|

Over the past several weeks, markets have pulled back across precious metals and copper equities. For many investors, that raises a natural question: is the cycle losing steam?

Our view is clear: this looks far more like a healthy reset within a developing bull market than the end of one.

A Necessary Pause in a Rising Market

Commodity cycles are never linear - and history is consistent on this point.

- During the 2001–2011 gold bull market, corrections of ~15-20% occurred regularly before prices continued higher

- In the 1970s cycle, gold experienced multiple drawdowns exceeding 20%, including a ~47% pullback - yet still delivered one of the strongest runs in history

These pullbacks tend to occur as:

- speculative capital exits after sharp rallies

- macro or liquidity events force short-term selling

- positioning and leverage reset

Importantly, these phases have historically reinforced - not broken - longer-term trends, allowing markets to consolidate before the next leg higher.

The Structural Case Has Only Strengthened

What matters most is not short-term price action, but whether the core drivers of the cycle remain intact.

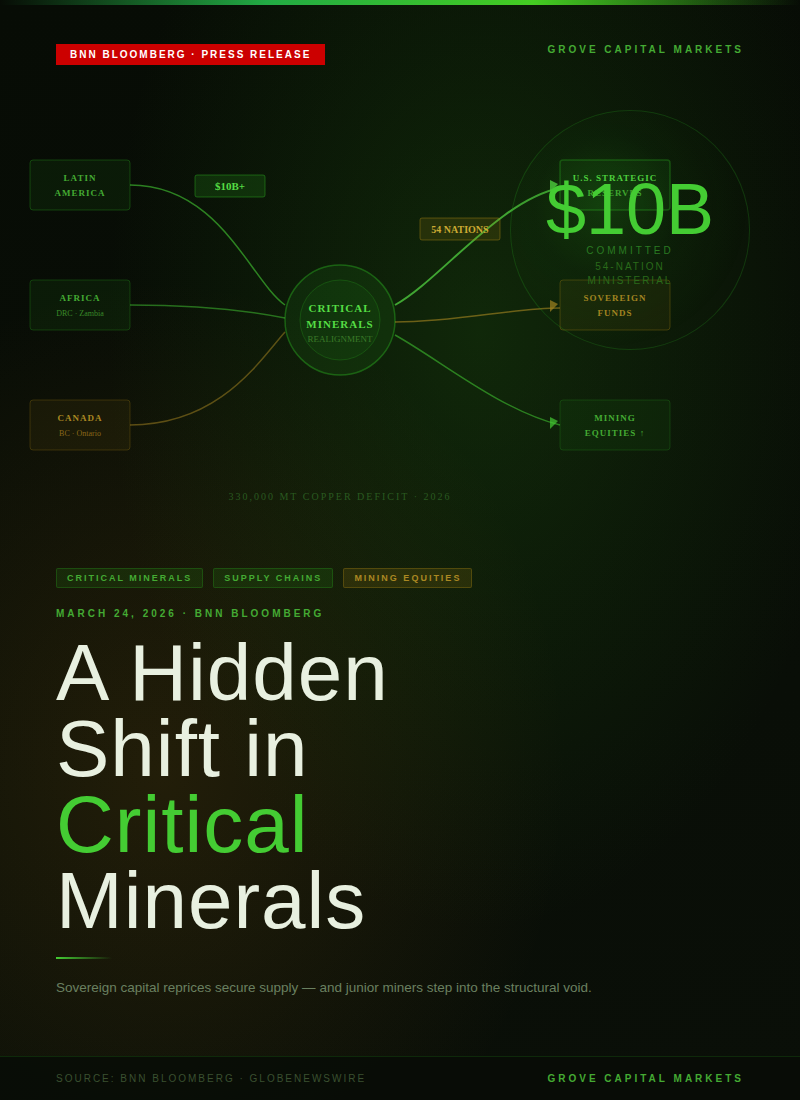

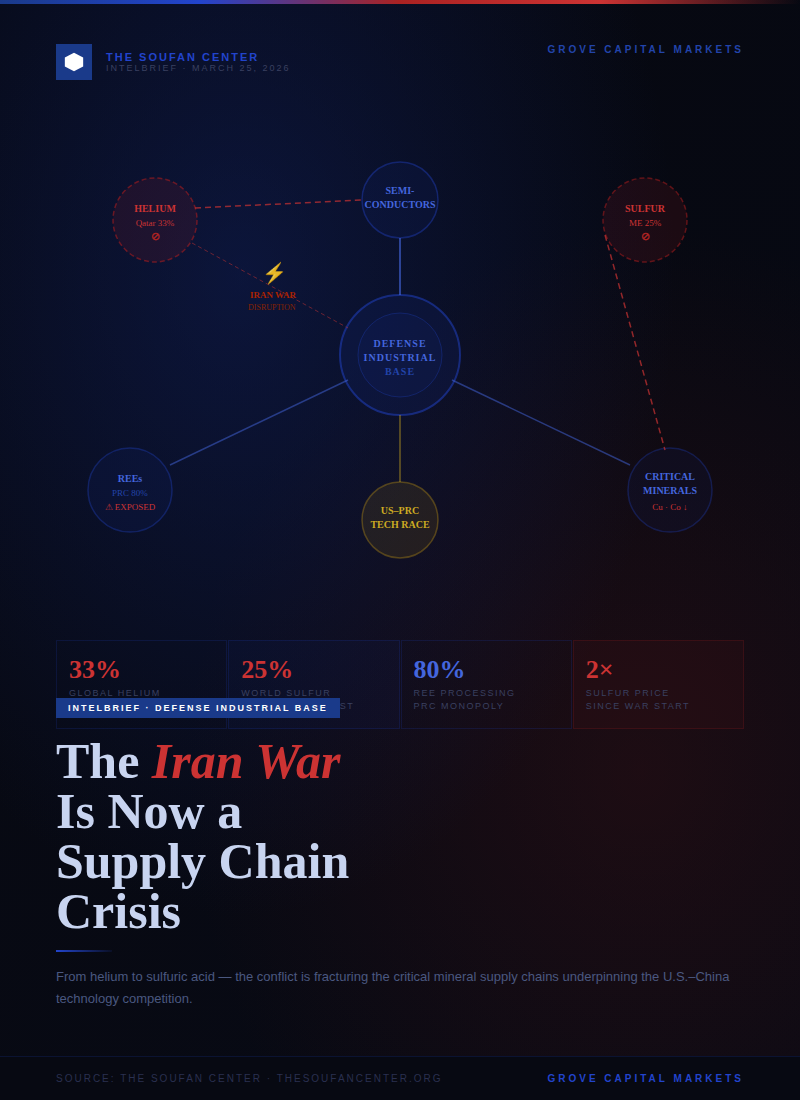

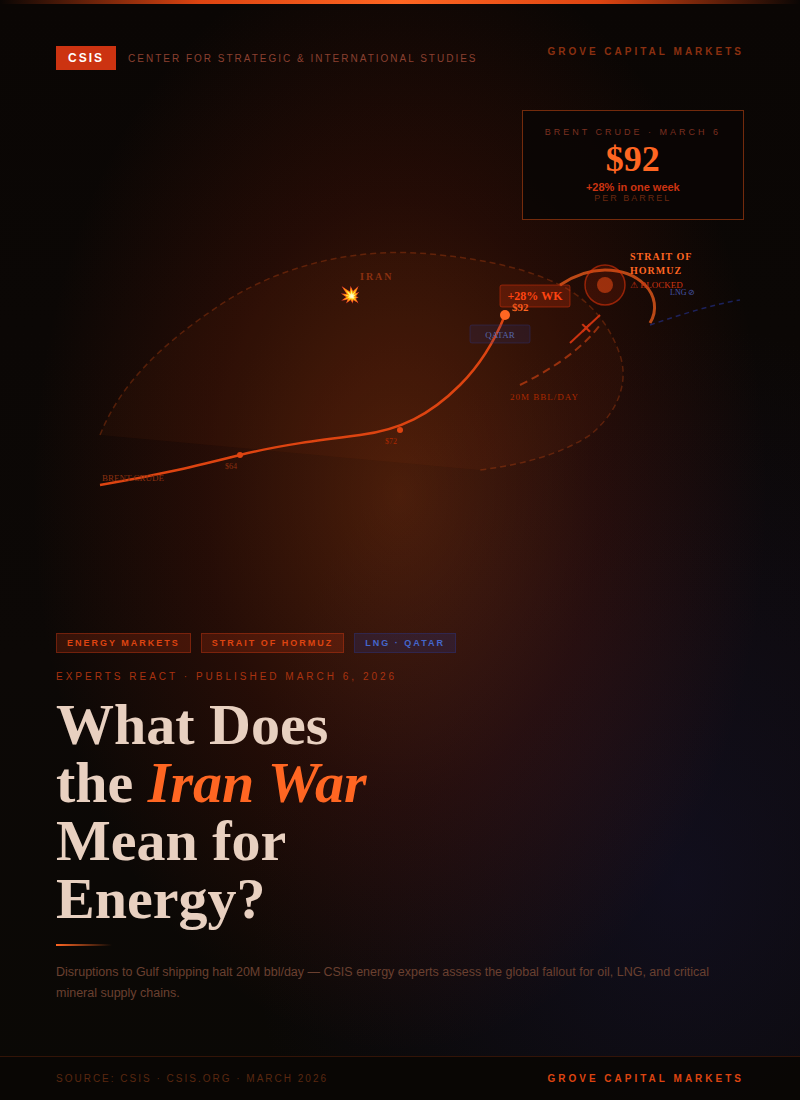

On that front, the picture remains compelling. Supply constraints have not eased, while long-term demand tied to electrification, infrastructure, and strategic resource security continues to build. At the same time, a backdrop of persistent geopolitical tension and supply chain fragmentation is reinforcing the importance of hard assets.

In short, the fundamentals are not weakening - they’re becoming more pronounced.

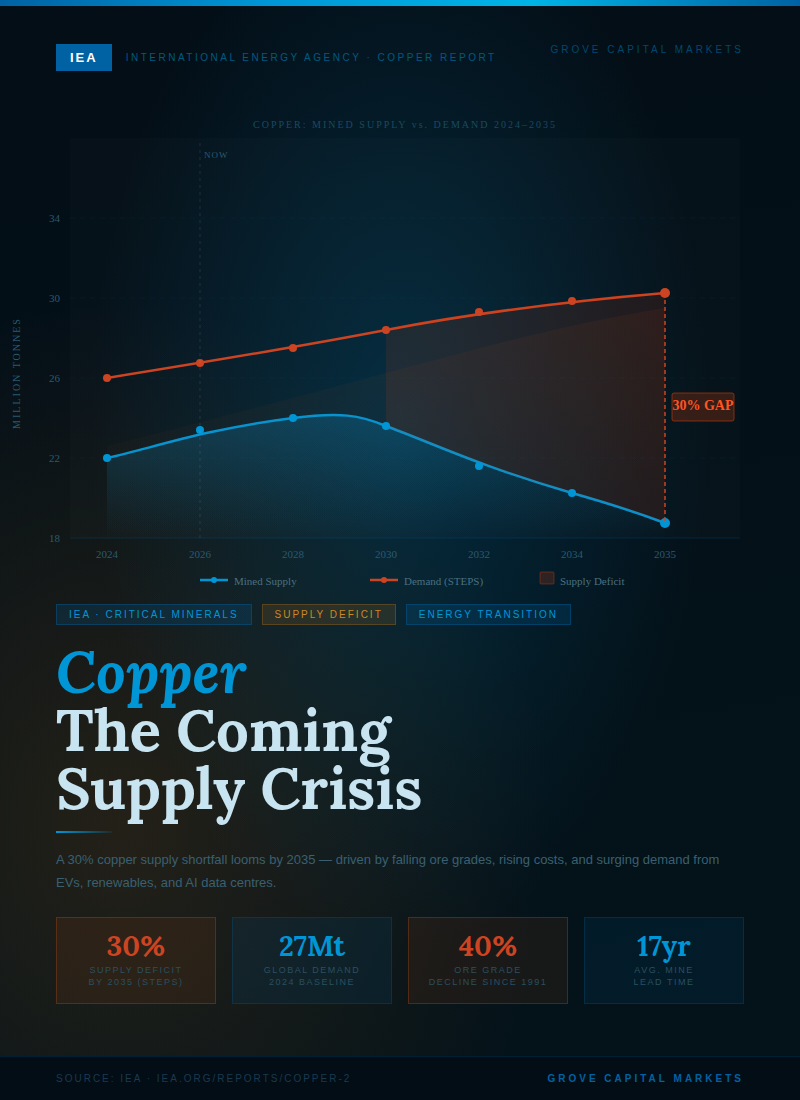

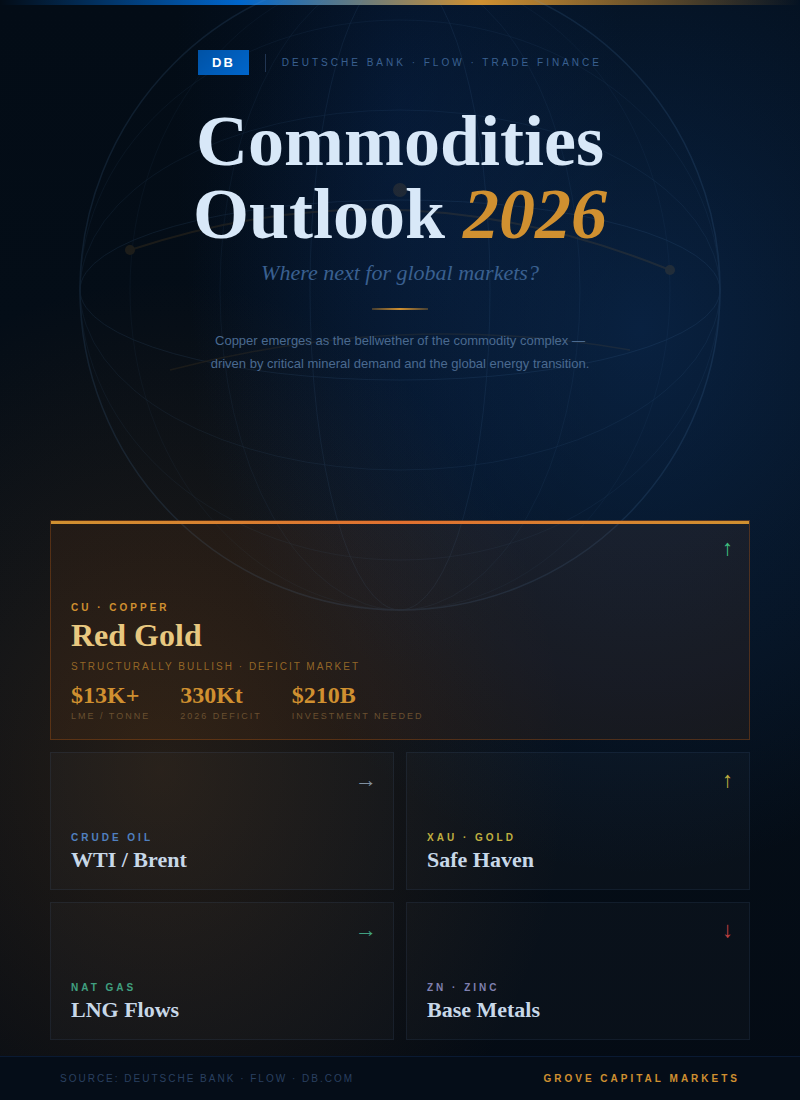

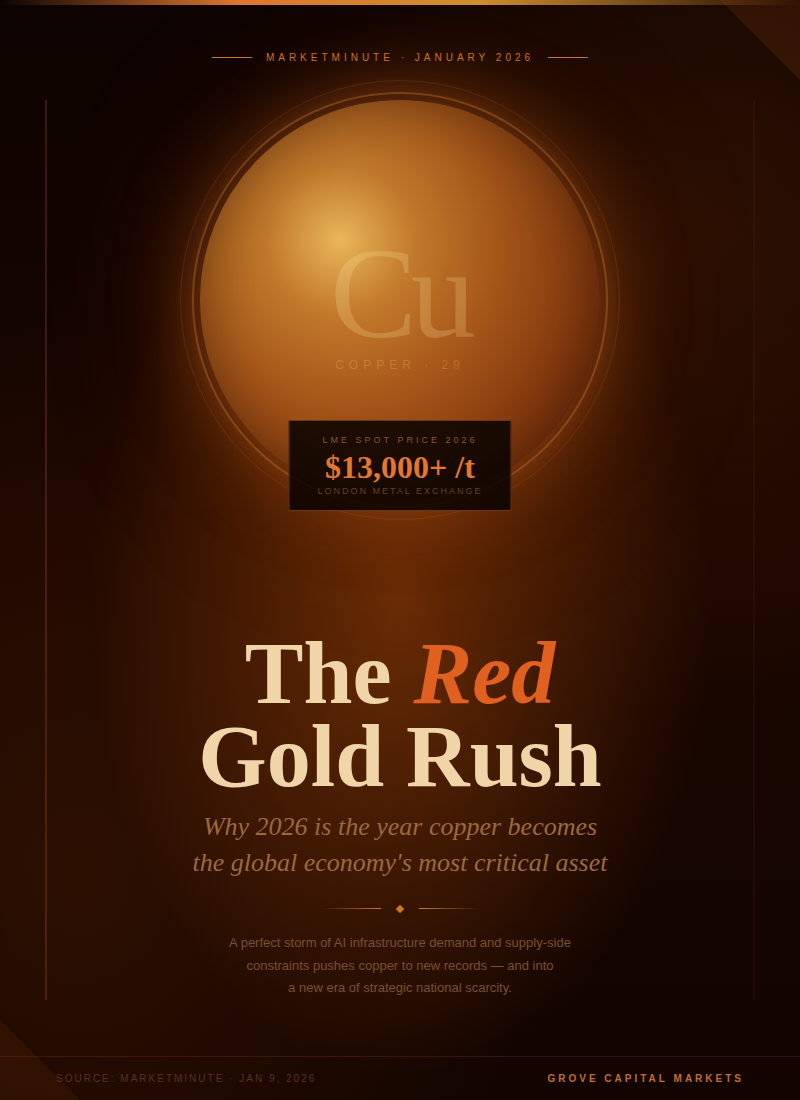

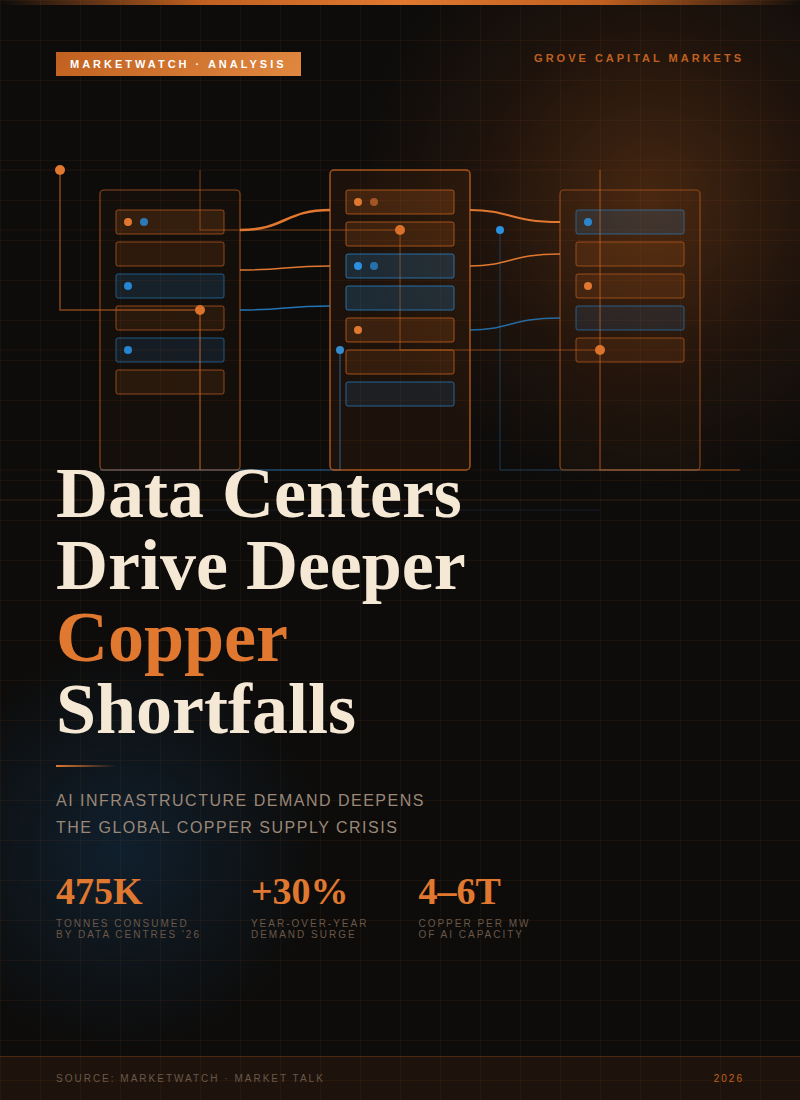

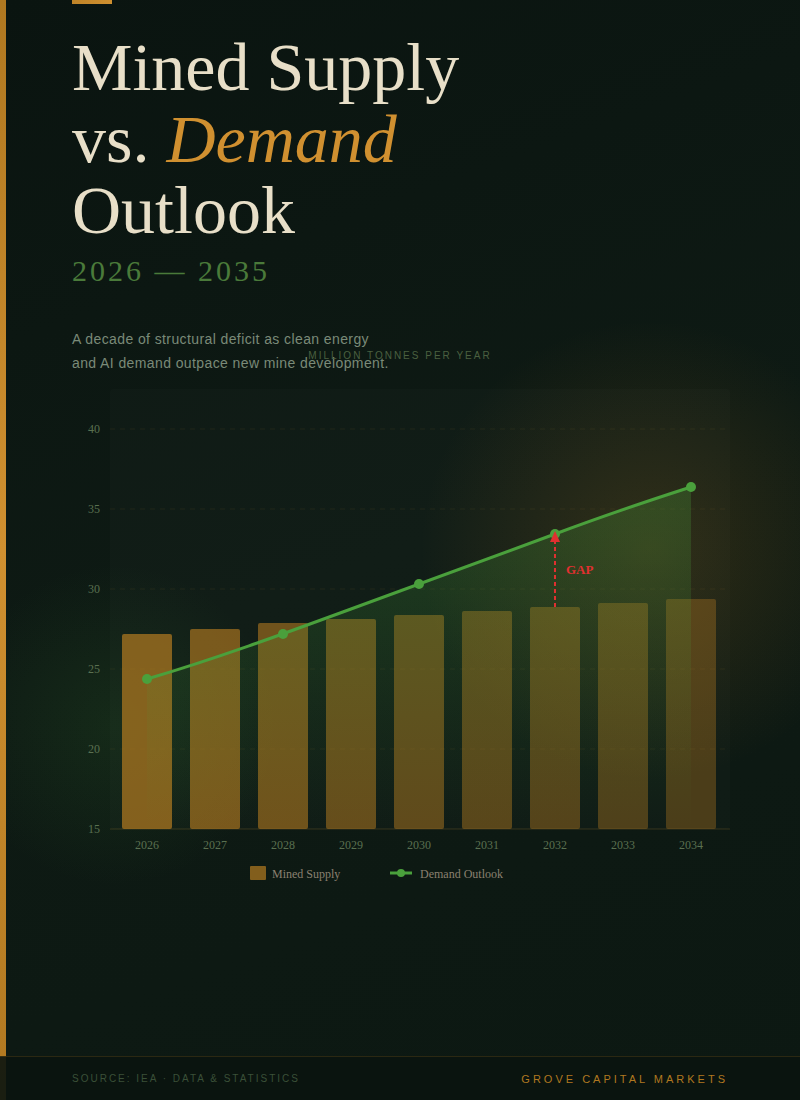

1. Copper: A Structural Deficit Story

Copper remains one of the clearest long-term supply-demand imbalances in global markets. Demand is being structurally driven higher by electrification, grid expansion, EV adoption, and the buildout of digital and AI infrastructure—and the numbers are increasingly difficult to ignore:

- Global demand is expected to increase by over 40% by 2040

- Meeting that demand may require 80 new mines and more than $250 billion in investment by 2030

- Supply is already falling behind, with deficits now beginning to emerge in 2026 and expected to widen through the remainder of the decade

At the same time, the supply side is becoming more constrained. Declining ore grades, rising capital costs, longer permitting timelines, and increasing geopolitical complexity are all contributing to a slower and more uncertain supply response.

Even more importantly, the timeline to solve this imbalance is measured in decades:

- It takes ~15–17 years on average to bring a new copper project from discovery to production—one of the key reasons capital is gravitating toward brownfield, expansion-stage, and near-term production assets

This means that even if capital flows into the sector today, it will not materially impact supply until well into the next decade.

This is not a short-term imbalance—it’s a multi-decade structural constraint unfolding alongside one of the largest demand expansions the metal has ever seen.

|