THE STAGE FOR BROADENING DEFLATIONARY PRESSURES

As the schematic below indicates we believe there is more market upside associated with the Federal Reserves focus on an increasing Wealth Effect before the building pressures of Deflation hit.

The Global Recession (or worse) which lies due to a Demand/Supply shock to the global Supply Chain is quickly taking hold of the real economy. The evidence is overwhelming and indisputable and only obscured partially by near term market euphoria. The Era of MMT and "Helicopter" money is only in its infancy as a historic "Regime Change" in Monetary & Fiscal Policy is now underway for ALL FIAT CURRENCY BASED CENTRAL BANKS.

MATASII FIBONACCI PROJECTIONS

The markets have higher prices ahead but we can expect increased market turmoil and volatility over the 18-24 months.

Your LIVE DESK TOP / TABLET / PHONE

MACRO ANALYTIC Video Chart Link: SUBSCRIBER LINK

NOTE: Any Problems with this Chart: E-Mail lcmgroupe2@comcast.net

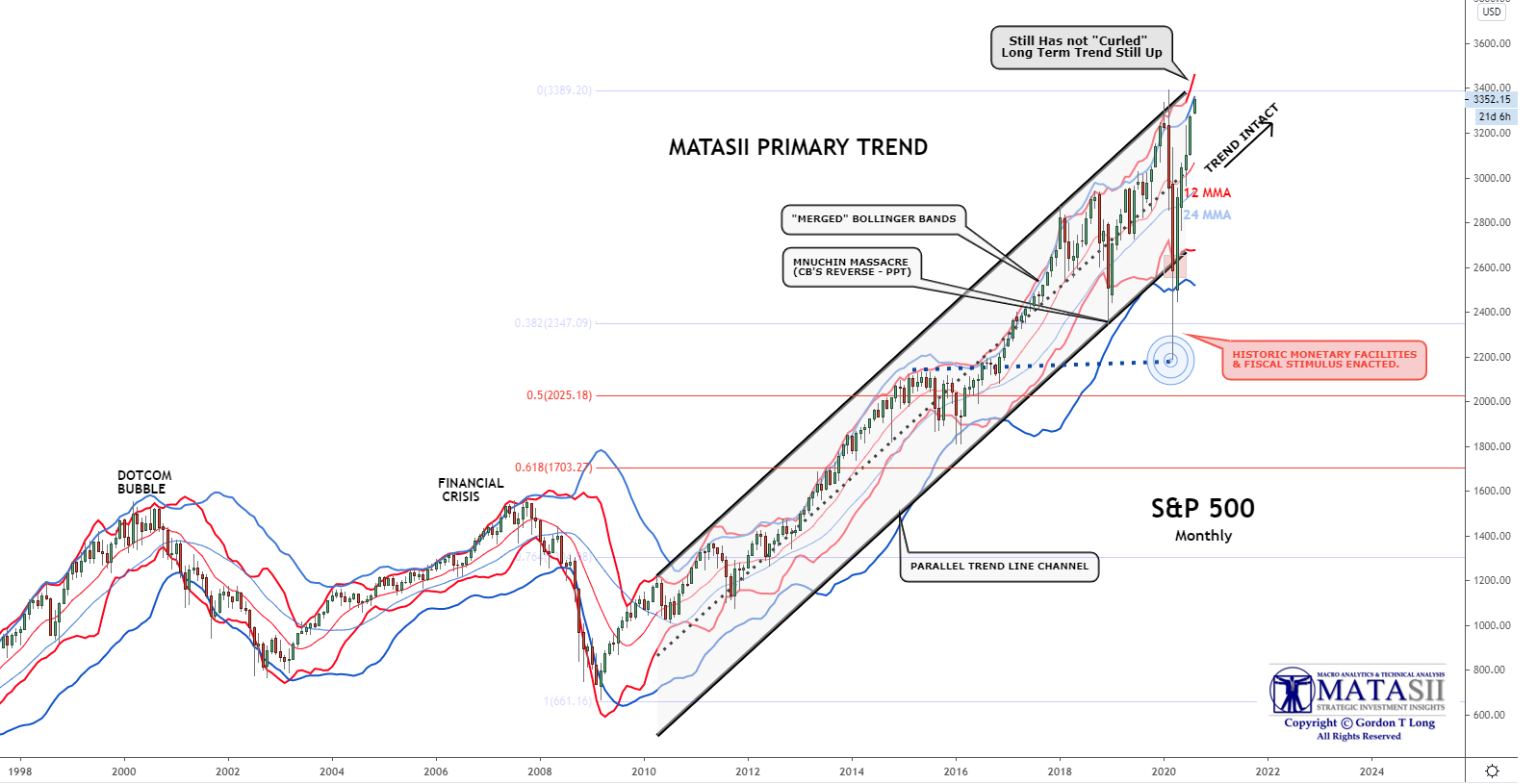

MATASII LONG TERM S&P 500 PRIMARY TREND - MONTHLY

Despite the February Covid-19 market sell-off the rising trend channel for the S&P 500 has not been violate. Though we do see a consolidation/correction in the near term the markets are headed higher in the intermediate to longer term.

NOTE: Do not confuse Market Activity with the Economy and Economic Activity. They are presently disconnected with the markets being presently controlled by Monetary & Fiscal Policy.

Your LIVE DESK TOP / TABLET / PHONE

MACRO ANALYTIC Video Chart Link: SUBSCRIBER LINK

NOTE: Any Problems with this Chart: E-Mail lcmgroupe2@comcast.net

|

|

LONGWave - AUGUST 2020

MATA PERSPECTIVE:

VIDEO: 20 Minutes with 39 supporting slides.

CURRENTLY AVAILABLE TO SUBSCRIBERS ONLY

FULL TRANSCRIPTION: CLICK

|

|

|

|

|

|