|

This months issue is a 6 min read

Download Images or Open in Browser for optimal viewing

|

| |

February's defining moment came on the 20th, when the U.S. Supreme Court struck down the IEEPA-based emergency tariffs in a 6-3 ruling. For Canada, the relief was real but incomplete. Within hours Trump signed a new executive order imposing a 10% global tariff under Section 122, with CUSMA-compliant goods exempt. Roughly 90% of Canadian exports to the U.S. remain tariff-free, but the steel, aluminum, and auto tariffs imposed under separate legislation stay in place. The ruling shifts the terrain without resolving the uncertainty, and CUSMA renewal talks in July will be the next major milestone.

Domestically, the earnings season was strong. All six of Canada's major banks beat Q1 expectations, gold touched intraday highs above $5,200 USD/oz on safe-haven demand, and the TSX closed the month at record levels. The loonie, however, continues to trade in a narrow range around 0.73, caught between trade optimism and persistent macro headwinds.

Against this backdrop, the timing of PDAC could not be more relevant. Running next week, the world's biggest mining convention will be shaped heavily by the global trading regime, tariffs, gold's record run, and the accelerating race for critical minerals. With over 1,300 exhibitors, 700 presenters and programming spanning across markets, geology, and politics, this conference acts as both a barometer for sentiment and as a genuine deal-making marketplace.

But not every investment theme this year is being forged underground. While the resources sector navigates a bullish yet complicated outlook, one of the most consequential investment opportunities of the decade is playing out in the clinic. This month's feature explores GLP-1 drugs; what they are, who controls the market, and what investors should understand before positioning.

| | |

From TradingView

As of close on Thursday February 26, 2026

| |

Weight of the World

GLP-1 Drugs and the Opportunity Behind Them

| | |

Few developments in modern medicine have captured the attention of patients, physicians, and investors quite like GLP-1 receptor agonists. In a remarkably short time, these drugs have moved from niche diabetes treatment to the centre of a global health and capital markets story.

What Are GLP-1s?

GLP-1 stands for glucagon-like peptide-1, a hormone naturally produced in the gut that regulates blood sugar and appetite. GLP-1 receptor agonist drugs mimic this hormone, suppressing appetite, slowing digestion, and enhancing insulin response. The result is better glycemic control for people with type 2 diabetes and meaningful, sustained weight loss for patients with obesity.

The health benefits extend well beyond blood sugar. Clinical evidence now supports the use of GLP-1s in reducing the risk of major cardiovascular events, treating sleep apnea, and managing fatty liver disease. The global market - valued at roughly $52 billion USD in 2024 - is projected to reach $187 billion by 2032, and the WHO issued its first formal recommendation for GLP-1 therapy in obesity treatment in December 2025.

A Market With Two Dominant Players - and a Widening Gap

The GLP-1 market is effectively a duopoly. Eli Lilly and Novo Nordisk control virtually all prescription volume, but their trajectories have sharply diverged.

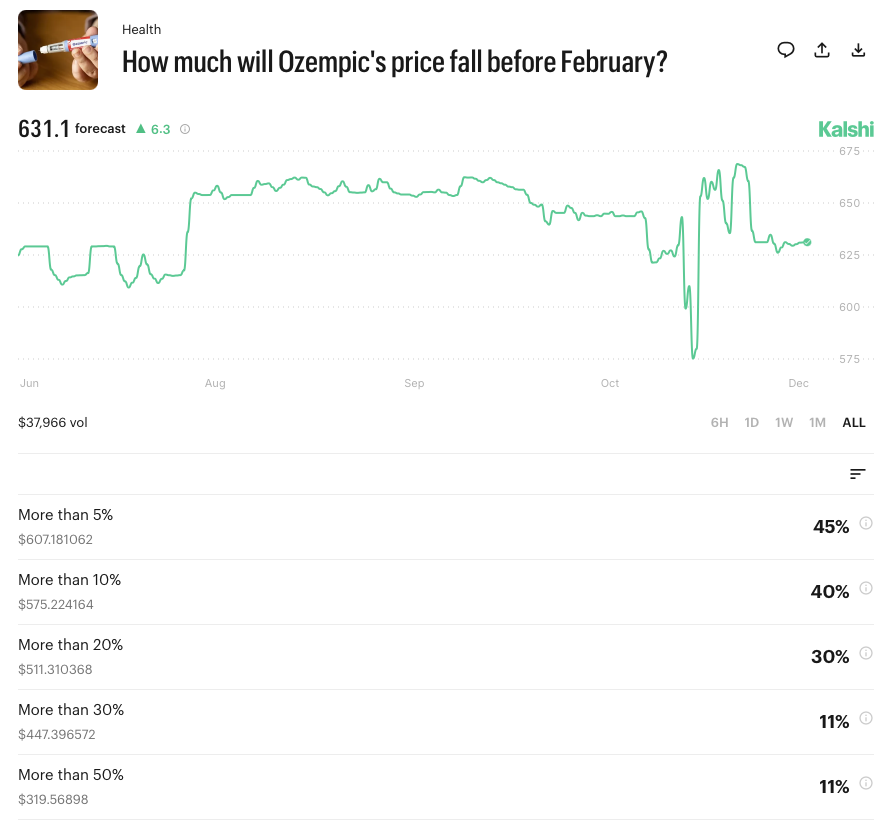

Novo Nordisk built the category - Ozempic has been Canada's best-selling prescription drug for four consecutive years. But Eli Lilly has seized the momentum. This is a common phenomenon of Schumpeterian duopoly markets - the incumbent is disrupted by a firm that's able to innovate and improve the consumer experience. Eli Lily's tirzepatide molecule (Mounjaro, Zepbound) acts on both GLP-1 and GIP receptors, delivering approximately 20% average weight loss versus 14–15% for semaglutide. By Q4 2025, Lilly held 60.5% of U.S. GLP-1 prescriptions and guided 2026 revenues to $80–83 billion USD - 25% growth. Novo, by contrast, guided to its first revenue decline in a decade. The competitive landscape is broadening, with Roche, Viking Therapeutics, Pfizer, and Amgen all advancing programs, intensifying the race for next-generation oral formulations.

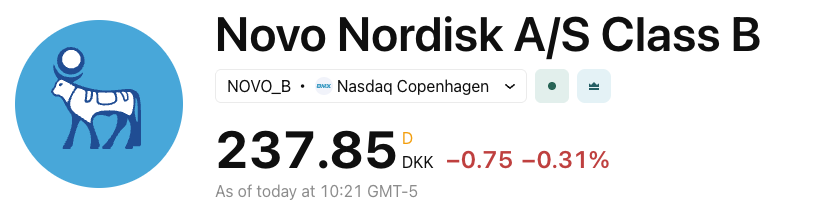

| Novo Nordisk Stock chart, February | |

On February 4th, Novo Nordisk shares fell sharply, declining approximately 15% in a single trading session. The selloff followed an after-market announcement on February 3rd in which the company warned that its 2026 sales and profits are expected to decline year over year due to intensifying pricing pressure, increased competition, and upcoming patent expirations.

On February 23rd Novo saw another significant decline tied to news that its next-generation weight-loss drug, CagriSema failed to achieve non-inferiority in a major clinical trial, which meant it fell short of Eli Lilly's competing tirzepatide products.

In a duopoly market such as this one, where the patent regime pushes companies to compete on formula, method and regimens, firms don't compete on prices. Competitive advantages come from clinical trial success and innovating to improve the customer experience. As Novo continues to fall short on their R&D pipeline and patents expire, expect to see more competition, lower prices and lower margins for the legacy firm.

| | | |

Pharma Giants Bet on Next-Generation GLP-1 Treatments to Sustain Growth

S&P Global Intelligence

March 26, 2025

Read the Article

| | | |

The Ecosystem: Producers, Payers, Pharmacies, and Patients

The GLP-1 value chain involves stakeholders with often competing interests. Manufacturers negotiate net prices with insurers, pharmacy benefit managers, and government health plans - well below list prices. In the U.S., a November 2025 federal deal brought branded GLP-1 prices for Medicare patients down to approximately $245–$299/month, with obesity coverage now in effect as of January 1, 2026

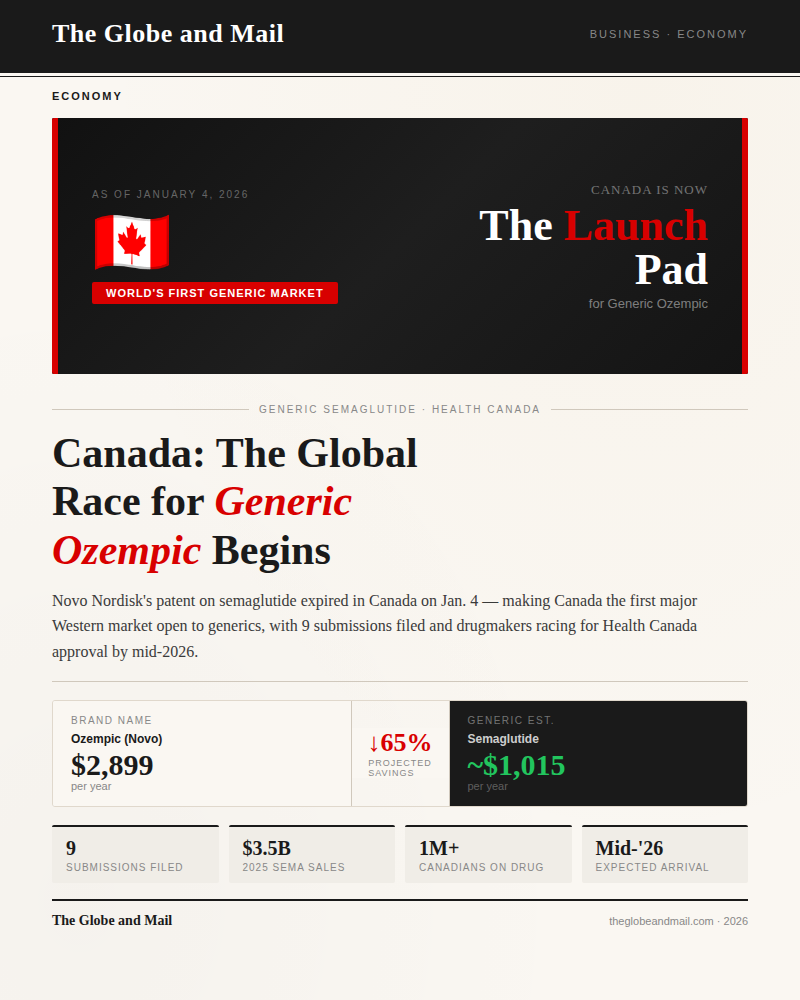

In Canada, the dynamic is distinct and particularly relevant for domestic investors. On January 4, 2026, Novo Nordisk's Canadian patent protection for semaglutide expired - potentially making Canada the first country in the world to offer generic Ozempic and Wegovy. Nine manufacturers, including Sandoz Canada, Apotex, and Teva Canada, have filed with Health Canada, with generic approvals expected in mid-to-late 2026 at an estimated $100–$150/month, versus the $200–$400 Canadians currently pay out of pocket. Lilly's tirzepatide patents remain intact, insulating it from this pressure. Insurance coverage for GLP-1s in Canada remains largely restricted to type 2 diabetes, with private insurers under growing pressure to expand coverage for obesity.

| | | |

Canada will be the launching pad in the global race for generic Ozempic

The Globe and Mail

January 30, 2026

Read the Article

| | | |

Key Events : Next 6 to 12 Months

-

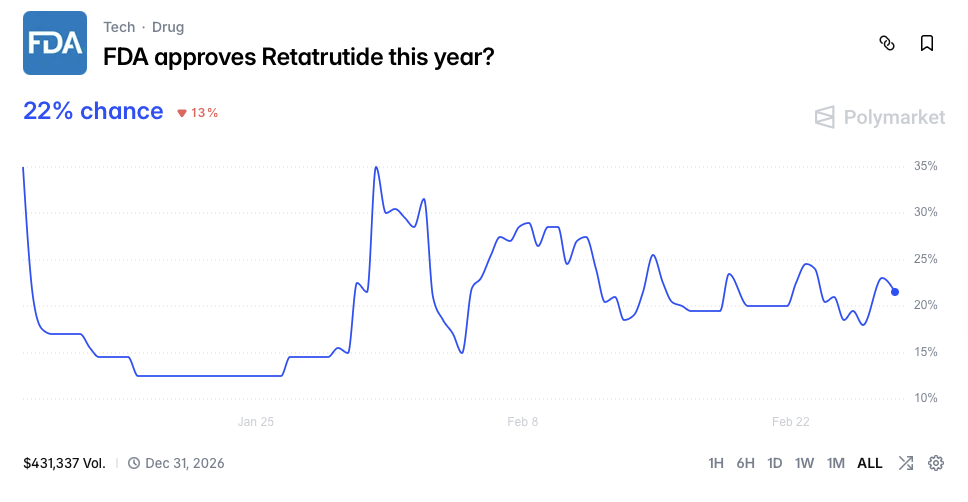

Q2 2026 - when Eli Lilly is expected to receive FDA approval for their new oral obesity drug, orforgilpron, making it the first major manufacturer of an oral obesity drug.

-

Mid-Year - when the first generic semaglutide drugs could be approved, triggering a spike in prescription volumes as costs fall.

Catalysts

- Over 3 million Canadian and over 40 million Americans (1 in 8) have been diagnosed with type 2 diabetes

- Growing prevalence of cardiovascular disease and weight morbidity

- Ageing populations and the associated growing public health burden

- Increasing consumer healthcare and lifestyle applications

What Investors Should Know

The GLP-1 wave is structural, not cyclical - but selectivity matters. The Lilly/Novo divergence is real and likely to persist, driven by efficacy data, manufacturing scale, and distribution advantages. Canada's generic semaglutide race is worth watching as a test case for how sharply adoption scales when prices drop, with domestic manufacturers like Apotex and Sandoz positioned to benefit. Beyond the two majors, the opportunity set extends to contract manufacturers, specialty pharmacies, and digital health platforms. Risk factors include ongoing government pricing pressure, manufacturing execution challenges, and the eventual threat of broader bio-similar competition.

The sector rewards investors who understand the ecosystem - not just the headline drugs.

| | |

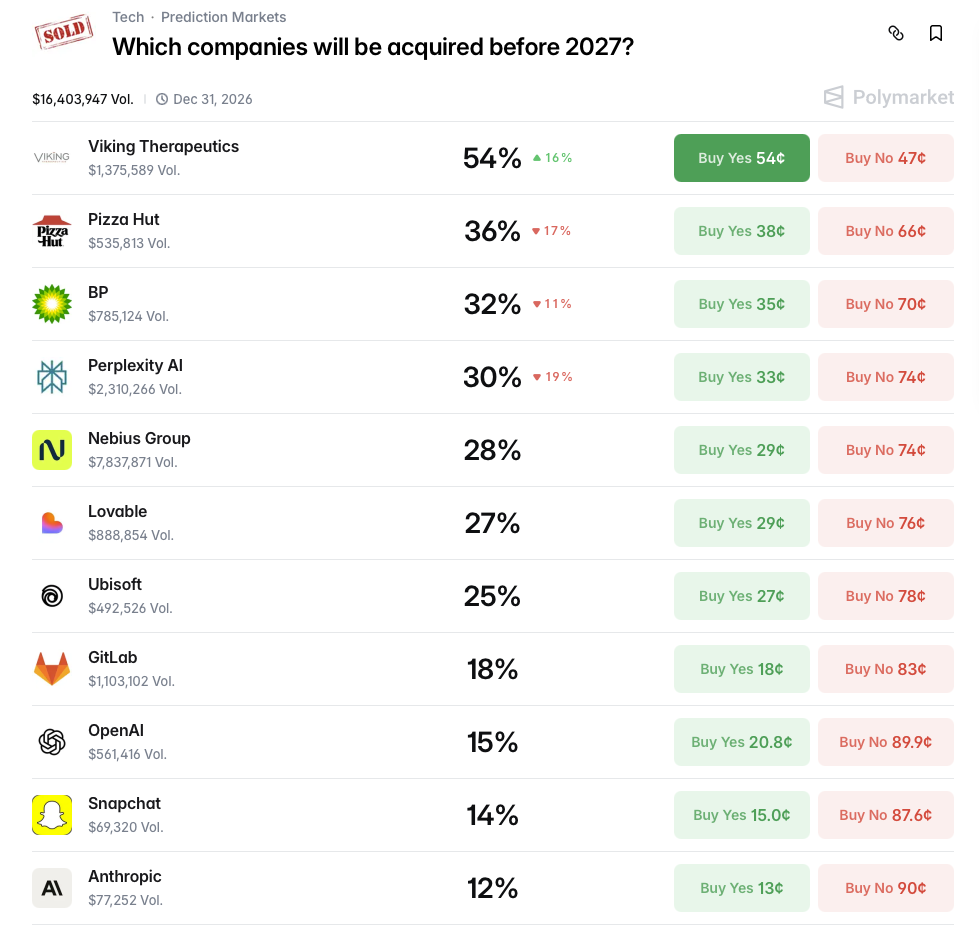

The company with the highest perceived probability of being acquired is Viking Therapeutics, a clinical-stage biopharmaceutical company advancing GLP-1/ GIP receptor agonists for obesity and thyroid hormone receptor beta agonists for lipid disorders.

Further demonstrating the duopolistic realities of the GLP-1 industry.

| | |

Where insight meets opportunity - tailored solutions and strategic guidance to help you navigate the capital markets with confidence. Reply to this email or reach out to Nick at nick@grovecorp.ca to explore how Grove can help your business.

| | From our Grove Departments | | |

Our Company | Contact Us | FAQs | Privacy Policy |

| | | |